Here is our latest article on bank safety: Bank Of America Is In Trouble.

We have already written an article debunking BAC’s own claim that its balance sheet and overall position have improved massively since 2009. And, as we concluded, there are issues sitting within BAC’s balance sheets that could lead to worse consequences than what they experienced during the Great Financial Crisis.

In this article, we take a fresh look at the bank and its FY2025 financial results. And, it does not look any better.

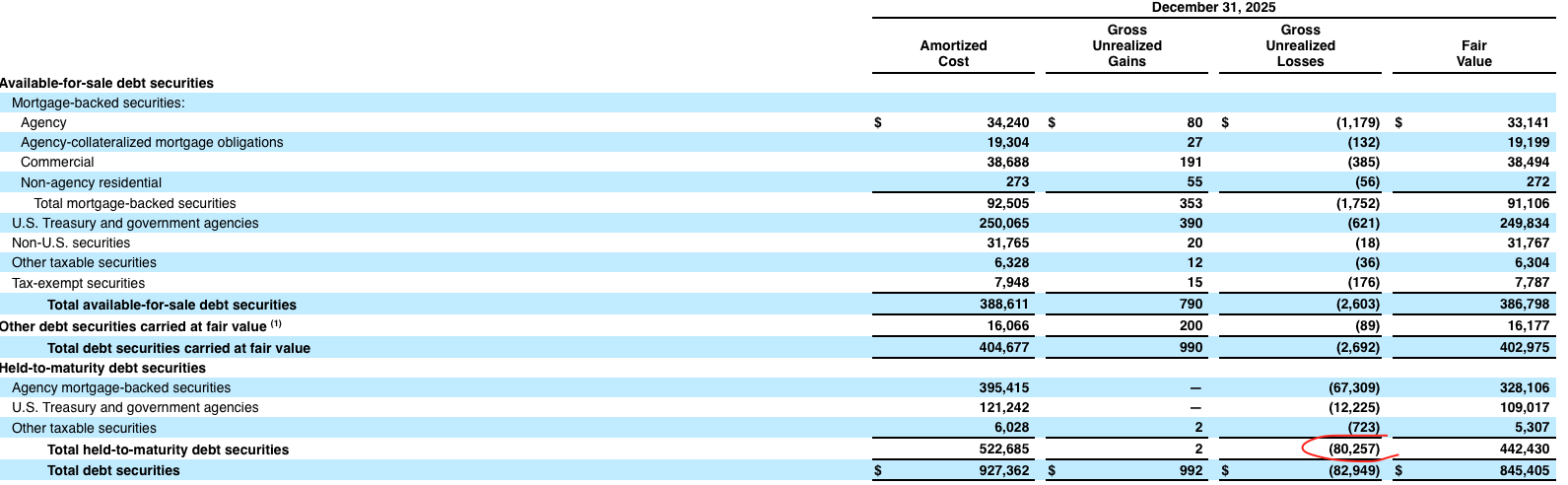

Underwater HTM bonds

BAC has a very large unrealized loss in its HTM bond portfolio. As of the end of 2025, this loss was as high as $80.3B, which accounts for 40% of the bank’s CET1 capital.

Source: Company data

Source: Company data

Needless to say, these deeply underwater HTM bonds cannot be sold or even repositioned without realizing a loss equal to roughly 40% of the bank’s capital. As such, they cannot be called “liquidity sources.” Notably, according to the Florida Atlantic University screener, BAC has the highest unrealized loss from securities in absolute terms. This says a lot about BAC’s risk management in that such a large share of low-yielding securities implies BAC was effectively taking a “lower-for-longer” rate bet - more reminiscent of a hedge fund than a traditional banking institution.

High share of commercial loans, CRE lending, and international exposure

As of the end of 2025, total commercial loans account for almost 60% of BAC’s total credit portfolio.

![]()

Source: Company data

In one of our previous articles, we highlighted major risks associated with commercial and industrial (C&I) loans. In particular, according to S&P Global, large U.S. corporate bankruptcies surged in 1Q25, reaching their highest 1Q level since 2010. S&P noted that companies now face refinancing maturing debt at significantly higher interest rates than original issuance levels, creating ongoing challenges - particularly for firms with weaker balance sheets. This directly impacts the largest banks like BAC, as they primarily serve large corporations.

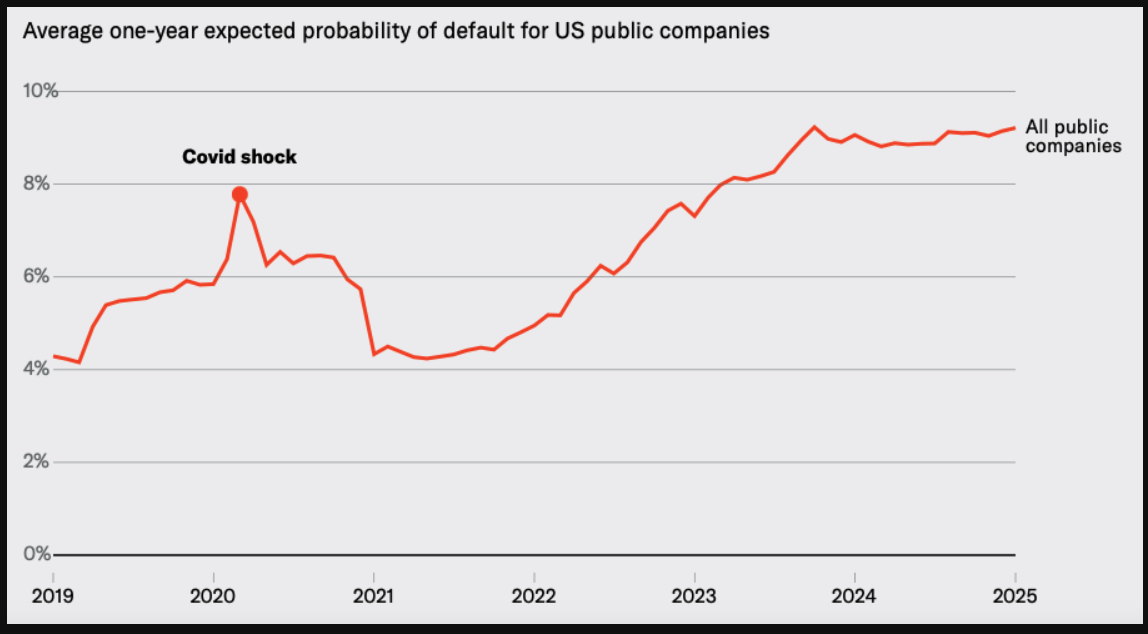

More critically, Moody’s reports that default risk among approximately 5,500 U.S. public companies has reached 9.2% - the highest level since the Global Financial Crisis. Default risk (probability of default) measures the one-year likelihood of a company defaulting.

![]()

Source: Moody’s

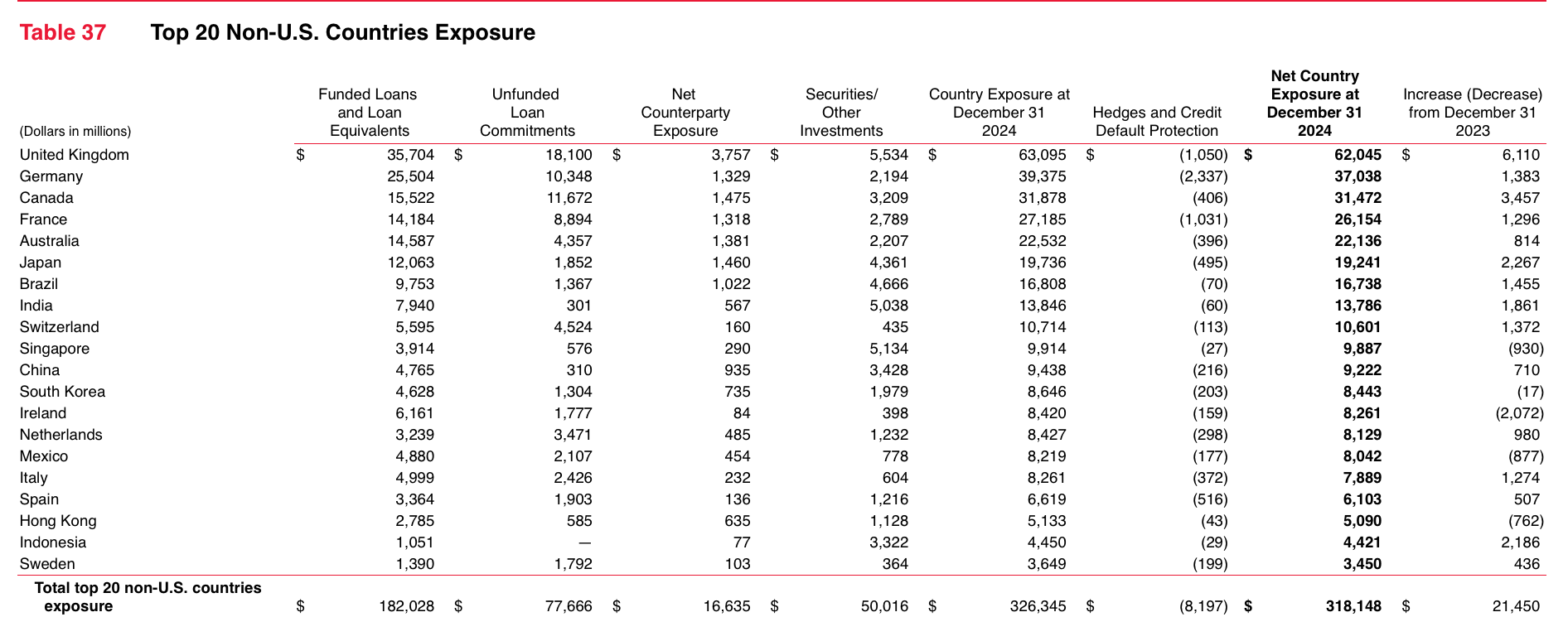

As shown below, BAC also has net international exposure as high as $318B (YE2024 data).

Source: Company data

Here’s what the bank says about its non-U.S. exposure:

Our non-U.S. credit and trading portfolios are subject to country risk. We define country risk as the risk of loss from unfavorable economic and political conditions, currency fluctuations, social instability and changes in government policies...

This suggests these loans and other commitments are subject not only to credit risk, but also to FX risk and other sovereign risks as well.

Finally, BAC has $67B of CRE loans and, while their share of total loans is smaller than at some other banks, this is still significant - especially given that academic papers we discussed in previous articles suggest that up to 20% of CRE loans could default in the next 2-3 years as the refinancing window accelerates. These losses would be another hit to BAC’s capital.

Significant exposure to unsecured retail lending

BAC has a credit card portfolio of more than $106B and an auto loan book of $55B.

Source: Company data

We have written extensively about the ongoing weakness in the U.S. consumer credit market and the fact that the sector’s delinquency ratio is only 100-200 bps below the GFC peak. BAC is not an exception: its net charge-off rate for credit cards was 3.68% in FY2025. Obviously, if even a mild deterioration in the job market occurs, credit-card asset quality would deteriorate further-and BAC would be hit as well.

Auto loans are another topic we regularly discuss, and the delinquency ratio in the segment has nearly reached the GFC peak. BAC’s exposure is not as large as that of auto-focused lenders, but it is still another potential source of pressure on earnings- and, eventually, capital.

Weak operating efficiency and a high share of volatile market earnings make BAC’s operating model fragile

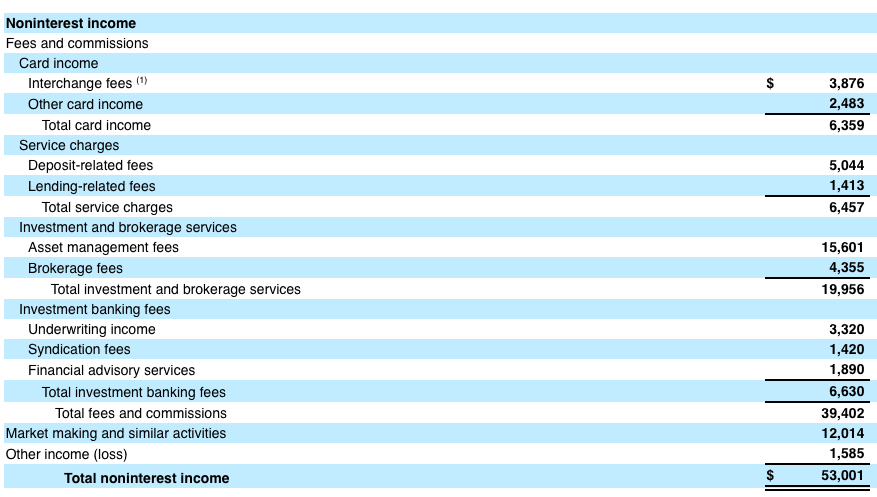

Below is a breakdown of BAC’s sales and trading revenue and its noninterest income for FY2025.

![]()

Source: Company data

![]()

Source: Company data

As you can see, BAC generates roughly a quarter - possibly closer to a third - of its total income from market-related activities: investment banking, asset management, brokerage, and market making. Sales and trading revenue was very strong in 2025, but these sources of income are volatile. Importantly, despite strong income generation from sales and trading and other market-related activities, the bank’s efficiency ratio was weak at 62%.

If a crisis occurs, these volatile and cyclical revenue streams could drop quickly, as it typically takes much longer to cut expenses. As a result, BAC could post an operating loss even before accounting for credit losses.

BAC no longer has a low deposit beta

For many years, BAC enjoyed near-zero deposit costs thanks to its franchise. However, there has been a major shift lately and, as shown below, BAC’s average deposit cost was 2.14% in 4Q25. That’s quite high for a bank some considered “too big to fail” (TBTF).

![]()

Source: Company data

Capital adequacy ratios are weak for this business model

Source: Company data

As of year-end 2025, BAC’s CET1 ratio was as low as 11.4%, down from 11.9% in 2024. In our view, this is a weak CET1 ratio given BAC’s loan mix (high exposure to commercial loans and unsecured lending) and its large share of underwater securities. In addition, BAC has said its minimum regulatory requirement is likely to be around 10.2%, which means the capital cushion is very small. By comparison, the banks we recommend to our clients have CET1 ratios of 15%+.

Bottom line

Believe it or not, there are more major issues on the larger bank balance sheets as compared to smaller banks, which we have covered in past articles. Moreover, consider that there was one major issue which caused the GFC back in 2008, whereas today, we currently have many more large issues on bank balance sheets. These risk factors include major issues in commercial real estate, rising risks in consumer debt (approaching 2007 levels), underwater long-term securities, over-the-counter derivatives, high-risk shadow banking (the lending for which has exploded), and elevated default risk in commercial and industrial (C&I) lending. So, in our opinion, the current banking environment presents even greater risks than what we have seen during the 2008 GFC.

Almost all the banks that we have recommended to our clients are community banks, which do not have any of the issues we have been outlining over the last several years. Of course, we're not saying that all community banks are good. There are a lot of small community banks that are much weaker than larger banks. That’s why it's absolutely imperative to engage in a thorough due diligence to find a safer bank for your hard-earned money. And what we have found is that there are still some very solid and safe community banks with conservative business models.

So, I want to take this opportunity to remind you that we have reviewed many larger banks in our public articles. But I must warn you: The substance of that analysis is not looking too good for the future of the larger banks in the United States, and you can read about them in the prior articles we have written.

Moreover, if you believe that the banking issues have been addressed, I think that New York Community Bank is reminding us that we have likely only seen the tip of the iceberg. We were also able to identify the exact reasons in a public article which caused SVB to fail. And I can assure you that they have not been resolved. It's now only a matter of time before the rest of the market begins to take notice. By then, it will likely be too late for many bank deposit holders.

At the end of the day, we're speaking of protecting your hard-earned money. Therefore, it behooves you to engage in due diligence regarding the banks which currently house your money.

You have a responsibility to yourself and your family to make sure your money resides in only the safest of institutions. And if you're relying on the FDIC, I suggest you read our prior articles, which outline why such reliance will not be as prudent as you may believe in the coming years, with one of the main reasons being the banking industry’s desired move towards bail-ins. (And, if you do not know what a bail-in is, I suggest you read our prior articles.)

It's time for you to do a deep dive on the banks that house your hard-earned money in order to determine whether your bank is truly solid or not. You can feel free to review our due diligence methodology here, as well as all our prior public articles on the financial industry here: https://www.saferbankingresearch.com/articles

About the author