Gold has started the new year off right, powering to nearly $1,850 an ounce Tuesday, Jan. 3, a six-month high. Silver followed suit, with March futures notching an eight-month peak of $24.22.

One-year gold and silver. Source: Kitco

One-year gold and silver. Source: Kitco

Among the factors favoring precious metals in 2023, are wobbly stock markets — the S&P 500 lost 19% last year in its worst performance since 2008, and analysts at major banks are forecasting that indices will retest their 2022 lows in the first half; higher US Treasury yields commensurate with still-hawkish monetary policies from most of the world’s major central banks; worries about economic growth in China, the US and the European Union; and the continued Russia-Ukraine war, in particular its effects on commodities supply.

After suffering for much of 2022 due to an elevated US dollar and higher bonds yields, gold has trended up since the beginning of November, fueled by market turbulence, rising recession expectations and more gold purchases from central banks underpinning demand.

“In general, we are looking for a price-friendly 2023 supported by recession and stock market valuation risks — an eventual peak in central bank rates combined with the prospect of a weaker dollar and inflation not returning to the expected sub-3% level by year-end — all adding support,” CNBC quotes Ole Hansen, head of commodity strategy at Saxo Bank.

“In addition, the de-dollarization seen by several central banks last year when a record amount of gold was bought look set to continue, thereby providing a soft floor under the market.”

The news outlet has two more analysts sounding even more bullish on gold. Eric Strand, manager of the AuAg ESG Gold Mining ETF, predicts that 2023 will see an all-time high and the start of a “new secular bull market,” based on the fact that central banks are adding more gold to their reserves, even setting a record in Q3 2022.

Juerg Kiener, managing director and chief investment officer at Swiss Asia Capital, noticed last month that the current market conditions mirror those of 2001 and 2008.

“In 2001, the market didn’t just move 20 or 30%, it moved a lot, the same in 2008 when we had actually a smaller sell-off in the market and the stimulus coming back in, and gold went from $600 to $1,800 in no time, so I think we have a very good chance that we see a major move,” Kiener told CNBC’s “Street Signs Asia” in late December.

“It is not going to be just 10 or 20%, I think I’m looking at a move which will really make new highs.”

Central bank buying

In November the World Gold Council said central banks bought 399 tonnes of gold in the third quarter, by far the most ever in a single quarterly period. According to the WGC, central banks globally added another 31 tons of gold to official reserves in October, putting central bank holdings at their highest level since 1974.

Source: QTR’s Fringe Finance

Source: QTR’s Fringe Finance

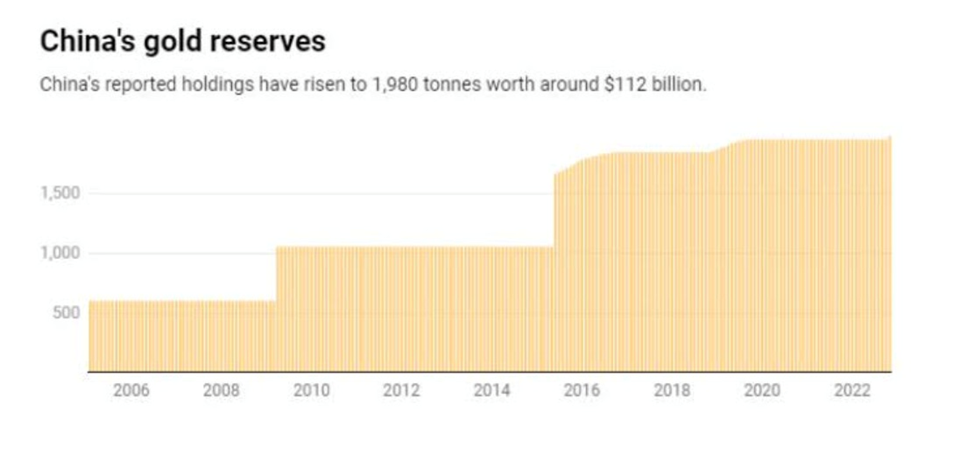

China, which is famous for not reporting its gold holdings, disclosed an increase in its reserves for the first time since September, 2019 — adding 32 tonnes worth around $1.8 billion, according to Reuters.

The coming cashless society and gold

On Dec. 29, the Financial Post reported central banks are hoovering up gold at the fastest pace since 1967. The article makes three important points about current central bank gold purchases.

First is it’s an indication that some nations want to diversify their foreign exchange reserves away from the US dollar. Adrian Ash, head of research at BullionVault, says it “would suggest the geopolitical backdrop is one of mistrust, doubt and uncertainty” after the US and its allies froze $300 billion of Russia’s foreign currency reserves through sanctions. The drastic tactic has prompted non-Western nations to ask, “Should we have exposure to so many dollars when the US and western governments can confiscate that at any time?”

Russia is the poster-child of de-dollarization and, ipso facto, gold accumulation. The Central Bank of Russia has reduced its holdings of US Treasuries to only $2 billion from more than $150 billion in 2012. At the same time, the CBR has increased its gold reserves by more than 1,350 tonnes, putting Russia in fifth place among the world’s top gold-holding countries, behind only France, Italy, Germany and the United States, which holds top spot at 8,133.5t.

The second point is regarding the central banks’ official figures, versus estimates of how much gold is actually being bought. As mentioned, according to the WGC, the third quarter 2022 saw 399 tonnes purchased, which is the largest three-month binge since quarterly records began in 2000. However, the reported purchases to the IMF and by individual central banks, for the first nine months to September, amounted to only 333t.

What accounts for the discrepancy? The Financial Post story says it can be partially explained by government agencies besides the central banks in Russia, China and others that can buy and hold gold without reporting it as reserves.

Certain central banks are simply failing to disclose their purchases, no doubt directed by top politicians. While China reported the first increase in its gold holdings since 2019, with a 32-tonne bump worth about $1.8 billion, the gold industry says Chinese buying is almost certainly higher.

Mark Bristow, chief executive of Barrick Gold, the world’s second-largest gold miner, said China had bought tonnes of gold around the high-200s mark, based on his discussions with numerous sources.

Which brings us to the third, and most important point of the article. Metals strategist Nicky Shiels, from MKS PAMP, a precious metals trading company, is quoted saying that gold prices would have peaked around $75 lower in November if the People’s Bank of China had only purchased 32 tonnes in November (i.e. it’s buying more). The inference being that China is deliberately suppressing the amount of gold it is buying, to keep the price low while it continues to stock up on bullion.

Supply constraints

The high demand for gold among central banks, and among investors hoping to get in early on the next gold bull run, is only one part of the demand side of the gold market equation. There is also the gold required for jewelry fabrication and for electronics. At AOTH we have shown that over the past three years, peak mined gold has been reached, meaning that the world’s gold mines cannot produce enough metal to meet demand, without recycling gold jewelry.

The gold market continues to experience tightness due to difficulties expanding existing deposits, and a pronounced lack of large discoveries in recent years.

Demand is equally important for other metals (especially the increasing need for so-called “green economy” minerals central to electrification and decarbonization, such as silver, copper, nickel, graphite, etc.) but we need to take an even closer look at supply.

According to a Dec. 30 article by Bloomberg, readily available warehouse inventories plunged 66% in 2022, with all key London Metal Exchange (LME) except nickel poised for an annual decline:

The London Metal Exchange will enter 2023 with the smallest available warehouse stockpiles in at least 25 years, setting the stage for future squeezes and spikes if demand turns out stronger than expected.

Available inventories of the six main metals traded on the LME plunged by two thirds in 2022, with aluminum’s 72% decline accounting for the bulk of the drop, while zinc shrank by 90%.

How much should we care about these warehouse inventories? Well, although most of the world’s metal is not warehoused, inventory levels are important because traders who sign a contract to deliver metal must have the physical metal under LME (or Comex) storage. We at AOTH therefore pay close attention to them.

One thing we noticed in the Bloomberg article is there is a divergence among those who believe that copper will fall into a deficit this year, or swing over to surplus. For example analysts at Goldman Sachs predict copper will hit a record-high $11,000 a ton within 12 months, while for BNP Paribas, prices will fall to $6,465 a ton by the middle of next year.

At AOTH we think those on the major surplus and dramatic price drop side of the equation don’t realize, or quite understand, that the copper market is facing a serious crisis of under-supply.

Some of the largest copper mines are seeing their reserves dwindle; they are having to slow production due to major capital-intensive projects to move operations from open pit to underground.

New deposits are getting trickier and pricier to find and develop. In Canada and the United States, there is a lot of anti-mining sentiment and politicians are beholden to these pressure groups. It can take up to 20 years to build a mine, after all the stakeholders (including indigenous peoples and greens) have been consulted and the many permitting requirements, at the Federal level in both countries, and the states and provinces have been satisfied. Overall it is getting harder, and taking longer, for new projects to be green-lit.

According to Goehring & Rozencwajg Associates, the number of new world-class copper discoveries coming online this decade “will decline substantially and depletion problems at existing mines will accelerate.”

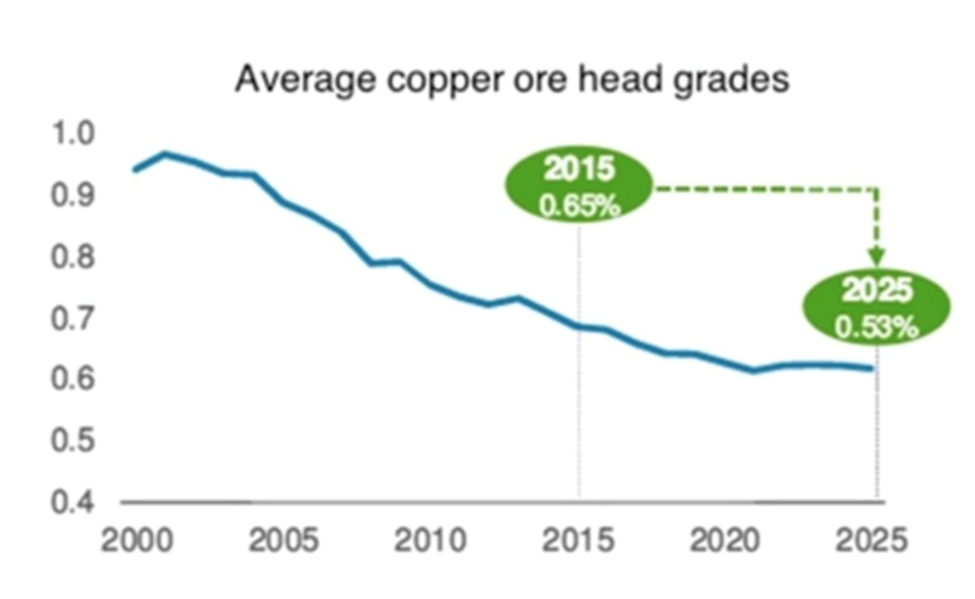

E&MJ Engineering stated in its outlook for copper production to 2050, “The trend toward declining orebody grades and continued development of the pursuit of existing operations to exploit lower grade deposits is likely to continue, in the absence of high-grade project discovery.

A decline in ore grade results in higher operating costs due primarily to the amount and depth of material required to be mined and processed to produce the same amount of copper product. It is no surprise that both GHG emission intensity and energy intensity increase as ore grade decreases. There is a point of inflection, where below an ore grade of around 0.5% copper, the intensity of both metrics rises sharply.”

Given that many mines are fast approaching, if not already tackling, similar grades, this is a pressing problem. In its fiscal year 2020 commodity outlook, BHP, the world’s third largest copper producer, estimated that grade decline could remove about 2 million metric tons per year (mt/y) of refined copper supply by 2030, with resource depletion potentially removing an additional 1.5 million to 2.25 million mt/y by this date.”

Along with technical issues such as falling grades/ deteriorating ore quality, there is also supply pressure from growing resource nationalism.

In Chile, a left-ward shift is a mark against the top copper producer as far as attracting mining investment. Although Chile’s constitutional assembly has rejected plans to nationalize parts of the mining sector, the government is now weighing how much to increase royalties; a decision is expected soon.

Peru’s President Pedro Castillo has proposed to raise taxes on the mining sector by at least 3%, which the country’s mining chamber says could cost US$50 billion in future investments. In December, Castillo dissolved congress hours before an impeachment vote, escalating a political crisis in the South American nation. Members of the constitutional court called the move, which is sure to increase doubts about Peru as a mining-friendly jurisdiction, a “coup”.

Given this and all the other supply challenges the copper mining industry faces, it’s hard to disagree with Glencore’s CEO Gary Nagle’s comment that, “There’s a huge deficit coming in copper.”

Why the upcoming copper supply deficit can’t be easily fixed

Commodities will boom

While copper, zinc and aluminum were all down more than 10% in 2022, they are poised for a rebound, driven chiefly by two factors: the rebound in demand from China, as it begins to re-open its economy following strict covid-related closures and restrictions; and the continued decline in the US dollar, which over the past year has fallen from around 114 at the end of September 2022, to the current 104.58 (commodity prices and the dollar generally move in opposite directions).

Source: MarketWatch

Source: MarketWatch

While a global recession in 2023 will obviously slow the demand for metals and other raw materials, there are those who say that commodity prices are expected to remain high, in everything from oil to copper to wheat.

The Washington Post published an op-ed by Javier Blas, former Bloomberg News reporter and Financial Times commodities editor, stating that The global economy is hard-pressed to satisfy its own commodity needs. Despite the past year of sky-high prices, the natural resources industry isn’t rushing to invest in more capacity to alleviate supply shortages. Without an investment boom, the only way to rebalance the market in the new year is through lowering demand.

We’ve heard this argument numerous times over the past year. To “kill demand” central banks hike interest rates, thereby incentivizing consumers to save, and discouraging homeowners and businesses from borrowing. But this tactic does nothing to alleviate supply interruptions caused, for example, by the war in Ukraine. Nor does it address the above-mentioned mine supply constraints. Blas rightly points out that, unless mining companies build more mines, which would increase supply, the only way to bring down commodity prices is by influencing them on the demand side, through interest rate increases. Yet, the impact will be limited, because even if macroeconomic forces ease some commodity cost pressures, microeconomic factors, such as low inventories and limited spare capacity, will keep prices higher than during past recessions in 2023.

Take a moment to digest what is being said here. Even if tight monetary policy works in suppressing inflation to some degree, in fact, even if they drive the world economy into a recession, as many predict will happen over the next year, that won’t be enough to cancel out prices being ratcheted higher due to tight supply conditions.

Blas wants us to understand that, while the Bloomberg Commodity Spot Index has fallen about 20% since its peak in June, the basket of goods is higher than it was during its peaks in 2008 and in 2011. For example, oil. While crude has fallen from an early 2022 peak of $125 a barrel, to about $80 at the end of the year, the price is well above the bottom set in December 2008 of $35/bl. The same applies to other commodities, leading to Blas’ conclusion: The commodities boom is taking a pause, not ending.

Source: Investing.com

Source: Investing.com

Conclusion

I agree with this assessment.

There are many reasons to be bullish on commodities and, a lot to indicate that inflation is not going away anytime soon, thus setting up the conditions for a multi-year commodities up-trend.

I see the Fed reducing its rate hikes to 25 basis points before the end of the first quarter 2023 and pausing by the middle of the year. A reversal could follow shortly after.

That means a weakening US dollar and a rising price environment for all metals, in particular gold and silver.

Song by Ghost Town Blues Band – “TIP of My Hat“

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.