The slavish mainstream financial media was quick to claim that August’s slight rise in inflation was likely temporary and, therefore, insignificant; and the stock market largely shrugged off the turn in inflation by fixating on that desired narrative.

Overall (headline) inflation rose from 3.2% YoY in July to 3.7% in August — a pretty good bump. In June, inflation only rose 3.0%. So, July put in what looked like the first nudge of a possible turn in inflation, and August clearly followed through.

Not so quick say some

The U.S. consumer price index (CPI) for August rose 3.7% year-over-year, according to the Depart of Labor, with the increase largely accounted for by a spike in gasoline prices, while CPI data overall showed a decrease in inflation….

"The move higher in headline inflation is a head-fake since it was mostly driven by a huge 10.5% jump in energy commodity prices," Reuters cited Brian Jacobsen, chief economist at Annex Wealth Management in Wisconsin, as saying on Wednesday.

The basis for the new “transitory” is that most of the rise was in energy. Gasoline prices rose a “HUGE” 10.6% month-on-month and 3.3% year-on-year. The low latter number is because we had a steep fall in gasoline prices at this time last year.

How transitory is inflation this time?

Since the rise in inflation was largely due to the rise in prices of petroleum-based product, this sounds a lot like the old “inflation is transitory” argument the last time the Fed ignored inflation. That was based on the misguided belief that shortages caused by Covid lockdown would settle as quickly as dust.

They did not.

This time it is shortages caused by Saudi Arabia (oh, yeah and Russian sanctions - like those are going away).

They will not.

Has the Fed learned enough from last time's head plant to avoid taking up the new transitory argument being proffered by their mainstream media minions?

“This report interrupts the run of good news [and] makes it more difficult to talk a happy game about inflation,” said Vincent Reinhart, chief economist at Dreyfus and Mellon. “It doesn’t matter for the upcoming FOMC meeting’s results. They’re not going to act. They have not signaled action. Market participants do not expect action. And that’s because they’ve shifted down the pace of tightening.”

“If they act, it will be in November,” Reinhart added.

He might be right about how the Fed will respond. We are sitting on the cusp of a slight upturn in overall inflation so far. It remains to be seen in the Fed’s eyes if it is a blip or a change in the trend. So, I think there is a better than even chance, unless there is more bad inflation news between now and next week’s FOMC meeting, that the Fed will hold to await more data to know if the apparent turn in inflation looks threatening to their plan.

That is not to say that waiting won’t be a mistake. There is a better than even chance of that, too, since all the optimistic slant in the articles on inflation in today’s news headlines below is based on the fact that August’s increases were due to a rise in energy costs that is temporary; but betting those prices will settle back down before the year is out, is a rosy guess at best.

Saudi Arabia has told the world it intends to hold with all of its production cuts through the end the year. Russian oil will certainly remain somewhat scarce on the market as it has because sanctions won’t be going away this year. As the demand for gasoline and diesel drops with the move away from the high-travel summer season, lowering the price of gasoline (perhaps), the rise in heating-oil use and natural gas for heating will offset all of that.

The sunny idea that Petroleum price increases are just a temporary phase feels quaint to me. It’s sort of old-world. Since Grampa Joe issued his “Come on, Man” yell at Saudi Arabia’s Crown Prince Mohammed bin Salman to cajole him into rescuing the US with lowered oil prices along with his salutary fist bump, which was a total fail, Saudi Arabia has actually distanced itself from the US and formed a closer alliance with Russia. At least, it appears Biden done fist-bumped the Saudis into Putin’s fringy ring of frazzled friends. MBS is more likely to seize the opportunity to shave off a little US hegemony in his oily world by holding oil prices higher for longer.

It comes down to whether the damage to the US economy from the Prince’s production cuts will be greater than the benefit that comes to US oil producers who are able to raise their prices for their oil more if the Saudis hold back production. I think higher gasoline prices and other petroleum product prices is a big bad for all things in the economy, regardless of the help they give to some US big-oil corporations.

I am sure MBS’s ears are still ring with these words, spoken by candidate Biden: “We [are] going to, in fact, make them pay the price, and make them, in fact, the pariah that they are.” You can hardly count on your pariahs to help you out with fuel prices. In his visit this month at the G20, Biden has tried hard to sweeten the relationship. We’ll see if that adds up to a lot more sweet crude down the road.

What Biden didn’t mention was the elephant in the room: Saudi Arabia has oil – lots and lots of it – that the United States needs. That’s always been true, but it is even more true with Biden pledging not to import any oil from Russia due to its invasion of Ukraine.

While the US is an oil exporter, Arabian oil has different qualities that US refiners need in their mix; but it is not just about needing their oil, it’s about their ability to control the price of energy in the world. We’ve known that since the 70s.

The great diaspora of high oil prices

Most of all, however, if overall fossil-fuel energy stays as high as it is through the remainder of the year, it will begin migrating into the cost of everything else. As a major component of the production of everything, there is only so much time before energy takes up the cost of everything. There is, first, a slight lag between the rise in crude and the rise in electrical costs for all electricity that is produced with fossil fuels, then a lag between those rising electrical costs of doing business getting passed along in general pricing.

The Fed, of course, ignores energy in determining its interest-rate target, so that is solid reason for thinking this inflation report may not influence the Fed all that much; but it may very well influence the future price of everything.

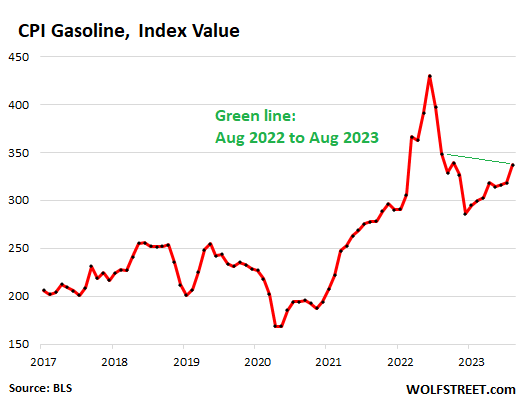

But, getting back to transitory, here’s the trend in gasoline prices, in case you have been wondering, and it does not look particularly transitory so far:

Wolf Street: “The green line in the chart connects August 2023 and August 2022”

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!