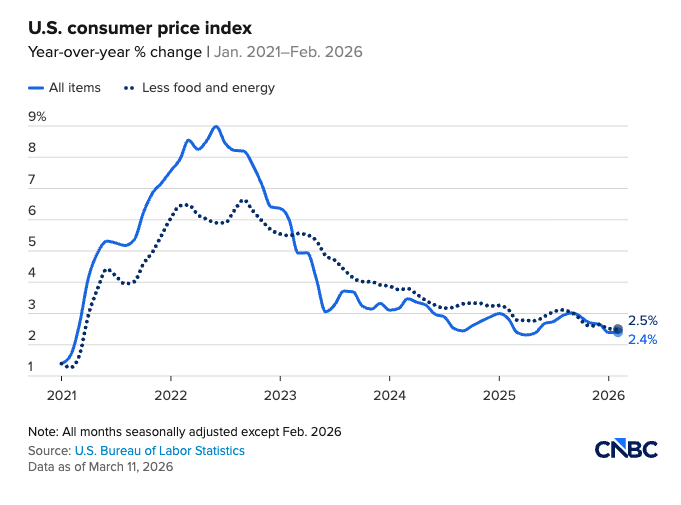

The headline Consumer Price Index was steady in February as inflation continues to rise.

How could this be?

Because the CPI doesn’t measure “inflation” (as properly defined). It simply reflects the price movements of a basket of goods dreamed up by the BLS. Yes, this does give some indication of the trajectory of price inflation. However, price inflation is just one symptom of monetary inflation.

February CPI By the Numbers

Based on the February CPI, one can argue that price inflation is holding steady. However, it remains stubbornly stuck above the Federal Reserve’s mythical 2 percent target.

According to the most recent CPI data released by the BLS, prices rose 2.4 percent over the last 12 months. That was the consensus forecast and identical to the January reading. It was also the same rate the BLS reported in May 2025, the month after President Trump announced his aggressive tariff policy.

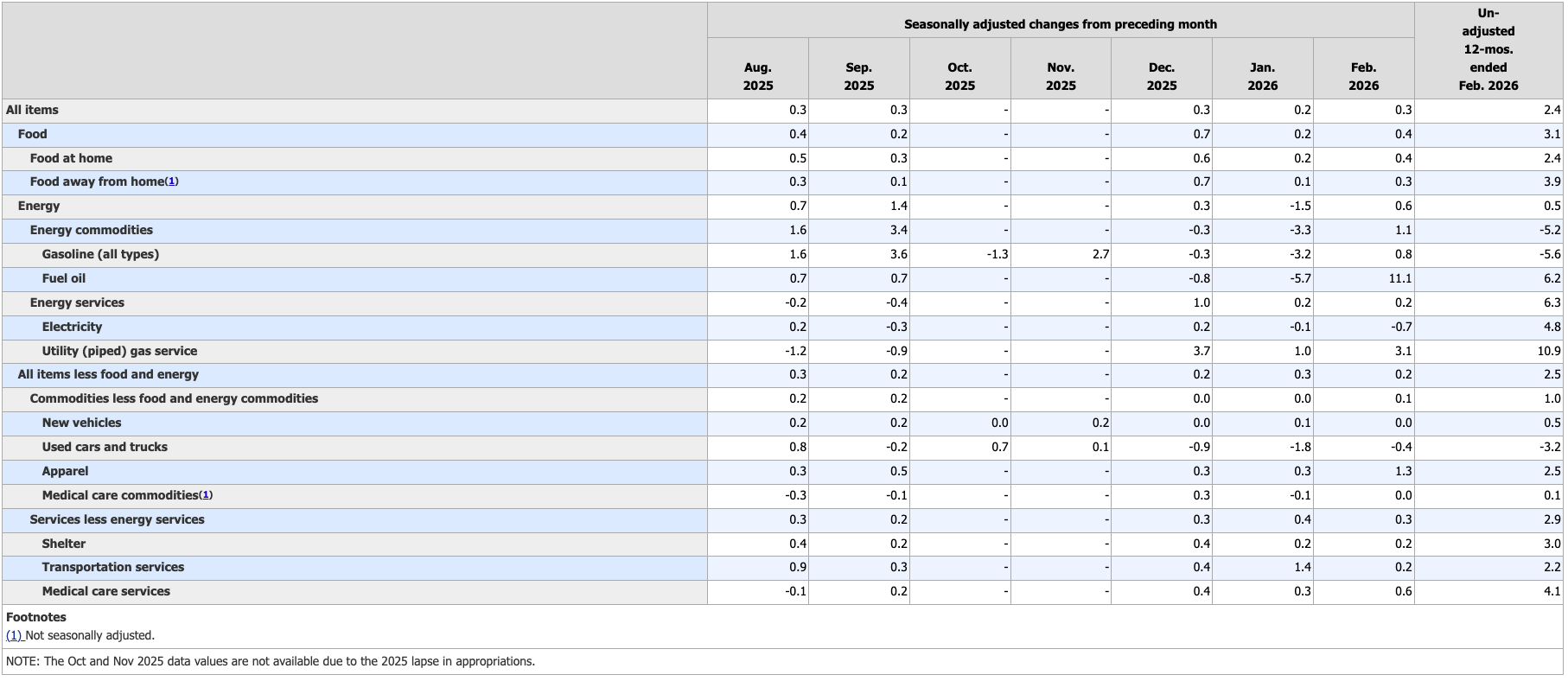

On a monthly basis, price inflation was a little hotter, rising by 0.3 percent.

Stripping out more volatile food and energy prices, core CPI prices cooled modestly, rising 0.2 percent month on month, after a 0.3 percent increase in January.

The annual core CPI held steady at 2.5 percent.

However, over the last six readings (with no October data), core CPI has increased by 0.3, 0.2, 0.2, 0.2, 0.3, and 0.2 percent, annualizing to 2.8 percent. Core CPI has been mired in this range for well over a year.

Looking at the details, rent (a convoluted BLS formula that tells us little about the actual cost of rent in the real world) hit the lowest level (0.1 percent month-on-month) since January 2021. That drove cooling prices in the overall shelter category, which rose by 0.2 percent. Shelter has been one of the biggest CPI drivers over the last several months.

Even as shelter costs moderated (based on the convoluted CPI formula), food prices heated up, rising by 0.4 percent during the month.

Energy prices also nudged up (even before the U.S./Isreal attack on Iran), with gasoline 0.8 percent in February. Even with the boost to gas prices, they are still down over 5 percent compared to the same period in 2025.

Apparel prices jumped sharply. Analysts attributed this to tariff costs.

Service prices continue to run hot, rising by 0.3 percent last month after a 0.4 percent gain in January. On an annual basis, service prices have gone up 2.9 percent.

As I mentioned, any time I report on government CPI data, it’s important to take this (and every) CPI report with a grain of salt. It is still factoring in November data that they basically just made up. And the constant revisions to the labor data should also make you skeptical of government numbers.

You also need to remember that the CPI data understates price inflation by design. The government revised the CPI formula in the 1990s so that it understated the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS used the old formula, we’d be looking at CPI closer to 6 percent. And using an honest formula, it would probably be worse than that.

However, this government data drives decision-making, so we need to pay attention to what it tells us.

CPI May Be Steady, But Inflation Is Heating Up

So, what is the data telling us?

CNBC summed it up like this.

“The annual rates were unchanged from January, indicating that inflation was holding above the Federal Reserve’s 2 percent target but not getting worse.”

However, as I’ve already mentioned, CPI only measures price inflation, one symptom of monetary inflation (which is what economists and pundits used to mean when they talked about inflation).

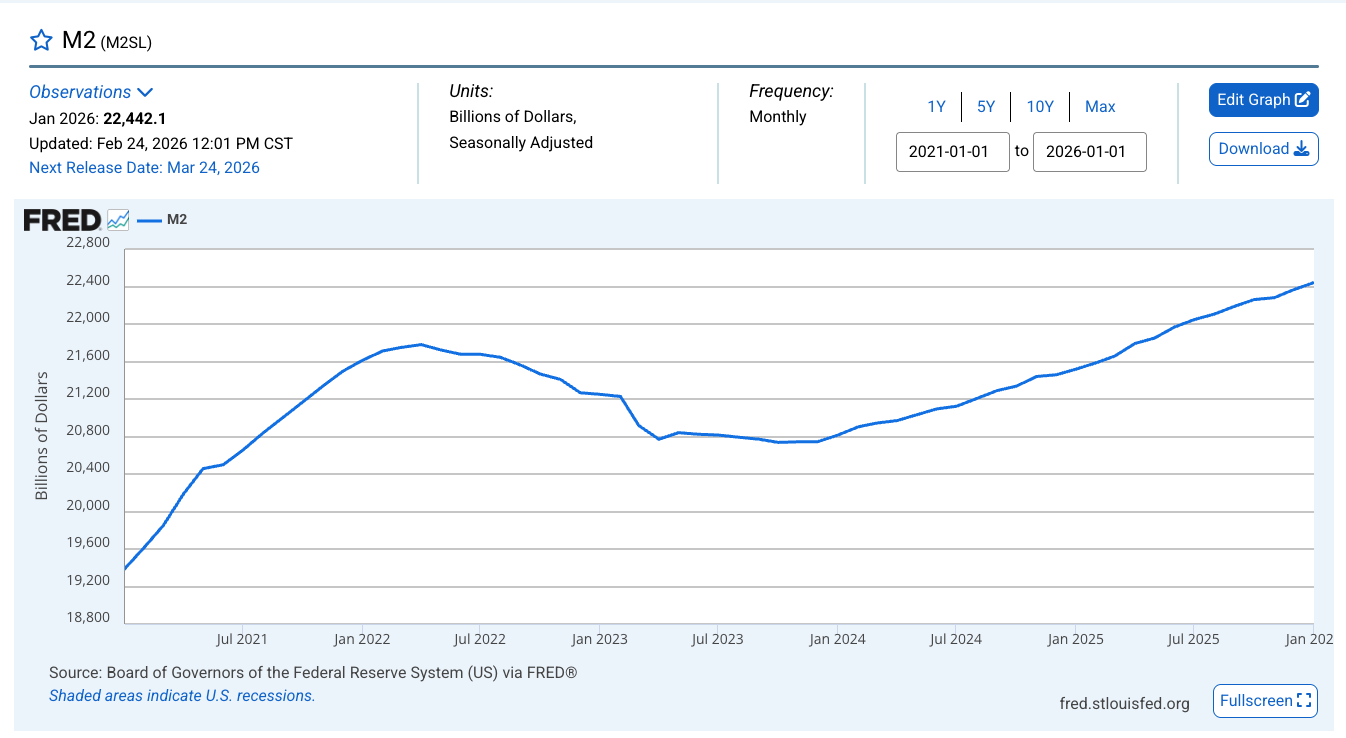

If we look at the money supply, we find that inflation is heating up.

As the Federal Reserve revs up the money-creating machine even higher, the money supply is already growing at the fastest rate since July 2022, in the early stages of the tightening cycle.

After peaking in April 2022, the money supply began to decline as the Fed hiked rates that year. The money supply bottomed in October 2023 and began increasing again. The money supply is now well above the pandemic peak.

And money creation has accelerated over the last several months.

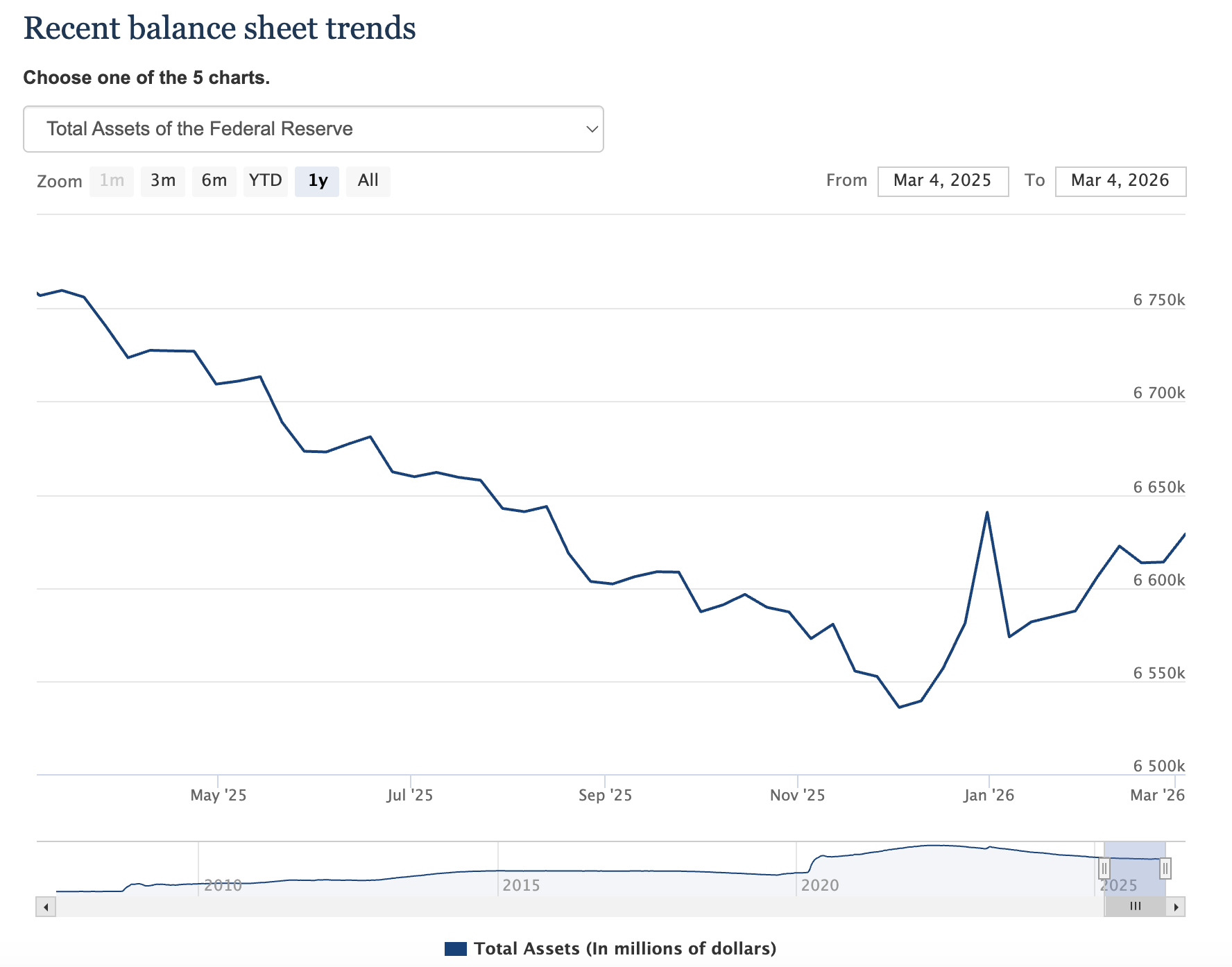

We also know inflationary pressures are increasing because the Federal Reserve is once again expanding its balance sheet.

While you’ll never hear anybody at the Fed utter the term, the central bank relaunched quantitative easing in December. That means they are once again buying U.S. Treasuries using money created out of thin air.

While you’ll never hear anybody at the Fed utter the term, the central bank relaunched quantitative easing in December. That means they are once again buying U.S. Treasuries using money created out of thin air.

Ultimately, this monetary inflation will work its way through the economy. It will either manifest in rising asset prices or rising consumer prices. Ultimately, it is devaluing your money (by design).

War and Inflation

Market reaction to the February CPI data was muted. Everybody is sitting on pins and needles waiting for surging oil prices to show up in the CPI data.

When they do, keep in mind that it’s not “inflation” as technically defined. It is a price shock.

That’s not to say it won’t impact the economy. That’s not to say higher energy costs won’t be passed on through the price of other products. That’s not to say it won’t cause consumer pain. It’s only to say that rising oil prices due to a war are fundamentally different than rising prices due to inflation. It’s important to disambiguate and untangle these phenomena, or you’ll never get a clear understanding of what’s happening in the economy and the financial system.

Because make no mistake – the war will cause inflation – on top of the oil shock.

Analysts say Uncle Sam is spending around $1 billion every day to fight the war. I will remind you that the federal government is broke and is already running massive deficits month after month. The war will widen the budget gap and require more borrowing. The Fed is already running stealth QE to prop up the sagging Treasury market. As the U.S. is required to issue more debt, it is likely the Fed will have to step in even more aggressively because there is no significant demand for U.S. Treasuries, despite geopolitical uncertainty that would historically create a safe-haven bid.

The bottom line is more money-printing.

And that IS by definition inflation.

About the author