Let me translate – We at The Fed have to pretend that we might one day stop QE, but we know in truth that that we can’t. The last time we tried tapping our foot lightly on the brake we blew up the markets. We are trapped. We know it. You know it. But we need to pretend otherwise. – Albert Edwards, Global Strategist and noted bear, in response the FOMC minutes released this past Wednesday in which some FOMC members said it might be “appropriate” to begin discussions on tapering QE in upcoming meetings

The rapid escalation of the Fed’s Reverse Repo activity has garnered a lot of attention and commentary. While no one outside of the Fed’s inner circle can say for sure what it going with this, it’s highly unlikely that the activity is a pre-cursor to and eventual tapering of the Fed’s money printing policy.

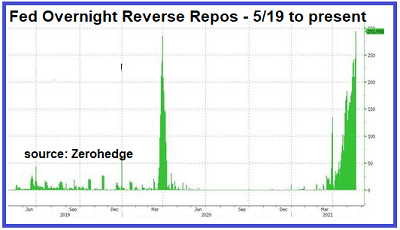

Repos and Reverse Repos (RRPs) traditionally are tools the Fed uses to implement its monetary policy in order to maintain its target Fed funds range, currently 0% to 0.25%. Interestingly, the Fed’s overnight RRPs activity has grown rapidly in volume since early March.

In response to several requests, I’m going to take stab at what I think is going on with the RRP activity. Dissecting the nature of the RRP transaction should help to understand the reason for the sudden implementation of RRPs to manage monetary policy along with the implications for the stock market. But my analysis is based only on an educated guess.

There’s a lot to unpack, and a lot of moving parts, when trying to analyze and interpret unusual Fed activity. The Fed hopes that the mainstream explanation – a pre-cursor to a taper – will be accepted at face value, in the hopes that only a few people will dig around to see if there’s more than meets the eye.

The Fed is walking a thin tightrope between fighting off financial asset deflation (a stock and bond market crash). To do this it needs to continue printing enormous sums of money. But it also has to avoid the money printing from translating into Weimar-scale hyperinflation and a crash in the dollar. Along with this, the Fed also needs to prevent the Fed funds rate from going negative. The RRP mechanism is the Fed’s attempt to “mop up” the excess liquidity that has accumulated in large pools at the spectrum of financial intermediaries (banks, money market funds, GSEs).

Repos traditionally give banks needed liquidity on a short term basis. In a Repo operation, the Fed “lends” cash to counterparties, usually banks, and the counterparties collateralize the loan with Treasuries or agency mortgages (FNM, FRE). The traditional use is to prevent the Fed funds rate from moving above the top end of the Fed funds target range. “QE” is a “non-traditional” long term, if not permanent, form of this transaction.

With an RRP, the Fed exchanges its Treasury/mortgage holdings for cash held in reserves by the banks in the Fed’s excess reserve account. For an overnight or over weekend operation, the transaction temporarily removes liquidity from the banking system. The next day the counterparty sells the Treasuries back to the Fed at a slightly higher price on terms that give the counterparty a higher return from participating in the RRP than holding cash. That’s the counterparty’s incentive to participate in RRPs. While the percentage interest earned is tiny, applied over $10’s of billions it’s not an insignificant amount cash interest earned.

The Fed engages in RRPs when it has determined there is an excess supply of cash in the banking system. If the banking system is awash in liquidity, it presents the danger that the Fed funds rate will drop below the low end of the target range. In the context of the current target range, it would mean the Fed funds rate goes negative and the Fed would be paying banks to borrow money.

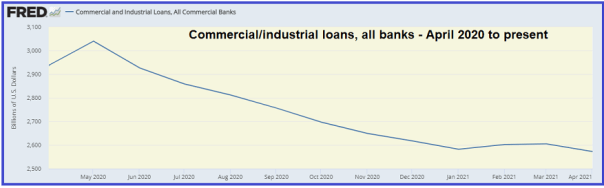

The banking system would be awash in cash liquidity resulting from excess money supply created by the trillions of QE money printing since March 2020. The Repo system is set up to enable banks with excess cash to lend on a short term basis to banks that need cash for business activities, with the Fed as the intermediary. But in an environment in which the real economy is not expanding, business demand for loans is low. This is confirmed by looking at the demand for commercial/industrial loans, has been falling since April 2020:

Contrary to the blaring mainstream media propaganda, the economy is not improving. If the economy were improving that chart above would be the opposite of what it is. We know banks have excess liquidity earning a near-zero rate of interest sitting at the Fed, so why is it not being loaned to businesses? Lack of demand for the loans, perhaps?

If real economic activity is not expanding, businesses do not have the need to borrow money to expand their operations in order to meet the demands of expanding economic activity. As a result, banks are left sitting on an “oversupply” of cash that earns close to zero percent (the interest on excess reserves paid to the banks by the Fed is 0.10%, while the 3-month T-Bill rate on paper used by money market funds and GSE’s is 0.02%).

We know the Fed has to continue expanding its balance sheet by printing more money to help fund new Treasury issuance in order to prevent the 10yr Treasury yield from spiking up to a level that would torpedo the financial markets – primarily the stock market – and send the economy into a depression. The last time the 10yr Treasury yield was above 2%, the SPX was over 20% lower than where it is now.

Thus, the Fed is faced with a conundrum. It needs to expand its balance sheet by printing money to buy new Treasury and mortgage issuance and to maintain “orderly” financial markets – i.e. to mute as much as possible the price discovery mechanism of free markets. But the Fed also needs to prevent its money printing from translating into price inflation. Price inflation results from an oversupply of money relative to the wealth output of an economic system.

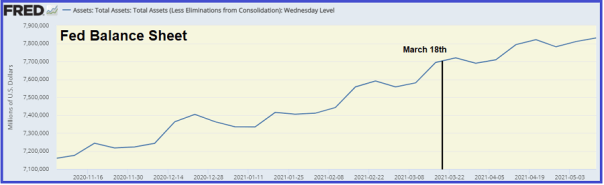

Several MSM commentators have suggested that the RRP operations are being conducted in advance of an eventual move by the Fed to taper QE and eventually to begin reducing the size of its balance sheet. But this is not a “taper warm-up” exercise in my view. Why? Because the Fed’s balance sheet has continued to grow in size over the two-month period that the RRP activity took off:

Per the historical data available on the Fed’s website, the RRP activity began in size on March 18th at $26.5 billion and 25 counterparties. The size of the RRP operations has expanded progressively and rapidly. The size crossed the $100 billion level on April 26th. On May 12th the RRP operation size was $209 billion, with 39 counterparties. By May 20th it jumped to $351 billion, with 48 counterparties, up from $293 billion and 43 counterparties the day before. Currently the RRP activity is running close to $500 billion per day.

In the context of the two charts above, the size of and breadth of the RRP operations has rapidly accelerated while, at the same time, the Fed’s balance sheet continues to grow. The RRPs are not removing liquidity from the banking system per se. Rather, the operations shift printed money back and forth between the Fed and the banking system on a daily basis at an increasing rate. Note: it’s important to understand the the overnight RRPs do not remove liquidity from the market.

By “breadth” I mean the number of participants allowed to participate in the RRP operations, as well as the size of the transaction limit per participant. In addition to banks, the Fed began to include money market funds and GSE’s in the repo market party 2009 (there’s several GSE’s in addition to FNM, FRE and FHA) – RRP Counterparties

The Fed also implemented the “tri-party” repo system which, in a way, brought money market funds (MMFs) into the banking system. This is important background information because, even though MMFs are now allowed to “break the buck,” it sends a negative signal to the markets if this happens. MMFs break the buck – NAV falls below $1 – when its interest income falls below operating costs. This would occur when interest rates fall too low or go below zero.

MMFs are meant to be “riskless.” Currently there is a shortage of short term Treasuries as a result of the Fed’s QE. Because of this, MMFs have and excess amount of cash relative the amount of available short term yield-bearing investment options. Including MMFs in the RRP mechanism enables the Fed to “sweep” cash out of MMFs in exchange for short term securities in the Feds SOMA (QE) portfolio, thereby avoiding, or at least deferring, the possibility that MMFs break the buck and lose money for their investors. The RRP is structured to give MMFs a higher short rate of return than they would earn on T-Bills.

On April 30th this year, the Fed reduced the AUM size requirements for money market funds to participate in RRPs. It also removed entirely the AUM requirements for GSE’s to participate: NY Fed Operating Policy. Then, on March 17th, the Fed increased the transaction limit for each counterparty (banks, money market funds and GSE’s) from $30 billion per day to $80 billion per day: NY Fed Operating Policy. This enabled the Fed to expand the size of the RRP operations by a considerable amount.

The bottom line is the Fed knows that it has to keep expanding its balance sheet – i.e. printing money and buying Treasuries and mortgages – while keeping as much of the printed money inside the closed banking system in an attempt to prevent it from escaping the circular path between the banks and the Fed and translating into accelerating price inflation. The move to widen the circle of RRP participants is evidence of the Fed’s intensified effort to maintain as much control over the excess cash it has printed as possible.

The “taper warm-up” argument is a non-starter. If is dropping the term “taper” in its FOMC policy statement as propaganda mechanism used to support the dollar. The Fed has already tried to taper. This led to a sharp draw down in the stock market and rise in interest rates at the long end of the curve. By September 2019 the Fed resumed printing money under the thinly veiled guise of “term repos.”

In essence, the Fed is running a Ponzi scheme using it’s own printed money as the source of funds to keep the scheme from collapsing. Compounding the problem is the progressive devaluation of the dollar caused by the Fed’s interminable money printing. The RRP operation is an attempt to prevent the Ponzi scheme from generating Weimar-scale hyperinflation without curtailing the size of the QE operation.

The rapid escalation in the RRP operations signals the enormous financial system imbalances created by the Fed’s money printing. I believe the RRP operations is the Fed’s attempt to prevent the excess cash from translating into uncontrollable price inflation. It is direct evidence that Fed’s Ponzi scheme, supported by its enormous money printing, is quickly becoming unmanageable. Watch for more overt advertisement and implementation of the well-telegraphed “Yield Curve Control” policy in the coming months.

The inevitable conclusion is hyperinflation followed by a collapse of the dollar and the stock and bond markets. My bet is that it is too late to prevent the inevitable.

Whether my analysis and conclusion is mostly correct or even just somewhat correct – in terms of what is going on with the sudden increase in RRP activity – it brings out two important points to consider when evaluating your investment decisions – long or short. First, the Fed has created a large reservoir of excess liquidity which it is working on trying to control.

Second, unless the Fed removes the liquidity permanently, price inflation will not only not be transitory but it will get much worse. In order to remove that liquidity permanently and reduce the size of its balance sheet, the Fed would need to exchange its Treasury/mortgage holdings for the cash it created and then destroy that cash, not keep rolling forward the RRPs.

So if the Fed continues printing more money to fund Government debt issuance (MMT) and tries to control it with RRPs, at some point the devaluative effect on the dollar on the money printing will trigger a rapid decline in the dollar. This might initially give the Dow and SPX a boost, but tech stocks hate inflation and the Nasdaq will tank hard.

Third, if my analysis is wrong and the Fed does indeed embark on a taper and balance sheet reduction program, the stock market will likely crash and interest rates at the long end of the curve will spike up. This is why the Fed stopped tapering over the summer of 2019 after it had reduced its balance sheet just 10%. The stock market became turbulent with a 19.5% draw-down starting in October 2018 and another 6% selloff starting in May 2019.

In addition, if the Fed tapers instead of increasing QE to fund the coming deluge of new Treasury issuance, interest rates at the longer end of the Treasury curve will spike up. Housing prices will contract sharply to the extent that buyers in the last 5 years who used high loan-to-value mortgages or did cash-out refis will find themselves underwater, in a significant negative equity position. A taper thus would be a disaster for the markets, interest rates and the economy.

The above commentary was published in the May 23rd issue of my Short Seller’s Journal. I also presented some short ideas that went along with the analysis. In each issue I analyze the economy and the markets as well discuss short ideas. I also provide a weekly update on Tesla. You can learn more about this newsletter here: Short Seller’s Journal Information.

About the author