In a sure sign that the times have changed, the scam of "Exchanges For Physical" that The Bullion Banks have utilized for several years as a risk-free profit method appears to have finally collapsed.

If you've been following along in these pages, then this surely is not "breaking news". We've written about the Bank abuse of EFPs on multiple occasions over the past three years. Here are just a couple of the links:

- https://www.sprottmoney.com/blog/comex-exchanges-for-physical-craig-hem…

- https://www.sprottmoney.com/blog/exchange-for-physical-craig-hemke-04-122019

Astute followers of the precious metals also know that the entire digital derivative pricing dynamic changed on March 23 with the advent of QE∞ and a fracture in the global physical metal market. Back in June of this year, we wrote about the collapse in EFP abuse that followed the craziness of late March. Please review this link before continuing:

From that June post, please be sure to see this passage:

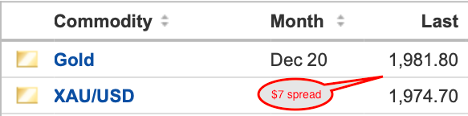

Well, it's clear that the bullion banks were abusing this process to make a steady, simple, and relatively risk-free profit each day by arbitraging the price fluctuations between New York and London. In essence, buying or selling a COMEX futures contract in New York and then selling or buying a spot contract for delivery in London and capturing the spread between the two. If you're HSBC and doing this with 10,000 contracts, a simple $2 spread nets you a tidy $2,000,000 profit. Good work if you can get it.

All is well and fine for this trade so long as there's physical metal to deliver versus your spot sale—and this is where the entire machine fell apart in late March. Many mints, mines, and refineries were closed due to Covid-19, and the supply chain of physical metal to the highly leveraged global gold market broke down in spectacular fashion. Without physical metal to deliver, the bullion banks playing the EFP game were forced to close positions in a true short squeeze. The result? It wasn't just HSBC that (literally) took it in the shorts. See this regarding CIBC: https://www.reuters.com/article/us-cibc-gold/canadas-cibc-lost-64-milli…

In the three months since, Bank EFP abuse has continued to decline. Thus it has now become clear that The Bank's pricing scheme suffered irreparable damage back in March and it won't be returning in full force anytime soon. And how significantly has EFP abuse fallen off in 2020? See below. Keep in mind that each contract "exchanged for physical" allegedly moves 100 ounces of gold. So when you see 213,671 contracts "exchanged for physical" in just January of 2018, that's a total of 21,367,100 ounces or about 665 METRIC TONNES!

JANUARY: 213,671 EFPs in 2018. 174,964 in January 2019. 207,674 in 2020.

FEBRUARY: 196,076 in 2018. 111,476 in 2019. 188,543 in 2020.

MARCH: 242,973 in 2018. 155,401 in 2019. A whopping 362,049.

APRIL: 221,542 in 2018. 141,311 in 2019. 71,527 in 2020.

MAY: 225,279 in 2018. 151,276 in 2019. 79,230 in 2020.

JUNE: 207,347 in 2018. 202,656 in 2019. 65,405 in 2020.

JULY: 201,140 in 2018. 187,859 in 2019. 91,685 in 2020.

AUGUST: 152,805 in 2018. 201,473 in 2019. 52,275 in 2020.

As you can see, while not at ZERO, Bank EFP use is down by as much as 75% versus years past. This is significant, as it betrays both a lack of physical metal and a lack of counter-party confidence. This also explains why the spread between spot gold and the front month futures contract persists. When you lack confidence in your counter-party, what was once perceived as a risk-free arbitrage becomes something quite risky, indeed.

So we'll continue to monitor the EFP and spot-futures relationship very closely in the months ahead. If the trend away from EFP abuse continues, then it would seem that we are slowly making progress toward a more physically-based pricing system. And as you likely know, any system that discovers price based upon actual physical metal instead of derivative contracts is likely to benefit all of us who hold and stack that actual physical metal.

About the author

Our Ask The Expert interviewer Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.