The major gold miners’ latest quarterly results proved epic! Thanks to record gold prices, they achieved record revenues, record bottom-line earnings, and record operating cash flows. Such amazing profits drove down gold-stock valuations to their most-undervalued levels in many years. These super-strong fundamentals combined with gold’s healthy and overdue pullback are creating excellent buying opportunities.

The GDX VanEck Gold Miners ETF remains this sector’s dominant benchmark. Birthed way back in May 2006, GDX has parlayed its first-mover advantage into an insurmountable lead. Its $13.2b of net assets mid-week dwarfed the next-largest 1x-long major-gold-miners ETF by nearly 19x! GDX is undisputedly the trading vehicle of choice in this sector, with the world’s biggest gold miners commanding most of its weighting.

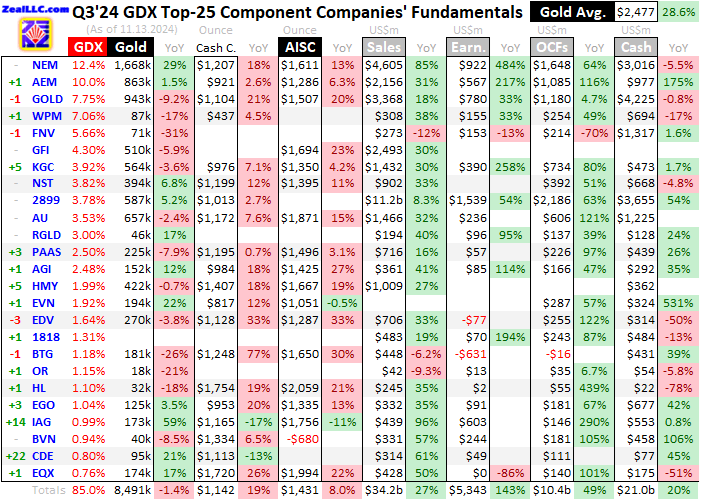

Gold-stock tiers are defined by miners’ annual production rates in ounces of gold. Small juniors have little sub-300k outputs, medium mid-tiers run 300k to 1,000k, large majors yield over 1,000k, and huge super-majors operate at vast scales exceeding 2,000k. Translated into quarterly terms, these thresholds shake out under 75k, 75k to 250k, 250k+, and 500k+. Those two largest categories account for over 53% of GDX.

Gold stocks have been correcting hard in recent weeks, exacerbated by gold plunging in the wake of the US elections. Traders view Trump’s tax cuts and tariffs as inflationary, slashing Fed-rate-cut odds. The prospects of higher yields going forward catapulted up the US Dollar Index a massive 2.9% in just six trading days! That shook lose colossal gold-futures selling, hammering gold 6.1% lower since Election Day.

Gold stocks per GDX plunged 11.3% in sympathy, actually making for fairly-mild 1.9x downside leverage to the metal which overwhelmingly drives their profits. Usually GDX tends to amplify material gold moves by 2x to 3x. At worst since late October, gold’s total pullback is running 7.6%. That selloff was overdue and expected. Just a few weeks earlier, I wrote a whole essay analyzing why gold’s selloff risk was high.

At best gold had soared an incredible 35.0% year-to-date, trouncing the S&P 500’s 21.9% gains! That left gold extremely-overbought, and speculators’ gold-futures positioning exceedingly-overextended. So a sentiment-rebalancing selloff on these hyper-leveraged traders normalizing their bets was inevitable. We ratcheted up trailing-stop-loss percentages on our gold-stock trades to prepare, soon realizing big-to-huge gains.

While gold stocks have surged dramatically this year, they still really lagged gold with GDX up 42.2% YTD at best in late October. Gold stocks were starting to catch up with their metal, accelerating towards that 2x-to-3x upside leverage. But GDX’s correction ignited before gold’s, after the world’s largest gold miner reported disappointing and misleading Q3 results. There’s much more below on Newmont’s latest debacle.

Gold stocks’ total correction extended to 19.3% as of mid-week, which is perfectly-normal 2.6x downside leverage to gold. Speculators and investors rushing to buy gold stocks in mid-October as GDX made a dazzling secular breakout and challenged a far-bigger one ought to be licking their chops! Being able to now buy in about 20% cheaper with gold miners printing money in this gold environment is awesome.

For 34 quarters in a row now, I’ve painstakingly analyzed the latest operational and financial results from GDX’s 25-largest component stocks. Mostly super-majors, majors, and larger mid-tiers, they dominate this ETF at 85.0% of its total weighting! While digging through quarterlies is a ton of work, understanding the gold miners’ latest fundamentals really cuts through the obscuring sentiment fogs shrouding this sector.

This table summarizes the operational and financial highlights from the GDX top 25 during Q3’24. These gold miners’ stock symbols aren’t all US listings, and are preceded by their rankings changes within GDX over this past year. The shuffling in their ETF weightings reflects shifting market caps, which reveal both outperformers and underperformers since Q3’23. Those symbols are followed by their current GDX weightings.

Next comes these gold miners’ Q3’24 production in ounces, along with their year-over-year changes from the comparable Q3’23. Output is the lifeblood of this industry, with investors generally prizing production growth above everything else. After are the costs of wresting that gold from the bowels of the earth in per-ounce terms, both cash costs and all-in sustaining costs. The latter help illuminate miners’ profitability.

That’s followed by a bunch of hard accounting data reported to securities regulators, quarterly revenues, earnings, operating cash flows, and resulting cash treasuries. Blank data fields mean companies hadn’t disclosed that particular data as of the middle of this week. The annual changes aren’t included if they would be misleading, like comparing negative numbers or data shifting from positive to negative or vice-versa.

In mid-October well before this latest earnings season got underway, I predicted gold miners’ epic quarter in an essay. That concluded “dazzling record gold prices combined with forecast lower mining costs will catapult unit earnings to astounding levels. They are likely to about double to amazing records, extending gold stocks’ massive-earnings-growth streak to five consecutive quarters.” Indeed that mostly came to pass.

Despite their epic quarter, as long-time readers know I’ve never been a fan of most of the world’s largest gold miners that dominate GDX. They perpetually fail to organically grow their production at their vast operational scales, unable to overcome depletion. They’ve mostly been able to boost output only through expensive acquisitions. And paradoxically their mining costs have been rising faster than their smaller peers’.

So for a quarter-century now, our very-profitable subscription-newsletter gold-stock trading has focused on fundamentally-superior smaller mid-tiers and juniors. Operating fewer gold mines often at lower costs, they are better able to consistently grow production through expansions and new mine-builds. Both their earnings growth and stock-price appreciation have long proven way better than GDX’s super-majors and majors.

GDX’s little-brother GDXJ ETF mostly comprised of mid-tiers is much better. Like usual I’ll analyze the GDXJ-top-25 stocks’ Q3’24 results in next week’s essay. I bring this up now because the world’s biggest gold miners certainly aren’t best-in-breed. Last quarter was the seventh in a row where the GDX top 25’s production slumped, now by 1.4% year-over-year to 8,491k ounces. That seriously underperformed this industry.

About a month after every quarter when earnings season is underway, the World Gold Council publishes the best-available global gold supply-and-demand data. That’s detailed and analyzed in the fantastic Gold Demand Trends reports, which are essential reading for gold-stock traders. The WGC found that world gold-mining output actually grew a strong-and-impressive 5.8% YoY to 31,824k ounces in Q3’24!

Last quarter’s GDX-top-25 output was only halfway up into its past-34-quarter range. That’s despite the world’s biggest gold miner Newmont reporting Q3 production rocketing up 29.3% YoY to 1,668k ounces! That sounds fantastic, but two big factors make it misleading. First the comparable quarter’s output was slashed by a major strike at one of Newmont’s larger gold mines in Mexico, which suffered zero output in Q3’23.

Second Newmont paid $16.8b last year to gobble up Australian super-major Newcrest Mining, with that deal closing in early November 2023. Rather damningly even despite that strike, in Q3’23 the combined output of NEM and NCM actually ran 1,744k ozs which was much better than Q3’24’s! To establish a baseline, in the four quarters before Q3’23 NEM+NCM production averaged a way-higher 1,979k ounces.

Newmont has actually cursed the gold-mining sector for years, seriously damaging sector returns and institutional-investor perceptions through rank mismanagement. I’ve written extensively about this in the past, including why NEM’s gold-stock mega-mergers are really bad for this sector. Newmont overpays wildly, resulting in tens of billions of dollars of subsequent writeoffs that really tank overall sector earnings.

NEM is not only the world’s biggest gold miner, but the only one included in the S&P 500. So for large fund managers, Newmont is the only gold stock liquid enough for them to consider taking positions in. And Newmont’s operational performance has proven so inferior to its peers’ for decades that a Newmont-centric view of gold stocks will sour anyone on this sector. Q3’24 saw another infuriating case in point on this.

Most gold miners offer production and cost guidance, trying to set market expectations. Released early in new years, this can naturally change as individual mines encounter operational challenges or unexpected outperformance. Good managements adjust their guidances as conditions shift, but not Newmont! It is endlessly overpromising, pretending everything is awesome, then underdelivering to disappoint everyone.

Back in late February, NEM initially set 2024 guidance at 6.9m ounces of gold mined around all-in sustaining costs of $1,400 per ounce. That was good, as this company produced 5.5m ounces in 2023 at higher $1,444 AISCs. In late April Newmont’s Q1’24 results reported AISCs of $1,439, and management declared then NEM was “Firmly on track to deliver 2024 guidance for production, costs and capital spend”.

In late July NEM reported mining 1.6m ounces at way-higher $1,562 AISCs in Q2’24. Management tried to obscure those from investors, removing AISCs from the opening summary of the quarterly press release to bury deeper in a table! And 2024’s guidance was again reaffirmed, with the assertion “On track to deliver 2024 guidance for production, costs and capital spend”. On the crucial AISC front, that meant $1,400.

In H1’24, Newmont’s AISCs averaged $1,500 per ounce. Thus to hit that still-active guidance of $1,400 on the year, H2’24’s AISCs would have to plunge to a $1,300 average. NEM intentionally implied some hope of that, asserting “anticipating a sequential increase in production in the second half of the year, weighted towards the fourth quarter”. I was skeptical of $1,300 after Newmont’s long history of disappointing.

Meanwhile gold and GDX were surging into late summer and early autumn, the metal hitting many new nominal record closes. GDX broke out to a 4.2-year high in late October, and closed a mere 0.9% under achieving an epic 11.8-year one! With gold still powering higher on balance, that psychologically-huge gold-stock secular breakout would’ve happened within days and accelerated the bullish sentiment shift.

Most gold miners would issue separate press releases between quarterly results if operations materially affected their guidances. There were plenty of examples of that in Q3’24, including from the GDX top 25’s best performer operationally last quarter IAMGOLD. It is ramping up a major new mine-build, which is why its production soared and mining costs plunged. But that process encountered some setbacks.

Processing plants naturally have to be adjusted when they first come online, as the actual ores run through vary from what geologists projected. IAG had to shut down its mill for over a week to replace components with ones better suited to the ores. So it warned that mine’s 2024 guidance was lowered from its 153k-attributable-ounce midpoint to the lower end near 130k. IAG’s stock still climbed 3.3% the next day!

Investors fully realize plans change, we just like to be informed not blindsided. But the inept management running Newmont doesn’t respect investors. Just one day after GDX achieved that awesome secular high, NEM released its Q3’24 results after the close. Those were mostly great, with revenues, earnings, and operating cash flows skyrocketing 85%, 484%, and 64% YoY! 2024 output guidance was even reaffirmed.

But management again tried to hide soaring AISCs, not mentioning them at all in the quarterly summary like every other gold miner. Those actually shot up 13.0% YoY to $1,611 in Q3’24, averaging $1,537 in 2024’s first three quarters! Still rather than come clean and raise 2024 cost guidance, NEM merely said it expected “All-In Sustaining Cost (AISC) of $1,475 per ounce in the fourth quarter”. Soaring costs weren’t analyzed.

Most gold miners seeing rising costs detail exactly why and what they are doing to mitigate those. But not Newmont. If Q4’24 AISCs actually come in at $1,475 which seems unlikely given its long track record of misleading investors, 2024’s would average $1,522. That’s a big miss, but investors might not care much with far-higher prevailing gold prices. But NEM’s dissembling leaves analysts wondering what else it is disguising.

In my line of work as a professional gold-stock speculator and newsletter writer for a quarter-century now, I talk with plenty of fund managers. I consult for some as well. Every time Newmont comes up, you can just feel the contempt for its poor management and endless underperformance. It has long been a pox on this sector, deadweight dragging down its peers. The day after those Q3’24 results, NEM’s stock crashed 14.7%!

Dumbfoundingly that was its worst daily loss in 27 years in the best quarter ever for gold stocks! And that didn’t even happen in a weak sector tape, as gold rallied 0.7% that day for GDX to amplify. Most of the radically-superior mid-tiers and juniors in our newsletter trading books were flat or even climbed a bit that day! But NEM’s dishonest attempts to obscure cost challenges left institutional investors totally exasperated.

Wall Street didn’t understand what had happened, blaming NEM’s crash on a relatively-minor earnings-per-share miss. But that event tainted gold-stock sentiment among fund managers, prematurely forcing this sector to correct. Again for professional investors and analysts not focused on gold stocks, Newmont is the only supposed-blue-chip gold miner they would consider. And it pooped in the punch bowl with that Q3 report!

Newmont wasn’t alone on costs, most major gold miners suffered sharply-higher ones last quarter. Those were mostly blamed on rising labor prices in the latest 10-Qs. A sizable fraction of the GDX top 25 said their AISCs this year are going to come in at the upper end of their 2024 guidances. Yet their stocks didn’t plunge after their Q3 results, as those managements were honest and open explaining those challenges.

Unit gold-mining costs are generally inversely proportional to gold-production levels. That’s because gold mines’ total operating costs are largely fixed during pre-construction planning stages, when designed throughputs are determined for plants processing gold-bearing ores. Their nameplate capacities don’t change quarter to quarter, requiring similar levels of infrastructure, equipment, and employees to keep running.

So the only real variable driving quarterly gold production is the ore grades fed into these plants. Those vary widely even within individual gold deposits. Richer ores yield more ounces to spread mining’s big fixed expenses across, lowering unit costs and boosting profitability. But while fixed costs are the lion’s share of gold mining, there are also sizable variable costs. That’s where recent years’ raging inflation hit hard.

Cash costs are the classic measure of gold-mining costs, including all cash expenses necessary to mine each ounce of gold. But they are misleading as a true cost measure, excluding the big capital needed to explore for gold deposits and build mines. So cash costs are best viewed as survivability acid-test levels for the major gold miners. They illuminate the minimum gold prices necessary to keep the mines running.

The GDX top 25’s cash costs last quarter soared 19.2% YoY to a record $1,142 per ounce. The previous high was the preceding Q2’24’s $1,020. Gold-mining costs naturally follow gold higher, but way more slowly than that. Better gold prices eventually allow lower ore grades to be mined, which force unit costs higher. Q3’s cash-cost inflation is concerning, way worse than the prior-four-quarter average increase of 3.2% YoY.

All-in sustaining costs are far superior than cash costs, and were introduced by the World Gold Council in June 2013. They add on to cash costs everything else that is necessary to maintain and replenish gold-mining operations at current output tempos. AISCs give a much-better understanding of what it really costs to maintain gold mines as ongoing concerns, and reveal the major gold miners’ true operating profitability.

Unfortunately the GDX top 25’s AISCs, which are mostly comprised of those cash costs, proved very disappointing as well in Q3. They surged 8.0% YoY to $1,431 per ounce, their highest levels ever! In the four quarters before that, GDX-top-25 AISCs had actually averaged 3.5%-YoY declines with inflation coming back under control. The previous record was $1,405 in Q3’22. Again labor costs were most often cited.

Those sharply-higher AISCs were the chonky fly in the ointment in the major gold miners’ latest results. In my mid-October essay previewing gold miners’ epic quarter, I had explained that “A surprising number of major gold miners continued guiding to considerably-lower costs in Q3 and Q4.” I even used Newmont as an example, which I did qualify with “While I really doubt NEM will achieve such low Q3 and Q4 AISCs...”

With Q2’24’s GDX-top-25 AISCs clocking in at a nine-quarter low of $1,239 and plenty of gold miners forecasting better H2’24 costs, my worst-case scenario for Q3’24’s was $1,350. So seeing $1,431 was quite a shock. And that includes Buenaventura’s crazy negative $680 per ounce! Its big silver, zinc, and lead output used as gold byproduct credits skyrocketed 122%, 98%, and 251% YoY from a mine expansion.

Still since Q3’24’s average gold price soared 28.6% YoY to a nominal record high of $2,477, the major gold miners were super-profitable even with high $1,431 AISCs. Subtract those, and implied sector unit profits ran $1,046 per ounce. I sure didn’t expect them to print under Q2’24’s dazzling record $1,099, but those are still fat-and-rich earnings. They soared 74.0% YoY from Q3’23’s, and that’s nothing new for gold stocks.

During these last five reported quarters ending in Q3, the GDX top 25’s implied unit earnings rocketed by 87.2%, 42.3%, 34.9%, 83.7%, and 74.0% YoY! That massive profits growth is unequalled in all the stock markets, truly remarkable. And despite gold’s healthy pullback, this current half-over Q4’24 is shaping up to be another stunner. So far this quarter, gold is averaging $2,686 which would make for a 36%-YoY soaring!

But even if gold’s pullback or larger correction hasn’t fully run its course yet, if gold averages a far-lower $2,515 for the rest of Q4 this quarter would still achieve $2,600 overall. And the majority of the GDX-top-25 gold miners with guidances still see AISCs improving into year-end. Assume $2,600 gold and $1,400 AISCs in Q4, and we’d be looking at record $1,200-per-ounce profits skyrocketing another 100% YoY!

While it was a bummer last quarter’s AISCs came in much higher than expected, the underlying hard accounting numbers reported to securities regulators were spectacular. The GDX top 25’s total revenues soared 27.0% YoY in Q3 to a record $34.2b! That matches gold’s quarterly-average 28.6% gain less that 1.4% output shrinkage. That huge sales growth catapulted bottom-line GAAP earnings an epic 142.7% higher!

Those hit $5.3b for the GDX top 25, astounding levels! And they were pretty clean, as gold miners as a group are often flushing unusual large unrealized and sometimes realized gains and losses through their income statements. The most-common ones are impairments to mines’ carrying values on books and occasionally reversals of those. I track these, and reversing out material ones yields even-better Q3 profits.

Adjusted those ran $5,828m, skyrocketing 152.0% YoY from Q3’23’s adjusted levels! Either way, major gold miners’ Q3’24 earnings were their highest ever reported by far. The gold miners are printing money at these lofty prevailing gold prices, which will enable them to expand existing mines and build new mines to overcome depletion and hopefully grow their output. Q3’24 indeed proved gold miners’ best quarter ever!

That forced down gold-stock valuations to their lowest levels seen in my 34-quarter research thread, and maybe ever with such gigantic earnings. Early this week, the GDX top 25 averaged trailing-twelve-month price-to-earnings ratios of just 22.5x. That was skewed higher by a few outliers, with plenty of major gold miners trading in the low double-digits. And most of these P/Es don’t even yet include Q3’s just-reported profits!

So the major gold miners’ Q3’24 results proved epic overall. It was disappointing AISCs surged sharply, and infuriating Newmont deceptively trying to hide them blasted gold-stock sentiment on the verge of a huge secular breakout! But holy cow the gold miners still have massive room to run to reflect these awesome prevailing gold prices. They could easily double from here with such epic fundamentals on strong gold.

This overdue gold pullback and resulting gold-stock correction are great gifts. Speculators and investors who were interested in gold stocks in late October should be salivating at buying much lower soon here. After our newsletter trades were stopped out at big realized gains, I’m looking to reload our trading books with fundamentally-superior mid-tiers and juniors as gold’s selloff matures. Then gold stocks are off to the races.

Successful trading demands always staying informed on markets, to understand opportunities as they arise. We can help! For decades we’ve published popular weekly and monthly newsletters focused on contrarian speculation and investment. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks.

Our holistic integrated contrarian approach has proven very successful, and you can reap the benefits for only $10 an issue. We extensively research gold and silver miners to find cheap fundamentally-superior mid-tiers and juniors with outsized upside potential. Sign up for free e-mail notifications when we publish new content. Even better, subscribe today to our acclaimed newsletters and start growing smarter and richer!

The bottom line is major gold miners just reported their best quarter ever by far! Fueled by dazzling record gold prices, revenues, earnings, and operating cash flows all blasted up dramatically to all-time record highs. And that was despite resurgent mining costs also climbing to records partially fueled by more-expensive labor. Those fat-and-rich profits drove gold-stock valuations to their lowest in many years.

Gold stocks are correcting now, forced by gold’s overdue rebalancing selloff after it soared to extreme overboughtness on excessively-bullish speculator gold-futures positioning. The world’s largest gold miner trying to obscure rising costs sparked the gold-stock selling. But what an amazing opportunity to add gold stocks at deep discounts with their strongest and most-bullish fundamentals ever. Their upside is far from over.

Adam Hamilton, CPA

November 15, 2024

Copyright 2000 - 2024 Zeal LLC (www.ZealLLC.com)

About the author