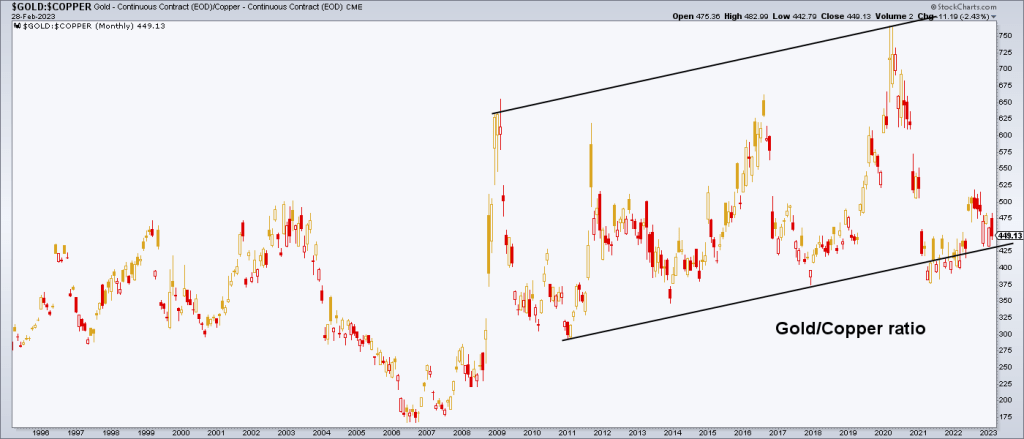

We projected a rally to run from Q4, 2022 to or through Q1, 2023. It is technically intact with the Gold/Copper ratio trending down since last summer. What’s more, the global market rally has been led by Doctor Copper and companies that dig Cu out of the ground. So the Gold/Copper ratio has trended down the whole way, even as gold has ground out uptrends vs. some other commodities and stock markets.

However, dialing out to the big picture (monthly chart) or the Gold/Copper ratio, we find logical and hysterical spike upward amid the acute phase of the pandemic crisis in 2020 and the equally logical crash right back down to trend, with a little shakeout wiggle room below the lower channel line in 2021.

Then came a recovery in 2022 to fill a gap (I think gaps are pretty important, even on a monthly ratio chart, because they are emotional flash points and in the financial markets emotion is usually addressed sooner or later). The 2022 recovery in the Gold/Copper ratio oh so logically came as the inflation trades started to roll over. Now, it is back to trend with the risk on Doctor Copper’s side of the boat and the potential reward on old man Gold’s side.

What this will mean for the wider markets if the Gold/Copper ratio rises anew would be anti-inflationary, anti-cyclical and pro-contraction. In other words, as I’ve been saying for a couple months now, “the [Bob] Hoye Squirrel may actually find his post-bubble contraction nut” * this time after several failed nut finding expeditions over the previous 20 years. It could be, well, epic (and painful if you’re on the wrong side of it, or FOMO inducing if you are not actively on the right side).

There are other positive cycle signals in play that have been guiding the Q4-Q1 rally theme, and the Gold/Copper ratio has not yet begun a new bull move. But on a risk vs. reward basis, that which sits on the lower line on the chart above (gold during the post-2020 inflation trades) is much less risky than that which pinged the upper line (gold during the 2020 hysteria). I love simple pictures. This one is projected to resolve badly for cyclical, inflation sensitive and economically positive areas and positively for those few areas that are ‘counter’ all that. Keep the highest quality gold stocks in mind, for one.

* Bob Hoye is someone from whom I long ago learned some core reasoning about why gold/gold stock promoters should be avoided and proper gold mining fundamentals considered. A post-bubble contraction, not an inflationary macro would be the preferred environment for holding gold mining stocks longer than the cyclical trades we’ve had since 2011. The Gold/Copper ratio above is among the indicators toward such an environment.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by Credit Card or PayPal using a link on the right sidebar (if using a mobile device you may need to scroll down) or see all options and more info. Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter@NFTRHgt.

About the author