The gold stock correction is playing out mostly as expected, now hitting targets

Back in January we (NFTRH) targeted the PDAC time frame (1st week of March) for a much needed correction of the excesses to begin. Gold stocks, along with gold and silver were due for a beat down after all that 2025 bullishness and market leadership.

This was aside from the fundamentals, which have deteriorated to a moderate degree in 2026. It was simply market mechanics. The market was going to find some excuse to knock gold stocks down. That excuse finally came in the form of war and the resulting spike in oil prices (oil/energy being a heavy factor in mining costs).

It may sound obvious, but there is a distinction within the gold stock universe. Mining companies will be at least temporarily dragged by the spike in energy. Royalty and Exploration generally will not. These are sector fundamentals. On the macro, the wider gold stock correction does not care about sector fundamentals. It cares about emotion, and there’s plenty of that flying around right now.

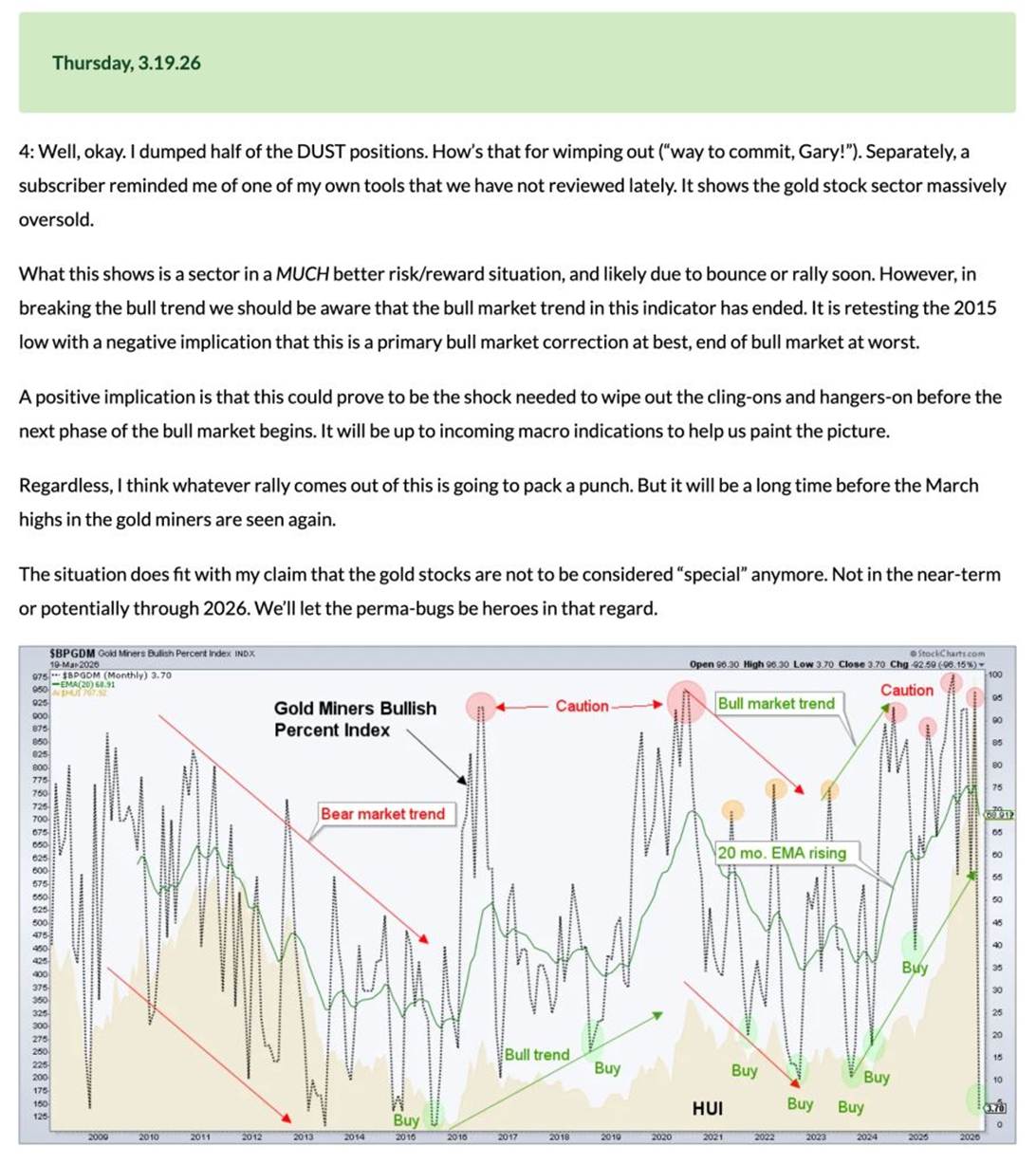

BPGDM is on a “buy” signal, as it is oversold to the degree of the 2015 low, which launched the bull market. But you will notice a broken trend in the indicator. Gold stocks are going to bounce, rally or potentially incinerate the shorts. But the broken bull trend in BPGDM implies a primary correction. Per yesterday’s in-week subscriber notes:

Note 4 was discussion of the BPGDM and its implications. Notes 1-3 included gold stocks I bought on Thursday (under cover of gold miner, gold and silver short hedges) as they tanked to downside targets we’d projected in NFTRH 906 last weekend.

Fundamental Note

As far back as last year the advice to subscribers was that more commodities – including energy commodities – would join the bull market. Royalty companies (e.g. Royal Gold, Wheaton, Franco and the likes of several smaller and intermediate Royalties) and Mineral Exploration operations (hole drillers) would have more weight in our view. That is because their cost structures will be relatively unscathed by the effects of inflation.

GDX and the Daily Chart Technical Situation

You noticed no bullish public posts from me during 2026 so far, and from this post on January 25 discussing corrective options for HUI:

…the first correction could feel like a cyclical bear market in its intensity.

Since then, management of the gold stock correction was reserved for the premium service. Subscribers always come first in my world. Never will I spew out critically actionable, real-time public intelligence to attract eyeballs. But today correction management is all done and now we look to capitalize in a different and more pleasant direction (with patience and no undue exclusive obsession on the sector).

As to the gold stock correction in general, it turned out not to be as simple as picking a target. Our favored targets are highlighted at left of each of the Fibonacci grids shown on the daily chart of GDX. The upper levels were hit on Thursday at a clear visual support (green shaded) in the 80-82 area.

But over the scope of the correction, it was not as easy as picking a downside target and preparing for it. Because of course GDX/HUI, etc. put in marginal higher highs (double top) amid negative RSI divergence at point (B) of an A-B-C corrective structure. The volume into corrective leg (A) looks climactic, but it was not. It was the first leg getting kicked out from under the table. Then a rise to (B) on low volume into a cruel bull trap. Then?

Here we are. The gold stock correction has made itself known to one and all after NFTRH tracked the process for all of 2026 so far. We were well prepared for the now hysterical downside event taking place (personally, short to hedge as noted above).

While there could easily be more short-term downside, as per the clip of yesterday’s subscriber notes above, the gold stock sector is in a much better risk/reward situation. A majority of the downside is in the books and it is time to slowly, patiently plot buying opportunities for a tradeable rally, at least.

Beyond Gold Stocks

As noted above, whatever unfolds, the gold stock sector is no longer special, as wider inflation trades are expected to take hold across commodities and certain markets. Oil and the current inflation mini-hysteria * is not that. Not yet.

I expect 2027 to ultimately shake out inflationary. But in the interim we continue to await the first deflation scare of the new macro. Once again, our pictorial view of the new macro:

* Spiking oil prices are not the result of monetary policy. Hence not the result of inflation. The last inflationary operation took place in H1, 2020 as the Fed blew a gasket and the government (Trump 1.0 & then Biden) spewed newly printed funny munny across the land. The inflation problem then predictably became apparent starting in 2021. When oil prices resolve, I expect disinflation to continue and likely morph to a deflation scare prior to the next inflationary operation, which will at first feel good, but soon turn quite unpleasant in its after-effects.

About the author