Gold investment capital flows are a primary driver of gold-price trends, fueling both major uplegs and corrections. Massive outflows from dominant gold exchange-traded funds really intensified gold’s recent extended correction into early March. But gold’s young upleg since has increasingly dampened that mass exodus of American stock traders. Stabilizing gold investment precedes new buying, which is bullish for gold.

The venerable World Gold Council tracks and publishes the best-available global gold fundamental data on supply and demand. The all-important demand side is broken down into four categories which are jewelry, investment, central banks, and technology. That’s normally their size order. From 2015 to 2019, these categories averaged accounting for 51%, 29%, 12%, and 8% of overall global gold demand each year.

But 2020’s pandemic chaos shuffled these rankings, with lockdowns hammering jewelry demand while investment demand exploded. Those four categories represented 38%, 47%, 7%, and 8% of last year’s overall world gold demand. Yet even when jewelry is bigger, investment demand is far more important for moving gold prices. That’s because it is way more volatile, fluctuating greatly with investors’ herd psychology.

In the decade from 2010 to 2019, annual global jewelry demand varied by 669.1 metric tons or 33% at most. Yet the smaller yearly world investment demand, which averaged 4/7ths of jewelry demand during that span, had a much-bigger variance of 919.9t or 110%! So mercurial investment demand commands an outsized influence over gold-price trends, which was even more pronounced last year as COVID-19 raged.

The WGC’s awesome gold data is only released quarterly, with Q4’20’s Gold Demand Trends report the latest-available as I penned this essay. During 2020’s four quarters, investment demand ballooned to a staggering 52%, 58%, 55%, and 18% of gold’s world total. And of investment, exchange-traded funds buying physical gold bullion accounted for 54%, 74%, and 55% in Q1 to Q3. Q4 saw massive capital outflows.

The WGC also tracks the world’s physically-backed gold ETFs, and as last year wound to a close two American behemoths continued to dominate that space. Those are the GLD SPDR Gold Shares and the IAU iShares Gold Trust. Exiting Q4’20 holding 1,170.7t and 525.1t on behalf of their shareholders, these colossi commanded 31% and 14% of all the gold held by all the world’s gold ETFs! The third-largest was just 6%.

Led by GLD and IAU, investment capital flows into and out of gold ETFs are increasingly dominating gold demand and thus gold-price trends. Since they report their bullion holdings every market day, these gold ETFs also offer the highest-resolution read available on gold investment demand. Changes in gold-ETF holdings, particularly GLD’s and IAU’s, reveal whether investors are shifting money into or out of gold.

The only way gold ETFs can mirror gold’s price action is if their managers shunt excess ETF-share supply and demand directly into the underlying physical gold market. If GLD or IAU shares are bid up faster than gold itself, they threaten to decouple to the upside and fail their tracking mission. This must be averted by issuing enough new gold-ETF shares to offset that differential demand. The proceeds are used to buy gold.

So when GLD or IAU holdings are rising, it shows American stock-market capital flowing into gold bullion. These dominant ETFs have to act as capital conduits on the selling side too. When GLD or IAU shares are sold faster than gold, their shares prices will soon disconnect to the downside. So ETF managers must buy back enough of their shares to absorb that differential supply. They raise the funds by selling gold.

So the daily changes in GLD+IAU holdings reveal stock-market capital flows to and from gold. And due to their massive sizes and the increasing importance of gold ETFs in general, GLD+IAU holdings are the best daily proxy for overall global gold investment demand. That World Gold Council quarterly data sure confirms this, as the last several quarters of 2020 reinforce. GLD+IAU are a force of nature in the gold markets.

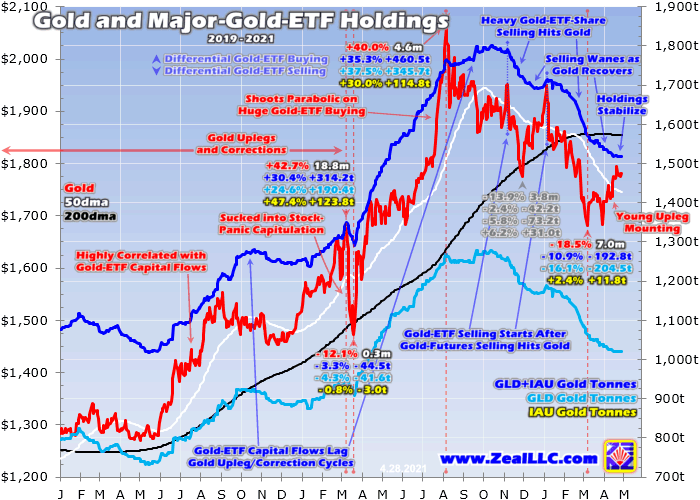

This chart superimposes GLD’s and IAU’s physical-gold-bullion holdings in metric tons over gold prices in the last couple years or so. GLD+IAU are rendered in dark blue, GLD alone in light blue, and IAU would be in yellow had its holdings been big enough for this chart’s axis. Gold’s price is shown in red. There’s no doubt American-stock-market capital flows into and out of gold via these ETFs has a huge price impact.

From last March’s COVID-19-lockdown-fueled stock panic to early August, gold soared 40.0% higher in just 4.6 months in a mighty upleg. During that exact span, GLD+IAU holdings rocketed 460.5t or 35.3% higher! That was an enormous amount of differential gold-ETF-share buying, huge inflows of American stock-market capital pushing gold higher. Based on its average price in that span, a ballpark estimate is $25.9b.

Unfortunately that can’t be directly compared to the WGC’s overall investment data, which is parsed only in calendar-quarter terms. But peak GLD+IAU inflows during that last gold upleg came in Q2’20, where these two ETFs’ holdings soared 276.8t or 20.4% higher. That represented nearly 64% of the entire gold buying by all the world’s gold ETFs! And that in turn weighed in at 74% of overall global investment demand.

Because American stock traders command such vast pools of capital, and since GLD and IAU are their gold trading vehicles of choice, these colossal ETFs increasingly dominate the global gold markets. So tracking the trends in their daily holdings changes is exceedingly important for everyone speculating or investing in gold, silver, and their miners’ stocks. GLD and IAU are pipelines linking stock markets to gold.

That gargantuan differential gold-ETF-share buying last summer helped catapult gold parabolic, leaving it extraordinarily overbought in early August. The popular greed leading into that major topping was immense. The great majority of gold-stock-ETF traders are momentum players, piling on en masse after trends run long and big enough to be widely noticed. They only like to buy or sell as a herd when everyone else is.

This momentum-following dynamic causes gold-ETF holdings to lag major toppings and bottomings in gold. Those are mostly driven by gold’s other primary driver, which is speculators’ gold-futures trading. While they wield vastly less capital than American stock traders, the futures speculators employ extreme leverage which greatly amplifies their gold-price impact. That necessarily compresses their trading time horizons.

Each gold-futures contract controls 100 troy ounces of gold, which was worth $178,200 in the middle of this week. Yet speculators are only required to keep $10,000 cash in their accounts for each contract they bought or sold. That implies crazy maximum leverage of 17.8x, radically exceeding the decades-old 2x legal limit in the stock markets! The unforgiving risks at those extremes forces speculators to be myopic.

A mere 5.6% gold move against their bets would wipe out 100% of their capital risked! So all they can care about is ultra-short-term gold-price action measured in days to weeks on the outside. This hyper-leveraged gold-futures trading is what carves major gold tops and bottoms. But those inflection points are rarely obvious in real-time, so gold’s prevailing herd psychology doesn’t start adjusting until well later.

When gold peaked in early August, GLD+IAU holdings ran 1,765.0t. But even as gold rolled over into a young correction, they continued climbing on balance for another 2.3 months into mid-October. That minor 2.0% build happened despite gold selling off 7.8%. It takes some time for gold sentiment to shift after a major high or low, so the momentum-driven gold-ETF-share trading lags gold’s upleg-correction transitions.

After a couple months with gold grinding lower on balance, American stock traders increasingly realized gold’s meteoric ascent had failed. With that upward momentum broken, they stopped upping their capital allocated to gold via ETFs. But they generally seemed content to hold their new positions in GLD and IAU, until gold plummeted 4.4% on November 9th. That gold-futures-driven collapse really scared them.

That was the day Pfizer reported its new mRNA COVID-19 vaccine was over 90% effective in trials, which offered the first real hope this pandemic would end. Gold-futures traders aggressively dumped contracts on that paradigm shift, which also pushed the US stock markets and US dollar sharply higher. Big gold-futures selling often snowballs to become self-feeding, as falling gold triggers stop losses forcing gold lower still.

The heavy differential GLD- and IAU-share selling in gold’s last correction didn’t start until that frightening day shattered remaining bullish sentiment. Then newly-fearful American stock traders joined the gold-futures speculators in hammering the yellow metal lower. Unfortunately speculators’ gold-futures trading can be the small tail wagging the vastly-larger gold-investment dog. Gold’s price action drives its popular psychology.

So heavy gold-futures selling, which is never sustainable for long because speculators’ capital is limited, effectively sends false price signals. At 18x leverage, every $1 of gold-futures selling has the same gold-price impact as $18 of outright gold selling! So American stock traders see gold plummeting, assume that must prove weakening fundamentals, and join in to amplify gold’s selloff. That dynamic works in reverse too.

After that frenzied selloff into late November where gold-futures and gold-ETF-share dumping reinforced each other, gold’s correction appeared to bottom on November 30th. Closing at $1,775, gold was finally oversold after a 13.9% correction over 3.8 months. That happened to be right in line with the precedent from this secular gold bull’s earlier three corrections, which averaged 14.3% losses over 4.1 months each.

So gold-futures speculators started to buy, driving this metal sharply higher in December. But like usual, differential GLD- and IAU-share buying also lagged gold. That day gold bottomed, the GLD+IAU holdings were running 1,722.7t. But over the next several weeks where gold surged 4.8% higher, these two dominant gold ETFs’ holdings fell another 1.9% to 1,690.6t. That again reflected sentiment gradually shifting.

The serious fear spawned by gold’s November plunge took some time to dissipate. The great sentiment pendulum swinging from greed to fear slows near extremes before accelerating back the other way. But as gold’s gains mounted in its apparent young upleg, American stock traders started buying the gold-ETF shares again in late December. The GLD+IAU builds resumed until gold suffered another brutal plummeting.

On January 8th, gold collapsed 3.5% after the psychologically-heavy $1,900 level failed overnight. That spooked gold-futures speculators into fleeing again, battering gold sharply lower. Just like back in early November, that single-day plummeting completely changed psychology among American stock traders. Again they started selling gold-ETF shares faster than gold was being sold, exacerbating its accelerating selloff.

The chart above has two vertical dotted-blue lines showing when these two gold plummetings happened. Those were exactly when heavy differential GLD+IAU share selling ignited, the gold-futures tail wagging the gold-investment dog! Yet again into early March, gold-futures and gold-ETF selling intensified as they played off each other. The more contracts and shares sold, the faster gold fell unleashing still more dumping.

That prematurely slayed gold’s young upleg, cascading into an anomalous extended correction fueling dismally-bearish psychology. Gold plunged into March 8th when it bottomed again at $1,681. That made for a monster 18.5% correction over 7.0 months, the worst yet seen in this secular bull. But speculators’ big gold-futures selling was quickly exhausting itself, with their contracts available to puke out quite finite.

I wrote a contrarian essay explaining that gold momentum selloff in early March, published the trading day before gold bottomed. I concluded then “The good news is the gold-futures selling that ignited all this is finite, and is likely nearing exhaustion. After that, gold should rally hard.” Indeed that soon came to pass. But as gold bounced sharply into mid-March and April, American stock traders still kept on fleeing gold ETFs.

Once again that lag effect kicked in, where it takes a month or two for gold sentiment to start reflecting a sharp futures-driven trend change. By late April about six weeks later, GLD+IAU holdings had dropped another 52.7t or 3.4%. That was during a span where gold surged 6.7% higher. But with gold rallying on balance again, the rate of differential gold-ETF-share selling was waning just like it had back in December.

This best daily proxy for global gold investment demand was stabilizing, which is a very-bullish omen for gold. Major gold uplegs are driven by big investment capital inflows into the yellow metal. These are first triggered by rising gold prices after correction bottomings, resulting from speculators buying gold futures. Eventually gold rallies long and high enough to start enticing American stock traders to return, to resume buying.

Again the great majority of gold-ETF-share traders need to see gold momentum to entice them to pile on to chase it. While that hasn’t happened yet as evidenced by GLD+IAU holdings still not climbing, it is coming. The pace of gold-ETF draws slowing, revealing dwindling bearishness, is necessary before mounting bullishness starts fueling capital inflows into gold again. These holdings troughs come early in uplegs.

That’s when American stock traders increasingly realize the preceding gold correction has given up its ghost. They are really attracted to gold’s mounting early-upleg momentum, and want to redeploy capital to chase those gains. So their differential gold-ETF-share selling slows, then stops, then starts reversing into differential buying. And once that gets underway in earnest, it forms a virtuous circle forcing gold higher.

The more GLD and IAU shares traders buy, the more these giant gold ETFs’ managers have to shunt excess demand directly into gold itself. Again they have to issue new shares to offset any demand above gold’s own, and the proceeds are used to buy more physical gold bullion boosting their holdings. And the more gold buying, the faster gold rallies. That entices more traders to buy even more gold-ETF shares!

We are nearing that crucial inflection point where gold investment demand reemerges in a young upleg before soon becoming self-sustaining. And there’s certainly good reason for diversifying portfolios with gold. Central banks are printing money at astounding epic rates like there is no tomorrow, and as a result stock markets are dangerously overvalued while serious price inflation is becoming increasingly evident everywhere.

The main beneficiaries of investment-demand-driven major gold uplegs are the gold miners’ stocks. The larger ones in the leading GDX gold-stock ETF generally leverage gold moves by 2x to 3x. And the smaller fundamentally-superior mid-tier and junior gold miners with far-better production-growth prospects tend to well outperform larger peers. So we used gold’s weakness in recent months to fill our newsletter trading books.

At Zeal we walk the contrarian walk, buying low when few others are willing before later selling high when few others can. We overcome popular greed and fear by diligently studying market cycles. We trade on time-tested indicators derived from technical, sentimental, and fundamental research. That’s why all 1178 stock trades recommended in our newsletters since 2001 averaged hefty +24.0% annualized realized gains!

To multiply your wealth trading high-potential gold stocks, you need to stay informed about what’s going on in this sector. Staying subscribed to our popular and affordable weekly and monthly newsletters is a great way. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today while this gold-stock upleg remains young! Our newly-reformatted newsletters have expanded individual-stock analysis.

The bottom line is gold investment demand is stabilizing. After plunging and exaggerating gold’s recent extended correction, the physical-gold-bullion holdings of the two giant dominant gold ETFs are carving a trough. Gold’s mounting upside momentum in this young-upleg rallying is increasingly shifting sentiment from bearish back to bullish again. American stock traders are intrigued, and tempted to start chasing.

They are ready to resume buying, bidding up gold-ETF shares faster than gold is being bought. Those big capital inflows will force the gold ETFs to shunt that excess demand directly into gold, amplifying its gains. That will stoke more greed among gold-ETF and gold-futures traders, unleashing more self-feeding buying. As gold powers higher in the resulting strengthening upleg, gold stocks will really leverage its upside.

Adam Hamilton, CPA

April 30, 2021

Copyright 2000 - 2021 Zeal LLC (www.ZealLLC.com)

About the author