The battle between King Dollar and Tsar Ruble is on, and Russia’s efforts to dethrone the dollar have already lost. The ruble has already been knocked off its rickety wicker throne and has had its head kicked in. It’s just that brutal. King Dollar, on the other hand, hasn’t sat so tall in years.

While much of my writing has been dedicated to proving the unfathomable flaws of the Fed, I won’t capitalize on that here. The Fed’s dollar has already won Putin’s War at every turn. Even though I agree with all that has been written about how Putin and Xi have conspired to bring the dollar down to end US hegemony, Russia just lost the battle of currencies in one cataclysmic global miscalculation by Tsar Putin. (And he does rule like a tsar, making decrees almost in isolation and changing election rules to make sure he stays in power. Democracy in Russia has always been a bit like matryoshka dolls where every time you open up a new election result, you seem to find the same guy inside running things.)

US dollar becomes refuge in flight from war

I wrote the following yesterday in my Patron Post:

A black-swan event as big as the outburst of a war that could turn into WWIII clearly changes things. In fact, Putin’s War may have shifted the scenario for the collapse of the housing bubble because that collapse is based, in large part, on the collapse of the bond bubble; and Putin’s War may delay that. Recall that I have laid out as a caveat along the way the one thing that could save the US from parts of the collapse of the Everything Bubble (particularly the bonds part that interconnects with the Zombie Apocalypse and the Housing Bubble Collapse 2.0) would be if the US were to become “the best horse in the glue factory.”

And that is what we see happening right now — today especially, in fact. As money flees Eastern Europe and also seeks safe haven from around the world, it has poured suddenly into US treasuries, most notably today. That nullifies the effect of the Fed in backing out of the treasury market because suddenly robust foreign demand as large as the Fed, itself, is streaming in to hose up all those treasuries the Fed is walking away from. In a single day, that has delivered a plunge in bond yields. The question is how long this rush to safe havens that is also sucking money out of US stocks will last….

As that war on Europe’s eastern flank goes — the worst since WWII — so goes flight risk from the EU to secure US treasuries. In other words, US treasuries could be supported by being the best of the bad that is out there for some time if the war keeps driving money from all over the world into US treasuries….

The war changes the balance of how things will fall, pressing harder on some areas and providing relief in others…. Look at how fast US treasury yields plunged today (Tuesday as I am finishing this):

“U.S. Treasury yields fell sharply on Tuesday as investors remained focused on Russia’s attack on Ukraine and its potential impact on Federal Reserve rate hikes…. The yield on the benchmark 10-year Treasury note fell 11 basis points….” (CNBC)

In the world of normally stable US treasuries, an eleven-basis-point move within a day is a big plunge. I would argue, however, the move had less to do with the potential for Fed rate hikes and a lot more to do with capital flight. In fact, after stumbling into the knee-jerk response that the Fed is the cause, the article quoted catches its balance and moves on to identify the real culprit:…

“The attack has roiled global markets and seen investors look to safe haven investments like U.S. government bonds, pushing yields down. Until there is some sort of cease fire in Ukraine and the market no longer has to process additional sanctions and those impacts to the global economy, we will see geopolitical money flows continue to dominate the currency and bond markets, even with Fed Chair Powell’s testimony tomorrow and Thursday….”

This war, because of the greatest, fastest roll-out of global economic sanctions in history (see “Russian Ruble Turns to Rubble”) changes the economic landscape.

“The Everything Bubble Bust Pt. 4: Housing”

While that is just a smattering of the more in-depth content of this Patron Post, it frames the one point I want to make here, which is that the crushing of the ruble, as I described in the final section of another article this week (“Russian Ruble Turns to Rubble“), is a big boost to some parts of the US market even while these same sanctions that are crushing the ruble hurt other areas of the US and global economies, such as inflation by increasing shortages. That has the odd effect of making the dollar stronger internationally for buying foreign goods even as shortages mean it still becomes weaker internally for buying US goods.

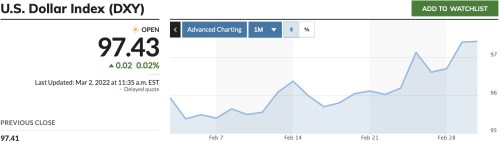

It should be no surprise that all this money fleeing Russia (to the extent that it can with sanctions locking most Russian money in place) and money fleeing some nations on Russia’s perimeter or nations that have a lot of financial connections with Russia is pouring into US treasuries as a safe haven in war like a horde of refugees. That is strengthening the dollar internationally like this:

Relative to other currencies, which is how the dollar index measures the value of the dollar, the dollar’s value is gaining.

There is much talk about how the sanctions being imposed on Russia will hasten the demise of the dollar’s role in the world economy, but today the dollar rides high. There is no sign of its abandonment as its safe haven appeal shines. The dollar-bloc currencies, helped perhaps by the commodity exposure are faring best.

The dollar is fairing well in foreign exchanges because other currencies are taking a bigger hit due to having more exposure to Russia:

Of note, the euro has been sold to about $1.1060. Among emerging market currencies, eastern and central European currencies are the weakest. The JP Morgan Emerging Market Currency Index is off for a third day, and the cumulative loss is around 3.5%. Equities in the Asia Pacific region were lower, snapping a three-day advance. South Korea and Australia were the exceptions.

Russia’s ability to damage the dollar has been caged

As I noted in my last article on the ruble turning to rubble, Russia has tried to protect the ruble against the dollar by hoarding gold. That didn’t work out well for them because the bear has been barred from its own bars of gold:

“Russia’s government was also frozen out of $630 billion in emergency funds, including foreign currency and gold, which Putin had set aside to fortify Russia’s financial system precisely for times of financial meltdown like this under sanctions or the weaponization of the US dollar.”

“Russian Ruble Turns to Rubble“

This is a point I’ve made many times in the past: while gold is often a good hedge, it is no hedge at all if governments confiscate it or freeze you out of it as they are more than capable of doing — just as we saw FDR do during the Great Depression. Because Putin brought the wrath of the world against himself, global markets rapidly fenced off a good chunk of Russia’s gold so that Putin cannot use if to trade in absence of being able to trade either rubles or dollars internationally. He’s fairly well sequestered within his own economy. In that kind of confinement, the best bet is the familiar “grow your own food,” and there he’s fairly well off once the crops come in, though there is likely still to be hunger in the streets due to the siege laid upon Russia by most of the world.

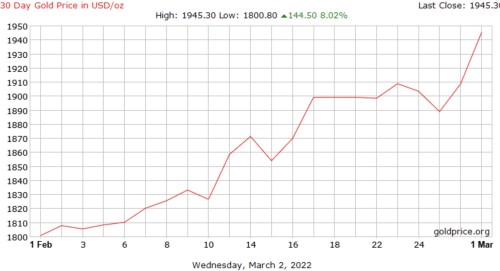

The cutting off of some of Putin’s gold certainly does not, however, hurt gold’s value for the rest of us:

Gold stalled near $1950 and is offered in Europe below $1930.

If anything, taking the potential for that gold to circulate out of play, only nudges scarcity up and supports the value of gold. The war has boosted gold even more because of the flight to safe havens, and it has done a lot for black gold due to coming shortages. Oil is now holding strong above $100/barrel.

April WTI rose to $111.50 before stabilizing. It finished last week near $91.60. US natgas is up about 3% after a nearly 4% advance yesterday. The same can be said for Europe’s natgas benchmark. It is matching and repeating yesterday’s gains, except there, we are talking about something closer to 26%-28%.

Iron is up, too, of course. War tends to blow through a lot of that, and it takes awhile to recycle it off the battlefield. (More significantly, sanctions limit any that comes from Russia.)

So far, Putin has been quarantined tighter than a COVID patient from infecting the dollar with the troubles he intended to bring.

Putin’s Asian anti-dollar alliance falls

An example of how tightly he’s been quarantined can be seen in his longstanding relationship with President Xi of China. Much has been made about the axis formed between Putin and Xi to help them end US dollar hegemony. Surprisingly, that alliance isn’t helping Putin any so far. The Chinese are nothing if they are not prudent:

Chinese banks are treading carefully and do not appear to be the escape-valve for Russia that was feared. Chinese business is concerned about payments, and this impacts not only Russia’s seaborne oil but also commodity shipments, including coal. China’s criticism of Russia has been ratcheted up. Foreign Minister Wang said China “deplores the outbreak of conflict between Ukraine and Russia, and yesterday for the first time officials seemed to refer to it as a war. Russia has been calling it a “special military operation.”

“Hey, Buddy, welcome to the club.”

“Hey, Buddy, welcome to the club.”

Putin doesn’t seem to have any friends right now, other than the KKK Klub I said he had joined earlier this week:

Putin and his buddies have now all been sanctioned by multiple nations, including the US, which puts Putin in the rare ranks of only three other national leaders — King Assad of Syria, Khameni of Iran, and Kim of North Korea, the KKK of the new axis of evil. Since they are coincidentally all Putin’s best buddies, with him being the last to join and make a foursome, they make a cozy country club of maniacs.

Putin may get support there, but he has received an almost stunning lack of support from China. China has not even seized the opportunity to attempt a similar takeover of Taiwan as some expected to come next if this was a schemed battle of the new axis nations. There is not much evidence to support that conspiracy. Though China flew some fighter jets into Taiwan’s air space, we haven’t heard many rumblings above the noise of those menacing jets. It does not appear, so far, that China is going to capitalize on the moment militarily, but the main surprise is that China is not assisting the Russian Ruble or the Russian leader, but is backing away in trade to contain any damage to itself.

Concerns about use of this war by China or Russia to break the dollar seem overblown. If there was such a conspiracy, China must have realized quickly that Russia has already lost that battle and hasn’t wanted to join a lost cause. Because of such cautious self-containment, Putin’s War is not hurting the Chinese Yuan in its global status as a new reserve/trade currency:

The greenback is slightly firmer against the Chinese yuan for the second consecutive session, but it remains a little lower for the week.

The damage to yuan has been mitigated by Chinese prudence.

US still steaming Fed ahead

As for the war’s impact on Fed actions, the market is only speculating minor changes:

The Fed funds market has gone from an 80% chance of a 50 bp hike on February 10 to slightly less than a 100% chance of a 25 bp increase. The market had been divided between 150 bp and 175 bp in hikes this year. Now the market is pricing in almost 125 bp. Despite some recent US data and favorable optics, including yesterday’s stronger than expected gain in the ISM and new orders, the US economy appears to be slowing sharply. The Atlanta Fed’s GDPNow tracker puts growth at zero this quarter, down from 0.6% in late February.

The final statement is, again, confirmation of my prediction last year that the US economy would be sliding into recession by the start of 2022. I actually pegged the end of 2021, but this is close enough for horseshoes and hand grenades, the latter of which seem to be flying around in greater abundance than rubles right now.

None of this is to say the dollar’s days are not numbered, but it won’t be Russia that took it down. Rather, the ruble has been taken down due to Putin’s miscalculation and the sweeping global response. The dollar stands to fight another day, but the world likely moves out of this to greater global cooperation. As said in closing my last Patron Post,

The next big answer to our problems, in my estimation, will be a global central-bank economic scheme to answer a global cataclysm, and what sets that up now better than the global sanctions of this new war? On one side of the equation, they have made things tougher for every nation in a world already struggling economically due to the plague and our global responses to it, thereby begging for global solutions to these globally metastasizing problems. On the other side of the equation, the effectiveness of global response to contain Putin will demonstrate that global cooperation can work to punish imperial aggression.

I’m not suggesting this war was started with Putin’s cooperation as part of some conspiracy by any means; but it is here, and I believe many in the world are already begging for a more global economic system. For some, the effectiveness of global sanctions against Russian aggression will accelerate globalism. For other nations in conflict with the US, the desire to remove the risk of US dollar dominance when the dollar is weaponized, as it just has been, will increase their willingness to move to a globally controlled currency for international trade. I have some pretty good ideas of what that economic monster will look like, but that’s for another time far down the road.

Liked it? Take a second to support David Haggith on Patreon!

![]()

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!