No sooner did we write Silver Rorschach Test, than the price of gold flash-crashed. On Sunday afternoon in Arizona—i.e. Monday morning in Australia and Asia—the price dropped sharply. Gold bug sources claim that the drop was $100, but as we can see from the price graph included in this report, the actual crash itself was about $70.

Some of these sources were very quick to assert that the drop was caused by naked selling of gold futures contracts. This is an allegation that is either supported by the data, or not.

Our comment yesterday regarding silver applies to gold as well:

“Price moves in themselves do not support any particular theory of who the actors are, what motivates them, or what they did (other than, broadly, buy or sell).”

Those who are hell-bent on believing in the existence of a nefarious and malevolent banking cartel who smashes gold to frustrate gold stackers (and to reduce inflation expectations, plus support the petrodollar) can always find reasons to reinforce this belief in the price action.

Monetary Metals’ Reports are for those who want to see the data.

Why is the gold price not “going up?”

Some common fallacies underpin and lead to the idea that gold has to be going up. First is the idea that prices should go up as a consequence of an increase in the quantity of the government scrip we call “money” nowadays. And gold, along with consumer prices. When gold doesn’t—and this happens all the time—the only explanation conceivable to people who believe this idea is that gold must be suppressed.

Second is the notion that gold is an inflation hedge. If consumer prices are rising, this view holds, then gold must be rising too. When it doesn’t, again, it leads back to the nostrum of suppression.

Third is the theory that the dollar is held up by nothing other than misguided faith, that any pin could prick the dollar bubble and cause total collapse, and therefore the Federal Reserve must suppress everything that looks like a pin. In this view, a rising gold price must be suppressed, or else people will suddenly repudiate the dollar.

When will dollar demand start “going down?”

We would suggest that the first sign of dollar repudiation is when the gold community stops thinking of the value of their gold in terms of dollars. When they look forward to every dip in the price as an opportunity to get more. Today, they may pay lip service to the latter (as the bitcoin maximalists do to their own price drops), but their angst over lower prices shows they want higher prices favorable to selling, not lower prices for more buying. Ergo they have not ceased demanding dollars just yet. The rest of the world will eventually stop demanding dollars, but this will be after the gold community stops. Which will be after more time, more crises, and more crazy policy responses. “Today is not that day,” quoth the Ranger from the North.

Do Central Banks dream of Gold at night?

In the meantime, the central bankers have no reason to worry that an $1,800 or even $3,800 gold price will make people reject their paper. And indeed the central bankers do not worry about the price of gold at all (notwithstanding old quotes from policy makers during the Bretton Woods gold price-fixing era).

Virtually everyone thinks that gold is a commodity, the dollar is money, and the value of gold is expressed in terms of dollars. They buy when they think it will go up, and they sell when they expect it to go down.

Fundamental Analysis of the Gold Smashdown

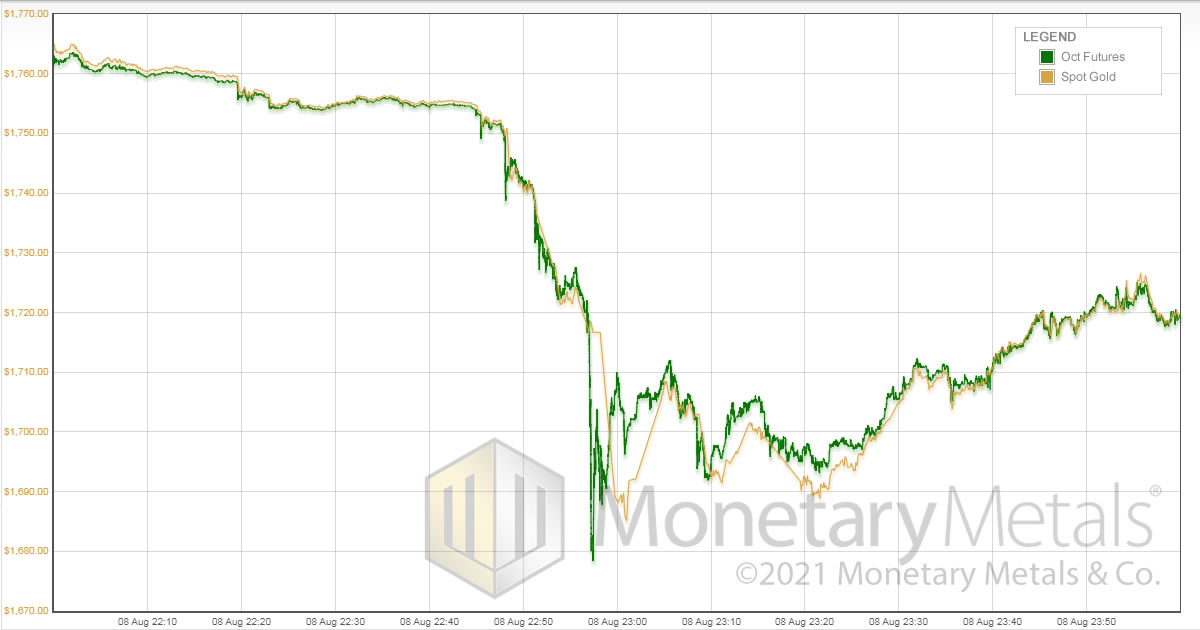

Anyways, here is a chart showing about an hour and a half of high-resolution price action.

We have included both spot and futures prices on this chart. Notice anything?

There are times when the price of futures is below the price of spot. For a minute, around 22:58 to 22:59, it looks like this is so (though spot quotes are spotty during this time, as evidenced by the long straight lines). But what is clear is that the opposite condition also occurs. Spot is below futures. And it remains so for about 40 minutes.

We repeat what we said yesterday:

“Note that if there had been a “smash” of futures, without any selling of physical, the basis would be something like -87%. Not minus zero point eight seven, but minus EIGHTY-SEVEN. We would be bellowing from the internet rooftops if such a huge backwardation in silver were occurring (and we would not be the only ones)!”

So, at best the argument is that “lots of people were motivated to sell lots of physical gold because, the cartel smashed the futures price.” Does this make any sense? Do you know any stackers who had been perfectly happy to think of the value of their gold as being, say, over $2,000? But suddenly they change their mind to think it is less than $1,700 and therefore rush to sell it now?

Zero Demand for Paper Gold, Unlimited Demand for Physical Gold

The headlines go a step further. We saw the alleged “gold price smash in paper, but physical demand is on fire.”

How do they square this circle? The price of physical metal fell as hard as the price of paper futures—but demand for physical is purported to be an inferno.

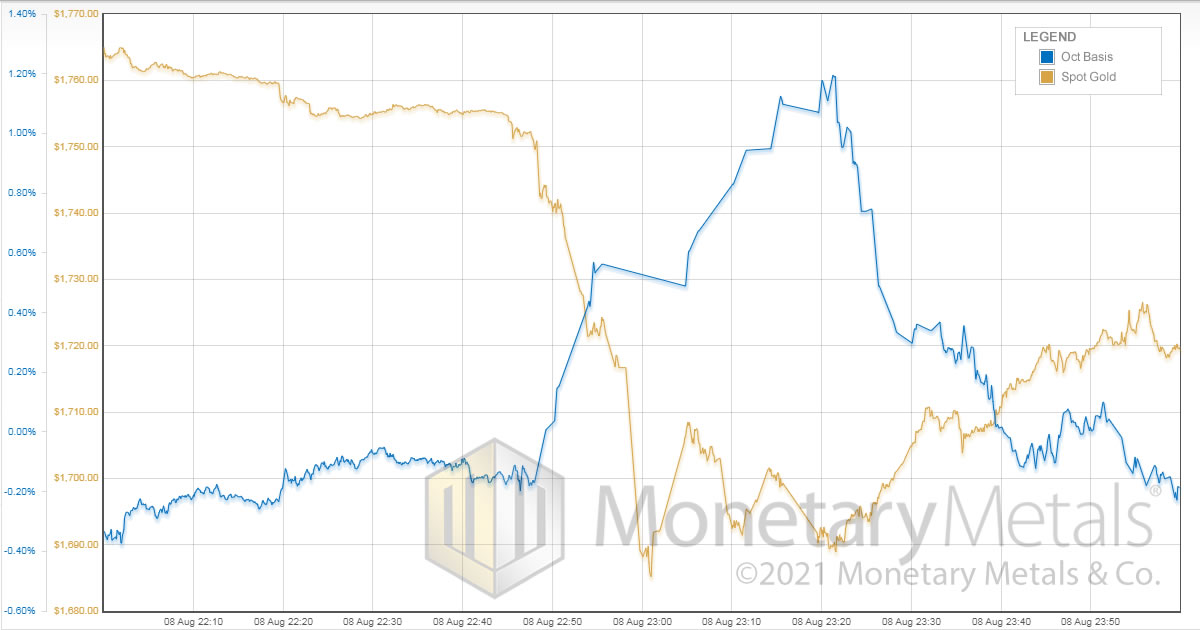

Let’s look at the same time period, this time showing spot price and basis (October contract).

Notice that big rise in basis, which occurs during the price drop. It continues another half hour, until the price has finally hit bottom. Basis is future – spot. If price is falling, and basis is rising, then what does that tell us?

A gold star to anyone who said that spot sold off more than futures.

What does demand for physical gold look like?

As with silver report, there is a second phase to this gold price action. In part two of the story, we see from around 23:21 that the price hits the bottom and the basis hits the top. After that the price recovers half what it lost, but the basis gives back everything that it gained.

This, folks, is what buying of physical looks like.

We are left with one lingering question. What could explain such a big price drop when the market opens? We will address this further in a separate article, but it could be margin calls and other not-entirely-voluntary selling, which could fit with the other selloffs that were occurring.

© 2021 Monetary Metals

About the author