Now that the Big Bond Bust has happened, as promised here, everyone wants to know how it happened. I want to know how on earth so many of them didn’t know it was going to happen — especially those who were supposed to be watching for this … including the regulators who were actively causing it?

What follows are some of the reasons:

Their hubris

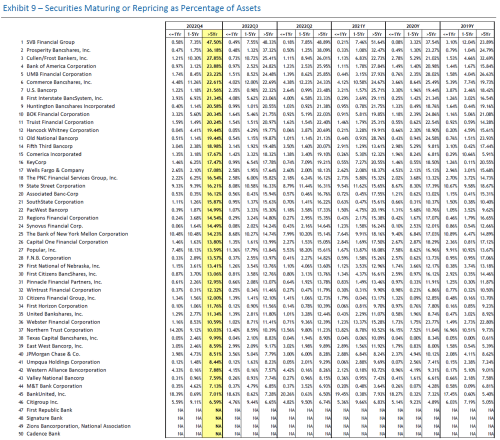

SVB had well over a year to prepare its portfolio to engage with the Fed’s decision to lift the yields on Treasuries, but it took no action to do so. At the time of its collapse 55% of its assets were still invested in bonds, mostly at low-interest rates available over the time when they acquired those bonds that are impossible to sell without a loss when interest rates rise. 47% of SVB’s assets were in long-term bonds (over 5 years to maturity) — the kind that fare worse when you have to trade them during a time when rates have risen!

Tim Gramatovich, chief investment officer at Gateway Capital, told Insider that even though the Fed has been raising interest rates for a year, it was as if a higher-interest-rate landscape came as a surprise for SVB.

“For a $200 billion bank to have no interest rate risk controls is staggering,” he said. “And of course the regulators and rating agencies are allegedly engaged here too. Doing what, we aren’t sure.”

And, yet, they took no risk measures at all. SVB could have started to sell off its longer-term bonds in January of 2022, when the Fed made it clear to the entire world it would begin raising interest rates, and then reinvested the money in short-term bonds of ninety days or less. Why didn’t it?

One explanation would be arrogance. In a word, like so many investors over the past year that took heavy losses in bonds and stocks, they believed in the “Fed Pivot” narrative. (OK, that’s two words, so “arrogance.”) They weren’t reading this blog obviously, so they didn’t get it pounded into their heads that the Fed would “not pivot.” And it did not occur to them they could be wrong about that and, so, should take some conservative measures just to be on the safe side. They had a higher percentage of the wrong stuff on their books than anyone. That’s one big reason SVB was first to fold under the Fed’s new tightening regime.

Surely these people, whose job it is to deal daily in the US bond market and to work daily with the Federal Reserve System, were not ignorant enough to not realize bond prices would crash as the Fed raised rates. So, they must have believed the Fed would chicken out. So overconfident were they, they would actually “fight the Fed” as bankers because they believed they could, through sheer testosterone, keep doing as everyone believed in this era they could do in stocks as well — force a different reality because they were indomitable, indestructible and investment geniuses.

Of course the “Fed has our backs” narrative was part of the moral hazard that led so many to ignorantly believe the Fed would chicken out as soon as stocks fell 20%. Then 25%. Then? It was the now infamous “Fed pivot” narrative that addled their brains.

I know I couldn’t convince anyone who wanted to believe otherwise because they all knew they were right, too. The only ones convinced as they read anything I wrote were those already open to consider the fact that the Fed, like a slug, has laid a long slime trail of economic failures through its hundred-plus-year history. The Fed pivot-heads, who have been the vast majority, ignored the obvious fact that the Fed has a legal mandate to fight inflation, which clearly made this time different from all the times when there was virtually no inflation in the Fed’s environs. Many argued with me on a variety of sites that it was always ridiculous at all times to say, “This time is different.”

Well, it was different.

Team SV was also arrogant in that some employees informed the higher-ups of the considerable (obvious) risk from non-diversification, but the highly successful, much-lauded higher-ups didn’t listen to their lessers. They failed because of their arrogance.

When I’m talking with friends about what to do, they would say to me, ‘well, would you just let these companies fail?’

That’s the wrong question. These companies have already failed.

It’s not for me or anybody else to interfere with that – they have failed.

—Joseph Calandro, Jr, November 7, 2009

Their greed

Longterm bonds get better rates than short-term bonds, as a rule, so SVB’s elite kept piling them in, even as the Fed moved into its tightening phase, when they should have been selling them in a more cautious stance, especially given that they held a higher percentage of their assets in such bonds than anyone else:

They suffered from FOMO, the fear of missing out on better yields, and chose to risk their depositors money (as well as their own) by continuing to chase higher yields while ignoring one of the most obvious risks foreseeable (not simply “imaginable”) for banks — a risk so easy to see it doesn’t take a single drop of Elizabeth Warren’s proposed intensified regulations for the regulators who oversaw SVB under existing laws and for the bank, itself, to identify the risk and for those regulators to force the bank to diversify if it was too greedy to do so on its own for its own good.

That recalls to mind Alan Greenspine’s rubric that banks will regulate themselves because it was in their best interest to do so.

Both parties — the bank and its regulators — are completely without excuse, but they will certainly make plenty of excuses.

Their lies

Janet Yellen said she did not see any possibility of systemic risk in Silicon Valley Bank and then Gramma Yellen and Papa Powell built a Fed “facility” overnight to stem the possibilities of systemic risk they didn’t see any possibility of. The ludicrous nature of her lie is self-evident from her actions.

As pointed out in my recent article, “CONTAGION: Terrorist Fed Wipes out Banks,” former FDIC Chair Sheila Bair also dismissed the problem at SVB by claiming,

This is a $200B bank in a $23T banking industry. I think it’s going to be hard to say that this is systemic in any way.

No.

In a word, NO! It would not be hard to say that at all.

Hence, the emergency creation of a new Fed facility to manage the systemic risk.

Those who created the new Fed “facility,” including the FDIC where Ms. Bair used to be in charge, even called their rescue plan for the recently failed banks “systemic”:

“We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority,” Treasury, Federal Reserve, and FDIC said in a joint statement Sunday evening.…

I don’t suppose you make massive “systemic risk exceptions” for something that is not systemic. They called their bailout plan that because the FDIC has been given special powers by congress for “systemic risk exceptions” — powers that let them bail out rich people and companies who are above the 250,000 FDIC limit if it is a “systemic” emergency. Maybe it is “systemic” when they need it to be, but not when they don’t want to admit it to be because it was under their watch. Otherwise, how dumb do you have to be to get promoted to lead the FDIC? Since Bair probably cannot be that stupid, she lied, and everyone can plainly see (if they are honest at heart) that she was lying.

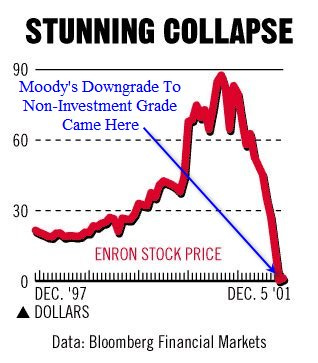

It also proved to be systemic by the number of banks that started sliding badly with six being downgraded by Moody’s with a “watch” warning on the their credit ratings in the past twenty-four hours. Worse still in terms of systemic breadth, Moody’s downgraded the ENTIRE US banking system outlook to “negative.”

It’s so systemic that it crossed the ocean to Europe. Credit Suisse joined the global stock plunge … again … taking down the euro, the pound Sterling, and the Swiss franc and leading global stock markets down another day. I’d say that felt pretty systemic!

The black heart at the center of BlackRock, CEO Larry the Fink, said the collapse of SVB reveals cracks in the US financial system, affirming Moody’s downgrade of the entire US banking industry; while Carl Icahn opined, “Our system is breaking down…. We absolutely have a major problem in our economy today!“

(All as reported in Wednesday mornings Daily Doom headlines. See the special FREE edition.)

I’d say those are some pretty “systemic” statements and some pretty systemic rating changes by Moody’s and a pretty systemic trans-Atlantic impact. So, Bair was lying through her teeth. When bankster buddies have to assure you all is well, you should probably figure it is not, or they wouldn’t have to make such assurances.

The whole system weakens itself because it gets caught in this big lie that says we have to pretend that Deutsche Bank is a bank instead of a criminal enterprise.

— Bill Black, 2018

Fleeing rats

A couple of weeks before SVB’s big bust, its CEO dumped a major load of stocks. Insider trading? You tell me. I’m sure the Department of Justice or the SEC will soon enough be telling all of us.

Oh, and Wednesday morning’s Daily Doom headlines, also revealed other rats of note. Turns out Signature Bank, which was just seized by the Fed/FDIC (they work in tandem) in a way that looks like the Fed is turning them into an anti-cyrpto poster child for the sake of launching its own central-bank digital currency this year (See my article yesterday, “To be Frank, Barney Bank…“), was already under investigation for money laundering.

Yes, that’s Barney’s Bank. Head banking-regulation legislator, Barney Frank — the guy whose signature and name is on the nation’s big banking regulation bill — sits on Signature Bank’s board. Now the regulators are investigating whether or not Barney’s buddies know how to run money washing machines.

Blind bats

We all clearly saw how Papa Powell and Janet Yellen didn’t see it coming as they reported only hours ahead of the major incidences that all was well on the banking front. Yet, anyone inside those banks and inside the Fed should have seen it coming in the case of these particular banks, and anyone could see it coming in general as part of the bond bust — that it was going to eventually hit banks just like the Repocalypse did in 2019 as reserves get drained down (the part we haven’t quite seen yet) and as bonds get devalued (the part we just saw in this major crash event — the kind of predictable event where I’ve explained you can tell how big it was by how big and exceptional the Fed’s response is).

As Silicon Valley Bank’s red flags were flying, the Fed was AWOL

On Jan. 18, William C. Martin, a short-seller and former hedge fund executive, warned his Twitter followers that they were missing something important about Silicon Valley Bank.

SVB’s shares had lost about 65% of their value over the previous 12 months. Investors had been “rightly fixated” on the bank’s exposure to the venture world, which was getting hammered by the rapid run-up in interest rates, he wrote.

“However, dig just a little deeper, and you will find a much bigger set of problems,” he wrote.

William C. Martin saw it coming, but the Fed didn’t. Apparently the regulators don’t believe in digging deeper because January 18 was far enough back that, if this guy could see it from the periphery so clearly, the regulators had plenty of time to dig are without excuse for being so blind.

What Martin had spotted was a plunge in the value of securities in the bank’s portfolio of “held to maturity” securities — Treasury bonds and government-backed mortgage securities that it owned as a backstop to its deposits.

And that is an “uh duh” observation, but no one noticed that bank held so many of those securities as to become a major problem, should it need to actually use its reserves for what reserves are for — making good with depositors should a bunch want their money back all at once — the kind of thing one should also easily have seen as a likelihood in a bank so loaded with the deposits of crypto users and crypto companies who might need to access their cash in the outfall from the Cryptocrash the summer before.

Better not hire the Fed to paint the side of your barn. They can’t see it.

The value of the HTM holdings had declined as interest rates rose. That’s a natural phenomenon: Fixed-income securities always decline in value as rates rise, and rise in value when rates fall.

Exactly. It’s given. That’s why I warned about it here many months ago in my Patron Posts: We’d have a major bond bubble bust that would damage banks once the Fed took interest rates up enough to push bond values down enough.

If the bank were forced to sell off those holdings before maturity, Martin observed, it would be “functionally underwater.”

Indeed. These are observations so simple they don’t even require a stress test.

SVB hadn’t kept this issue a secret. In its financial disclosure for the third quarter that ended Sept. 30, 2022, which was Martin’s source, it reported that its $93.3-billion held-to-maturity portfolio was worth only $77.4 billion in real time

That is true generally at all banks right now. Hence, Moody’s outlook downgrade to “negative” is just catching up with the problem now that it is obvious by making the outlook downgrade it should have made months ago. (It is not as if the problem suddenly changed last week when it surfaced. It is just that blind bats in the regulatory and ratings agencies didn’t see it forming. Now, they do, so it’s CYA time. Time to rate the obvious risk now that everyone knows about it and has seen how quickly the damage can accrue.)

Guys who can’t get a job on Wall Street get a job at Moody’s,” as one Goldman Sachs trader-turned-hedge fund manager put it.

— The Big Short

-or-

The fact that SVB’s problems were hiding in plain sight, right up to the point Friday when the bank was taken over and shut down by California and federal authorities, is certain to be near the top of the agenda as lawmakers, shareholders, customers and regulators examine the disaster.

Thank God Moody’s saw the train coming just after it hit them! Just like in 2008, they’re all over it now. I’ve been warning for two years about the Big Bond Bust that was definitely going to happen and its effect on banks just so they cannot say, “No one could have seen this coming.” Yes, you could see it coming, but the blind bats couldn’t see this train until it was shoving their car down the tracks sideways. Apparently they didn’t want to see it; yet, everyone in finance would rather trust credentialed experts than read logical opinions like I hope people will find here.

As the bank’s primary regulator, it was the Federal Reserve’s responsibility to recognize its growing problems and ensure it continued to meet standards of safety and soundness and financial stability, says Dennis Kelleher, chief executive of Better Markets, a Washington-based watchdog over financial institutions and government regulators.

They’ll pass the buck or use the familiar canard, “No one could see this coming.” They must read in all the wrong places.

The bank’s operations bristled with “screaming red flags,” Kelleher told me. These included a “hyperconcentration” of uninsured depositors from a narrow business sector — chiefly high-tech and biotech startups — as well as a dramatic mismatch between assets (that is, loans and investments) and liabilities (deposits) and the mounting tide of unrealized losses on its books.

“These were visible to anyone who wanted to look,” Kelleher told me. “But apparently, the Fed was AWOL.”

Alarm lights, red flags and sirens! It practically looked like a five-alarm fire, but the Fed didn’t see it coming. None of the experts saw it coming. Crazy Cramer even recommended the stock as a bargain buy a month ago as I showed in a video in my “CONTAGION” article.

Everyone who mattered was AWOL. Even the ratings agencies that are now playing CYA, changing their ratings to what everyone now already knows. Even the Fed head and top Treasury toady told us all was well on the banking front.

And such a familiar story this is:

Eisman and his team were so certain the world had been turned upside down that they just assumed Raymond McDaniel [CEO of Moody’s] must know it, too. “But we’re sitting there,” recalls Vinny, “and he says to us, like he actually means it, ‘I truly believe that our ratings will prove accurate.'” And Steve shoots up in his chair and asks, ‘What did you just say?’–as if the guy had just uttered the most preposterous statement in the history of finance. He repeated it. And Eisman just laughed at him. “With all due respect, sir,” said Vinny deferentially, as they left, “you’re delusional.” This wasn’t Fitch or even S&P. This was Moody’s. The aristocrats of the rating business, 20 percent owned by Warren Buffett. And its CEO was being told he was either a fool or a crook, by Vincent Daniel, from Queens….

Once, [Eisman] got himself invited to a meeting with the CEO of Bank of America, Ken Lewis. “I was sitting there listening to him. I had an epiphany. I said to myself, ‘Oh my God, he’s dumb!’ A lightbulb went off. The guy running one of the biggest banks in the world is dumb!”

Nowhere do they appear dumber, however, than at the top of the top of banking. The Fed HAD to know full well that raising interest rates would imperil the liquidity of banks who hold a great part of their reserves in the Treasuries the Fed was forcing to plunge in value. Therefore, the Fed should have and could have done an easy rundown on how many such bonds every bank held and ordered banks that held a risky balance to rebalance before it even got started with its rate hikes.

Was the Fed dumb? Lazy? Corrupt and wanted the banks to fail? Different people will gravitate toward different answers, but ONE answer is very clear. It is entirely without excuse. If I can figure out in general such a problem has to be coming from repricing bonds and will be the nation’s greatest bond bust and William C. Martin can see it is a problem at SVB in particular, it is hard to conceive that the Fed would be this blind.

So, let’s conclude they are not blind bats; they are …

Blind rats

To that screen title, I say, “Um, OK, sure. Whatever you say.” How are you going to keep fighting the inflation you fueled — and must fight by law — and not bust more banks? “I see no problem here,” Yellen is proclaiming. (Like all the other things she’s wrongly proclaimed in recent years.)

She was running the SF Fed when the following happened, so high up in the Fed that didn’t see this problem coming after other smaller problems had erupted:

As Countrywide and other institutions struggled, senior officials at Lehman Brothers pronounced their company safe and healthy. They said Lehman hadn’t made the kinds of bad choices that had sunk other financial firms. After posting another record year in 2006, pulling in $4 billion, it eclipsed its own record in 2007, reporting nearly $4.2 billion in profits. “We believe we have done a good job in managing our risks,” a top Lehman executive said.

from The Monster: How a Gang of Predatory Lenders and Wall Street Bankers Fleeced America by Michael Hudson

Um, OK, sure. Same song different verse. None of these people, Chief Yellen included, saw Lehman coming, even after Bear Stearns had collapsed, Countrywide and other large institutions were erupting with big zits o their noses, etc.

Now Fannie, Freddie Mac and Ginnie Mae have proved the point. The former two collapsed in bankruptcy in 2007, and they’ve now joined Ginnie Mae as departments of the U.S. government, and are sustained purely on taxpayer guarantees

Chris Maloney, MBS strategist at Bank of Oklahoma Capital Financial Markets

History lesson never learned. (Actually, they collapsed in 2008, but the crisis that led to their collapse started in 2007. But, the point is Bear Stearns had already collapsed in March of 2008. Fannie May and Freddie Mac had already been rescued by the government in July, and STILL no one saw Lehman’s September crash coming! It got away with all of its glowing reports, and no regulator called it out! You’d think they might have been digging deep beneath every hood by then.)

From tech stocks to high gas prices, Goldman Sachs has engineered every major market manipulation since the Great Depression — and they’re about to do it again

– Matt Taibbi, The Great American Bubble Machine, April 2010

See. Never learned.

But in his book, Bailout, Barofsky says that Paulson told him that he believed Morgan Stanley was “just days” from collapse before government intervention, while Bernanke later admitted that Goldman would have been the next to fall.

– Matt Taibbi, Secrets and Lies of the Bailout, January 2013

Ah, but who cares? What are a few bailouts among friends at the club but occasions for cigars and martinis? Somebody gets richer. That’s the whole point of my own little book, “DOWNTIME: Why We Fail to Recover from Rinse and Repeat Recession Cycles.“

After all, wasn’t Barney Frank in the bankster club? I mean, here he was the head legislator behind our major bank regulatory reform, and he was leading Signature Bank as one of its board members since 2015. Couldn’t he see any problems coming from the bond bomb?

No problem with Zombie banks as far as the eye can see:

Convention of Fed-Frozen Banks.

Convention of Fed-Frozen Banks.

Bet you couldn’t see that coming!

Send congress a message.

Send them a copy of this:

Liked it? Take a second to support David Haggith on Patreon!

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!