When you have a Debt Black Hole, it warps everything in the economy.

Global debt is at record high levels. This is a stick of dynamite just waiting for something to light the fuse.

UBS warns that the match could be the AI bubble.

The Swiss bank recently published its worst-case scenario for defaults in the private credit sector, estimating that default rates could surge to 15 percent if AI triggers an “aggressive” disruption among corporate borrowers.

The private credit market refers to non-bank lenders, such as private equity firms, asset managers, and other specialty funds. These institutions lend money directly to companies, providing alternative funding options for companies and individuals.

When an economy becomes overleveraged, there is generally some spark that triggers a meltdown. In the late 1990s, it was the dot-com bubble. In 2008, it was the real estate bubble. Today, we have an AI bubble.

Some might question whether the AI sector constitutes a bubble. While it is debatable, there are some clear parallels to the dot-com era in the mid to late 1990s. At the time, billions of dollars flowed into internet startups just because they were internet startups. This was exacerbated by artificially low interest rates that incentivized risky borrowing. That bubble eventually popped. It was inevitable, because when you borrow billions without a viable business plan, you're likely to get into trouble.

We're seeing similar mania in AI today. According to an MIT study, U.S. businesses have invested between $35 and $40 billion into AI projects, with 95 percent failing to generate any measurable return on investment.

UBS characterized “AI disruption” as a “clearer catalyst” for a credit meltdown.

According to a Bloomberg report, private lenders have significant exposure to potential problems in the AI sector.

“Direct lenders that took a lead role in financing software companies in recent years now look dangerously exposed to AI’s impact, stirring comparisons to the 2008 financial crisis. Some estimates suggest that the firms have 40 percent of all sponsor-backed loans tied up in the software industry.”

Private credit defaults are currently running between 3 and 5 percent, according to the UBS report, and it says there are signs of strain, including interest paid-in-kind (PIK) reaching post-pandemic highs. This means instead of paying interest expense in cash, the borrower adds it to the balance of the loan.

Some prominent figures in the financial world are also sounding alarms.

Money Manager Danny Moses told Bloomberg that an aggressive push by private investment firms into retail products reminds him of the years leading up to the subprime mortgage crisis that triggered the 2008 financial crisis.

In other words, private investment firms are trying to tap new revenue sources by selling products to everyday retail investors, and not just institutions and wealthy insiders. This is similar to what happened in the years leading up to the 2008 financial crisis, when subprime loans were repackaged and sold on the retail market.

The fact that we’re seeing this today implies private markets are seeking new sources of capital as the flow of institutional money slows.

The problem with this scenario is that retail investors generally don’t understand the risks inherent in these complex debt instruments.

JPMorgan Chase CEO Jamie Dimon also warned about the potential for a 2008-style crisis, noting he sees some players in the financial sector “doing dumb things to create NII (net interest income).”

Dimon said he wasn’t sure what would precipitate the next crash, but there is always something looming on the horizon.

“There’s always a surprise in a credit cycle. This time around it might be software because of AI.”

The UBS report warned that fallout from an AI meltdown might not be limited to the private credit market. According to Bloomberg, “The UBS strategists also see higher default risk for U.S. leveraged loans [loans made to companies that already have high levels of debt or weaker credit profiles] of up to 10 percent — and high-yield bonds of up to 6 percent — in a worst-case scenario.”

The private credit market makes up a small percentage of lending, but there is always the risk of contagion, as we saw during the 2008 financial crisis. And there are massive levels of debt.

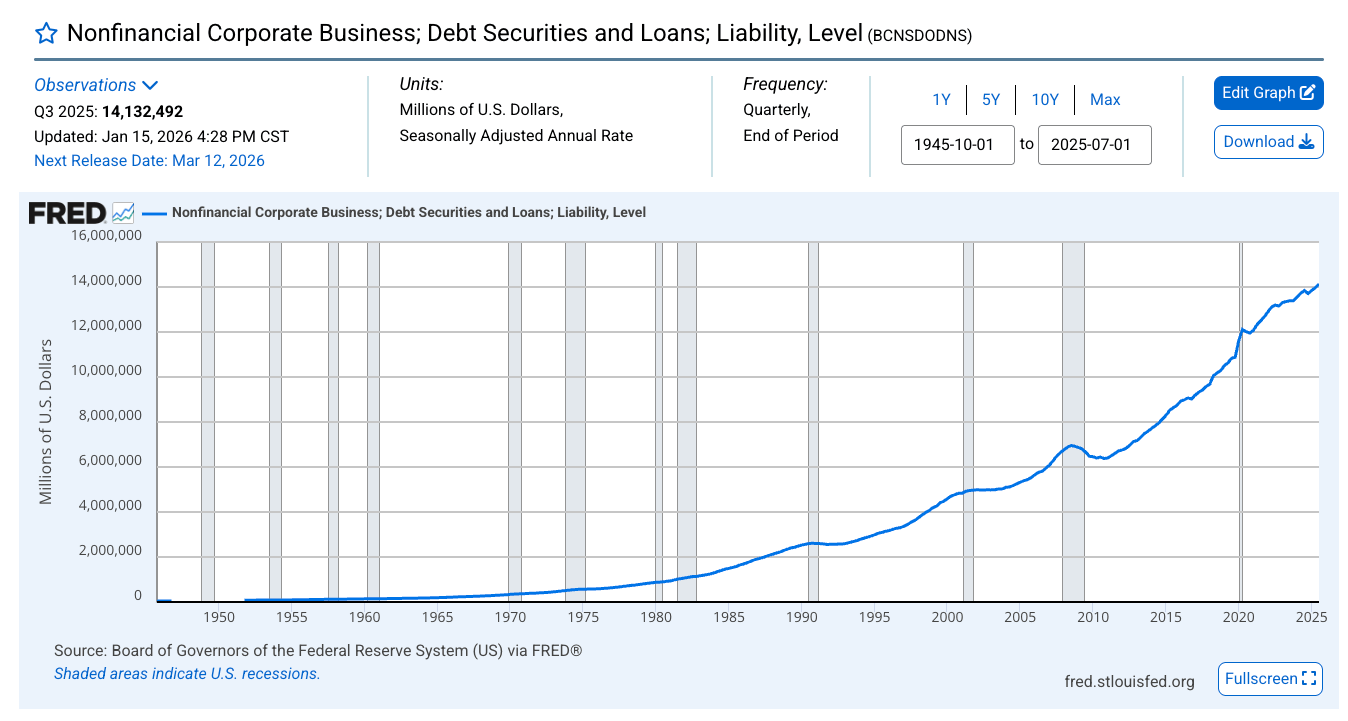

Nonfinancial corporate business debt in the U.S. surged to over $14 trillion in the third quarter of 2025.

This is precisely why so many people are clamoring for interest rate cuts despite price inflation still running above the mythical 2 percent target. A debt-riddled economy can’t function in a normal interest rate environment.

This is precisely why so many people are clamoring for interest rate cuts despite price inflation still running above the mythical 2 percent target. A debt-riddled economy can’t function in a normal interest rate environment.

Of course, lower rates incentivize more borrowing, feeding the Debt Black Hole.

In 2007, most mainstream analysts insisted everything was fine. They said that while the subprime mortgage situation was a problem, it was “contained.” We hear similar sanguine analysis today. As JPMorgan Asset Management global head of fixed income Bob Michele told Bloomberg, leveraged debt markets can keep riding the coattails of a healthy economy with no major blow-ups.

But is this a healthy economy?

The very existence of the Debt Black Hole calls that notion into question.

“What everyone’s worried about is we haven’t had a shake-out in private credit yet,” Michele said. “A recession is that ultimate shake-out.”

About the author