As inflation signals moderate and Goldilocks gets pumped, gold is forecasting something more virulent for Q4 – H1, 2025

While this is not an article about gold mining, it is an article about the counter-cyclical economic backdrop ahead that gold is forecasting, and a reminder that the gold mining industry is counter-cyclical and due to leverage gold’s macro relationships in a way that it could not during long inflationary trends.

Since projecting a Goldilocks (inflation not too hot or cold, but just right) flavored market recovery to be led by Tech/Growth stocks well over a year ago that is exactly what came about, with an interruption by the recent bump up in macro inflation signaling, which we also anticipated in advance (due to Treasury yields bottoming and various inflation signals beginning to percolate). But that was expected to be counter the trend toward an interim deflationary liquidity problem for the markets.

Pivoting from the recent bump up in inflation anxieties, the process resumes in microcosm to what happened in 2021-2022 into 2023. On this shorter time frame the market may again follow the path of Inflation Anxiety > Goldilocks and this time, proceed on to liquidity problems. Our (NFTRH) ongoing thesis is that deflationary fears may and probably will be delayed until after the US presidential election; a rancorous and downright scary affair involving a guy who cannot even read teleprompted lines with any level of competence and an accused felon.

But that last line above represents a slippery slope into social/political commentary of a late stage, hubris choked society in decline. Let’s not go there at this time. Let’s simply note that a party in power is likely to pull out every stop it can to stay in power, and those stops are ultimately inflationary. But gold’s status relative to the markets dependent on inflationary monetary/fiscal policy on a global, not just US basis, is turning positive and anti-inflationary. As yet the macro appears to be slipping back to disinflationary Goldilocks mode. What comes after will be far less pleasant.

On now to some gold-centric internal market views. Counter-cyclical gold’s standing vs. economically cyclical markets has been and will continue to guide the way to a macro situation that is not at all what it appears to be in the mind of the casual public viewer. This is posted in-day on Friday, so we will use live charts as they appear during the trading day.

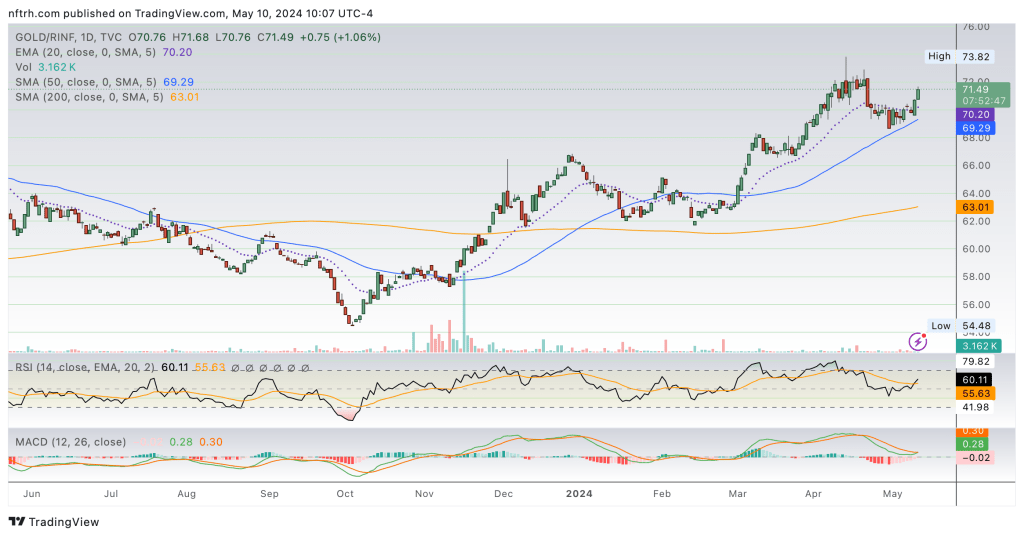

Gold in relation to an ETF billed as a representation of “inflation expectations”, RINF, has trended up vs. the bag of inputs commonly thought of as “inflation” since bottoming in Q4, 2023 (my view holds that “inflation” was the 2020 operation by the Fed and its fellows to massively pump money supplies and the problems since then are its effects).

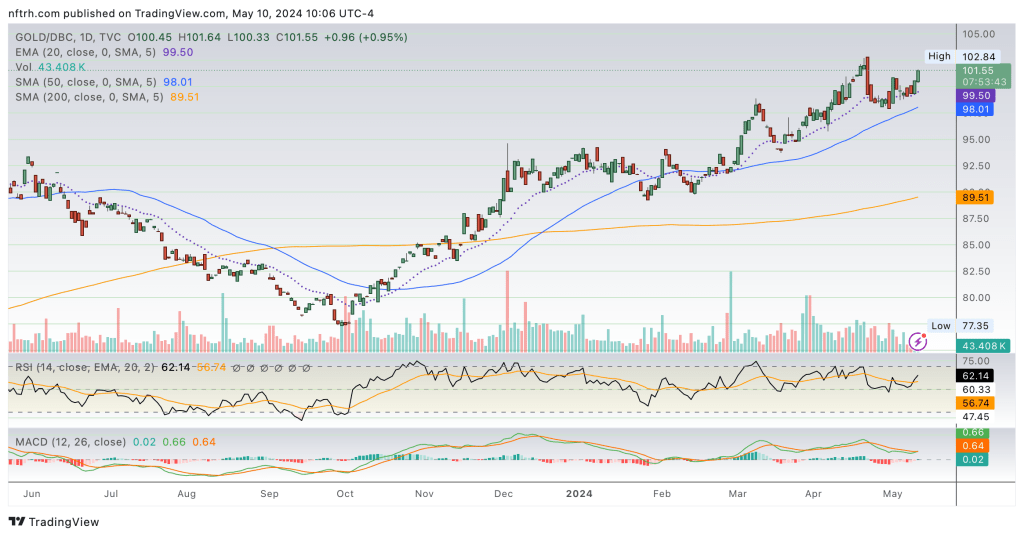

Gold has also maintained a post-Q4 uptrend vs. the broad commodity complex, represented here by DBC.

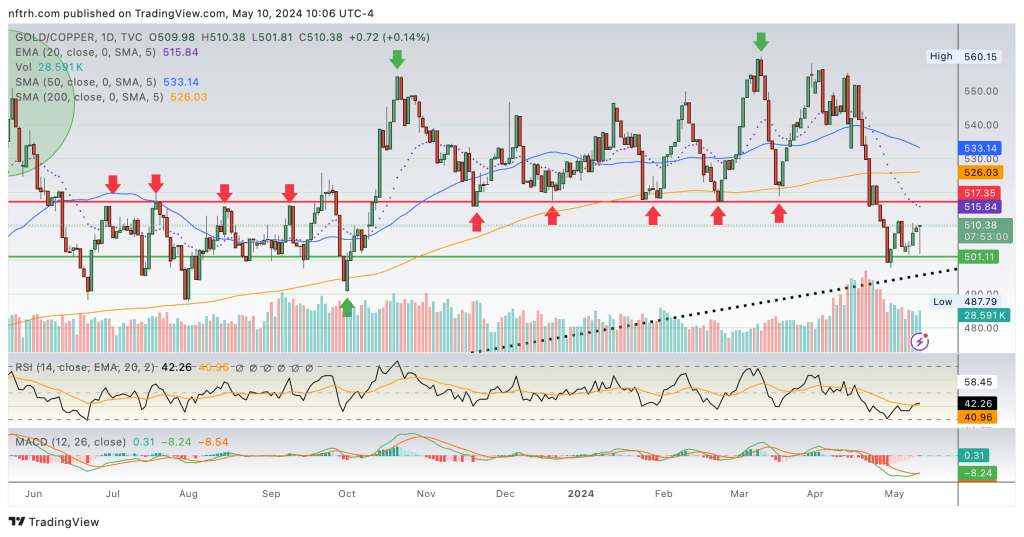

Within the complex, gold’s ratio to copper, the ultimate cyclical metal, has been beaten but not broken. The daily chart does not show it in full, but gold is still trending up vs. copper.

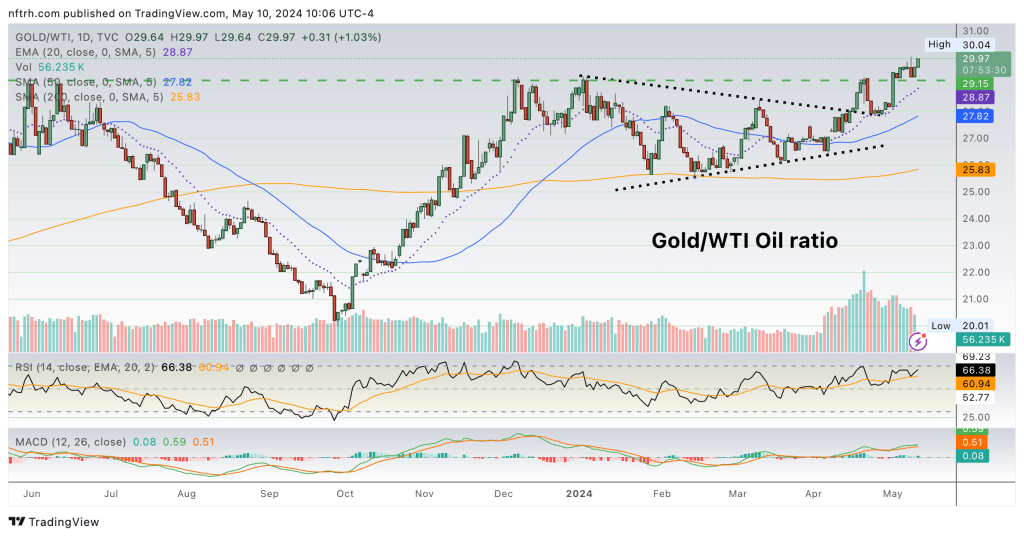

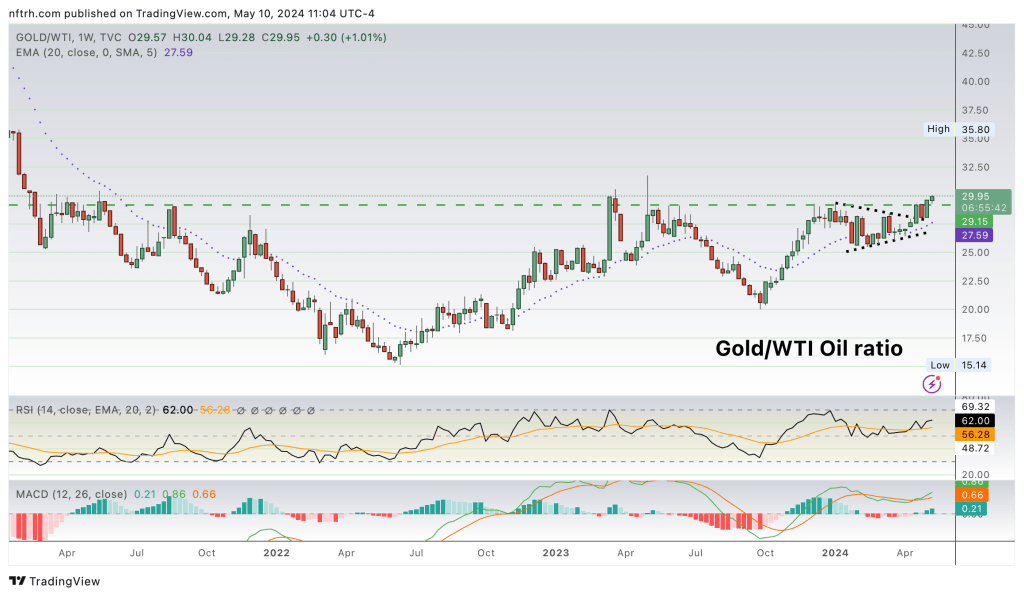

Also within the complex, and with particular importance to the Energy intensive gold mining industry, the Gold/Oil ratio (GOR) is on the verge of a breakout. Again, the daily chart does not provide full context…

…but the weekly chart does. GOR has taken out recent upside bounds and has a little more noise from 2023 standing in the way of new highs for the cycle. Your product rises more than your primary cost input? Gold miners will leverage that dynamic.

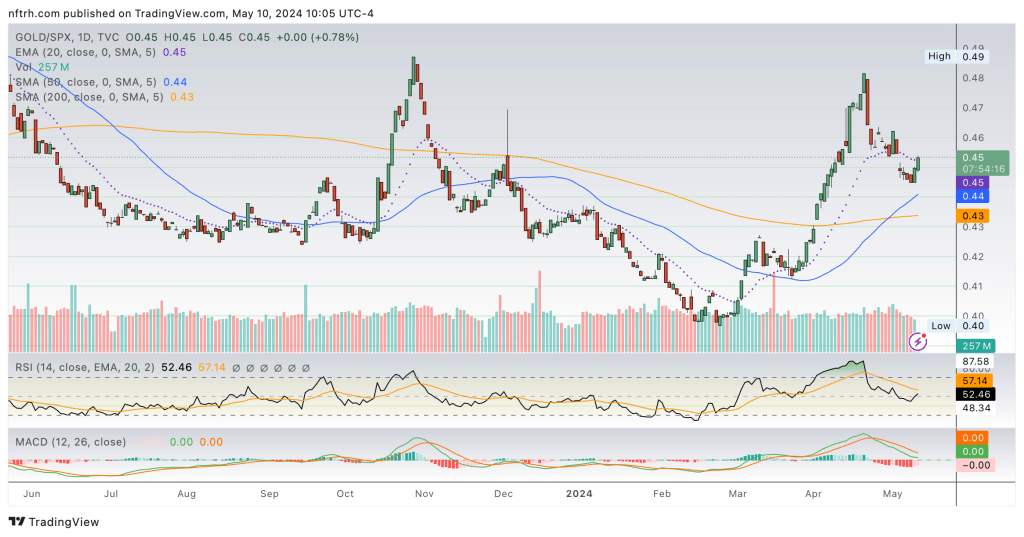

Moving on to stock markets, the Gold/SPX ratio has consolidated gains from February-April and retains the potential to hold and resume that intermediate trend (within what is still a longer-term downtrend).

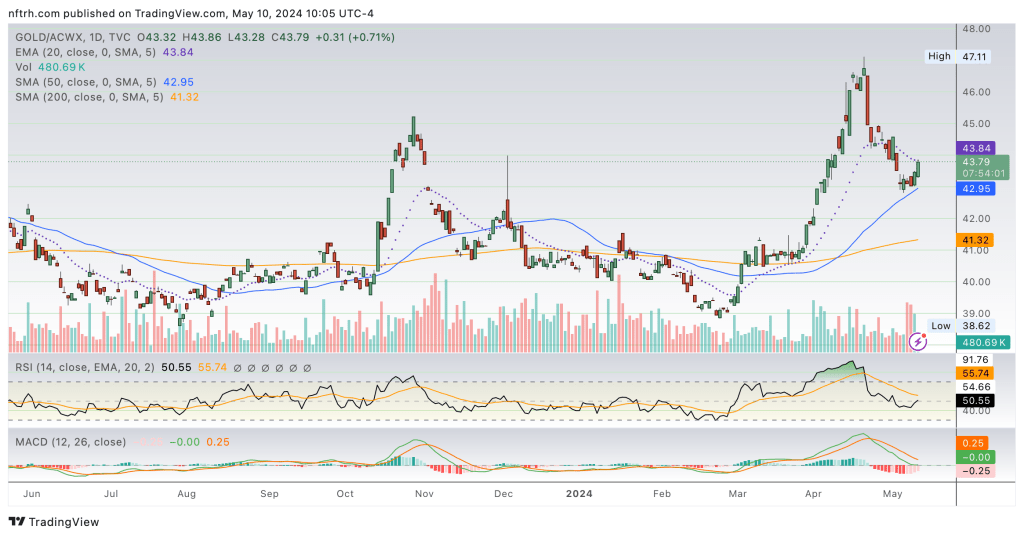

Gold/Global (ex-US) ETF is even better as the ratio could be interpreted as already being in the process of a trend change from down to up as it drops to test the uptrending SMA 50, and may be turning the SMA 200 up as well.

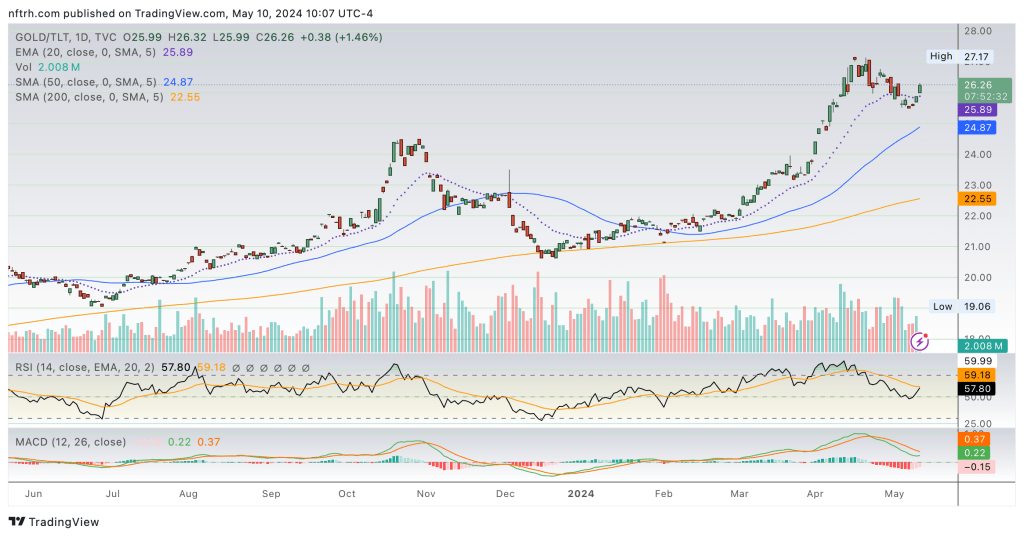

Gold remains in a firm uptrend in relation to US public debt, represented here by TLT. That includes the dividends that TLT spits out.

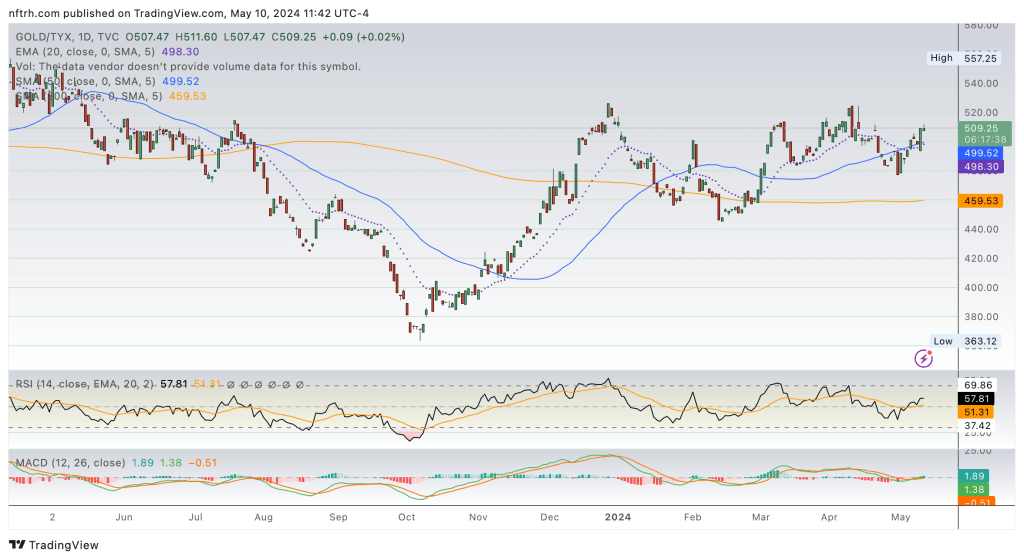

Flipping the above over to an opposing force to bonds, gold in relation to long-term (30yr) Treasury yields, which are supposed to be the vigilant overseer of, and compensate for the US debt creation machine, is also establishing an uptrend. These two combined represent a massive vote of no confidence in the US by collective global macro forces, in my opinion.

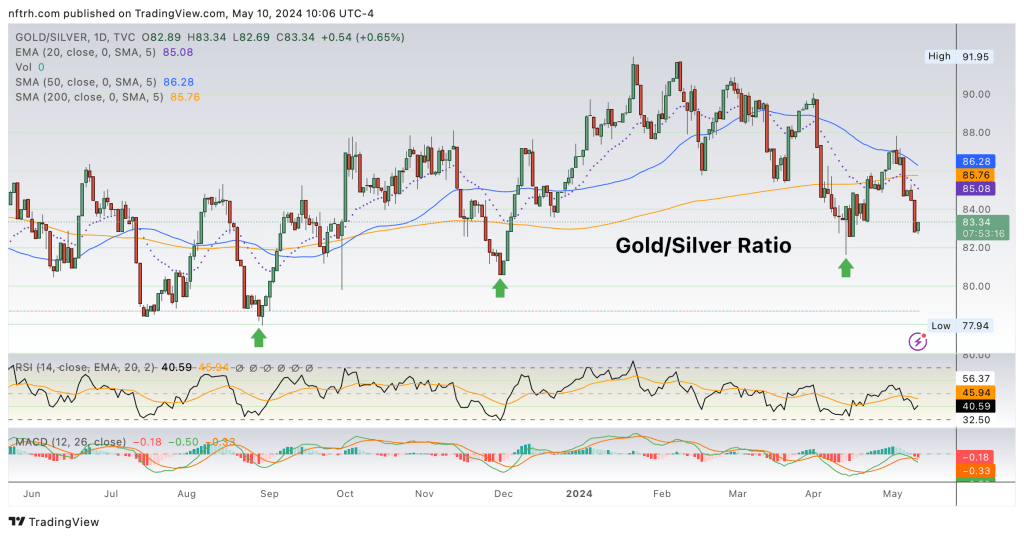

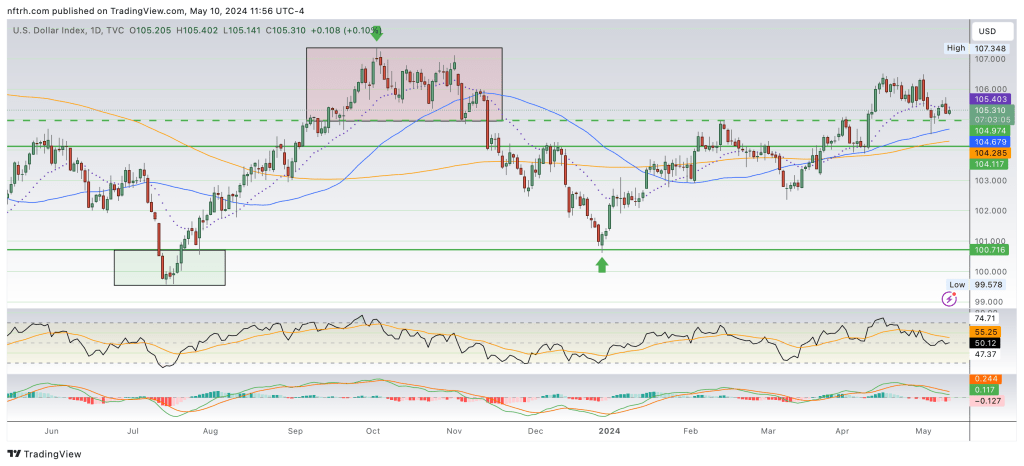

Finally, the combination of the Gold/Silver ratio (GSR) and US dollar (DXY) should signal a widespread asset market party atmosphere in the near-term if GSR breaks down and DXY loses the uptrending moving averages and makes a lower low to the March low. The other side of the coin is that should these maintain their uptrends market stress could soon follow, on an interim basis at least.

Bottom Line

- The near-term is in question for asset markets during a divisive (to put it mildly) election year where government can be expected to do what it can to keep the image of a firm economy in view.

- But gold is either trending up or changing trend vs. the cyclical world (and we have not even looked at Gold/Currencies ratios, which are universally trending up, including the Gold/USD ratio).

- While the stress could become front page news at any time, the process could endure into and through the election.

- But gold is changing trends now, and that does not bode well for 2025 for most markets as the macro is expected to flip counter-cyclical and recessionary. Gold has counter-cyclical characteristics and the gold mining industry leverages gold’s relative standing to the cyclical macro.

About the author