Stock investors don’t believe Powell because the Fed lost most of its credibility in recent years by promising it could do quantitative tightening on autopilot in its long-awaited and feared balance-sheet unwind, which crashed stocks back in 2018.

Next it slammed the brakes on QT in a Fed faceplant because it had also crushed bank reserves, which the Fed, more than any entity on the earth, is supposed to understand and manage. After causing the Repo Crisis, the Fed exited that misstep by overprinting money in the wildest cash spree in history, in the hysterical fantasy that massive money printing (under the new pop philosophy of Modern Monetary Theory) would not cause inflation, which it immediately caused … eventually on a large scale that it has found hard to stop.

It got to that point because the Fed denied inflation was significant when it was obvious that inflation was rising behind the scenes into a boundless inferno. Under its misinformed and clearly misspoken belief that inflation would prove all on its own to be “transitory,” the Fed waited too long to tighten after printing way too much money in the face of the worst shortages seen since WWII, and we all know scarcity, by itself, drives up prices. That’s why diamonds are worth more than glass and gold worth more than tin.

Now, this week, Powell talked out of both sides of his face in that his written speech sounded hawkish as did some of his initial words in each answer during the Q&A, BUT every answer seemed to conclude with a follow-up comment that went something like, “Of course inflation could come down faster than we expect; in which, case we’ll be able to back off from fighting it so hard because we are making good progress.”

Like an out-of-touch parent who doesn’t know sugar makes kids more active, Powell offered this kind of candy more than a couple dozen times as if he really didn’t realize the long-delusional stock market would seize solely upon every morsel that sounded sweet and ignore all the bitter Brussel sprouts in his packet of goodies and medicine.

If Powell’s aim ever was to tighten financial conditions, he either failed miserably at his last presser, or the plan has suddenly taken an important turn, because immediately financial conditions loosened all the way back to the pre-inflation days of massive money printing. Interest rates fell as bonds repriced, and stocks surged as expectations for easier times soared in the lunatic asylum on Wall Street.

Welcome to our barmy and brainless new world

This note of optimism throughout the Powell presser created a sense that the Fed’s plan was based on a worst-case-scenario so that anything that happened outside of the Fed’s expectations would likely be for the better, even though everything Powell said the Fed would actually do was exactly what he’s led the world to believe for a few months now. All it took was a breath of etherium for markets to rise higher than a Chinese helium balloon.

Wolf Richter put together a good summary of just how hawkish Powells’ words were, but Powell surely had to know that if he left little hanging bits of hope in front of the children, they would grasp for the treats and use them as an excuse to go berserk, which, of course, they predictably did.

“The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done,” but it’s not done, Powell said.

However, the market heard none of that. You can read Wolf’s list of the Fed’s tough talk to see all the hawkish statements the Fed made, and Powell made a lot. I won’t reiterate any of it here because none of it mattered. Powell repeated many times what everyone already knew about how the Fed would tighten a little more and then stay tight for the full year, but the market only hit on his hopium.

The question is what happens next? If Powell misspoke and was surprised to see he undid some of the tightening of financial conditions, will he use Tuesday’s talk to bring it all back down? Will it even matter if he does since the market is still smoking delirium handed out at the last Fed meeting?

Perhaps Powell felt he had pounded the points of tightening so hard that he had better back off a little, lest he cause economic wreckage from saying it so many times. If so, it appears he miscalculated badly. He should have known this market only wants its next high, no matter how insane that is in the present falling world.

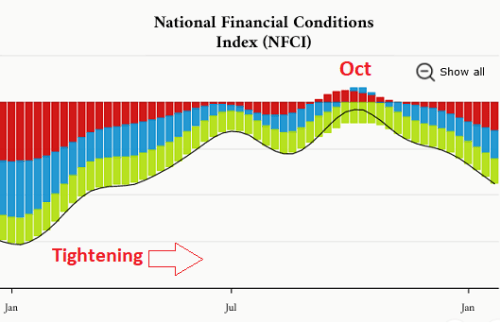

Powell, in the very least, pretended he cared about keeping financial conditions tight, which since October have done this:

Higher asset prices inevitably mean looser financial conditions. Powell said this mattered:

The minutes of the December meeting mentioned this “unwarranted easing of financial conditions,” and pointed it out as a risk that would make it more difficult for the Fed to bring inflation down. Powell was asked a couple of times about that….

“Financial conditions have tightened significantly over the last year,” he said. “The financial conditions haven’t changed much from the December meeting [Dec 14] until now.”

Well, the latter statement was a bit out of touch, given the graph above shows they certainly changed a lot.

It is important that the markets do reflect the tightening that we are putting in place as we have discussed a couple of times here. There is a difference in perspective by some market measures on how fast inflation will come down. We will have to see.

I mean I am not going to try to persuade people. I have a different forecast. Our forecast is that it will take some time and patience, and we will need to keep rates higher for longer.

And there is where he went off the rails. If he wants to keep conditions tightening, instead of easing back down, he should have cared about trying to persuade people because financial conditions became looser still in response to his talk.

Of course, many things affect financial conditions, not just our policy. We will take into account overall financial conditions along with many other factors as we set policy.

We think we covered a lot of ground, and financial conditions have certainly tightened. I would say we still think there is work to do there.

Keep talking like that to this market, and you’ll have a lot more to do.

Powell talked about the metrics the Fed actually pays most attention to, which he said haven’t budged at all — zero progress he indicated. The market didn’t care what he said about that. It only heard Powell say the Fed might be wrong, and, if so, it could back off a little. The market has seen the Fed do that so many times with all the other Fed mistakes that investors seemed to take it as the given they want to believe in.

This is not a market you can talk to rationally. The problem is, the more the market rises on fantasies, the harder it will have to fall with greater momentum when it finally realizes tightening really is going to last through the year and that the market’s rise only means the Fed, at some point, is likely to have to tighten even harder. If Powell is smart, he’ll smack the market down hard right now; but it’s highly debatable he’s smart about that particular thing.

Of course, I have people tell me I’m delusional to think this bear market isn’t dead with a new bull already being born. Well, I guess, as Powell said, “We will have to see.”

As Wolf Richter commented toward the end of his article,

What was hilarious at the press conference today was a slew of crybaby can’t-you-stop-the-rate-hikes questions. They were so funny that we’ll go through some of them here, and you’ll see that Powell should have answered them with: “Stupid question. Next!” Or “I already shot this down twice. Next!”

But that’s just it. That is the thinking prevalent throughout financial media, so it is prevalent throughout the stock market — this idea that we’ve done enough now, so we can take a break. Powell encourages this kind of thinking because, I think, he is a gentle person by nature, so he tries to give nice answers; but what you really need to do to people who are living in a state of mania is slap them hard in the face. Powell tried to answer them all politely, and that had no wake-up quality.

The giddy market merely giggled in Powell’s face, conditioned by years of the Fed fading on toughness and caving into the craven market’s wishes, oblivious now to the fact that there was no inflation then to stiffen his spine like a plank as he has now.

That does, of course, mean the Fed’s policy approach of forward guidance is no longer working due to loss of credibility or loss of fear of the Fed … or both. The market is playing chicken with the Fed. However, investors need to realize that the Fed no longer wants to save the market. It doesn’t care if the market falls hard this time. In fact, it is hoping the market falls, as that is a major part of the financial conditions that Powell said do matter.

Blinking back bleak reality

Here is some of the reality the market chose to ignore when Papa Powell spoke in calm and reassuring tones:

The profit outlook for companies in the S&P 500 Index is rapidly deteriorating — yet analysts can’t raise their stock-price targets fast enough…. But the degree to which analysts are raising stock-price targets while slashing the earnings estimates is puzzling for those used to seeing the market hinge on the underlying strength of corporate America….

Fourth-quarter reporting season has done little to support optimism about the fundamentals. Earnings in sectors from energy to consumer discretionary have been coming in below pre-season estimates and companies are dialing back outlooks based on expectations growth will slow. In fact, Bloomberg Intelligence’s model shows that such earnings guidance for the first quarter has been cut by the most since at least 2010….

Among all changes analysts made to their earnings projections last month, just 37% were upgrades, data compiled by Citigroup Inc. show. The level has been associated with the past three economic recessions and is 30% below a historical average….

“We’re starting to see some of these companies come out and give less than ideal guidance on growth,” said Brian Jankowski, senior investment analyst at Fort Pitt Capital Group. “We’re starting to see those business forecasts for growth line up better with GDP, which is predicted to be very little to flat.

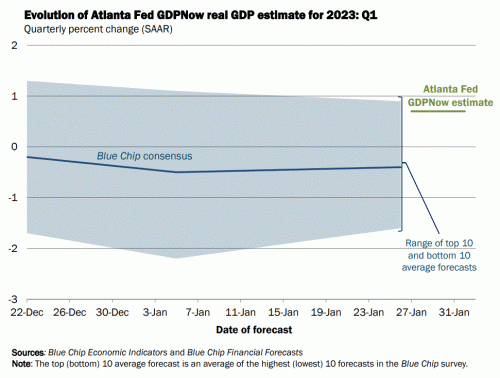

Here are where those GDP predictions are from establishment economists and the Atlanta Fed:

The Federal Reserve Bank of Atlanta

The Federal Reserve Bank of Atlanta

Virtually everyone now puts the present quarter back down to 1% growth at best, and top estimates for GDP growth are slowly sinking.

The Fed has said for months it would likely be backing down the size of its interest-rate increases at the last meeting, so there was no surprise hope in the decreased scale of the hikes. It was just the Fed doing what it has telegraphed for months it was most likely to do. Yet, we saw analysts raise their share-price estimates at the fastest pace since the spring of 2021. Why? Just because the Fed is staying exactly with the program it has been saying it would do for months?

The Fed’s central role in the outlook for equity prices was underscored by how well the market performed this week in the face of some negative earnings surprises from major companies.

In fact, those were some very negative reports that widely missed expectations both for last quarter’s earnings and for future earnings from the likes of Apple and Alphabet; but stock market investors inanely shrugged them all off as if reality doesn’t matter … exactly as they did with every rally last year … and were wrong all year as though all that mattered was the Fed, then it shrugged off what the Fed said, too.

The punishment by Papa Powell will continue, no matter how gentle he tries to sounds. So, keep it up, and the pain will likely get worse by forcing him to tighten even harder for even longer because inflation is a bitch, and its whip is biting the head banker’s back.

But rationality applies to bears as well

It’s insane to walk through the insane asylum and expect to find rational people. So, those who are bears because economic reality isn’t improving (more on that at another time), need to recognize that rationality isn’t improving among market investors either. So …

Punch-Drunk Investors Will Keep Ignoring Reality…Until It’s Too Late

Back in January 2020, I was pointing out that the coronavirus was going to wreak havoc on markets weeks before it ever happened.

As I’ve noted many times on this blog, those days were immensely frustrating.

I waited for a collective market ethos that only viewed the news through a backward looking rearview mirror, with the attention span of a fruitfly and the collective IQ of a wooden ping-pong paddle, to catch up to a news story that was unfolding and evolving, by the second, right in front of their eyes. The news – and the ensuing chaos it would create – couldn’t have been more obvious if it was bludgeoning the market over the head with a wooden club, Bamm-Bamm Rubble style.

Quoth the Raven’s Fringe Finance

I can relate to QTR. Nothing makes less sense in this world than talking sense, and nothing is less respected by those who can collectively drive the market up with their irrationality, almost as if to spite those who warn them of the declines to come … until they can’t. But, even then, they don’t learn and just do it all over again and take the same punishment again.

Ultimately, I was proven right in my prognostication when the market crashed in March, before the Fed came in and launched unlimited quantitative easing and the public started to wrap their head around the fact that Covid wasn’t necessarily a death sentence.

Current markets seem hell-bent not just on once again ignoring the obvious right now, but spitting the obvious back in the faces of those who use reality as a guide to their decision making. And the real kick in the nuts is that the Fed, the broadest influencer of our economy and market sentiment, isn’t even a tailwind this time. On the contrary, it is a massive headwind.

Having long quoted “Don’t fight the Fed” to us, they now do the opposite of their own advice. But there is more pain to come:

The market is simply still hanging around – like a Mortal Kombat character stunned, but still on his feet, waiting for the Fed to deliver the final blow….

It is difficult to break the psychology of market participants who have been conditioned to buy the dip without consequence for the last 15 years. So, in that respect, I’m not surprised the market is rallying despite economic reality. But to say that the market has been grasping for straws when it comes to reasons to rally would be a vast understatement.

Take this week for instance. The market is rallying based on nebulous words Jerome Powell used or omitted from his presser on Wednesday despite the fact that he very clearly stated that more rate hikes were on their way. Its tea leaf reading on top of tea leaf reading, ignoring the very stark reality that interest rates are nearing 5%. There’s nothing to guess or speculate about with rates – they’re most certainly at their highest levels in decades.

Indeed. But, for now, the market is saying, “Reality be damned.”

Market optimists love to say this is because “the market is forward looking,” generally looking half a year down the road. No, it is not. If it were forward-looking, it would be expecting another full year of financial strangulation by the Fed at levels slightly tighter than now and than anything investors have known in the past fifteen years, and they would expecting all of that is likely to break some really important things that will make the economy and markets fall even worse.

They are not forward thinking. They are forward-denying. There is no chance that tightening into a recession that almost everyone was talking about as being likely last month is going to make things better in the second half of the year. Nevertheless, that is what they are believing, so the rest of us must wait out their irrationality before we can put our savings back into stocks as a reasonable risk for our future.

But this is the little monster of a brat the Fed raised, and we’re all stuck with it playing in our china cabinet as Papa Powell pats his proud muffin on the head and says, “Daddy has to play rough with the boys outside, but don’t worry they might all just run away when I open the door. Just keep playing with Joe’s heirloom china.”

There’s two ways to look at what the market is doing over the last couple of weeks: either we have firmly shifted into a new era, where we are at the beginning stages of a bull market once again and the fundamentals have changed (this, obviously, I don’t think is the case), or we are drifting further and further off the path of reality, which will eventually only lead to a bigger snap back when the time comes and the market can no longer turn its a blind eye to the obvious, wretched financial reality our country faces.

Of course, there is another way of looking at all of this, if I were to be generous: The Fed is lying as its new path of forward guidance — not lying about the fight not being over, but lying by presenting a false view that, if it is wrong, everything is only better than its worst-case scenario. Powell could be doing that as a way of continuing to actually tighten while undercutting that tightening a little to try to keep the landing soft, lowering the flaps for a little more drag and lift, but kicking up the engine speed just a little to help slow the rate of decent.

Maybe Powell is undercutting the reality of his rate hikes to soften any immediate blow, but believes that months of living under the reality of those hikes will have its own drift toward tightening, regardless of how the market responds now. Switching metaphors just a bit, maybe he’s coasting his ship into the doldrums to just let it drift for the next year and wait the scirocco winds of inflation out. Maybe he’s undercutting his message to slacken the sails and just let us drift the rest of the way into tightness as part of the soft-landing plan with a deft touch. However, given the Fed’s past ineptitude at tightening, I’m not sure I want to given him that.

Perhaps we’ll find out on Tuesday by whether or not Powell maintains his undertones of hope or, seeing that the market loosened even more, goes back to some Jackson-Hole cowboy whip cracking.

Getting back to rational

Here are some of the “are we there yet” questions a rational investor should be asking before going back into stocks. Maybe they will help you make your own assessment at this time as Powell keeps us guessing with mixed tough-and-tender messaging:

- How do we get to the Fed’s 2% inflation goal with only a little pain when we already had a half year of negative GDP when we were barely getting started? Is it reasonable to think tips six months were not a foretaste of things to come?

- How can US Fed policies do anything about worldwide inflation on the price of imports that are such a big part of our economy, especially if stopping its rate increases causes the dollar to start to fall in value relative to other currencies?

- How can Fed policies do anything about shortages, which are pushing inflation by causing scarcity (as if widespread scarcity is not ALWAYS a cause of higher prices).

- How can stocks keep rising when money supply is shrinking, and we know money creation must be a thing of the past for as long as inflation continues so that, with every passing day, there is less money looking for a place to settle? As bank reserves start to come down under QT somewhere down the line as the Fed wants, won’t banks seek to invest less in stocks?

- How can the Fed even think about any return to looser conditions when the metrics by which it measures the job market are running diametrically opposite of what the Fed says it wants to see and opposite of what it must see legally in order to gain liberty to go back to easing under its second mandate of maintaining a strong labor market.

- How can a new bull market start without actual Fed money printing as the driver at a time of high PE valuations like we still have, especially right at the start of sharply falling earnings? Without either money printing or rising earnings to drive share prices up, what will? Buybacks when the interest that funded most of them is rising?

- How do rising interest rates affect the price of oil now that falling energy prices are the leading cause of the drop in inflation seen so far, given the large role of financing in developing oil production?

- Even if rate hikes are paused in a couple of months as nearly everyone now expects, how do we know how long restrictive, high rates will have to stay in place?

- Are you sure the present rally wasn’t built mostly from a lot of short covering?

- Do a few simple sentences by Powell on Tuesday really change the entire economic outlook that stocks will have to face?

Liked it? Take a second to support David Haggith on Patreon!

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!