A brief sector review

While I hold a special place (in my thoughts and in NFTRH) for the gold stock sector due to its counter-cyclical nature, it’s a big market out there and a strategic view of the macro helps with successful positioning. Following is a snapshot of some sectors/markets with general thoughts on each. I will provide one chart or graphic for each but not mark them up or get into too much technical or fundamental detail. There’s a weekend report for all of that stuff. For now, a brief review.

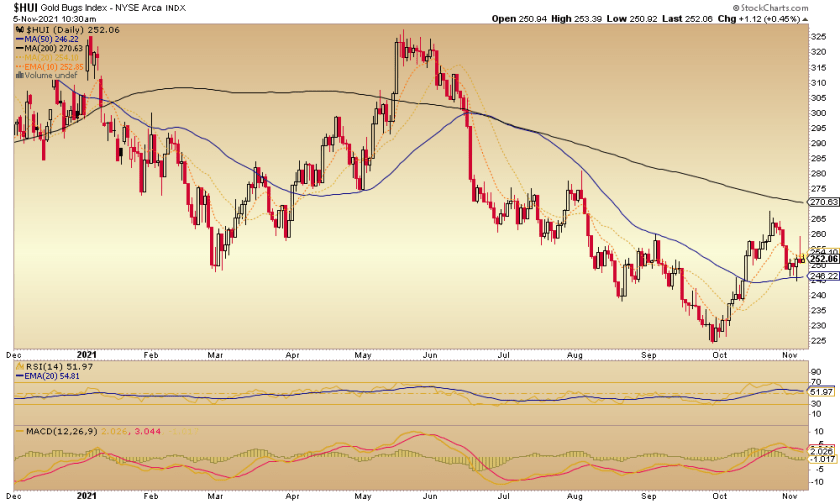

Gold/Silver Mining & Royalty

Gold miners have been fundamentally impaired by the inflationary macro as costs (energy, materials, humans) have outpaced product (gold) for well over a year. As with other markets/sectors, sentiment became overdone to the downside in September and from there (one of our key downside support targets at 230) we projected a bounce and with some stops and starts, the rally logically began.

I have now seen an Inverted H&S (bullish) show up among gold stock ‘analysts’ (code for ‘obsessives’ if all they manage are gold stocks amid a field of many sectors that are actually working). We projected a pre-FOMC pullback to the SMA 50, which would be the healthiest thing to do during FOMC week and that is what Huey has done. The H&S potential lives although the trends are down.

Bottom Line: Gold stocks are and have been trending down (ref. the 50 and especially 200 day moving averages) but can be on watch for a real rally (as opposed to bounce) to break the downtrend. That is because this is a sector on the other side of the cyclical inflation and when that starts to fail (disinflation) or morph (stagflation) the miners could start to gain fundamental tailwinds. For now, a bounce lives and I hold several gold stocks, some for said bounce and a very few as ‘core’.

Semiconductors

My favorite sector due to the implications of this graphic from SIA (included in the September 26 edition of NFTRH along with a special segment on the Semis)…

From medical devices to military to autos, gaming, cryptos and AI, the Semi sector is no longer as violently cyclical as it was when it was PCs (and later, smart phones) or bust. Semiconductors are everywhere, including in the minds of the lunatic fringe, inside our bodies as a Trojan Horse compliments of COVID vaccines. But I jest. Surely nobody actually believes that.

The 2021 play in Semis has been the Semi Equipment stocks first. There is a group of four that I consider the premier equipment stocks and I hold all of them. But eventually the COVID related supply chain problems are going to resolve and the wealth will spread out to the chip makers and picks and shovels (test equipment, materials, etc.). In fact, if this earnings season is a good guide, that wealth has already started to spread. I’ve positioned in several of these items with a few left out there on the vine for consideration.

Doomers can gloom all they want, but the Semis aren’t going anywhere. Not unless society itself dissolves into a real life version of the Walking Dead (which, after years of my wife telling me I have got to watch, I’ve been binging like nobody’s business lately). This once highly cyclical sector is now intimately woven into most economic areas.

The SOX index has blasted to new all-time highs and to boot, has started to reassert leadership to Tech (NDX) and the broad market (SPX).

Cannabis MSOs (US multi-state operators)

We all know the legislative changes that came about in 2020, with more states granting less restrictive and even non-restrictive (beyond medical) access to Pot. My personal view is that if alcohol is legal, why not pot? If pot is illegal, outlaw booze as well. After all, a pot head is a lot less likely to incite or inflict violence due to the munchies than someone with all inhibitions stripped away by too many shots of Southern Comfort.

The MSOs are growing and the rationale I’ve seen for the painful 2021 correction is that legislation has not moved to the degree foreseen by investors in 2020. First of all, they were generally not investors; they were momentum freaks. The sector is taking a well earned cool down and while we are managing the correction (and opportunity) in several MSOs each week in NFTRH, the correction persists. I have started positions in a few MSOs, but there are still support levels lower within an ongoing big picture bullish technical situation.

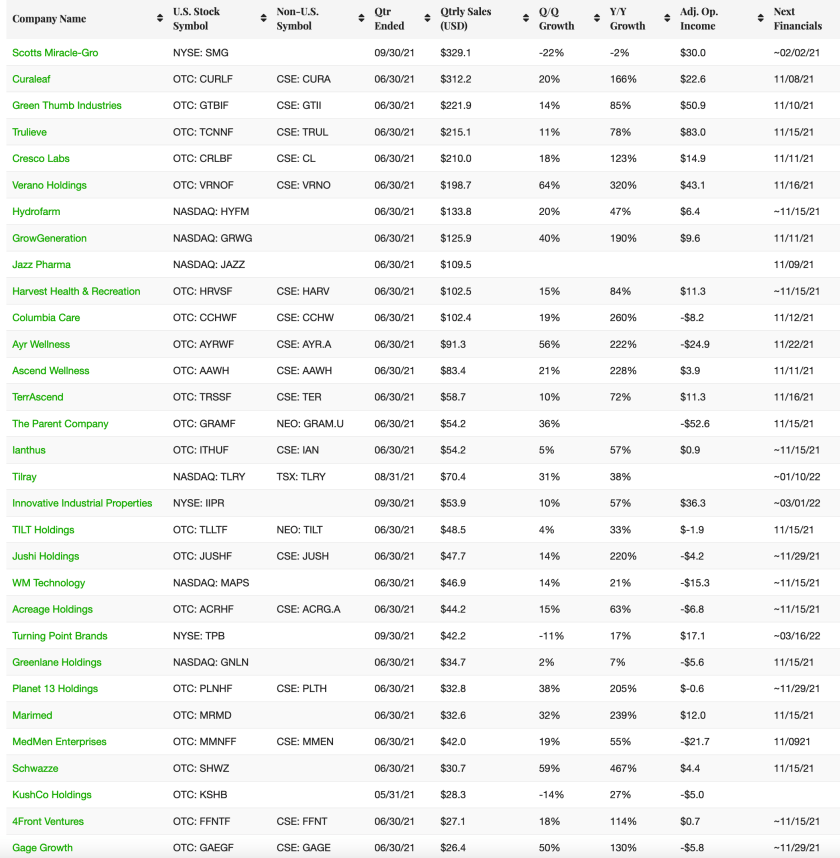

To a degree, I think the MSOs are getting caught up with the correction in the Canadian Cannabis companies, on which I am not as positive. But sooner or later, the fundamentals are going to percolate to the surface in the MSOs. We’ll continue managing by the charts in NFTRH. Meanwhile, this website has some handy information on the whole of the segment, US and Canada alike, including this Revenue & Income tracker.

Commodities

Ah, the vast collection of materials and resources known as commodities. From the headliners like crude oil and copper to the outliers like uranium and lithium, we cover them all extensively each week in NFTRH (as long as the inflation trades are ‘on’ at least). They power our vehicles and grids, provide the skeletal bones to our homes and buildings, our nourishment and thus, life itself.

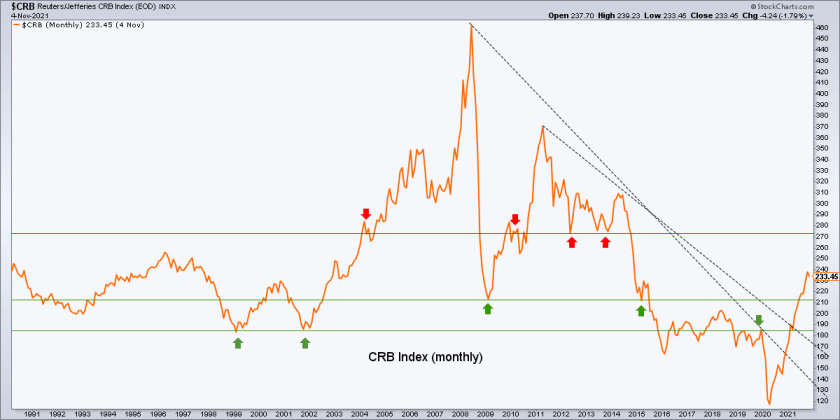

My favored sub-sector is Agriculture simply because it has gained the least hype (ref. oil/gas, copper, lithium, etc.) in 2021, and the Ag index has the chart to prove it. Moderate, but still bullish. There are too many sub-sectors in the commodity complex for this article, so let’s just note that with the revival of inflation expectations per this morning’s post the CRB index is still targeting the 270+ level per this big picture monthly chart included most weeks in NFTRH.

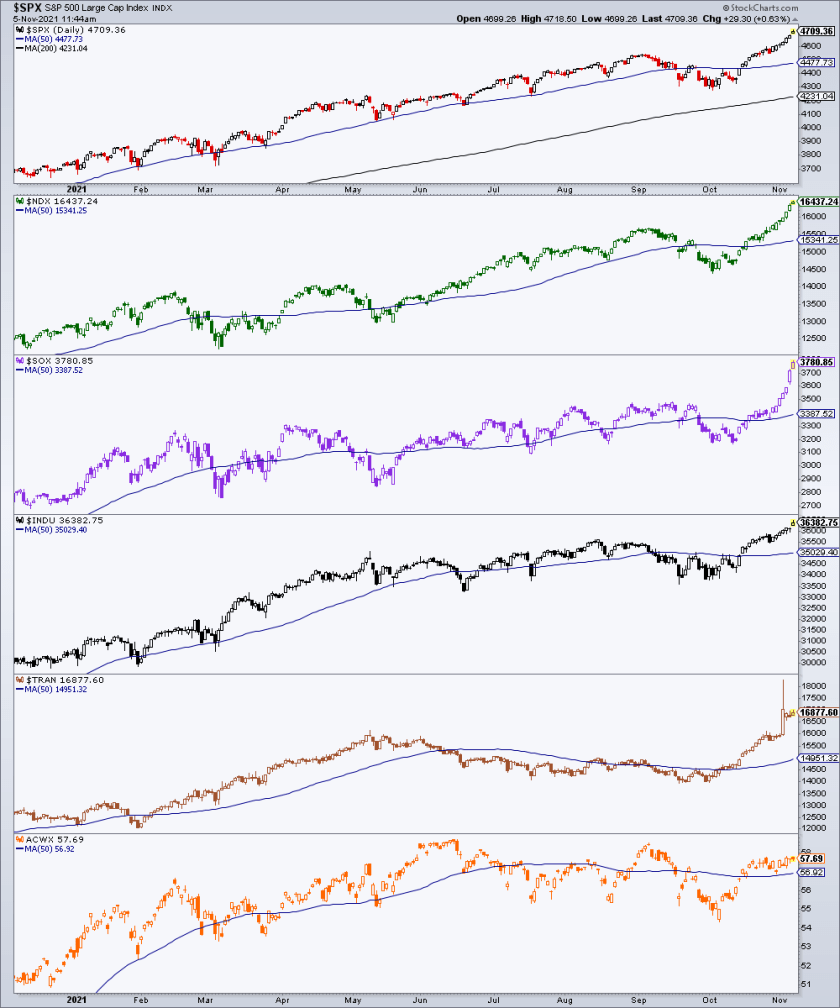

Some of the Rest

As the Fed pretends to be pivoting hawkish, making a slight alteration to its inflationary policies, the market simply laughed it off and bought the news, as we had anticipated last weekend in NFTRH 679. Unlike recently dropping inflation expectations, the stock market Good Ship Lollipop continued apace into and through FOMC. A few reflation-sensitive sectors took a brief pause but that was about it.

Here we find US indexes (SPX, NDX, SOX, DJIA and its Dow Theorizing fellow, the Transports) all at varying flavors of bullish. The World (ex-US) in the bottom panel is bull biased as we have noted weekly in NFTRH lately the mixed bag (bullish, bearish and potentially topping) that is the world at this time.

This bullishness comes amid a resumption of the US stock market’s structurally over-bullish sentiment profile after September’s much needed correction in price and therefore, sentiment. It also comes at what is on average a seasonally firm time of year.

So at the very least my bearish friends, gold stock and/or commodity obsessives, realize that the Armageddon touted to you in 2020 and every step of the way since by perma-bears (hello Zero Hedge) is as yet proving hard to come by as Garth, Wayne and those of us rationally tracking and managing the market party on. *

* No, I have not gone perma-bull. I am fully aware that this is another manifestation of the central bank liquidity orgy as (funny) munny units printed to denominate asset prices, by definition, make those prices go up. It’s supply (currency) vs. demand (goods & services). But it is also reality for now (and since Q1 2020).

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by PayPal or credit card using a button on the right sidebar (if using a mobile device you may need to scroll down). Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.

About the author