Strengths

- The best performing precious metal for the week was platinum, up 6.48%. The increase may have been buoyed by a report by the Hydrogen Council in collaboration with McKinsey & Co. that notes that to reach the goals of the Inflation Reduction Act, there needs to be a tripling of current spending on green hydrogen production where platinum acts as a catalyst boost the production. Lundin Gold reported a strong third quarter 2022 production beat. Gold production was 122,000 ounces, 13% higher than the 108,000-ounces consensus, driven by better-than-expected head grade and improved recoveries.

- K92 Mining reported third quarter production of 32,995 gold equivalent ounces from its Papua New Guinea mine, up from 24,122 in the prior quarter. K92 noted the increased production came from processing 37% more ore through the mill at its Kainantu mine. The mine is currently outperforming the mill and the mill stockpile has reached its highest level since late 2020. Head grade to the mill averaged 8.67 g/t gold, 0.72% copper and 11.53 g/t silver with gold grades coming in 3% higher than budget.

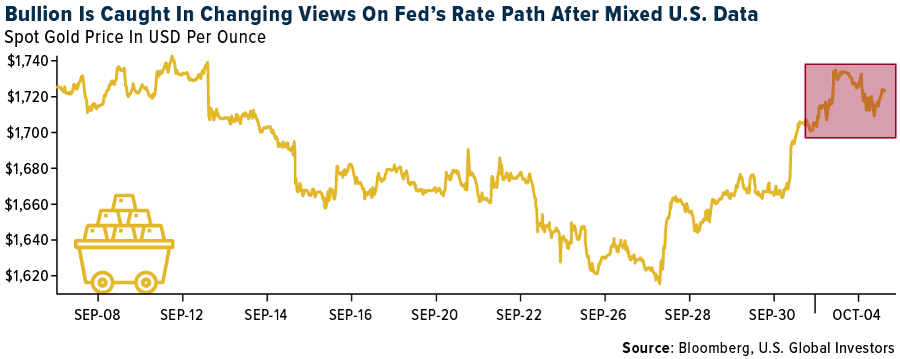

- Gold soared the most since March at the start of the week, writes Bloomberg, helped by a continued decline in Treasury yields, as traders weighed concerns that central banks’ monetary tightening will lead to recession and the possibility that bond rates may have reached a peak. Although the yellow metal fell approaching week-end, bullion extended its first weekly gain in three as of October 2, as lower bond rates boosted the appeal of the non-interest bearing asset. However, gains were higher than expected in employment, initial jobless claims and nonfarm payrolls, which eroded about half of the gains gold made earlier in the week.

Weaknesses

- The worst performing precious metal for the week was palladium, but still up 0.70%. Exchange-traded funds (ETFs) cut 143,678 troy ounces of gold from their holdings in the last trading session, bringing this year's net sales to 808,948 ounces, according to data compiled by Bloomberg. Gold fell near the end of the week, sliding toward $1,700 an ounce as traders assess whether the U.S. central bank may maintain its hawkish stance after a slew of mixed U.S. data, Bloomberg reports.

- Morgan Stanley expects Endeavour Mining to produce 318,000 ounces of gold during the third quarter, or 6% below its previous forecast, as the company provisions for a worse-than-expected rainy season in Senegal, impacting output at Sabodala-Massawa. The group also fine-tuned volume estimates at other mines, including Ity and Hounde, and lifted its all-in-sustaining cost (AISC) to $1,040 per ounce to reflect the lower production base. Therefore, its third-quarter EBITDA (earnings before interest, taxes, depreciation and amortization) now stands at $269 million versus the prior estimate of $296 million, compared to the consensus of $295 million.

- Gatos Silver released an updated mineral reserve estimate and plan for its Cerro Los Gatos mine, after the company announced in January 2022 that the 2020 technical report should not be relied upon, estimating 30%-50% of the metal content had been overstated. The updated estimate includes decreases of 32% silver, 37% zinc, 36% lead, and 35% gold after accounting for depletion. The revised plan has a mine life to 2028, with a 5% net present value (NPV) of $377 million on a 100% basis.

Opportunities

- Financing decisions are a key component to advancing a project in the mining sector, with the most common sources of financing being debt, equity, private equity, a royalty or stream on the asset, or a combination of these alternatives. Over the past decade, royalties and streams have become increasingly more mainstream, offering a competitive source of financing for mine operators. Further to the benefits to mine operators, these arrangements are beneficial to royalty and streaming companies, providing them exposure to the asset, usually for life of mine, and thus allowing them to share in future growth from project expansions, exploration potential and upside from commodity price increases, with more limited exposure to inflation.

- The World Platinum Investment Council (WPIC) estimates if China imports platinum at its current pace, the market will register a deficit of 800,000 ounces in 2023, increasing to 1 million ounces by 2025. That said, the WPIC has revised down automotive demand by 1.6% per year in its base case for the 2023-2026 period, albeit still up 8% per year. Mine supply growth has been moderated by 1% per year, and jewelry demand has lifted 4% per year, deepening annual deficits by 50,000 ounces per year.

- In a Bloomberg interview with Neal Froneman, CEO of Sibanye Stillwater, he noted that they expect the market to tighten further as some buyers seek to avoid Russian sourced palladium. MMC Norilsk Nickel PJSC currently supplies about 40% of world production from its Russian operations. Froneman said “We could see a real shortage of supply.” as platinum group metal producers in South Africa could lose 10% to 20% of their planned production if the current system of rolling power cuts are maintained by Eskom.

Threats

- Ibrahim Traore, a military officer in Burkina Faso, has formally announced a countercoup, removing the prior military leader, Paul-Henri Damiba, who took control of the government in January 2022. The new military leader has announced the government and constitution has been dissolved, and the country's borders have been closed. Reportedly, the actions of the military are in response to increasing terrorist activity. IAMGOLD has not yet made a statement on its Essakane mine, which operates in Burkina Faso—the mine is unlikely to be directly affected by political instability, although logistics and productivity could be temporarily negatively affected. Essakane represents the overwhelming majority of IAMGOLD's current cash flow, and potential operating disruptions could materially impact the company's financial position.

- Victoria Gold (VGCX) production in the third quarter of 50,028 ounces met BMO’s expectations, but a conveyor failure at the end of the quarter will weigh on the fourth quarter with two to three weeks of expected ore stacking downtime. VGCX has retracted its annual guidance (previously 165,000 ounces) until the conveyor is back online; the company lowered its fourth quarter production estimates and now forecasts full-year production of 150,000 ounces, down from 159,800 ounces.

- Upon reflection, investors expressed their disapproval of the $27.5 million Gold Royalty transaction with Nevada Gold Mines this past week by selling the stock down more than 14%. Gold Royalties paid the consideration by issuing 100% of the proceeds in newly registered stock to Nevada Gold Mines at a deemed price of $2.93.

About the author