Meme stock mania is back in full idiocy. And it’s time again to revisit $GME as a short. On March 14th, GME closed at $78, its lowest level in February 23, 2021. The stock had been down nearly 75% since June 9, 2021. But after the market closed on March 21st, GME Chairman Ryan Cohen, announced that he bought 100,000 shares in the open market, taking his ownership stake to 11.9%. This drove the stock price from $94 to as high as $189 by March 28th.

Then after the market closed on March 31st, GME announced its intent to do a stock-split. The stock jumped after hours from its closing price that day of $165 to as high as $203. It opened at $189 Friday and sold off steadily during the day to as low as $155, before closing at $163. Note: GME is doing a “stock dividend” rather than a stock split. While there’s GAAP accounting differences with respect to the shareholders equity accounting, for practical purposes there’s no difference.

There’s a lot to unpack there, not the least of which is the fact that the entire two-event sequence reeks of intentional stock price manipulation. Cohen clearly understands that the announcement of both his share purchase and the stock split would cause the Wall St Bets Reddit meme-chasing “apes” to stampede into the stock and OTM call options. This is an explosive combination given that the share float of GME is just 62.48mm shares and short-interest is close 20%. Cohen announced his share purchase just nine days ahead of the stock-split announcement. Of course he knew ahead of his stock purchase that his next move would be to announce the stock-split.

This is “stock manipulation” 101. Unfortunately, we live in an era in which the regulators look the other way. Many of them indirectly benefit in that they previously worked at Wall Street firms and maintain equity in their former banks. As an example, SEC Chairman, Gary Gensler, was at one time in the running to become CEO of Goldman Sachs.

In early March, Cohen announced that he had a 9.8% stake in Bed Bath and Beyond, another Reddit meme stock that loses $100’s of millions on an operating basis. That announcement drove the stock from $16 to has high as $30. BBBY closed at $22.84 on Friday. As with GME, BBBY has a small share float, with a 21% short interest plus a rabid meme stock following that boasts about its ability to create short-squeezes in stocks with high short-interest and a small float. It would be naive to believe that Cohen is not exploiting this dynamic.

Does investing in GME make sense from a fundamental standpoint? Zerohedge referenced the stock purchase/stock split combo maneuver as “a brilliant ruse by the management team which is far more focused on financial engineering and how to create stock squeezes than actually running the mostly worthless company.”

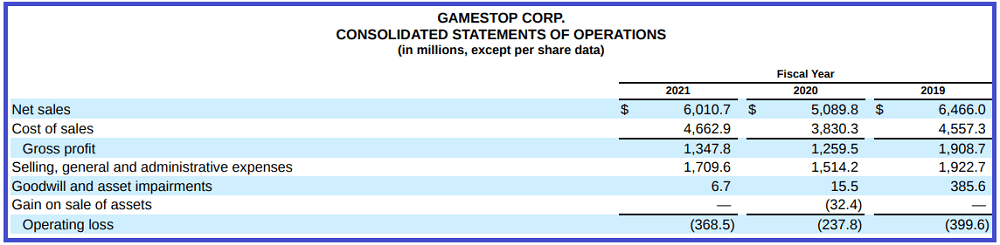

Cohen made his fortune as the co-founder of the online pet store, Chewy Inc. $CHWY has never been profitable. He took his stake in GME in November 2020, seeking to transform GME from a brick/mortar-store based retail business into an e-commerce operation. Here’s the operating performance of the business over the last three years (GME released its FY 2021 Q4/full-year on March 17th:

Revenue fell in 2020 because of the virus crisis and related lock-down, which affected all brick/ mortar businesses. But 2021 revenues were still 7% below 2019. For Q4 (not shown), revenues increased slightly over Q4/2020, but the gross profit plunged 15.6% and an $18.8 million operating profit in 2020 swung to $166 million operating loss in Q4/2021.

From the pattern in the Company’s operating losses, it would appear that operating losses vary with revenues – i.e. this business does not have economies of scale. The gross margin in 2019 was 29.1%. It fell over the next two years down to 22.4%. In 2021, the operations (from the statement of cash flows) burned $434 million in cash. As for the plan to shutter the brick/mortar stores, the Company closed down just 5% of its store base in 2021.

The sizzle in the gaming business is with the software. 53% of GME’s revenues in 2021 came from selling gaming hardware and accessories. This is a low-margin business. In 2020 hardware was 49% of sales and it was 42% of sales in 2019. It would appear that software sales as a percentage of revenues is going the wrong way. This explains why the gross margin is declining precipitously.

In 2021 the Company took advantage of the meme-stock driven short-squeeze operation and raised $1.6 billion selling shares. It used some of the cash to pay off debt that was due in 2021 and 2023. The Company has $1.27 billion in cash, which is the only valuable asset on its balance sheet. But against this, there’s $1.35 billion in current liabilities (accounts payable, accrued liabilities, operating lease payables). This Company is technically insolvent. I would be surprised if the Company does not take advantage of the share price run-up and unload even more shares on the market.

Bottom line: This is a business that is slowly withering away. Ryan Cohen, whose Chewy online pet store has never made money, apparently believes he can transition GME’s business into a more software-focused e-commerce business model. Good luck. The gaming software business is extremely competitive. Regardless, I strongly believe that Cohen’s primary motive with GME is financial engineering and stock price manipulation. There’s ways for Cohen to monetize some of his shareholdings without directly selling shares in the open market.

GME’s market cap as of Friday’s close is $12.5 billion. It’s a non-nonsensical market cap for a business with serial operating losses, declining gross margins and stagnating to declining sales. Plus the fact that it is technically insolvent. The stock split/dividend will increase the number of authorized shares from 300 million to a billion. The annual shareholder meeting will likely occur in June (June 9th last year), which means the stock split will likely occur in mid-June. The additional shares outstanding should alleviate the susceptibility of the stock to short-squeezes.

A year ago the Street forecast for GME was to earn $1.30/share this year (2022). Now the Street is forecasting a loss of $4.17/share for this year and $3.00/share loss for 2023.

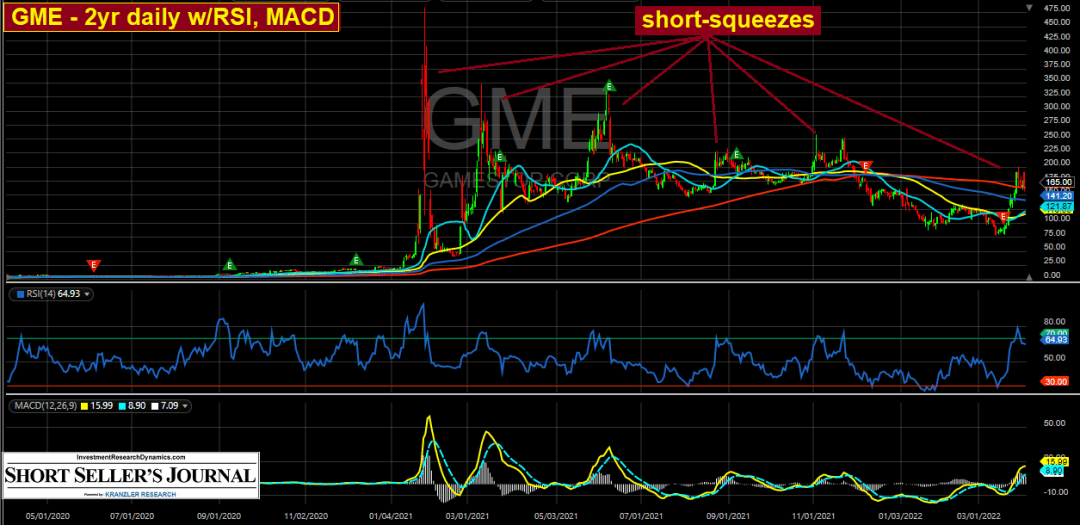

I believe over the next few months, especially if/when the bear market decline resumes, GME will minimally retrace back to the $80 level, where it was trading before Cohen restarted his stock manipulation schemes. The stock is hard to borrow right now but that status will change after the stock split. The good news is that, while implied volatility in the options is north of 100%, it’s half of what it was when I was presenting GME as a short in late 2020.

*******************************

The above commentary on $GME is an excerpt from my latest Short Seller’s Journal – I’ve hit several home runs over the last year, including $DKNG, $HOOD, $Z and $NAIL. There’s still a lot of money to be had on the short side before the stock bubble fully deflates…

About the author