- Pendulum Swing

- Falling Dominoes

- Wounded Regime

- New York, Energy Costs, and Thanksgiving

Historical comparisons are always risky. This is particularly so when comparing different eras in vastly different countries like the US and China. Similarities can actually obscure more important differences.

Nevertheless, familiar knowledge can help build a framework for understanding. Obviously, present-day China is radically unlike any point in US history. But with that caveat, it bears some striking similarities to one part of our past. Today we’ll look at that period and see what it can tell us about China under Xi Jinping.

As I mentioned last week in Xi’s Changing Plan, China could be an economic partner as well as competitor, cooperating in ways that benefit its own people and the entire world. And while both our economies are bound together, that doesn’t seem to be the Chinese goal anymore, if it ever was. The US side clearly thought China would become more capitalistic and open as it became more prosperous and entrepreneurial.

This has important investment consequences you need to understand. We’ll start with some US history and the see how China’s course may be both similar and sharply different.

The US hasn’t always been the world’s dominant economy. Our first step in that direction may have been after the Civil War in what is now called the “Gilded Age.” Here is how Wikipedia describes that time.

In United States history, the Gilded Age was an era that occurred during the late 19th century, from the 1870s to about 1900. The Gilded Age was an era of rapid economic growth, especially in the Northern and Western United States.

As American wages grew much higher than those in Europe, especially for skilled workers, and industrialization demanded an ever-increasing unskilled labor force, the period saw an influx of millions of European immigrants. The rapid expansion of industrialization led to a real wage growth of 60% [JM comment: this period was one of the longest periods of outright deflation in US history, thus the emphasis in this article on “real” wage growth], between 1860 and 1890, and spread across the ever-increasing labor force. The average annual wage per industrial worker (including men, women, and children) rose from $380 in 1880, to $564 in 1890, a gain of 48%.

Conversely, the Gilded Age was also an era of abject poverty and inequality, as millions of immigrants—many from impoverished regions—poured into the United States, and the high concentration of wealth became more visible and contentious.

Thirty or so years of rapid economic growth brought many changes to the US. You could say the same of the last 30 or so years in China. In both cases, occasional crises popped up but subsided. The growth was uneven, too.

In the US example, large monopolistic trusts developed in railroads, steel, oil, and other key industries, facilitated by corrupt politics. Wealthy tycoons built giant mansions and summer homes in Newport, Rhode Island, to popular acclaim as well as criticism. Again, we see similarities in China’s recent past.

The pendulum eventually swings to correct such excesses. Around 1900, the Gilded Age gave way to a “Progressive Era.” From the Wikipedia entry…

The Progressive Era (1896–1932) was a period of widespread social activism and political reform across the United States of America that spanned the 1890s to the 1920s. Progressive reformers were typically middle-class society women or Christian ministers.

The main objectives of the Progressive movement were addressing problems caused by industrialization, urbanization, immigration, and political corruption. Social reformers were primarily middle-class citizens who targeted political machines and their bosses. By taking down these corrupt representatives in office, a further means of direct democracy would be established.

They also sought regulation of monopolies through methods such as trustbusting and corporations through antitrust laws, which were seen as a way to promote equal competition for the advantage of legitimate competitors. They also advocated for new government roles and regulations, and new agencies to carry out those roles, such as the FDA.

The president most associated with that time is Theodore Roosevelt, who took office in 1901 following the McKinley assassination. His domestic agenda promised a “Square Deal” for average citizens, breakup of the powerful business trusts, environmental conservation and safe food and drugs—all understandably popular policies, given the prevailing mood. (What is it with politicians and “deals?” FDR’s New Deal? The Green New Deal?)

Xi Jinping is certainly no Roosevelt (though they seemingly share a similar resolve when facing problems), but he’s facing a similar time in China. His country had its own kind of Gilded Age, beginning back in the 1980s and extending into the 2010s and 2020, until Xi began to crack down.

In hindsight, the images we saw in those years—futuristic cities, gleaming railways, giant IPOs, and all the rest—now look like “Peak China.” That period’s excesses set up an inevitable backlash. I don’t think Xi caused this frustration. Like all national leaders, he is largely captive to circumstances. But he can control the response, and it looks more than passingly similar to the US Progressive Era: anti-corruption, anti-corporate, and pro-consumer.

You can try to achieve those through gentle persuasion or autocratic decrees. Xi is choosing the latter, so I suspect it won’t go as smoothly or end as well as it did in the US a century ago. And our own transition was more than a little bumpy, even if voters fueled it.

Xi’s crackdown on successful technology and other companies is basically telling entrepreneurs to be careful about getting too big. This is a monster experiment in changing the human entrepreneurial equation. Xi needs entrepreneurs to drive the Chinese economy forward. But moving away from Deng Xiaoping’s “Some must get rich first” will certainly change how entrepreneurs run their businesses. Maybe it will work but it does give credence to the concept of “Peak China.”

As investors, we have to consider both what will happen and when it will happen. Long-term benefits won’t matter if short-term risks take you out of the game first. But taking steps to endure the short-term can help you stay around long enough to reap bigger rewards. So let’s consider the near future, then come back to the longer-range outlook.

Property developer Evergrande is the top-of-mind concern right now. Its business risks are largely confined to China; the fear is more about possible financial contagion, which could extend outside China to foreign investors and lenders. Non-Chinese debt is around $20 billion and will likely be written off. While painful to the institutions involved, the debt is manageable.

How might a contagion unfold? Here’s one scenario, outlined by my friends at The London Brief, in which Evergrande is the first domino of something worse.

Domino 2: Companies Similar to Evergrande. A significant number of companies are borrowing above 20% rates and can no longer fund from the dollar funding market. These companies can either default, they can try to sell assets, they can go to government banks to borrow money (but this route is currently closed until January) or they can go to the government. Today there are 35 “significant” companies, as per the strategist’s definition, and 13 are saying in the dollar funding market that they should not be refinanced. This is like the sub-prime equivalent; one has gone down, and the others are feeling the knock-on effect. These companies are 12.5% of the current market cap of the property sector. The amount of market cap that has been lost is $250 billion and including Evergrande is $500 billion to give some scale of numbers.

Sidebar: In the late 1970s I borrowed money at 18% to buy literal train carloads of paper. I could afford it because paper costs were rising faster than 18% and there were actual shortages. The only way to ensure I had paper for my publishing business was to store well in advance. When property developers are borrowing money at 20% and inflation is much less than 5% that tends to indicate the housing markets are overheated.

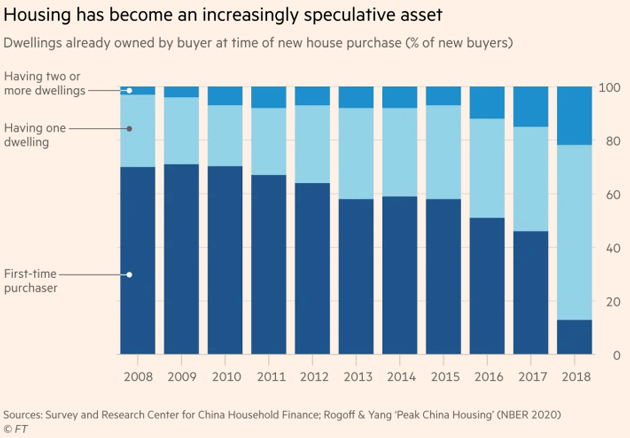

Note below that prior to the Great Recession, first-time homebuyers were roughly 70% of the Chinese market. Today it looks like 15%. Now 85% of homes are bought by people who already have one or more homes. Just like Dave Portnoy, they believe that home prices can only go in one direction: UP!!! This is rampant speculation. and while it is not subprime in the sense that these people are actually investing their savings in the second property, it is speculation nonetheless. Unless the Chinese government changes its current policy, there is going to be a serious revaluation of home prices in China, as many of these homes are empty and are out of the price range for new homebuyers.

Source: Financial Times

Domino 3: Minsheng Bank. In 2008, Bear Stearns imploded due to subprime debt. Citigroup is watching Minsheng Bank, which has lost over half of its market cap over the last few months. It is currently modelling a 20% probability of default. It could create contagion effects within the banking system.

Sidebar: We think of Evergrande as a large company. It is dwarfed by the size of Chinese banks, many of which have large loans to the real estate market as a percentage of their assets. Thus, we come to the next Domino.

Domino 4: Small Banks. There are numerous banks in China that are very similar to Northern Rock, a small bank in the UK which imploded due to its exposure to subprime debt and a balance sheet that was wrong-sized. These banks have low transparency but create exposure to larger banks and insurers. If more property developers go supernova these banks are vulnerable.

Domino 5: Ping An. This is a private insurer with a lot of problems. They own a property company called China Fortune Land. 5% of the investment portfolio is leveraged 10X. The CEO and company are under regulatory investigations. They issued wealth management products for Hong Kong tech shares. These have been sold to millions of people across the investor base of Ping An. They could see their savings wiped out and China may force Ping An to make them whole. Ping An is systemically important. The dollar bonds only widened out 40 bps last week, but it shows the market knows there is a problem. [There is never just one cockroach.]

Domino 6: The Equity Market. There are $300 billion worth of margin loans. If an insurer like Ping An went into stress, there could be more share selling on other banks creating a cascading impact that triggers margin calls.

Domino 7: Big Banks. ICBC and other systemic banks interface with international markets. Their equity prices could plummet and their CDS [Credit Default Swaps] could widen. Regulators and the banks have been assessing their risk exposures optimistically much like Morgan Stanley and other large US banks did during the subprime crisis.

Domino 8: The Credit Market. If China bank CDS blows out everything else blows out too and credit contracts dramatically. With $50 trillion of bank assets, that’s a lot of contraction.

Domino 9: The RMB Breaks. Chinese banks would have to go on a worldwide hunt for dollars, which would lead to pressure on RMB and volatility and potentially force China to break its peg.

Domino 10: The Crisis Goes Global. European, Korean, and Indian banks with yuan exposure could collapse and start to create an international contagion impact.

This is an extreme scenario which the authors don’t believe will happen. It would not be in Beijing’s interest to let events progress that far. But it’s also unclear at what point the Chinese government would intervene. That introduces uncertainty that could get out of control. This week another developer, Fantasia Holdings, defaulted on $206 million in dollar-denominated bonds—a small drop in the bucket, but more could follow.

Again, I think China will muddle through this immediate problem, but the risks are high enough to justify some preparation. Nor is financial contagion the only risk. Dave Rosenberg thinks Evergrande could set off a global recession.

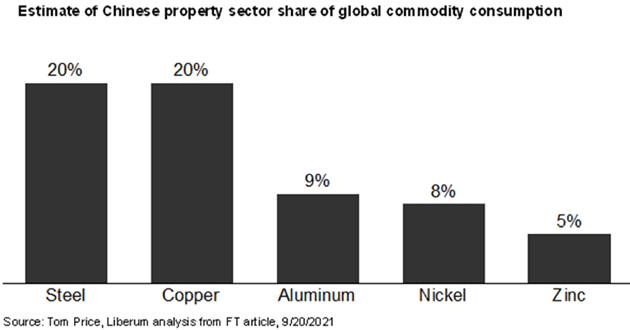

This is really a contained financial event within China since most of the debt is held onshore, but it is also a huge negative macro event for the world’s second-largest economy and I see that Goldman Sachs is all the way down to 0% for Chinese Q3 real GDP. It is a huge internal deflationary shock that could easily send China into a recession and anyone who doesn’t think that will have knock-on effects on the rest of the world doesn’t obviously realize that China accounts for nearly 20% of global GDP and still consumes half of the world’s basic materials. This story is going to have global macro knock-on effects that we haven’t seen yet.

Now, the silver lining here is that such a recession would probably end our commodity price inflation worries. It might replace them with other, bigger problems.

Bain Macro Trends Group offers us this simple chart. A slowing Chinese housing market will reduce demand for materials across the board. Note that property construction accounts for one-third of the Chinese economy. As pointed out above, that large proportion is now being fueled at least in part by speculation and not actual demand. I expect any day now that we will hear the Chinese equivalent of Ben Bernanke saying, “Subprime is contained.”

Source: Bain Macro Trends Group

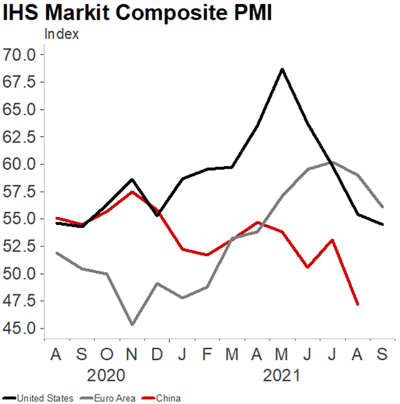

Nearly every major country has what is called a PMI index, or Purchasing Managers’ Index. When the number slips below 50, it indicates that the manufacturing portion of the country is not growing. That is the case in China. Let’s look at the US, Europe, and China courtesy of Bain:

Source: Bain Macro Trends Group

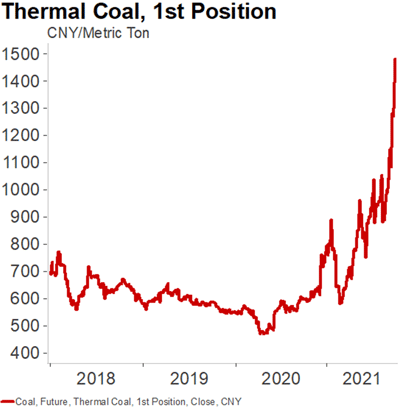

This is compounded by a serious energy crisis in China. My friend Bill Bishop writes:

They [the power shortages] appear to be a result of a witch’s brew of partially and poorly implemented power market reforms, surging coal costs that have led power generators to operate at a loss, and the political commands in some provinces leading to campaign-style efforts to reduce energy consumption and intensity to meet targets set by the central government. Something is going to have to give, and quickly, as winter is approaching.

We are all familiar with rising natural gas prices in Europe and the US. And while China does use a great deal of LNG, they are most dependent on coal. And coal prices have risen over 150% in the last year in Chinese currency:

Source: Bain Macro Trends Group

Even high-priority industries like technology and semiconductors are subject to rolling blackouts. While we might see relief in commodity prices, energy shortages could aggravate supply chain problems. Many US and European industries still depend heavily on Chinese components.

Many in the West view China as a rival power, fearing its size and ambitions will lead it to eventual domination. The real danger, though, may arrive when Chinese leaders conclude their power has peaked.

A recent historical analysis in Foreign Policy described how growing wealth motivates leaders to act boldly, shrugging off minor annoyances. Fear of decline does the opposite. Leaders try to hide their weakness, which becomes increasingly difficult.

Eras of rapid growth supercharge a country’s ambitions, raise its people’s expectations, and make its rivals nervous. During a sustained economic boom, businesses enjoy rising profits and citizens get used to living large. The country becomes a bigger player on the global stage. Then stagnation strikes.

Slowing growth makes it harder for leaders to keep the public happy. Economic underperformance weakens the country against its rivals. Fearing upheaval, leaders crack down on dissent. They maneuver desperately to keep geopolitical enemies at bay. Expansion seems like a solution—a way of grabbing economic resources and markets, making nationalism a crutch for a wounded regime, and beating back foreign threats.

It goes on to show how many of China’s previous advantages disappeared in the last decade or so. A once self-sufficient country now depends on imported energy and food, is approaching a demographic precipice, and is ideologically centralizing power at the expense of economic prosperity, all while external pressure grows more intense.

That’s not to say war or economic collapse is inevitable. I think both are very unlikely. But it does serious damage to the idea of China as a “state capitalist” economy that can work with Western businesses and governments. Companies in the US and Europe who have made large investments in China will increasingly find their deals come with unacceptable “new” conditions, especially technology sharing. Chinese companies exporting to the West will encounter more barriers. US consumers who have grown accustomed to low-priced Chinese goods may see higher prices, if they can get those goods at all.

This isn’t catastrophic, but it will certainly be different. Many US companies are at high valuations because investors think they will keep growing in new markets like China. That now looks like a pipe dream. Whatever you have to sell, a Chinese company probably has a home-grown version and will beat you to market, with the government’s enthusiastic help.

That’s the best case. It’s also possible someone (not necessarily in China) will trigger events that make a bad situation worse. China is now so interwoven into the global economy, problems could start anywhere.

I’ve been saying for some time the 2030s will be a bright time, but we have to get through the 2020s first. China is one reason the next decade could be tough.

New York, Energy Costs, and Thanksgiving

My current intention is to be in New York from October 27 through November 2. Not sure what to do on Halloween in NYC. I’m sure we will have at least one client (and possible new clients) dinner. I’ll spend Thanksgiving with family in Dallas.

I got into a bit of a debate on Twitter last week about energy. I said that to a climate warrior, high fossil fuel prices are a feature, not a bug. They make solar and wind more competitive. That started a back-and-forth that was quite fun. You should follow me on Twitter.

We really do try to keep this letter to around 3,000 words. Honestly, there is so much to say about China it could easily have gone 12,000 words. And of course, I said nothing about Friday’s jobs report, which was strong enough in the current environment that the Fed should seriously begin to taper in December. Unless Biden appoints a serious dove.

And with that I will hit the send button. Have a great week and spend more time with friends and family.

Your happy to be mostly hedged analyst,

|

|

John Mauldin |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.

About the author