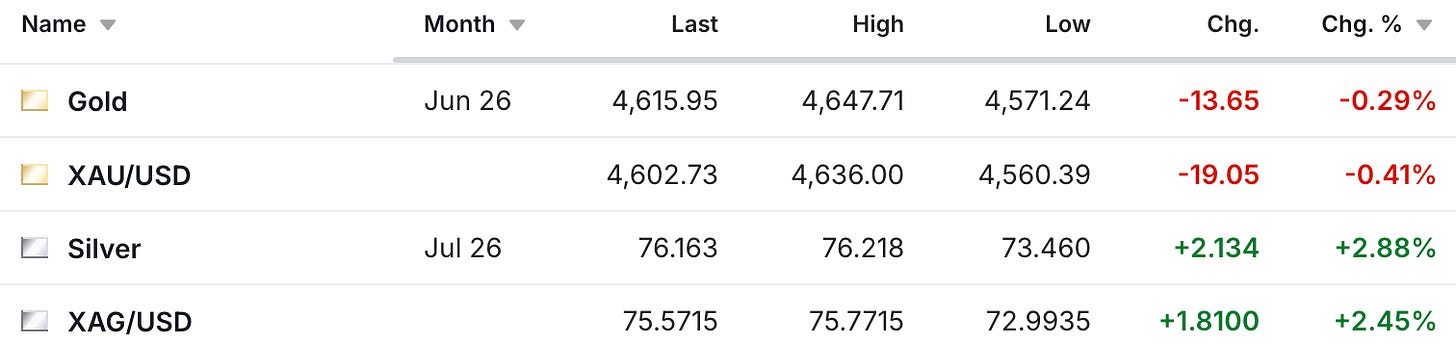

We’re seeing unusual pricing in the precious metals markets on Friday, as the gold futures are basically flat on the day at $4,616, while the silver futures are up $2.13 to $76.15.

CNBC is reporting that the oil price is down on a ‘report’ that Iran is drafting a peace agreement, although I would easily bet on that peace agreement, if it does actually exist, not being accepted by Israel any time soon.

There were some interesting reports from Metals Focus this week about the silver market that shed some insight on everything that’s happened in the past year, and I wanted to go through some of those highlights today.

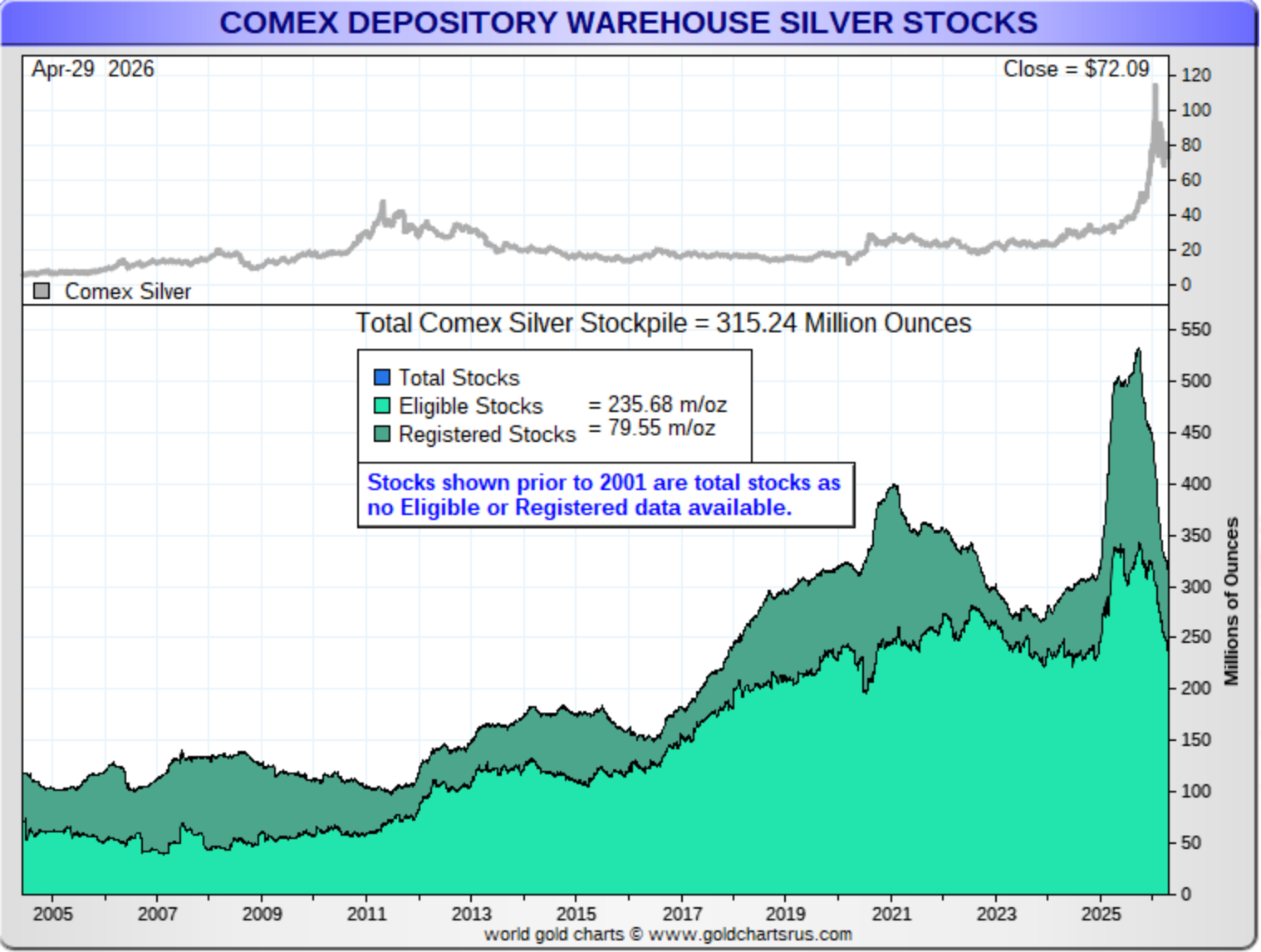

CME inventories fall to pre-Trump 2.0 levels Outflows from CME-approved warehouses have helped to ease supply tightness since late 2025. After peaking at 531.9Moz in October 2025, CME silver inventories have since recorded sustained withdrawals.

At the time of writing, total CME stocks stood at 315.2Moz, levels last seen in November 2024, effectively unwinding all tariff-driven inflows between December 2024 and October 2025.

Here’s the chart of the COMEX silver inventories, and you can see the sharp drop-off in the past half-year.

Obviously, compared to historical levels, there’s still a lot of silver in the COMEX, although we still haven’t seen the decline slow down yet.

That will be one of the key areas of the silver market to keep track of, in terms of how much metal keeps leaving. And as for where it’s going, here’s what Metals Focus had to say about that.

Trade data confirms that much of these CME outflows were redirected abroad. As shown in the chart, US silver bullion exports totalled 95Moz in the first two months of 2026, already exceeding annual totals in most recent years (except 2025’s 144Moz). The UK remained by far the largest destination, accounting for just over half of these exports.

In terms of what’s happened to the London silver market ever since it broke back on October 9 of last year, Metals Focus touched on how things look since they restocked their inventory, largely with silver from the COMEX.

By end-March, Metals Focus’ analysis of ETP and LBMA data indicates that physically backed products accounted for 71% of London inventories, leaving the “free float” at an estimated 253Moz. This marks the highest level since December 2024 and represents an increase of around 116Moz from the trough seen last September. An ongoing deficit make silver vulnerable to a further squeeze

At the time of writing, the physical silver market appears closer to historical norms, as evidenced by a further decline in leasing rates in recent weeks. However, global identifiable inventories remain low compared to levels seen in the early 2020s. More importantly, as highlighted in World Silver Survey 2026, the silver market is expected to remain in a fundamental deficit in 2026, at a level similar to that recorded in 2025.

Interestingly, Metals Focus notes how the silver market does still remain vulnerable to more squeezes.

This would mark the sixth consecutive year of deficit and, combined with elevated ETP holdings and the prospect of improving investor interest later this year, implies a continued cumulative drawdown of stocks. As a result, the market remains vulnerable to periodic liquidity squeezes. While such events will remain uncommon, structurally lower liquidity than in previous years suggests that price and lease rate volatility will persist.

Lastly, in a separate report, Metals Focus also had an update on the Indian silver market and mentioned the following:

Insights from World Silver Survey 2026 highlighted a jump in Indian physical investment in 2025 (covering bar and coin demand), which rose by 35% y/y to 2,505t, marking the highest level since 2015. Notably, that earlier peak was achieved without the presence of exchange-traded products (ETPs).

Indian silver ETP demand rose by approximately 2,100t in 2025, reflecting strong investor interest in silver-backed financial instruments. This also suggests that a significant share of retail investment was absorbed by ETPs, and in their absence, retail investment demand could have been even higher. More importantly, this has opened up the domestic silver market to a broader set of investors, who increasingly view silver as an asset class alongside equities. This underscores the structural shift underway.

In a sense, it’s almost surreal to think back on how just three months ago, the silver price had soared over $121. Obviously, a lot has happened in the world since then. Although some of the quotes shared in today’s article allude to how I don’t think we’ve seen the end of this situation.

But at least we are coming to the end of this week, and hopefully it was a good one for you, and you’re getting set for a relaxing and restful weekend. I will be taking a break next week, but will be back the following week, and we’ll pick this back up again then.

Sincerely,

Chris Marcus

About the author