Strengths

- The best performing precious metal for the (past) week was platinum, up 3.74%. The Gold/Copper ratio has been on an upward trend since mid-March as gold has outperformed copper. The ratio is now approaching the recent highs seen last July when recession fears were rising but well off the levels seen in early 2020. Gold has seen support from safe haven demand and falling U.S. yields, while copper has seen more sideways performance as investors weigh up global economic growth risks against supply disruptions and China’s reopening.

- Royal Gold reported first-quarter stream segment results. Stream sales were 60,800 ounces versus the consensus of 57,000oz (6% higher), with stream deliveries of 57,800oz, 1% higher than the consensus. Overall, gold inventories were 11% lower at 25,500oz.

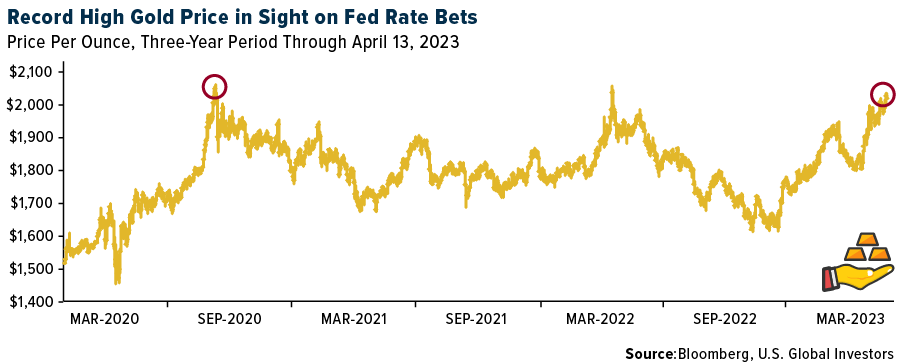

- Gold extended gains above $2,000 an ounce, inching closer to a record as investors awaited U.S. inflation data that may offer fresh insight into the Federal Reserve’s next rate move. Bullion rose for a second day to trade about 3% below a record set in 2020.

Weaknesses

- The worst-performing precious metal for the week was gold, but down just 0.36%. Global platinum production declined by 5.7% to 5.8 million ounces (moz) in 2022, with combined output from South Africa and the U.S. declining from 4.7moz in 2021 to 4.4Moz in 2022. Looking ahead, global platinum production is expected to recover in 2023, up by 3.1% to 6.1moz. While South Africa is expected to contribute the majority of this growth, a marginal increase is also expected from the U.S. In South Africa, growth will be mainly supported by an expected increase in production from Impala, coupled with Sibanye Stillwater’s Marikana and Rustenburg Complex.

- Evolution Gold provided an update on the March quarter, which highlighted gold and copper production that was below expectations at 163,900oz and 9,700 tons, respectively. Annual guidance was moved from approximately 720,00oz gold at cash costs of A$1,240/oz to approximately 660,00oz gold at cash costs of A$1,390/oz.

- K92 Mining announced first-quarter production of 21,500oz gold, 1.7 million pounds copper and 29,900oz silver. The company expects second-quarter production to be moderately below budget, with the second half being the strongest and 2023 production within the bottom half of the guidance range.

Opportunities

- A story on Bloomberg highlights potential opportunity for gold to take investor confidence up a notch in terms of technical signals to watch for next week. Over the last three years, gold has traded above $2,000 per ounce three times but in the previous two instances, gold didn’t stay above this technical hurdle for very long before the rally failed. The longest span was five days, so with the current price run we are now on four days above $2,000. While it’s only a technical trading level, gold bulls would love to have $2,000 become the new floor in gold prices and not the ceiling.

- Scotia expects higher gold prices to boost margins and cash flow as companies begin to report results later this month; however, much of the benefit from higher metals prices is likely to fall into the second quarter (assuming metals prices remain at elevated levels).

- Newmont Corp. has increased its record offer for Australian competitor Newcrest Mining Ltd. to A$29.4 billion ($19.5 billion) to create a precious metal powerhouse. Two months after Newcrest rejected Newmont's $17 billion all-stock offer, the amended deal would give Newcrest shareholders 0.4 shares in the world's largest gold miner. Newcrest can pay a $1.10 franked special dividend under the arrangement. That is A$32.87 per share, a 46% premium to Newcrest's undisturbed price before February's offer. It could be the largest gold mining takeover.

Threats

- British money supply economist Simon Ward correctly predicted sky-high inflation before anyone else did is sounding the alarm that central bankers have raised interest rates too far as money supply in the U.K., eurozone and U.S. is collapsing. When the pandemic hit central banks’ vast quantitative easing programs and sharp rate cuts led to double-digit money supply growth in the U.S. and Europe. A year later we had double digit inflation. Today, money supply is plummeting. M1 narrow money, cash and overnight deposits, is negative for the first time since the eurozone block formed in 1999. M2 growth. M2, which measures cash in circulation, plus dollar in the bank and money market accounts, in U.S. recently contracted and suggest recession, disinflation and deflation.

- Bank of America believes Kinross could be weaker-than-expected on continued inflationary cost pressures and seasonal production weakness at the North American mines, and tie-ins for the Tasiast expansion to 24,000 tons per day, which Kinross expects to reach design throughput by mid-year. Kinross has the highest debt in their coverage and will be susceptible to any downward pressure on the gold price.

- The largest cyclone to hit Western Australia in over a decade is anticipated to impact Newcrest Mining; it may be the worst storm in over a decade. It will be category 4 and operations at the Telfer gold mine are on pause. Hopefully this cyclone will not create significant damage, people will stay healthy and business will return to normal.

About the author