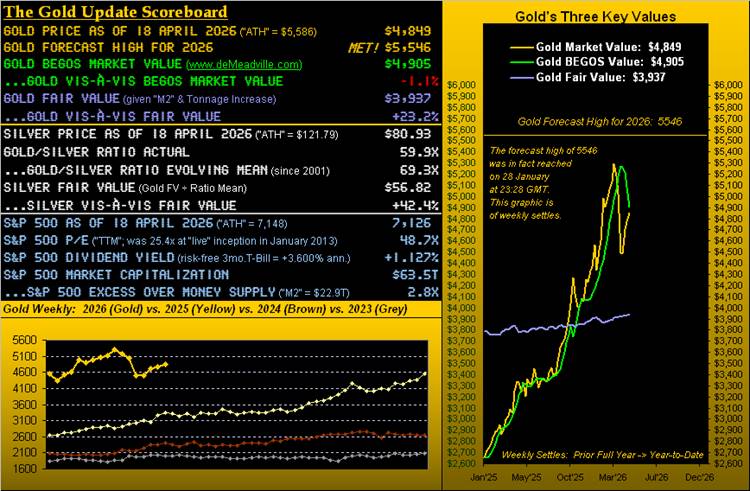

The Gold Update by Mark Mead Baillie — 857th Edition — Monte-Carlo — 18 April 2026 (published each Saturday) — www.deMeadville.com

“Gold’s Means Reversion; S&P’s Record Excursion“

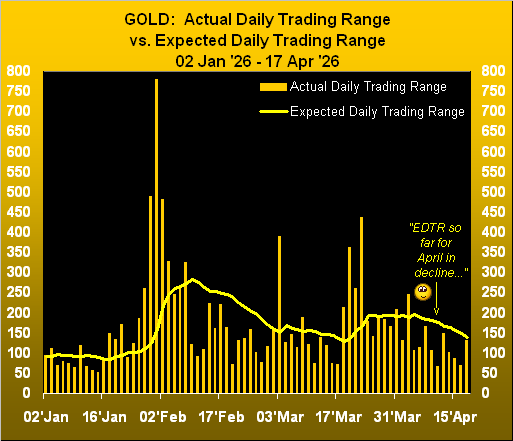

Our recent missives have underscored Gold’s volatility as having been reduced from vehement to narrow. Here at deMeadville, we are keen watchers of one of the most overlooked metrics in trading: range, notably that which is expected for each ensuing trading day, regardless of direction. ‘Tis why on the website we’ve the Market Ranges page which embodies the year-over-year “EDTR” (“Expected Daily Trading Range”) for each of the eight BEGOS Markets (Bond, Euro/Swiss Franc, Gold/Silver/Copper, Oil, S&P 500).

Knowing the EDTR — be it for any of the BEGOS Markets or even equites — helps to keep one’s feet on the ground. For example, how many times across the S&P 500’s post-COVID six-year rally have we heard some yahoo boastfully exclaim: “Oh! I just bought XXX ’cause after earnings today it’s gonna fly” … only to find some days later that it never got very far off the tarmac. (You ought have had a sense of expected range there, Bunky).

Either way, with Gold having settled its week yesterday (Friday) at 4849, the compressing of range continues. The following graphic is our year-to-date view of Gold’s actual daily trading ranges (the bars) vis-à-vis each day’s EDTR (the line). Clearly during April, daily range has been narrowing. In fact, specific to the past 10 trading days’ ranges, none have reached up to the EDTR, even as ’tis been contracting:

Moreover, in each trading day’s Prescient Commentary we cite the stance of the BEGOS Markets relative to their “Neutral Zones”: be a market higher or lower, if its price is within that day’s Neutral Zone, we deem the day as essentially “unchanged”. And across Gold’s past 10 trading days, five have concluded within the Neutral Zone.

“It’s kinda like that Chris Isaac song, right mmb?”

Squire is referring to the ’95 tune about the girl with dirty blonde hair wearing a taupe miniskirt whilst standing with her overnight case in the Greyhound bus station: “Goin’ Nowhere”.

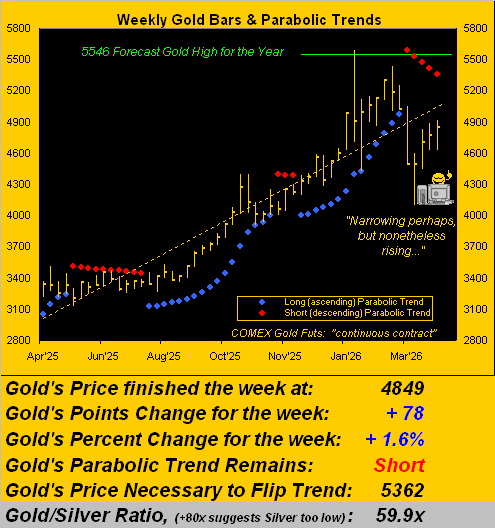

Not that Gold’s hasn’t gone anywhere. Price year-to-date has spanned from 5586 (our forecast high 5546) down to 4100 (our forecast low 4136), a range of -1486 points (-26.6%). ‘Course, with 179 trading days remaining in 2026, ’tis far too soon to “take credit” that we “nailed it”. But range has been nonetheless narrowing. Both of the past two weeks have recorded notably narrower trading ranges (262 and 292 points chronologically) than those of the three prior (571, 501 and 413 chronologically). So to Gold’s weekly bars we go, the red-dotted parabolic Short trend having completed its fifth week, such stance having commenced back on 16 March when priced opened at 5010:

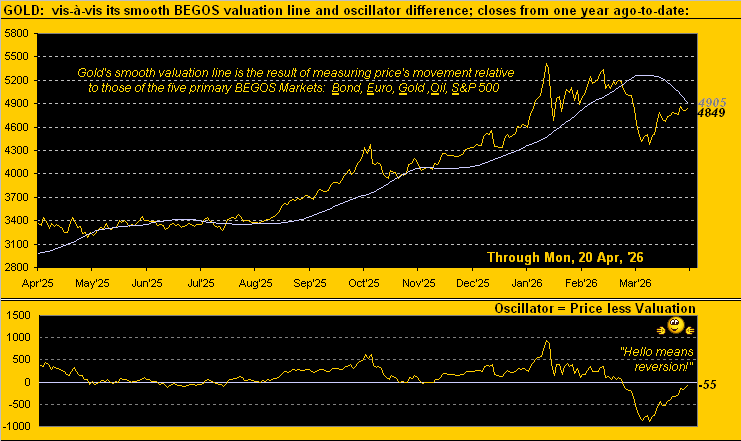

Meanwhile from the “Means Reversion Dept.” we’ve this updated graphic of Gold from a year ago-to-date along with its smooth valuation line born of price’s movement relative to those of the five primary BEGOS Markets as therein noted. To reprise, ’twasn’t that far back on 26 March (only 15 trading days ago) that Gold settled at a record -886 points (-16.8%) beneath valuation. Now as we below see, ’tis just -55 points “low”. As we oft quip, “Means reversion is a beautiful thAng” … (however, when it finally hits the S&P 500, ’twill be horrifying, perhaps per our wrap). Here’s the Gold graphic with price nearly having reverted back up to valuation, (which is a swifter valuing of Gold than is Fair Value by which Gold remains quite high):

Now we just made reference to the S&P 500, the mighty Index overvalued, overbought and overhyped beyond belief.

“Well, mmb, they say the war is winding down…”

Squire, it puts us in mind of the old saying “There’s been a sudden breakout of peace”, albeit so called “cease fires” carry a rather temporary tone. And now we’ve just learned the Straits of Hormuz have again been “closed”.

Regardless, ’twas but seven missives ago on 28 February that we penned “… in setting this morning to write our 850th consecutive Saturday missive, we’ve just learned of the commencement of USA/ISR attacks on IRN…” The S&P then was 6879, Oil 67.29 and Gold 5296. Today, Gold is -8% lower at 4849, Oil +27% higher at 85.57 (and at one point was +75% higher at 117.63) and the S&P now +4% higher at the record closing high of 7126. Were not higher energy prices to wreak havoc on corporate earnings?

To be sure, only the single war month of March is included in this Q1 Earnings Season, which whilst still quite young for the S&P 500 has thus far been excellent: 30 constituents have reported, of which 25 — that’s 83% — have bettered their bottom lines over Q1 of a year ago. Going as far back as 2017, the average quarterly year-over-year improvement is 66%. ![]() “Happy Days Are Here Again”

“Happy Days Are Here Again” ![]() –[Ager/Yellen, ’29]. However, problematic as we’ve time and again mentioned is that the nominal level of earnings need really to double toward supporting the stratospherically high level of the S&P; the median increase thus in Q1 earnings Season far is “only” +20% — which actually is great — but ’tis not the +100% “requisite” to get earnings in line with price.

–[Ager/Yellen, ’29]. However, problematic as we’ve time and again mentioned is that the nominal level of earnings need really to double toward supporting the stratospherically high level of the S&P; the median increase thus in Q1 earnings Season far is “only” +20% — which actually is great — but ’tis not the +100% “requisite” to get earnings in line with price.

Yet, so happy are the S&Pers that they’ve driven up the Index to now being (by our technical cocktail of Relative Strength, Stochastics and John Bollinger’s Bands) extremely “textbook overbought”, the price/earnings ratio a laughable 48.7x, with a pitifully puny yield of 1.127%, whereas noted in the opening Gold Scoreboard, the three-month annualized U.S. T-Bill yield is 3.600%. Again, that’s more than triple the S&P’s dividend return and you shan’t lose your money … at least not until the U.S. Treasury defaults and/or the Buck gets nixed as the world ‘s reserve currency. For you WestPalmBeachers down there, that is why you want to own Gold.

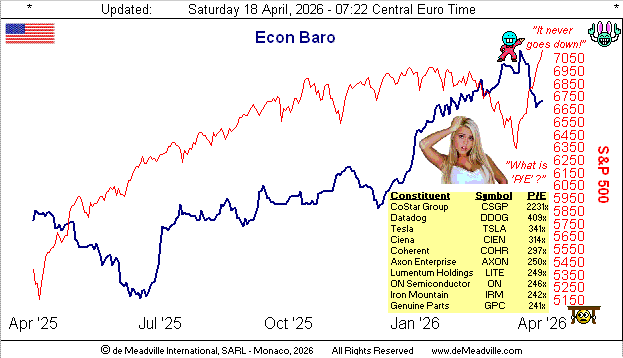

Meanwhile, to the suddenly sagging Econ Baro we go, ignored ‘natch by an S&P all aglow, the high P/Es list pulled from the website you know:

Indeed of the past week’s 11 incoming Economic Barometer metrics, just four improved period-over-period, notably therein both the New York State Empire and Philly Fed Indices for April. But March’s Producer Price Index (barring neither you eat nor drive) was again quite inflationary, the +0.5% pace annualized at +6.0% being ever so far afield from the Federal Reserve’s +2.0% target. Why, even FedGov Stephen “The Mirage” Miran on Thursday reduced his rate cuts projection for this year from four to perhaps three, inflation having become (hat-tip Barron’s) “more complicated even before war with Iran began”. Yo, Mirage Man: instead, how ’bout a rate increase or two, hmmm?

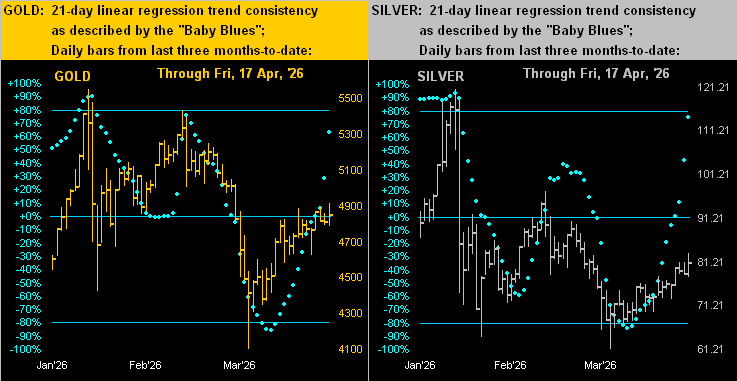

And speaking of increases, even as trading ranges narrow, our baby blue dots of regression trend consistency have been well on the rise for the precious metals as we below see for Gold on the left and for Silver on the right by the day across the past three months. Recall “Follow the Blues instead of the news, else lose yer shoes…”? Indeed you do:

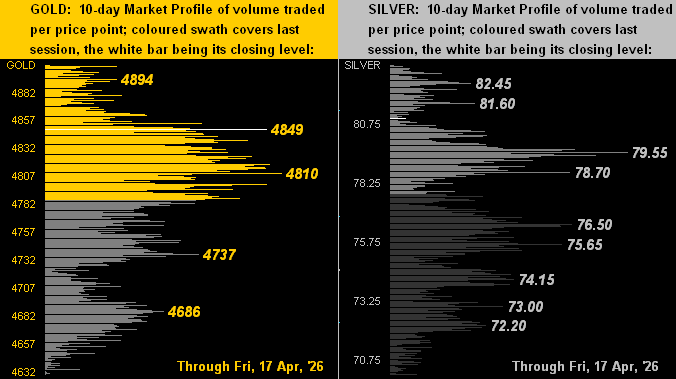

Too, we’ve the 10-day Market Profiles for Gold (below left) and for Silver (below right). Price is supportively-positioned in both cases, the yellow metal by the 4800s and the white metal basically by the 79 handle, her having just settled a completed week above 80 (at 80.93) for the first time since that ending 13 March. Cautiously however by the Scoreboard, whereas Gold is presently +23.2% above Fair Value (3937), Silver is +42.4% above same (56.82). Hang in there, Sister Silver…

Toward our wrap, here’s the stack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 5586 (29 January 2026)

2026’s High: 5586 (29 January)

Gold’s All-Time Closing High: 5411 (28 January 2026)

The Weekly Parabolic Price to flip Long: 5362

10-Session directional range: up to 4908 (from 4628) = +280 points or +6.1%

Gold’s BEGOS Market Value (from our opening “Scoreboard”): 4905

Trading Resistance: vis-à-vis the Market Profile, 4880 – 4910

Gold Currently: 4849, (expected daily trading range [“EDTR”]: 135 points)

Trading Support: vis-à-vis the Market Profile, the lower 4800s

10-Session “volume-weighted” average price magnet: 4785

2026’s Low: 4100 (23 March)

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3937

The 300-Day Moving Average: 3863 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

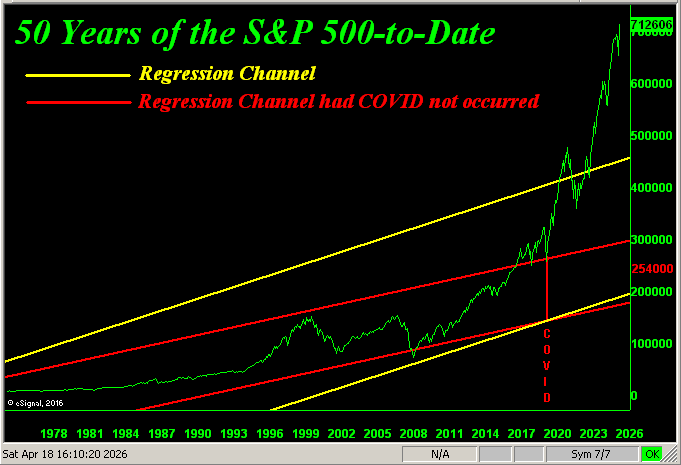

So as Gold gathers itself via means reversion, the S&P 500 has made a record high excursion. But is it really that impressive? After all, year-to-date Gold is now +11.9%, whereas the S&P is comparably +4.1%. Still, truth be told, both markets are fundamentally overvalued, Gold per its Fair Value and the S&P by its high (understatement) P/E. Gold indeed reverted well back down toward Fair Value when price plummeted to 4100 just this past 23 March, (Fair Value then 3890). But what about for the S&P? How far would price have to fall to bring the present dividend yield of 1.127% up to match the aforementioned T-Bill’s 3.600%? We put the question to “AI” (“Assembled Inaccuracy”), which responded thus:

- “Based on recent market data as of mid-April 2026, the S&P 500 would need to fall approximately 4,586 points to increase the dividend yield from 1.127% to 3.600%.”

Naturally, we followed-up with the math to find ‘twould be an S&P 500 “correction” of -64% to 2540 — right in the heart as below marked of the extrapolated “had COVID not occurred” red regression channel … just in case you’re scoring at home:

Query: How are those Gold n’ Silver holdings workin’ out for ya?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

deMeadville. Copyright Ⓒ 2010 - 2026. All Rights Reserved

About the author