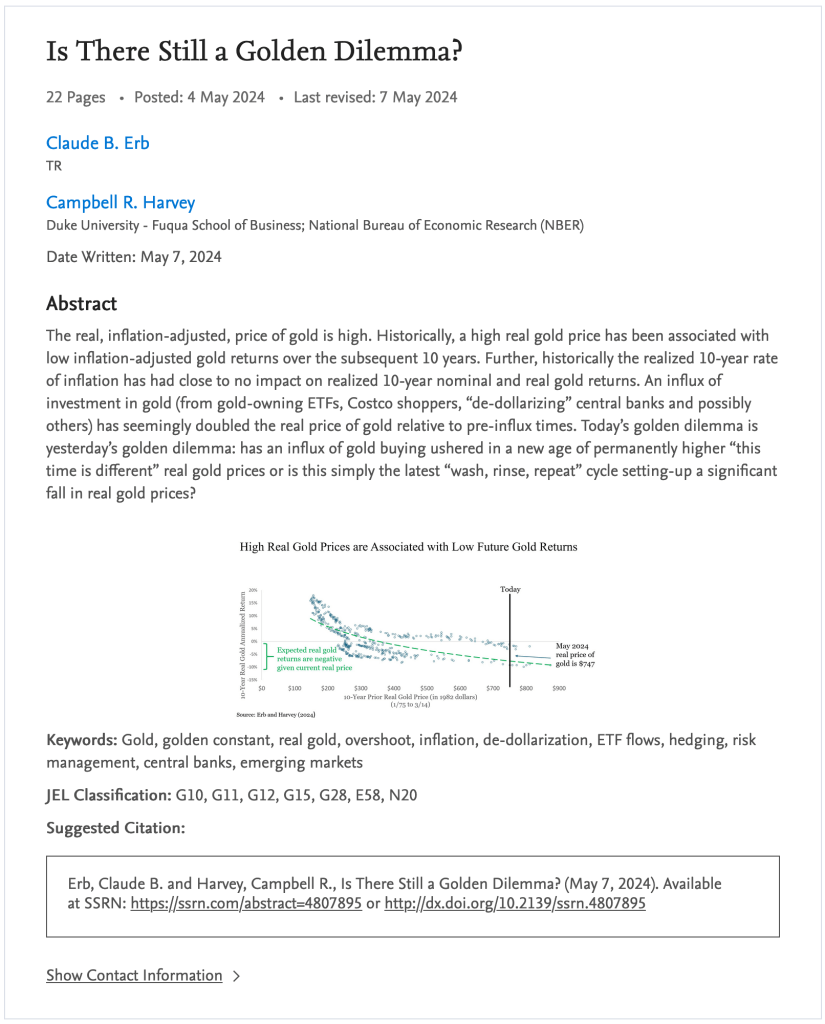

Harvey & Erb, they of the Golden Dilemma, once again promote a story that only an academic would stick to years after being proven wrong

They are back, ole’ Harvey and Erb. First there was the Golden Dilemma in 2012, where they predicted $800 for the gold price (it made a low of 1046 in 2015) based in part on its lack of effective inflation utility (well, they were at least half right, sort of).

Then came the Golden Constant as I highlighted in 2019. Again applying faulty assumptions from the rarefied air of academia, they state:

A “golden constant” perspective suggests a fair value price for gold of $840 an ounce and a possible overshoot price of $353 an ounce.

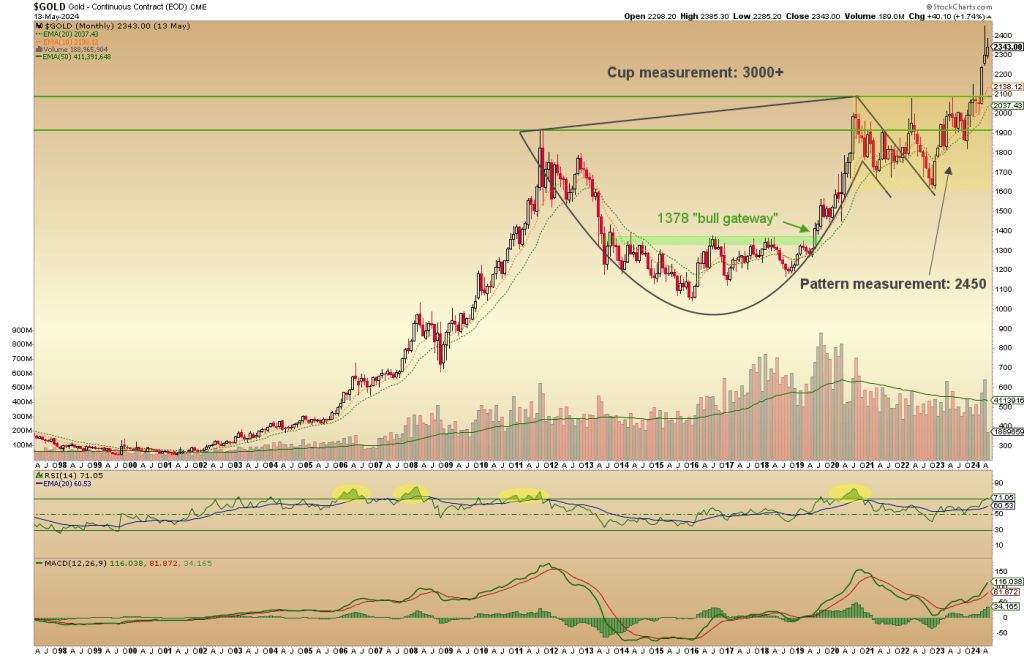

Mind you, this was produced during the very year that NFTRH clearly marked the beginning of the next bull phase as the gold price took out the “Bull Gateway” at 1378.

Twice wrong for the plucky professors. Yet somehow, the media have decided that they are worthy of feeding more assumptions to the public to digest. They are academics after all; experts, after all. Media serves experts, after all. And being right or wrong seems not to matter because once you’re codified in the pubic consciousness, you are all that. When you’re an unknown blogger or other such riff raff, you are none of that.

Now you can download a professionally produced research report by clicking the abstract. The article is so important, you see, that it needs an abstract to prepare you.

Within the research, Harvey & Erb are tripling down on the same premise, which was wrong 12 years ago, wrong 5 years ago and is wrong again now. In their insistence on tying gold to inflation (also mentioning lesser considerations like China buying, BRICS dedollarization, Central Bank buying and GLD bullion holdings) they ignore other more important utilities for gold and focus on its ‘price’ and what they think its ‘price’ should be. In other words, all the stuff you see out there leading the masses away from the real utility for gold, which is value. A plain and simple word ignored by most in the financial markets, media and apparently, academia.

As posted at https://www.ssrn.com/index.cfm/en/

As posted at https://www.ssrn.com/index.cfm/en/

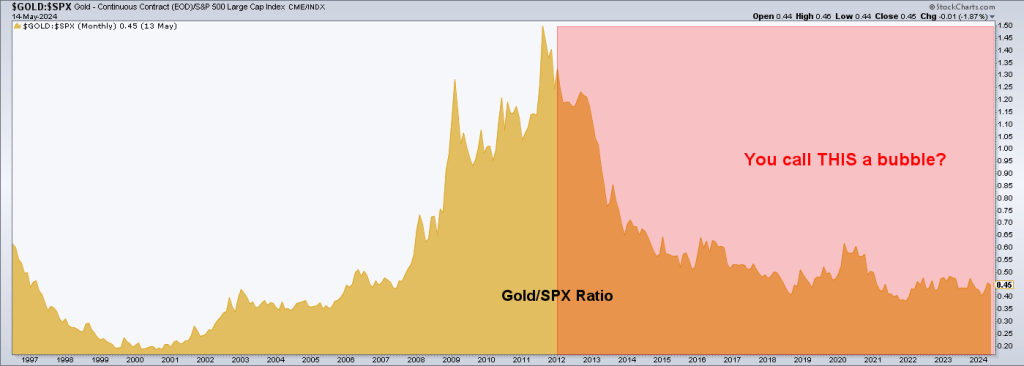

Gold is simply the anti-bubble, the asset outside the official system accepting no liability, owing nobody, holding long-term value and sure, protecting against officially manufactured inflation within a Keynesian debt system (until that inflation begins to temporarily rig the economy positively), against economic down cycles and frankly, against the end of the bubble era.

The bottom line as relates to Harvey & Erb is that they have once again produced a piece with a lot of moving parts, a lot of noise, conjecture and firm assumptions, the primary of which is wrong. They are in essence saying that gold is vulnerable due to its high “real price” as it finally starts outpacing inflation signals, like those noted in yesterday’s article. Imagine that, the very thing that right-minded gold bulls have been waiting for is now being touted as a means to gold’s price destruction.

Here is their conclusion, with a few rebuttals by me after.

Conclusions

High real gold prices presage future unattractive real gold returns. [1] Gold purchases and sales by market participants, such as gold owning ETFs and “de-dollarizing” central banks and others, can affect the real price of gold and prospective real gold returns. There is no simple and unarguable way to calculate the impact of gold market participants on the real price of gold. There are debatable and approximate ways to speculate about the contours of this market impact. Irving Fisher has been criticized forsuggesting on October 16, 1929 (shortly before “Black Monday” on October 28, 1929) that stock prices had reached “what looks like a permanently high plateau”. It is possible that an analysis of stock purchases and sales by market participants, comparable to the analysis of gold purchases and sales by market participants, would shed light on the financial devastation Fisher experienced as the Great Depression unfolded. [2] Have real gold prices reached “what looks like a permanently high plateau”? Probably not. Could real gold prices fall substantially? Yes, especially if gold market participants directly or indirectly value gold as an aspirational inflation hedge, a golden constant. [3] It is worth considering that China’s pursuit of de-dollarization is unlikely to be motivated by the idea that gold is an inflation hedge or a store of value. De-dollarization is a governmental goal just as “Made in China 2025” (a state-led industrial policy which seeks to capture foreign markets and promote domestic innovation and self-reliance) and the reunification of Taiwan with China are government goals. In this case, gold may possibly serve as a tool for de-dollarization. [4] Today’s golden dilemma is yesterday’s golden dilemma: has an influx of gold buying ushered in a new age of permanently and perpetually rising real gold prices or has it simply set-up real gold prices for a significant fall? [5]Harvey & Erb, Is There Still A Golden Dilemma?

[1] High real gold prices presage a new era in the macro, as evidenced by the long-term trend break in long-term Treasury yields, among other things.

[2] Are you seriously comparing current gold or its real price to a historical stock bubble? Without even a mention of the ongoing “everything bubble” in stocks and many more assets? Come on guys.

[3] Whereby the gold bugs bring about their own demise. Well, this website and this market report have for years rejected any gold bug dogma spewing on about inflation as the primary reason for owning gold. And there you two go again, obsessing not only on inflation and gold but also…

[4] Obsessing China buying of gold, CB buying of gold, de-dollarization, all the things that have gotten gung ho gold bugs in trouble all along.

[5] Like good academics you hold that today's golden dilemma is yesterday’s golden dilemma because like good academics you have a thesis that you profess and on and on do you profess, professors. You take not even a little look at how the macro backdrop – the very big picture ecosystem in which your analysis exists – is changing right before your eyes (eyes that will not see).

You Harvey, and you Erb, appear to be of a different era. Removed from the Everyman and cloistered in the academic setting of the Fuqua School of Duke University in association with the National Bureau of Economic Research. You, Harvey and Erb, will be proven wrong once again.

About the author