I want to thank my patrons for hanging in there with me while my writing has been less frequent than you deserve. I’ve been battling with COVID for the past two weeks while also in the middle of a house move, but I hope now to get more on track as I seem to have won the battle with COVID, although not without it pillaging my sense of taste and smell. Here’s a short update on inflation as I attempt to crawl back into action.

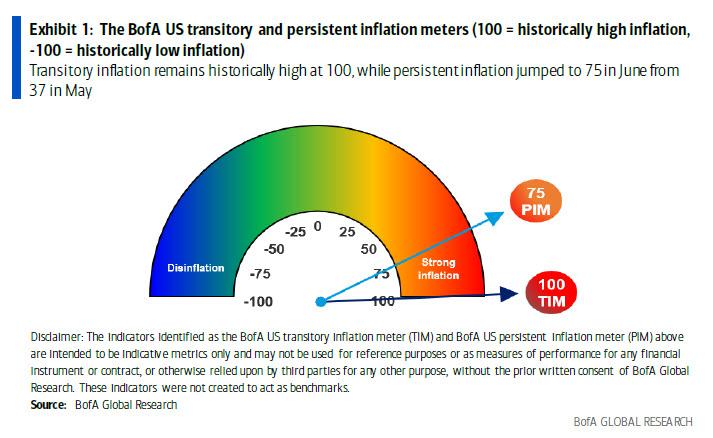

Awhile back, I presented a new graph from Bank of America that was designed to add a persistent inflation meter to their transitory inflation meter. It looked like this back in June:

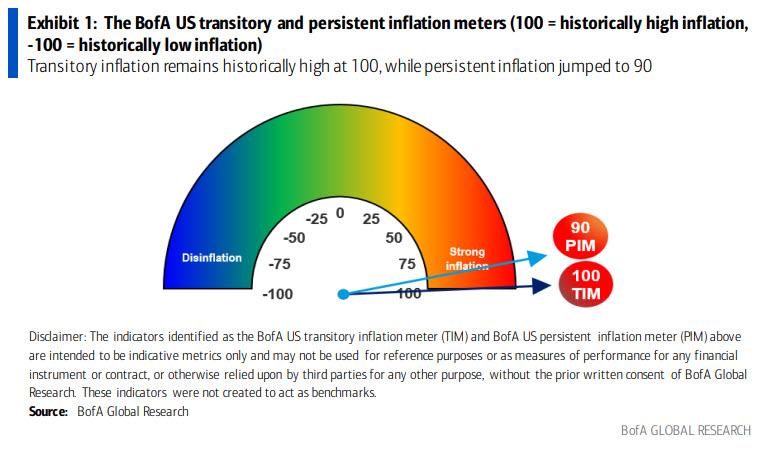

Well, jump to today, and the bank’s meter came out looking like this:

Transitory inflation measures haven’t backed off any, as the Fed was hoping they would. Instead, persistent inflation measures have almost caught up to them. The change in PIM is largely due to the category I said would start playing through and will keep playing through for some time — housing. Owners Equivalent Rent (The BLS funny way of guesstimating the cost of home ownership) rose 0.3% since the previous month while actual rents rose 0.2% month on month. Both are normally slow to play through, but especially slow in today’s rent-moratorium environment of government price control by the nation’s central planners; so, expect rising housing prices to keep playing through for many months.

Used cars, already running scorching hot, added another 0.2% over the prior hot month, while new cars leaped up 1.7% over the prior month. Lodging came in hottest, soaring 6% in one month above June prices.

The BofA’s transitory inflation meter has been pegged at 100 for four months in a row, making even the transitory measures look a little persistent. Someone better tap the gauge to see if it is just stuck.

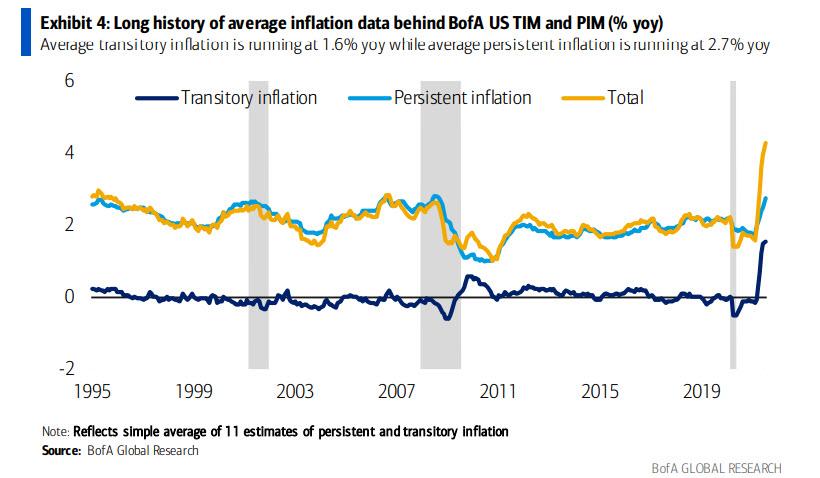

Taking the longer averaged view, you can see both kinds of inflation haven’t been higher than they are now going back to when they were first measured:

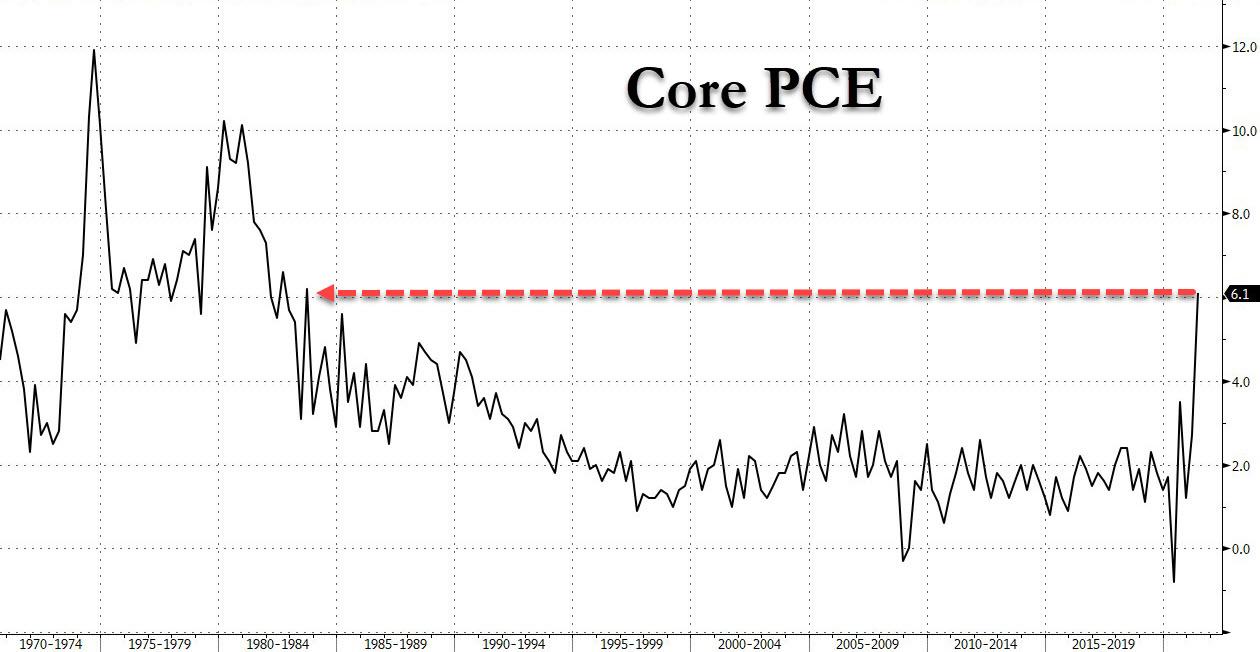

While core inflation, which factors out the things the Fed doesn’t want you to pay too much attention to, came out today looking like this:

Back to the stagflation of the seventies and eighties, and keep in mind it would actually be as high as shown in the seventies and eighties if it were measured the same way it was back then. Those of us who lived through that period remember how hard it was to tame inflation once it got that hot. It took several years and a force-Fed recession to get it back under control.

Time for another Powell punt?

So, what do you think? Should the Fed continue to fuel the fire or perhaps start to think about tapering its record-setting levels of economic stimulus? Should the Fed, in other words, continue to manipulate bond prices lower by continuing to sop up more than half of all US treasuries in order to maintain the illusion of a bond market that sees no inflation coming? Clearly anyone thinking bond prices have anything to say about inflation in today’s world is oblivious to how the Fed has completely destroyed price discovery in bonds by owning the market as its biggest whale with a heavy tale on the scale.

What surprises me are the number of people who know the Fed is soaking up the bond market who continue to think bond yields convey anything. It’s impossible to buy more than half of a market and not be the price-setter. (Which also makes you the yield-setter on bonds.) We all know, the Fed owns the bond market, especially in government bonds. Continually hosing up $80 billion in US treasuries across the maturity spectrum very month, assures yields will stay low in order to keep government debt affordable. Because buying bonds is how the Fed achieves its target interest rates, bond yields will stay where the Fed is setting them until the Fed decides it absolutely must raise interest rates to curb inflation, which recklessly assures one fierce inflation fight because the Fed has already waited too long.

I guess to understand something so mathematically basic, you have to step outside your old-school theories to realize we are not in your father’s world anymore where bond pricing conveyed meaningful market information. Back in the olden days, the Fed was not buying up a total of $120 billion in corporate and government bonds every month in order to attempt to rig the economy for success. The Fed, after all, has purchased $4 trillion in bonds since COVID began. So, whose the whale?

However, it is more like a pod of whales playing in the bond pool right now because all central banks together have hosed up almost a billion in bonds every hour since COVID began. We’re starting to talk real money here.

There may still be room for free price action in the larger corporate bond market, where the Fed is not a major player, but not in treasuries, which is what all the old-school economists still watch as their inflation gauge. The Fed, falling for its own trickery, has believed, based on those gauges, it still has time before it needs to fight inflation.

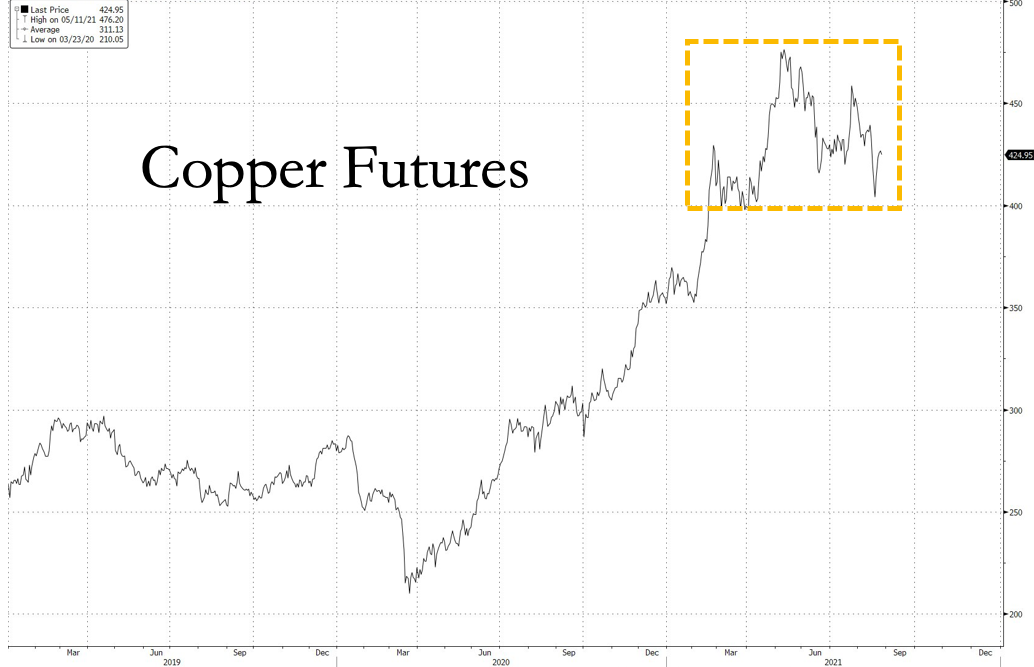

Meanwhile copper prices remain up in the inflationary stratosphere where they have hovered all year, and they are rising again:

In fact, all industrial metals remain persistently inflated:

So, keep the pedal to the metals, Jerome Powell. Their price accelerator clearly needs a fat Fed foot to the floor to maintain that heady price support. All markets are counting on you, Powell. Keep those bond yields floored while you’re at it, too, so the old-word thinkers in your back halls can continue to pretend hotter inflation isn’t coming, even as it burns them alive.

Those who reference bond yields as meaning anything about inflation right now remind me of Powell’s predecessor, Ben Burn-the-banky, telling the world there was no recession in sight back in early 2008 when he was standing in the deepest recession in his lifetime. Even the Fed seems to forget the only reason bonds are not warning of any inflation is that the Fed practically owns all US bonds.

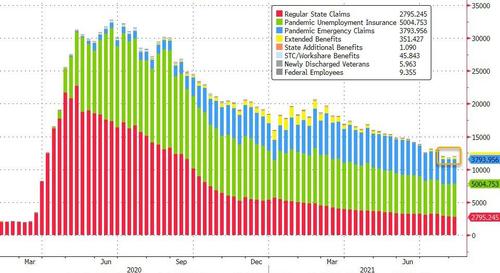

So, power up, Powell, and keep pretending you’re doing the economy some good. Add all the fuel you want, but it’s not going to produce more goods by getting more people back to work since it is helping fund their ability to stay at home:

GDP growth is falling in spite of it all, and prices are pillaging us all. It soon won’t matter that I’ve lost my sense of taste because I won’t be able to afford food anyway.

Liked it? Take a second to support David Haggith on Patreon!

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!