Strengths

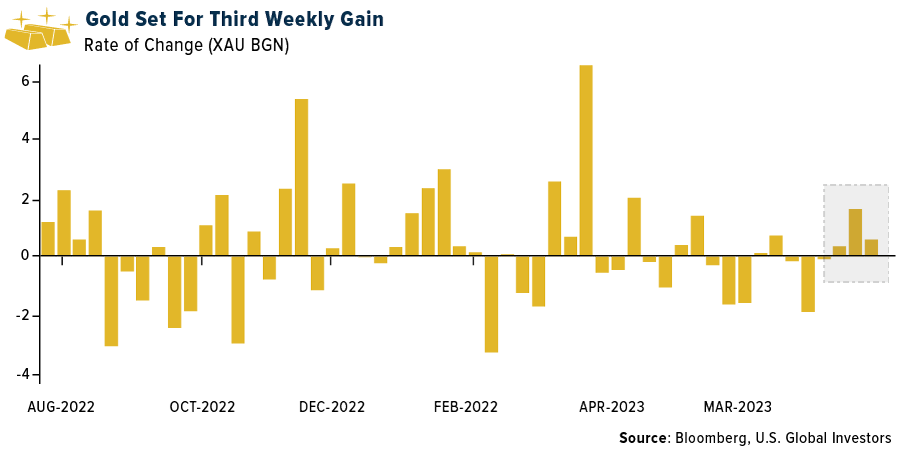

- The best performing precious metal for the week was palladium, up 1.71%. Gold is set to eke a third weekly gain despite going into next week’s likely 25-basis point lift in interest rates. Markets expect the Federal Reserve to pause again on further hikes. Northam Platinum chose to tender its 34.5% stake in Royal Bafokeng Platinum (RBPlat) by finally accepting the mandatory offer from Impala Platinum (Implats), which comprises R90 in cash and 0.30 Implats shares per RBPlat share held. Based on the last closing price for Implats, this implies an offer price of R131/share or R13.1bn for Northam's stake.

- According to Scotia, Q2/23 gold production is expected to be 7% better than Q1/23. They are forecasting group Q2/23 production of 6 million ounces, 7% higher than Q1/23 of 5.6 million ounces but 5% lower than Q2/22. Most companies are guiding for a stronger 2H/23, especially Q4/23, due to grade sequences and less maintenance shutdowns.

- Karora Resources had record quarterly production of 40.8k ounces gold, which beat consensus of 37.9k ounces (+8%) and was up +3% q/q. gold sales of 42.2k ounces landed modestly above production. The unaudited Q2/23 cash balance was reported at C$71M, up from C$66M as of Q1/23.

Weaknesses

- The worst performing precious metal for the week was platinum, down 1.1.12%. Evolution Mining cut its 2024 gold production forecast to 770,000 ounces, down from 800,000. Sustaining capital was raised by A$10 million but the range for major capital expenditures was broadened to A$320 million to $380 million from A$325 million to A$350. Production for the second quarter was down 2.5% quarter over quarter and missed analyst estimates.

- The value of polished stone exports from India – a proxy for demand – was down 31% YoY (20% MoM), while volumes decreased by 29% YoY (10% MoM), implying aggregate prices declined MoM and YoY, possibly due to a mix change. Polished diamond export volumes and value came in below the 5-year average.

- Anglo American Platinum (Amplats) released a trading statement guiding to a 65-75% decline YoY in its 1H23 headline earnings per share (HEPS) to between R25.44-35.69/share, missing Visible Alpha consensus earnings of R47.42 by 36%. The key driver of the miss could be due to higher than forecast unit costs and therefore the market will likely view this trading statement in a negative light.

Opportunities

- A Civil War-era treasure of more than 700 gold coins was unearthed in a

Kentucky cornfield, a find that has at least partly vindicated legends of lost

Civil War gold that have driven American treasure hunters for more than 150

years. GovMint.com, a coin dealer that is now selling the coins, valued a single gold dollar from the collection at roughly $1,000. With GovMint.com

selling several double eagles in the hoard for more than $100,000, the total

value of the treasure could exceed $1 million. - A Globe and Mail news article quoted a CEO saying many are “definitely looking for opportunities” to acquire producing assets, particularly those that are spun-off from big producers undergoing consolidation. This could include some of the struggling Canadian mines that are widely expected by investors to be spun out from Newmont’s (NEM) merger with Newcrest (NCM). Pan American Silver is also asset-rich, post the Yamana transaction.

- The macro driver for future silver demand is being supported by Chinese solar cell production. Bloomberg reported that China’s record-setting solar surge is set to grow even faster than expected this year. Decarbonation and extreme weather are driving the push forward. China has added 74.8 gigawatts of new panels in the first six months of year which is almost as much as they added in all of 2022. In addition, they lifted their forecast for installations this year to 120 to 140 gigawatts, which was previously 90 to 120 gigawatts.

Threats

- The Organization of Economic Co-operation and Development (OECD) confirmed near-global co-operation to advance its Global Minimum Tax (GMT) framework. Phased introduction of tax changes is planned over 2024-25, which most meaningfully includes the introduction of a 15% minimum tax rate across all jurisdictions. Under the current OECD framework, Franco-Nevada and Wheaton Precious Metals would both be classified as multi-national corporations which operate in lower-taxation jurisdictions. FNV operates its streaming model in Barbados, and WPM in the Cayman Islands, both low-taxation jurisdictions. Under the OECD framework, a minimum 15% tax would now be applicable to these jurisdictions.

- Newmont reported a second-quarter production miss and the share price had its biggest single-day fall in a year. Free cash flow came in at $40 million while analysts’ expectations were $227.5 million. Quarterly production was down 17% from a year earlier. Newmont suffered from a strike at the Penasquito mine in Mexico and weaker-than-expected mine performance at the Akem mine in Ghana and the Cerro Negro mine in Argentina. Newmont is still set to close on their Newcrest Mining Ltd. purchase to cement its place as the largest gold producer in the world but has a mountain of issues to sort through for the rest of this year if they expect to achieve full-year guidance. They are only 44% there to bottom end of guidance at 5.7Moz to 6.3Moz.

- According to BMO, Lucara Diamond announced an update to its flagship Karowe mine (Botswana) where the company is undertaking the underground expansion project (UGP). Initial production has been delayed until H1/28 from H2/26 and capex has increased by 25%. While they do not anticipate any near-term funding concerns, they expect that the company will need to restructure its debt facilities.

About the author