Stagflation is an economic event in which the inflation rate is high, economic growth rate slows, and unemployment remains steadily high. (Corporate Finance Institute)

Commodity prices influence the prices of manufactured goods, whether the end users are consumers, car companies, construction firms, or food suppliers. The monetary policy response is higher interest rates.

Take oil. Past increases in oil prices have been a strong indicator for inflation, given that oil is such a major input in the world economy. Try making plastics without petroleum, or fertilizer without natural gas.

Take sulphur. About 50% of the global seaborne sulphur trade, which is the key raw material for producing sulphuric acid, originates in the Middle East Gulf and must be transported through the Strait of Hormuz. This amounts to approximately 20 million tonnes of sulphur per year. Sulphur/sulphuric acid is crucial for fertilizer production (MAP & DAP) and critical metal mining (copper/cobalt/nickel leaching) in Africa and Indonesia.

The multiplier effects of closing the Hormuz Strait are going to be felt across the globe.

Rightly so the war between Iran and the United States/ Israel is worrying investors that it could cause the return of 1970s-style stagflation.

“The risk of a 1970s scenario is rising,” said Kaspar Hense, portfolio manager at RBC BlueBay Asset Management. (Reuters)

The epicentre of stagflation fears is the surge in oil prices, and the biggest question for world markets now is how long will those prices remain elevated.

1970s: dual energy crises

The economy was in a recession from December 1969 to November 1970 and again from November 1973 to March 1975.

The massive cost of the war in Vietnam and the expansion of social programs at home drove inflation higher.

Unemployment rose by 33% between 1968 and 1970 while the consumer price index went up by 11%.

In 1973 the country was hit by an oil crisis. The oil-rich nations of the Middle East were angered when the United States under President Nixon devalued the dollar. When the US supported Israel in the Yom Kippur War, OPEC exacted their revenge by imposing an oil embargo on the United States and Israel’s European allies.

The price of oil quadrupled from roughly $2.90 a barrel to $11.65 a barrel in just a few months. An inflationary wave washed over advanced economies.

A second energy shock occurred in 1979 following the Iranian Revolution. Political upheaval and strikes sharply curtailed Iranian oil production, removing significant global supply. Crude prices more than doubled over the following year. The Iran-Iraq War afterwards compounded the disruption.

These events fed directly into inflation. US consumer price inflation peaked at roughly 11% in 1974 before falling back, then surged again to around 13% in 1979. Inflation only retreated in the 1980s following aggressive monetary tightening. (LGT Wealth Management)

Stagflationary hit

Capital Economics says a useful rule of thumb is that a 5% rise in oil prices adds about 0.1% to developed-market inflation.

High oil prices also dampen economic growth, with the IMF estimating that for every 10% rise in oil prices, global economic output decreases by 0.1 to 0.2%.

Oil price increases not only contributed to the twin energy crises of the 1970s, but the US recessions in 1990 and 2008. Russia’s invasion of Ukraine in February 2022 also triggered a major energy shock, particularly in Europe.

Source: Trading Economics

Source: Trading Economics

While one analyst in the Reuters story said the stagflationary hit from the war will hurt the US less than Europe or Asia, due to America being largely self-sufficient in oil (and US markets have held up better than Asia or Europe), the United States is by no means immune to stagflation and was looking vulnerable even before the war started.

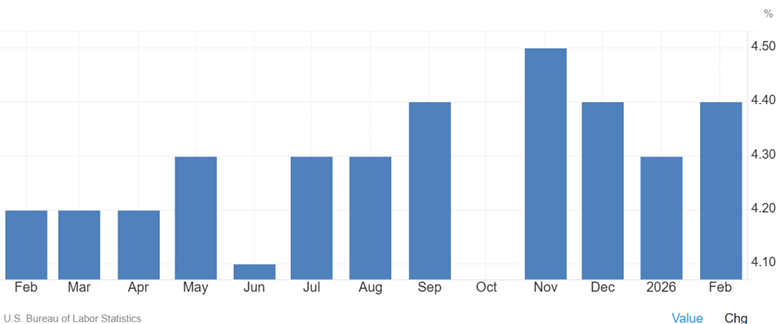

The economy lost 92,000 jobs in February, while the unemployment rate ticked up to 4.4%.

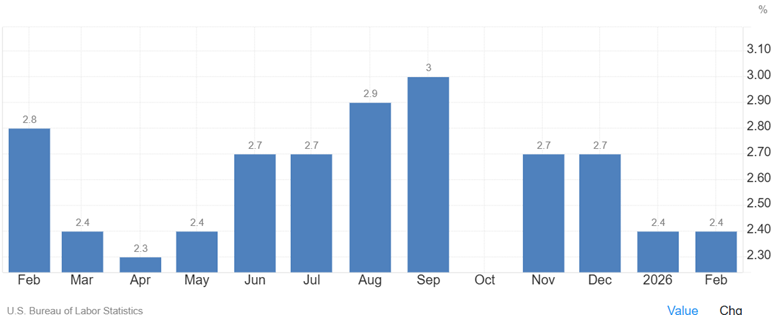

Data released this week showed that CPI inflation in February was sticky, rising 0.3% over January and 2.4% year over year, matching expectations. Of course, Wednesday’s inflation print didn’t capture the effects of the oil price surge this month.

US Treasury yields are rising with oil prices, as traders assess the war’s impact on inflation. On Friday morning the 10-year Treasury had climbed 5 basis points to 4.25% while the 30-year added more than 2 bp to 4.879%.

Kitco News reported on March 11 that the Strait of Hormuz closure is threatening the US bond market. Why are yields rising? According to Luke Groman, founder and president of Forest for the Trees, The core issue stems from the heavy reliance on the U.S. dollar by foreign nations that are concurrently dependent on imported energy.

When oil prices spike, these nations sell dollar assets, starting with Treasuries because they’re the most liquid, so they can afford to buy more expensive oil. This puts downward pressure on bond prices and upward pressure on bond yields.

“Iran doesn’t have to beat the U.S. military, if it even could, which I doubt,” Groman told Kitco. “All it has to beat is the bond market.”

US manufacturing employment continues to shrink, with the sector losing another 12,000 jobs in February, to 12.57 million, the lowest since January 2022.

According to the Kobeissi Letter, manufacturing employment has contracted in 23 of the last 25 months, the longest losing streak since the financial crisis.

The Letter expects the Iran war to make the manufacturing recession even worse, because higher energy costs could force factories to cut even more jobs.

Investors don’t like stagflation because it affects stocks and bonds.

A key question in terms of impacts on the world economy is how long oil prices stay above $100. The other related question, adds a piece in Motley Fool, is how long the war lasts.

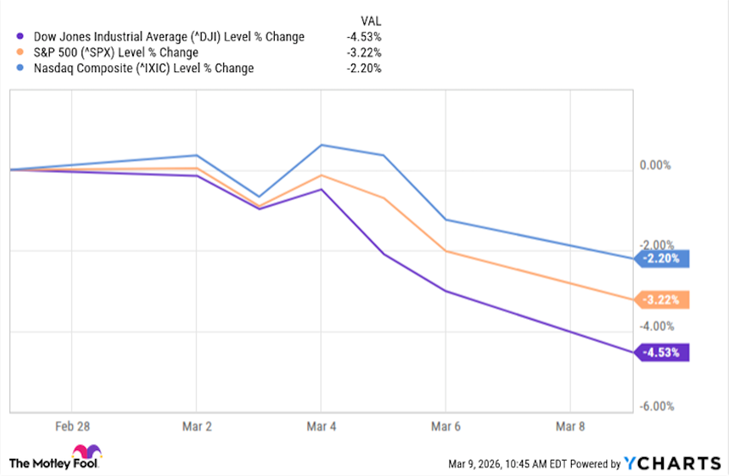

While US stock markets have sold off, the damage has been somewhat contained, as the chart below shows.

A prolonged conflict could have big consequences for the broader market.

The price of oil had fallen close to $55 per barrel earlier this year, and the outlook for oil in general was not positive heading into the year.

However, everything changed once rumors began to circulate about the U.S. and Israel conducting airstrikes on Iran.

Once those officially happened, the Iranian government subsequently announced the closure of the Strait of Hormuz to ships from the U.S., Israel, and Western allies, and oil prices skyrocketed…

There have also been concerns that energy assets in the Middle East could be damaged, potentially impacting production. Higher oil prices essentially serve as a tax on consumers and can also raise the cost of doing business for corporations.

Motley Fool cites Ed Yardeni, the prominent market strategist, who says a slowing economy with higher oil prices that could meaningfully push up inflation is a bad combination.

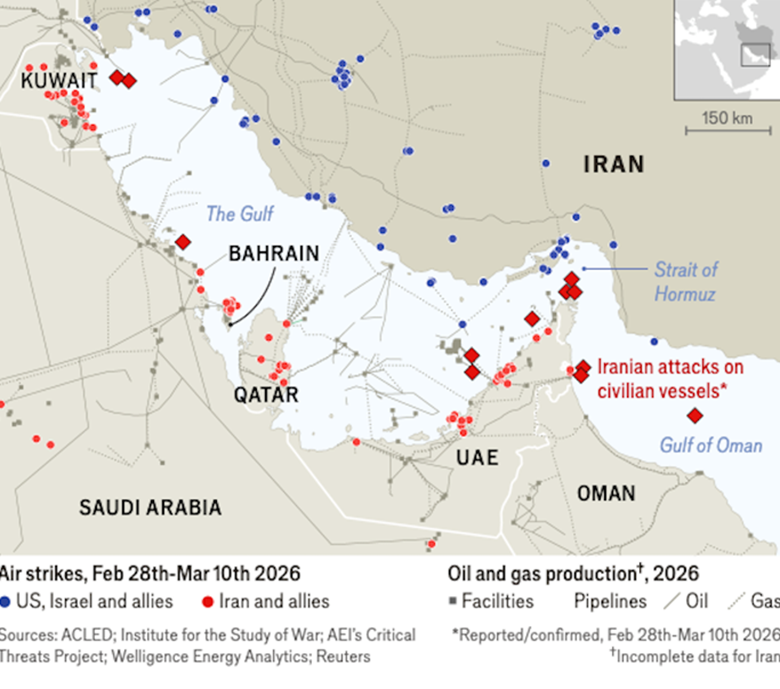

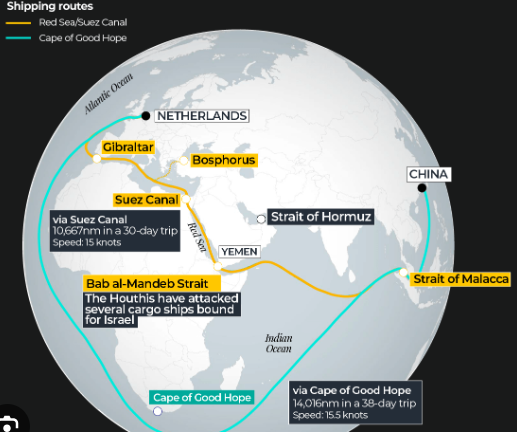

The Strait of Hormuz

In contemplating a war with Iran, the US had to have considered a partial or complete shutdown of the Strait of Hormuz, which Iran controls.

Twenty million barrels of oil flows by cargo ship through the strait daily, or about a fifth of global oil consumption. Significant volumes of LNG, along with distillates such as gasoline, diesel and jet fuel, fertilizer, and sulfuric acid used in metal refining, also transit the narrow waterway linking the Persian Gulf to the Arabian Sea. (more on this below)

Infrastructure developments provide alternatives, such as the pipeline operated by the UAE that allows some crude exports to bypass the strait; while Saudi Arabia maintains an east-west pipeline across the kingdom that connects oil fields to the Red Sea.

That still leaves around 15 million barrels of oil a day of oil and products trapped in the Persian Gulf.

As far as how long the Strait of Hormuz could be closed, I think it will be longer than expected and don’t think it will re-open immediately. The Iranians, being a major oil producer, just might say, “We like $200 oil for awhile.” They certainly will need the money to rebuild all the infrastructure the US and Israeli air forces have destroyed.

They could put a large transport fee on ships needing to pass through the strait, and/or stop oil sales to any country that helped the US, instead selling all their oil to China/ India.

Meanwhile, the Iranian regime remains intact — the dead Ayatollah replaced by his son, another hard-liner likely to resist Western-style reforms; and its nuclear program still functioning despite three sites being bombed last year. Satellite imagery showed that Iran sealed off its nuclear enrichment facility at Fordow in the days leading up to the US strikes, which would have shielded it against a potential ground raid.

Sky News reports Iran is thought to have moved any enriched uranium before the strikes occurred.

Feed your head — Richard Mills

The Economist asks: Can America clear the Strait of Hormuz of Iran’s drones and mines?

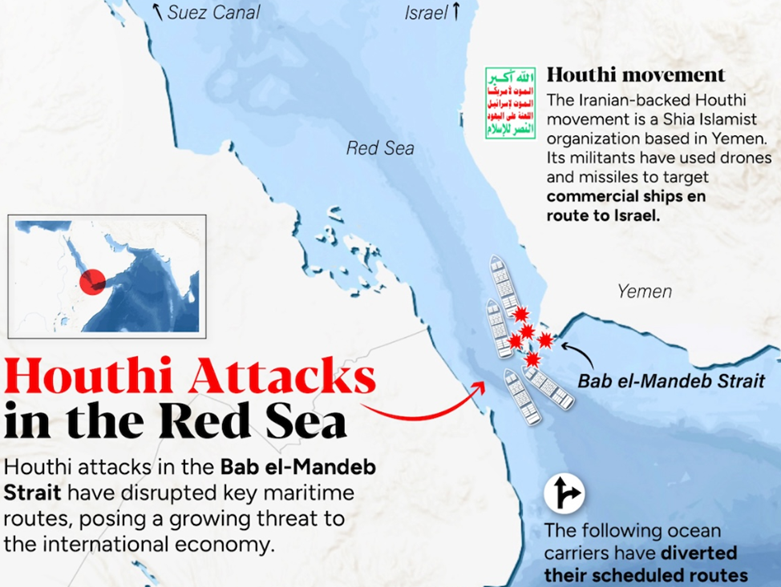

During the Gaza war the Houthis, a militia in Yemen allied to Iran, stopped much of the sea traffic in the Red Sea and Suez Canal by threatening ships in the Bab al-Mandab strait with fairly cheap drones and missiles. America struggled last year to destroy their forces and reopen the strait, losing an aircraft that fell off a carrier as it dodged Houthi attacks. It ended with a partial ceasefire. Traffic has yet to return to pre-crisis levels, and the Houthis have vowed to resume attacks in solidarity with Iran.

Maritime chokepoints favour the defender. In the past American commanders have said they would be able to reopen the strait within days or weeks, were Iran to attempt to close it. But experts point to the cautionary tale of Britain’s failed campaign in the first world war to force open the Dardanelles, part of the passage between the Black Sea and the Mediterranean. Ottoman forces had laid down complex defences consisting of mines, fortresses and mobile artillery. The allies lost several ships trying to fight their way through from the sea. The Gallipoli landings to seize the passage by land turned into an even bloodier debacle.

The Houthis are a big unknown at this point.

The US navy made a big mistake in decommissioning its mine sweepers and moving them out of the area before the conflict began. The Independent reports On Monday, a massive cargo ship, M/V Seaway Hawk, was spotted on camera arriving in Philadelphia carrying a quartet of Avenger-class Mine Countermeasure Ships that were based at U.S. Fifth Fleet headquarters in Bahrain as the Navy’s front-line deterrent against mining operations in the Middle East until this past fall, when the last of those ships, U.S.S. Devastator, was decommissioned…

Photographs released by the Pentagon on Jan. 21 show the Seaway Hawk carrying the four decommissioned minesweepers while being escorted by the Littoral Combat Ship U.S.S. Canberra — one of a troubled class of vessel which the Navy is pressing into service as a replacement for the minesweepers.

It arrived in Philadelphia on Tuesday the day Iran reportedly began laying mines.

IEA stockpile release

One way to contain prices is for oil importers to release strategic stocks.

On March 11, the International Energy Agency (IEA) agreed to a record release of 400 million barrels of oil from its members’ strategic reserves to counter a massive supply shock caused by Iran effectively blocking traffic through the Strait of Hormuz.

According to an AI Overview, this is the largest coordinated release in the IEA’s history, exceeding the 182 million barrels released in 2022 following Russia’s invasion of Ukraine.

The 32 member countries have up to 90 days to release their stocks into the market.

While a start in addressing the oil supply shock, the IEA stockpile release is in fact a pittance. 400 million barrels a day equates to just 20 days of oil that would normally transit the Strait of Hormuz.

Barron’s notes that, even if the release adds roughly 4 million barrels a day, and Saudi and UAE pipelines reroute around 7 million bpd, that will still leave around 4-5 million bpd of supply — roughly one third of the region’s normal crude exports — disrupted.

What else is affected?

As mentioned, it’s not only oil and LNG that are affected by the strait’s closure. Key products such as sulfur, distillates, fertilizer and sulfuric acid aren’t getting through, which could cause major damage to the industries which depend on them.

Sulfur

Reuters reports that nickel makers in Indonesia rely on the Middle East for 75% of their sulfur and therefore may have to cut production.

Sulfur is used to make sulfuric acid, which is essential for leaching metals from ore during nickel refining and copper processing.

According to the US Geological Survey, the Middle East accounts for around a quarter of global sulfur production. High-pressure acid leaching (HPAL) nickel plants only average one to two months’ worth of sulfur consumption. Without alternatives, plants could be forced to start cutting production next month.

Supply fears have raised sulfur prices almost 25% higher than the $500/ton they were at before the Iran war began.

Reuters notes A scramble for supplies would pit nickel refiners in Indonesia against copper miners in Africa, and both against fertiliser makers around the globe, which are also seeking replacements for Middle Eastern sulphur.

Source: Trading Economics

Source: Trading Economics

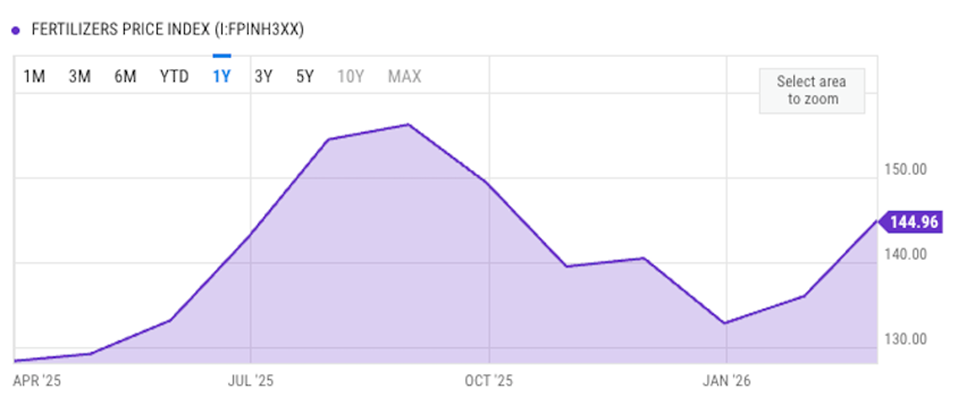

Fertilizer

Indeed, sulfur is not only used in mining but in making fertilizer. When Russia invaded Ukraine in 2022, fertilizer prices went ballistic.

BBC News reports that because the Strait of Hormuz is a key route for fertilizer and for natural gas used to produce it, the halting of traffic has prompted fears of shortages and increased prices.

Also, Qatar Energy, one of the world’s biggest exporters of gas and a producer of urea for use in fertilizer, has stopped production following attacks on its facilities.

With roughly one-third of the global fertilizer trade transiting the strait, including large volumes of nitrogen exports, the price of fertilizer has jumped, and there are fears that this could raise food inflation.

As of March 11, New Orleans fertilizer hub urea prices have already risen from $475/tonne to $680/t.

Source: YCharts

Source: YCharts

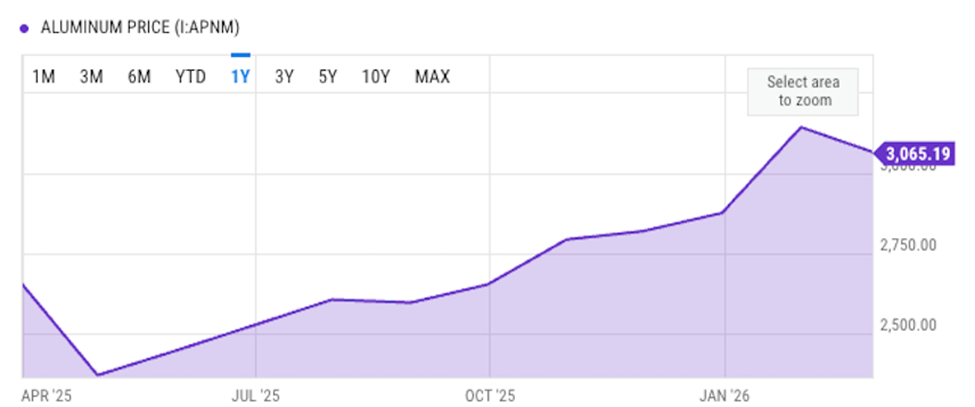

Aluminum

Readers may be surprised to learn that the Gulf region is a major supplier of aluminum, and that disruptions could tighten supply chains for advanced manufacturing.

CNBC reports that in 2025, the Middle East accounted for about 21% of unwrought aluminum imports and 13% of wrought aluminum imports, with those percentages rising.

Source: YCharts

Source: YCharts

Gasoline and diesel

The oil price spike has, unsurprisingly, found its way to the gas pump.

Motorists in Europe, the UK and North America are all facing sticker shock after months of relatively affordable fuel.

As of this writing, March 12, US retail gasoline is USD$3.63 per gallon, while in Great Britain, the cost of a liter of unleaded petrol is 139.65 pence, whereas for diesel it’s 157.20p. according to RAC.

Source: YCharts

Source: YCharts

BBC notes that, while UK petrol prices have doubled since the beginning of the conflict, they are less than the increase resulting from Russia attacking Ukraine in February 2022.

In the week before the invasion, unleaded petrol averaged 147.77 pence per liter in the UK. By early July 2022, prices had surged by more than 43p/l.

In the United States, gas and diesel prices climbed even more sharply, peaking at over $5 per gallon in June 2022.

Jet fuel

Jet fuel is another petroleum product that has risen in price. Since the fighting began, the European benchmark price has almost doubled, from $830 per tonne to more than $1,500/t. Europe gets about half of its jet fuel from the Gulf.

As a key input in airlines’ operating costs, accounting for 20-40%, the higher price of jet fuel is likely to increase fares.

But the BBC notes the impact may not be equal across the board, with many airlines such as British Airways and EasyJet using contracts to lock in the price of jet fuel for months or even years. By contrast, several large US carriers don’t do this and could therefore be exposed to short-term price increases.

What the war means for interest rates

The war’s knock-on inflationary effects could dash the market’s expectation of at least two interest rate cuts this year in the US.

In fact, in a dramatic reversal of fortune, they could even rise.

Federal Reserve officials say the war in Iran could impact the near-term inflation outlook and add to economic uncertainty, potentially pushing back the timeline for any further interest rate cuts under consideration until later this year.

The key questions for us at AOTH is how long the Hormuz Strait remains closed and if the Houthis, Iran’s proxies in Yemen, decide to try and close the Bab el-Mandeb strait.

Source Visual Capitalist

Source Visual Capitalist

Source AlJAZEERA

Source AlJAZEERA

Trump initially said the conflict could last four to five weeks and on Wednesday he said it may end “soon” because there is “practically nothing left” for the United States to bomb (Aljazeera)

Fed governor Stephen Miran said he is less concerned about the spike in oil and gas prices because they tend to be temporary events.

“Typically, the Federal Reserve doesn’t respond to higher oil prices like that,” Miran told CNBC. “It [boosts] headline inflation, but it tends to be a one-off shock. When you think about core inflation [which does not include energy prices], it tends to be more predictive of where inflation is going over the medium term than headline inflation.”

Similarly, Governor Chris Waller said he doesn’t expect high gas prices to lead to a sustained increase in inflation.

Yahoo Finance reports Fed officials are expected to hold interest rates steady when they meet later this month, as they did at their gathering in January.

Investors were pricing in 95% odds as of [March 6] that the Fed will hold rates steady this month.

Over in Europe, Reuters said markets see at least one European Central Bank hike this year, compared to a 40% chance before the war.

Markets now see a growing chance of a rate hike from the Bank of England this year, after previously pricing in at least two rate cuts.

What it means for the dollar

One of the few brights spots from the war, for the US, is a rise in the value of the dollar. Bloomberg’s dollar gauge is up more than 1% since the launch of US and Israeli strikes on Iran on Feb 28.

The US Dollar Index (DXY) on Friday extended gains for a fourth straight session and reached a level that has only been breached (barely) twice since May 2024.

Source: Trading Economics

Source: Trading Economics

Traders and strategists told Bloomberg that the dollar’s rise has been catalyzed by the US’s position as the world’s top oil producer, and by the dollar’s role as the currency for global crude trade.

However, it isn’t enough to reverse the buck’s downward trend since Trump took office in January 2025. Despite recent gains, Bloomberg’s dollar measure is still down 6% over the last year, as of March 10.

At least one market observer — the venerable Ron Paul, no less — recently wrote a column titled ‘Will the Dollar be a Casualty of the Iran War?’

Paul focuses not on high oil prices, but the ballooning US debt, which he believes will hasten a crash in the value of the greenback. Countries that have been buying US debt/ Treasuries will reduce their purchases because they are worried about the US government’s unsustainable spending and its “hyperinterventionist” foreign policy:

According to the Center for Strategic and International Studies, the US government is spending about 891.4 million dollars a day on the Iran War. These costs are likely to increase as the war drags on and the US increases its military presence, possibly even putting boots on the ground in Iran.

According to numerous media reports, the Trump administration is preparing a 50 billion dollars “supplemental” funding request for the Iran War. This request will soon be sent to Congress. This funding would be added on top of the defense budget…

The costs of the Iran War will further increase the already over 38 trillion dollars and rising national debt. The rate of increases will be greater as long as the government is spending almost a billion dollars a day, or more, on a regime change war in Iran.

The costs of this war will put added pressure on the Federal Reserve to keep interest rates low and increase its purchase of Treasury bonds in order to monetize the federal debt. The pressure on the Fed will also increase as other countries reduce their purchase of US debt. These reductions will be motivated by concerns over the economic instability caused by the US government’s out of control spending and by resentment over the US government’s hyperinterventionist foreign policy. These factors could also accelerate the increasing rejection of the dollar’s world reserve currency status. A loss of the reserve currency status will cause a dollar crisis, leading to an economic crash worse than the Great Depression.

Conclusion

What happens next? US President Donald Trump’s options to reduce oil prices are limited.

To alleviate the 15 million barrels-of-oil-per-day trapped in the Persian Gulf, governments can increase traffic in Hormuz, release strategic stocks, or boost crude exports from other places. (The Economist)

The problem with the first option is that it doesn’t change the insurance calculus — shipping companies will keep paying big bucks to their insurers for shouldering the risk of the vessels they are underwriting of being attacked. Although the US’s International Development Finance Corporation (DFC) earmarked $20 billion to insure vessels trying to exit the Gulf, JP Morgan figures it would require $352B to cover all the trapped oil tankers — more than the DFC’s maximum permitted liability under all its programs combined.

On the other hand, shipowners can absorb the higher costs, as freight rates from the Gulf to Asia have more than doubled.

Military escorts are a possibility, but one convoy a week would do little to return to prewar traffic of 50 oil tankers a day, states the Economist:

At that pace it would take two and a half years to get all 320 or so vessels currently stranded in the Gulf out of there. Even resuming three-quarters of Hormuz sailings would still prevent nearly 4m b/d of oil from getting to global markets.

A larger escort armada would get more ships moving, but US warships in the Gulf are already involved in “Operation Epic Fury” and reinforcements are weeks away.

A better way to contain oil prices is for IEA-member nations to release strategic stocks. They have already said they will release 400 million barrels into the market, but that only covers 20 days worth of oil that would normally transit Hormuz.

The Economist notes that the IEA’s emergency stocks total 1.2 billion barrels and that governments could requisition another 600 mb. But that would only cover 140 days of their total net imports. It also may not be possible to come up with such a large release. The US’s, for example, must be kept to a minimum of 150-160 mb to preserve the pressure inside the underground caverns it is kept in. Other countries aren’t allowed to completely drain their strategic reserves.

Morgan Stanley calculates that if all countries were to liquidate their strategic stocks to the maximum achievable rate, they could at most add 3 million barrels a day to global supply.

Alternative supplies are a third possibility. The fastest option is also the most unsavory — relaxing sanctions on Russia, which is among the world’s top three oil producers. Trump has already issued a 30-day sanctions waiver for India to buy Russia crude, and he has hinted that it could be broadened to include new Russian crude and other buyers.

The problem with this plan is that due to sanctions, the Russian oil industry will be challenged to raise output.

How about US shale oil? The problem here is that shale firms are more focused these days on returning cash to shareholders than on drilling. American production is at record highs and even if they could increase it, they could only add up to 300,000 barrels a day over six months to a year, according to energy consultancy Rystad.

Putting it all together, the best case scenario of another strategic reserve release, and more Russian crude and US shale oil would yield just over 4 million barrels per day, the Economist calculates. Less than a third of the Hormuz shortfall and it would take weeks to make happen.

In the meantime, Iraq and Kuwait are shutting wells and Saudi Arabia is reportedly trimming production, further tightening the oil market. And production will not come back to normal levels. Older oil fields are notoriously difficult to restart and seldom come back on line and produce at the same level.

The way things are going, we could soon see $150 oil — a nightmare for oil-importing nations and a massive drag on economic growth, as well as feeding global inflation.

The United States, while managing to curb the post-covid runaway price increases, has for months been experiencing sticky inflation. The latest inflation print shows CPI running at 2.4% year on year, still more than the Fed’s 2% target. Expect next month’s data to be much higher when the increase in oil prices is factored in.

The Strait of Hormuz closure isn’t only affecting oil prices. Cargoes of LNG, gasoline, diesel, jet fuel and other oil products are stranded, pushing up the prices of these commodities. We also talked about aluminum, sulfur and fertilizer. Eventually these industrial inputs will trickle down into higher manufacturing costs and likely higher food prices, which consumers are already struggling with.

US unemployment is at 4.4% — not terrible — but the real problem is manufacturing. Employment there has contracted in 23 of the last 25 months, the longest losing streak since the financial crisis.

The Iran war may make the manufacturing recession worse, because higher energy costs could force factories to cut even more jobs.

The end result is the dreaded stagflation, which, as defined at the top, is the combination of high inflation, high unemployment and low economic growth.

Unless the war with Iran ends soon, stagflation will soon be stalking global economies. Stagflation is bad for stocks, bonds, consumers and manufacturers. The only thing that it’s good for, history has shown, is gold.

In the 1970s gold’s price experienced a massive and historic bull market, rising from a fixed $35/oz to a peak near $850/oz by January 1980, an increase of over 2,300%.

As we’ve previously written, gold does well in stagflationary periods and outperforms equities during recessions.

In six of the last eight recessions, gold outperformed the S&P 500 by 37% on average.

Gold is currently at $5,094. Predictions are useless, but it could arguably move much higher as the war continues and inflation bites. Gold is considered both an inflation hedge and a safe haven.

Precious metals offer protection against looming economic challenges — Richard Mills

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.