Stagflation is showing up in data points and articles everywhere now.

Delta worries, labor shortages and fading Washington stimulus — it’s enough to cast a chill on the U.S. economy this fall.

A bevy of Wall Street forecasters chopped their targets for U.S. growth after a poor U.S. jobs report for August. The government on Friday said the economy gained 235,000 new jobs last month — just one-third of what investors were expecting.

Goldman Sachs, Morgan Stanley, BMO Capital Markets, TD Securities and other firms cut their forecasts — some by more than half.

An economy that was expected to grow at a sizzling 7% annual pace from July through September is now seen expanding at a more modest 3% to 3.5% clip….

The companies that have been hurt the worst during the pandemic — restaurants, hotels, theaters and so forth — added zero new jobs in August. They had created an average of 364,000 new jobs a month since May….

A possibly even bigger factor in the U.S. employment report is a lack of people willing to go back to work….

It’s not just labor shortages, either.

Companies are struggling to obtain the parts and materials they need to produce enough goods and services to satisfy the surge in demand….

Fading government stimulus could also weigh more heavily on the economy in the second half of the year….

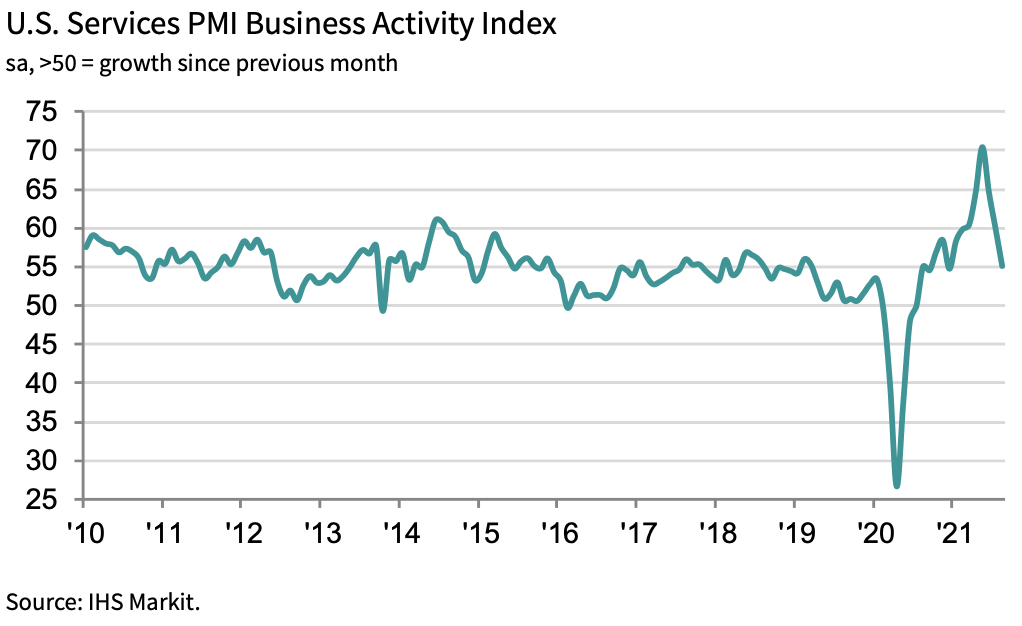

As Chris Williamson, Chief Business Economist at IHS Markit, noted after the latest IHS survey of US business activity:

Growth slowed sharply in the US service sector in August, joining the manufacturing sector in reporting a marked cooling in demand and encountering growing problems finding staff and supplies. Jobs growth almost stalled among the surveyed companies in August and supplier lead times are lengthening at a near record rate.

While the resulting overall pace of economic growth signalled is the weakest seen so far this year, backlogs of uncompleted work are rising at a rate unprecedented in at least 12 years, underscoring how supply and labor shortages are putting the brakes on the recovery. The inevitable upshot is higher prices, with firms’ input costs and selling prices rising at increased rates again in August, continuing the steepest period of price growth yet recorded by the survey by a wide margin.

Here is what the IHS survey showed for rapidly stalling business activity:

Stalling growth, accompanied by “the steepest period of price growth yet recorded by the survey by a wide margin.“

That translates “STAGFLATION” in stark terms.

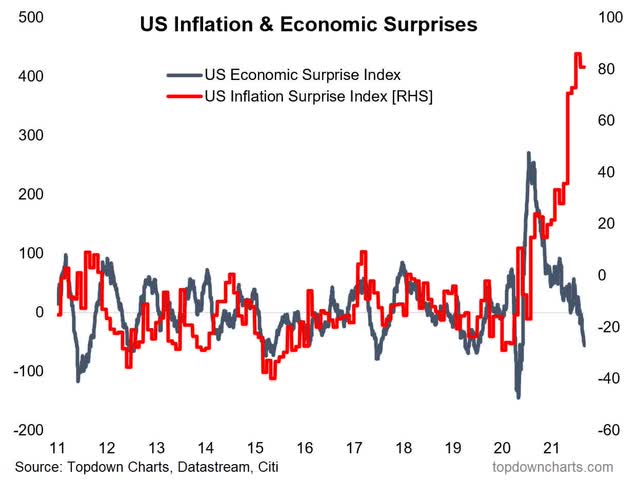

The gaping jaws of stagflation, capable of consuming any economy, now look like this:

Rapidly soaring surprises to the high side on prices accompanied by a steeply deepening downside to surprises for the economy.

Can stocks survive this monster?

In light of stagflation reality …

The big question overhanging the market is about how much longer can the Federal Reserve continue to support the stock market?

The answer seems to be, “Not much longer….”

The connection of the Federal Reserve and the stock market goes back to the time that Ben Bernanke was the Chair of the Fed. Mr. Bernanke, during the Great Recession, set off to generate an economic recovery based upon creating a wealth effect that would spur on consumer spending….

The Fed continued to pursue a rising stock market to fuel the economy and the economy responded, through the change in Fed chairs, up until the Covid-19 pandemic hit the U.S. Both Janet Yellen and Jerome Powell, who followed Mr. Bernanke as Federal Reserve chairs, continued the policy….

The big cloud hanging over this picture is the one pertaining to the need for Mr. Powell and the Federal Reserve to “back off” from purchasing $120.0 billion in securities every month and begin to “taper” the purchases….

What will investors do when they actually see the Fed easing off and the liquidity in the banking system begins to decline?

There is more than $4.0 trillion in reserve balances now sitting in commercial banks in the U.S. This is the foundation for all the market liquidity and confidence that now exists within the financial markets in the country.

The question that is being asked is “what happens when reserve balances begin to decline?”

The last time what happened was what I called “The Repocalypse: The Little Crisis That Roared.”

Let me answer John Mason’s question in the article I just quoted with a little history lesson, which I covered in much more detail in my last Patron Post.

As you can see in the following graph, when the Fed first tapered from late 2014 – 2016, the stock market went absolutely nowhere for two years. You could have sold out of stocks in 2014 and bought back in the middle of 2016 at exactly the same level. You missed nothing in terms of stock values, except the roller coaster ride of late 2015 through early 2016. (Of course, if you’re good at riding roller coasters, buying low and selling high and then repeating that, you could have done well selling at the top of each plunge and buying back in at the bottom.)

Then, in 2018-2019, when the Fed tried actually tightening by raising interest rates and reducing the size of its balance sheet (effectively money supply), stocks, again, went nowhere for almost two years. You could have sold all your stocks at the January peak in 2018 and bought back in at the same level late in the summer of 2019.

Federal Reserve Bank of St. Louis

Federal Reserve Bank of St. Louis

All along the way of the “longest bull market in history” and even into the present bull market (the final oval), the periods of phenomenal stock gains were fueled when the Fed was easing, with the greatest gains happening during the present bull because of the most extreme QE ever and joint federal-government money-doling during the COVIDcrisis period.

So, based on some pretty clear history, what will happen to stocks when stagflation forces the Fed to either taper, as it did in the first period of stock troubles on the chart, or actually tighten, as it did in the second period of more extreme stock troubles? You do the math. It’s not hard.

All the increases of the Great Bull Market can be accounted for by the long stretches where the Fed was actually easing and by the Trump Rally of 2017, which happened because of the promised Trump Tax Cuts (and their eventual fulfillment). Those huge cash flows into stocks fueled massive stock buybacks and huge increases to corporate bottom lines (earnings) to somewhat justify those rising stock valuations. The tax cuts provided as much available cash to stock buyers (especially those running corporate boards) as anything the Fed had done. Even the rise at the end of 2019 happened because the Fed returned to QE because of the Repo Crisis, though it denied it was doing so. At first, the Fed tried to resolve the crisis, which had been caused by its tightening, by adding hundreds of billions of dollars to the money supply through Repo loans then through outright QE during the last couple of months of 2019.

Quoting my last Patron Post,

My big prediction for 2019 was that Fed tightening would end in a massive repo crisis in the latter half of 2019 because bank reserves were being drawn down too far due to the Fed’s reluctance to give up tightening soon enough. That would only end, I said, by the Fed going back to QE to actually reverse its tightening….

The Fed had to rush back into QE during the final quarter of 2019, though, of course, Powell maintained that it wasn’t really QE because, again it was just temporary and did not involve long-term bonds. (Any excuse will do to avoid saying they have permanently monetized the US debt and its economy.)

“Fed-up and Failing: How FedMed Killed the Patient“

As Mason goes on to say in his Seeking Alpha article,

There are plenty of reasons for the Fed to reduce purchases. Even stop them.

The most important one to me is the fact that all the liquidity in the banking system is forcing short-term interest rates toward negative territory….

Mr. Powell and the Fed say that they do not want the federal funds rate to become negative. But, it looks like the Fed needs to stop purchasing all those securities if the federal funds rate is to stay in positive territory.

And then there is the looming threat of higher rates of inflation.

The Fed is going to have to make a move this fall….

Investors have been betting on the Federal Reserve support going back to 2009. The Fed has not let them down. Yet….

Mr. Powell kept the Fed excessively loose during his first months as Fed chair. Rather err on the side of monetary ease than be a part of a market collapse. Then the pandemic came along and Mr. Powell oversaw a massive injection of reserves into the banking system.

Now, it seems as if we have reached the point where all the “ease” in the past is catching up with us and we are reaching a spot when the Fed will have to catch up for all the trillions of dollars it has pumped into the economy.

And, what, then, are investors supposed to do?

Investors have, for the past twelve years or so, “followed the Fed.” And, this has made them billions and billions of dollars of profits.

But, all good things must come to an end….

The Fed is going to have to change its policy stance. Investors beware.

And that way of seeing things is why I bet my blog on the present inflation train continuing until it forces the Fed to tighten and, thereby, kill the stock market (based on historic precedent that is pretty clear about how the market responds). The market has risen higher on greater easing than ever before, so it has further to fall. The alternative, I said, is that the Fed refuses to tighten because it fears the market carnage its tightening will create (or because the government demands Fed funding), and so we move into even worse inflation than the present inflation, which will rip the economy apart even more than the present stagflation already appears to be doing. That kind of carnage, too, is not likely to end well for stocks. Tends to be the kind of thing that flips sentiment on its head.

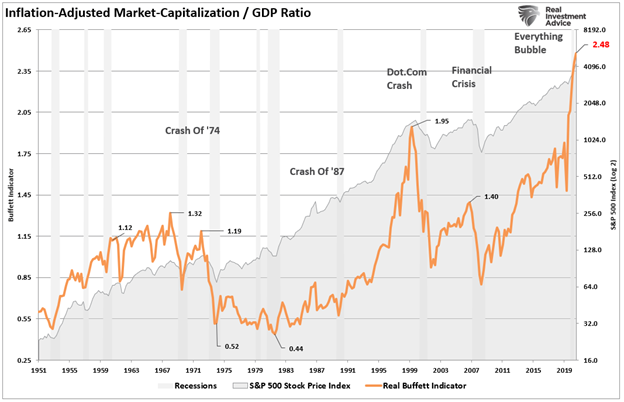

How high is too high?

The proverbial Buffet Indicator, which the Oracle of Omaha goes by for assessing whether stocks are overvalued, is further into the nosebleed section of stock valuations than it has ever been … by far:

And, if GDP continues to fall as is being widely predicted now, this gauge of stock values will look even worse.

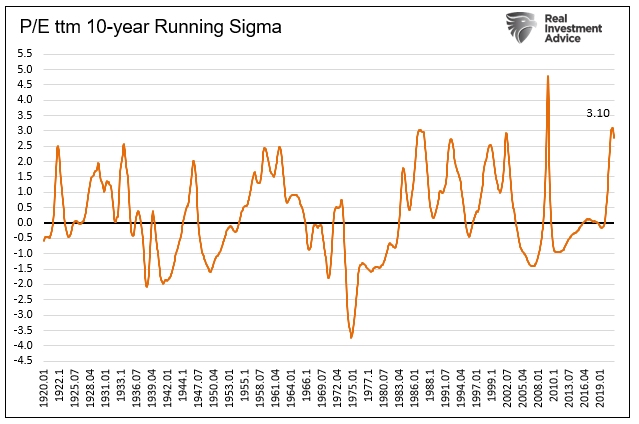

Price-Earnings ratios also look extreme:

As Lance Roberts notes,

Corporate earnings and profits ultimately get derived from economic activity (personal consumption and business investment). Therefore, it is unlikely the currently lofty expectations will get met…. Through the end of this year, companies will guide down earnings estimates for a variety of reasons: Economic growth won’t be as robust as anticipated. Potentially higher corporate tax rates could reduce earnings…. Higher interest rates increasing borrowing costs which impact earnings….

In other words, the Price/Earnings ratio for stocks will become even further overvalued because earnings will decline.

The problem for investors currently is that analysts’ assumptions are always high, and markets are trading at more extreme valuations, which leaves little room for disappointment.

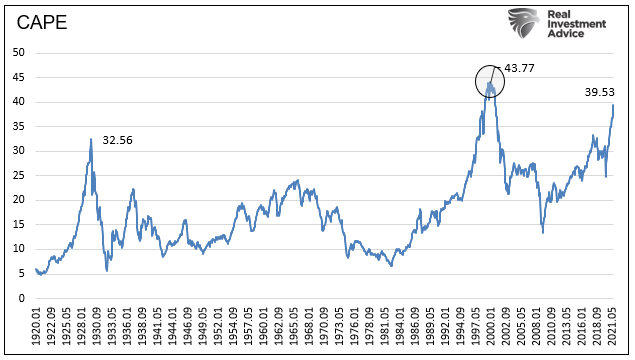

Historic CAPE valuation also shows stocks are more overvalued than anytime other than just before the great crash of 1929 and the dot-com bust of the early 2000’s:

However, the timing for the rise and fall of stocks is based on turns in the tide of investor sentiment. Although, the level to which they fall is likely to be a much deeper plunge when they are this highly overvalued historically.

Unfortunately, the early aught years offered far better economic growth prospects due to the burgeoning internet economy than the present COVID economy offers after decimating industries all over the globe, a ravaging that continues to broaden like ripples across the oceans of this world. If stocks were overvalued during the dot-com era with plenty of room to fall, how much more so now with the entire global economy in tatters?

As Michael Lebowitz noted on Lance Roberts’ Real Investment Advice site,

If the market falls to the average of the last ten years (0 sigmas), we should prepare for losses of over 30%. If it falls below zero, as is typical, more significant losses are likely in store.

As Lance Roberts of Real Investment Advice writes,

Significantly, investors never realize they are in a “melt-up” until after it is over…. However, there are clear signs the advance is beginning to narrow markedly, which has historically served as a warning to investors….

“Relative to their 200-day moving averages (DMA), all three indexes have been generally trending lower since April, as shown in the second chart below.” – Charles Schwab

That could be a sign the tide is turning.

The Fed is now getting pushed into needing to tighten monetary policy to quell inflationary pressures. However, a rising risk suggests they may be “trapped” in continuing their bond purchases and risking both an inflationary surge and creating market instability.

We know what the market historically does when the Fed either tapers or tightens. We don’t know if the Fed will taper or tighten since it, too, knows from experience it will crash the market if it does that, and it has the government debt pressing it toward endless money printing. Still, we do know the pressure to tighten has continued to build all year long, just as I’ve said it would, and we know it shows no signs of letting up, and we know current stagflation certainly isn’t helping the economy any. So, something is going to crack, even if the Fed doesn’t.

In the face of great inflationary pressure, the Fed has its back to the wall:

The scale and scope of government spending expansion in the last year are unprecedented. Because Uncle Sam doesn’t have the money, lots of it went on the government’s credit card. The deficit and debt skyrocketed. But this is only the beginning. The Biden administration recently proposed a $6 trillion budget for fiscal 2022, two-thirds of which would be borrowed.” – Reason

Exploding government debt will not let the Fed tighten. What is it going to do?

The problem, of course, is that the Fed must continue monetizing 30% of debt issuance to keep interest rates from surging and wrecking the economy.

That was also John Mason’s concern. Without continued Fed largesse, interest rates will certainly rise, as the government has to replace the Fed as chief financier. Fed bond buying is the only thing holding rates down, in spite of inflation, and rising interest will crash the bond market, as Bond King Bill Gross argues:

Bill Gross, the “bond king” believes that bond prices are at their peak with no place else to go but down…. Gross … is attracting more attention these days referring to bonds as “trash” and arguing that if one buys U.S. government debt, one is almost assured of losing money….

To Mr. Gross, the Federal Reserve must start reducing the amount of securities it is adding to its portfolio every month.

This past year the monetary authorities bought 60 percent of the “net issuance” of the federal government debt. If the Fed “backs off” from its current level of purchases, the question becomes, how much will the private markets be able to absorb in 2022 and beyond.

So, Fed policy will cause either a stock crash, a bond crash, or both. Gross says the 10-year must rise from its current yield around 1.35% to 2% or more just to track with inflation and to make up for the lack of demand for government bonds if the Fed backs away from being the main buyer in order to fight inflation — the buyer of last resort for government bonds. That, John Mason points out, would lead to substantial losses for current bond investors holding 10-year government bonds at the lower yield.

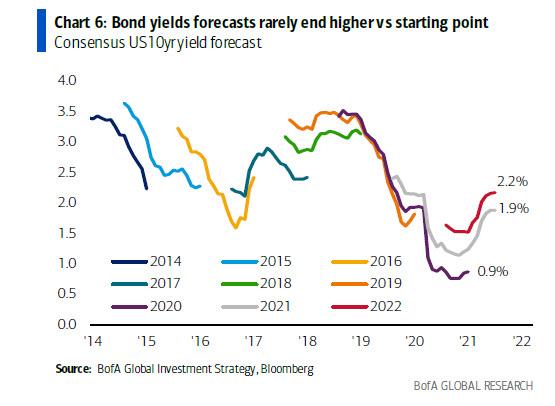

Bank of America, gives the following yield guidance for the remainder of the year:

Of course, if the Fed doesn’t tighten and keeps forcing bond yields to remain down by soaking up all government bond issuances at that 60% rate of consumption, stagflation will become a roaring inferno, the likes of which we haven’t seen in the US. I find it highly improbable that investor sentiment will survive that kind of upward surprise in prices and the downward surprises in the economy that those soaring prices will bring about.

Danged if you do and danged if you don’t

That’s to put it politely, of course. Sounds to me like, either way, the economy is going to collapse and markets with it. Either the stock market gives way because the Fed tapers its bond purchases or even tightens, which raises interest rates, in order to curb inflation, and the bond market fails simultaneously because yields rise as the market fills the gap in government funding as the Fed tightens, or soaring prices ravage corporate profits and consumer ability, destroying the economy, and stock investors will like that garden of horrors no better.

What I am seeing is the everything bubble bursting as anything the Fed tries to do to save one thing now now only makes something else worse.

Since the days when the Fed first started its “Great Recovery” program, as I call it, the economy, and often the stock market, has fallen every time the Fed has tried backing away from its quantitative-easing strategy. In one of my first articles written on this blog back in 2011, I wrote

I predicted that the government [its puppet or agent, depending on how you look at it, being the Fed] would try a second round of quantitative easing as soon as the first one they approved ended and downward reality began to reappear of a hard road in front of us. I have even stated the government would be strongly tempted to try a third round when the second ended and the ugly reality, again, began to reappear. Anything to avoid this austere reality. Stark realities mean angry voters….

That is the bleak landscape we now face (and are still trying to deny). The artificial recovery made it appear for awhile as if we were just going through another bursting economic bubble and were on our way out. In real fact, ALL of those efforts did nothing to correct the underlying problems of the economy. That is why this is the same recession, not a second recession. It is due to continuation of the same cause. It looks like two recessions or a double-dip only because it was falsely propped up in the middle by the unsustainable effort to create funny money. The worst part of Ben Bernanke’s solution is that he actually perpetuated the problem and even made it worse…. Ben Bernanke sought to prop up the failed housing market by expanding debt once again. Yet it was this highly indebted housing economy that led us into this mess.

“Saving Capitalists from Capitalism“

We’ve been kicking this can down the road of reviving the economy every time it fails by exponentially increasing government debt and Fed money printing. In my last Patron Post, I laid out in great detail how the economy has failed every time the Fed has backed away from QE. We’ve now reached the point where inflation is forcing the money printing to end just as the economy is going down again and when stocks are more dependent on Fed support for their extraordinary valuations than ever before.

We all remember how Fed tightening went when it actually tried it back in 2018. It was a disaster, which forced the Fed had to call it off well ahead of the Fed’s stated plans. Now mere tapering could be as big a disaster as tightening was because it happens in a vastly worse economy of rapidly plunging GDP if it happens at all.

As I concluded in that last Patron Post,

The new QE, QE4ever, has already managed to outdo all the previous rounds of QE put together. So, as I said back at the start of tired and endless recovery plan, once we began down the path of QE as a way out of recession, instead of rectifying the real problems that were the cause of the Great Recession, it became QE forever, Baby! We decided to solve a debt problem by piling on more debt in that all Fed money issuance happens through debt issuances.

And that’s why I call this the Great Recession Blog. We’re still on the Great Recession Recovery Plan with no end in sight because we solved nothing! We just bought time — “kicked the can down the road” –at the cost of ever spiraling debt, financed by exponentially growing Fed money printing. And we all know what happens now if the money printing actually stops. This time, however, the Fed has inflation breathing like a dragon down its back to face it to stop moneh printing, and this time the Fed faces that tightening pressure when the economy is already slumping:

“Fed officials themselves expect noticeably slower growth in the years ahead at a time when both monetary and fiscal policy will be tighter. That raises more questions about whether Powell and his cohorts can get the exit right. “Are they exiting at the right place? Are they exiting at the right time, at the right magnitude? Given the slowing of the economy, we have questions around both,” Misra said…. ‘I think people are very worried about the idea that maybe this isn’t going to work out the way we planned….”

It never has. Why would it start to now?

“Fed-up and Failing: How FedMed Killed the Patient“

Liked it? Take a second to support David Haggith on Patreon!

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!