According to Bloomberg the commercial real-estate (CRE) crisis is likely to be much, much bigger than what you hear most people talking about—bigger than they want to even think about. Bloomberg states that the collapse in value of CRE as people abandon office and retail space all across the nation plus the diminished value of bank reserves due to Fed tightening, and the higher rates of interest that CRE has to refinance at are likely to cause HUNDREDS of banks to crash.

To give you an example of the scale of troubles in CRE right now, one new study says that, within just four years, fifty percent of the downtown office space in Pittsburg could be empty! That’s halfway to a ghost town. As cities like Pittsburg board up that much office and retail space, more people move out of residential space, and more restaurants go out of business, so the collapse spreads. With the municipal tax base eviscerated, law enforcement reduced to meet caving budgets, and fewer people watching over things, vandalism and other crimes grow. The worse things look and the more dangerous they are, the fewer people want to live or visit until major US cities may start to look like ghost towns of an apocalypse less than a decade from now.

Another example comes from a separate story in today’s news that says the tallest tower in Brooklyn is going into a foreclosure auction. The Brooklyn Tower (see photo above), sometimes called the Eye of Sauron, is 1,066-feet tall (93 stories). So, financially, it is a falling Goliath — one of the largest to be foreclosed on due to the crash in commercial real estate.

Of course, there are always counter forces. Cities don’t want to die, so municipal Governments create bold redevelopment programs. Buildings get repurposed. But all of that is hard to do when the whole city’s tax base is badly damaged, and it is very hard to issue bonds to finance such projects when crashing bonds are right at the center of the problem. In the very least, it requires massive write-downs of rents to attract in new customers and massive write-downs of prices that buildings sell for in order for them to finance. So, the banks go under either way because they absorb those financial losses.

Banks go boom

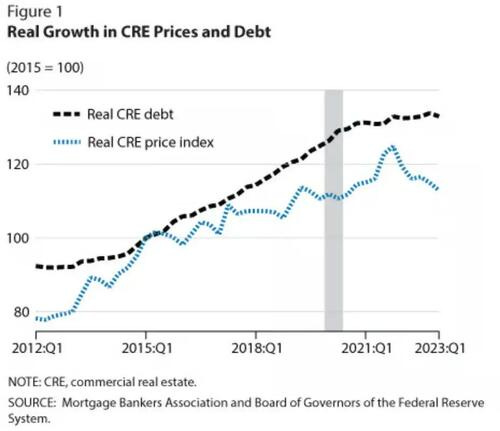

Let’s start with a picture of the growth in amount of debt and the drop in value of the collateral under that debt:

That gives a sense of the extra risk banks are carrying as CRE loans have to refinance or buildings have to be sold.

Since the banking bust of 2023, the Fed, government and FDIC have, in one way or another, bailed out a lot more banks than you ever heard about (through the Bank Term Lending Program, loans and other measures) so that only four banks failed.

Without those government pre-bailouts, one paper last year by researchers at Stanford and Columbia estimated that 1,619 U.S. banks—about a third of them—could be at risk of failure.

Yet, as I’ve pointed out, not much has been repaired. Bank reserves are still about as over-encumbered as they were last March. CRE is more devalued (not something that is fixable on anything but over a very long-term basis), and the Fed is still holding interest rates up until things crash because inflation is stuck. (Another report today (PCE) showed the Fed not getting any further on headline inflation.)

With a trillion dollars rolling over in CRE debt in the remainder of the year, the swell coming in is quite large, and it will build substantially for, at least, another three years after that. The amount is so great because the Fed’s practically free money in recent years enticed a lot of overdevelopment, amplifying the amount of vacancy that is happening due to reasons that didn’t involved the Fed as a prime cause—the government’s forced lockdowns that drove people out of major cities. So, you have a combination of gross overdevelopment and crushing lockdowns that drove away people … coming together like a rogue wave that you get when waves from two different storms meet and pile on top of each other.

We’ve just started into this deluge, and already we saw another regional bank fail in NYC, though it got saved by investors swooping in to grab bargain shares. Delinquency rates are already up by a third this year. Cutting interest rates would certainly help those who need to refinance and would shore up bank reserves that have lost value.

Could Bloomberg be right about the scale of banks that could topple? Is that the number Powell had in mind when he told congress this month that “Some banks will fail” due to the CRE problem? Just what is the size of “some?” Is this why he seems a bit eager to believe that January’s big rise in inflation, which he described again today as a major increase, is just transitory? Is he hoping he can cut before this house of cards starts falling?

Bloomberg even commented that those who called this problem “manageable” may regret doing so. “Those” would be J. Powell, who said that to congress. “Those people” may regret it like “they” regret calling inflation “transitory.” Of course, once Powell says it, everyone else in the mainstream financial media parrots it, so “those” becomes the right word to use about one hour after it originated with just one man.

You risk looking like you are a negligent failure at management when a problem you said was manageable develops into a catastrophe. It’s like when your son tells you there was a small fire on the kitchen stove, but he managed the situation so there is nothing to worry about. Then you find out, when you arrive home, that the fire did not stay well under management, and the house is now gone.

I see a cascade building. If just a few cards fall, the whole house may start to come down as credit seizes up when banks start to run scared of CRE loans, greatly exacerbating the problem companies and individuals will have refinancing in terms of cost and availability of refinancing options. Depositors will run if the momentum of collapse builds, and all of the above unfolds.

Based on Bloomberg’s structural analysis of the situation, failure of this house of cards is not an unlikely scenario.

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!