News of new jobs is supposed to be great, right? So, what kind of weird world do we live in when it is considered horrible? Welcome to Fedworld where most market decisions are nothing but bets on what the Fed will be doing next with its free money for millionaires.

Today we saw that in action as good job news kicked some reality into the FedMed-addled heads of investors about Fed tightening, which they have been denying all year. Suddenly, they realized they had a lot of catching down to do to align with a tightening target that readers here know the Fed has been heading to all along ... even before the Fed knew it. Obviously, the Fed didn’t know it, given that the Fed has revised its tightening targets all along the way as these article have said would happen.

While workers report in today’s survey that they don’t feel the job market is strong, the number of new jobs was high enough that it caused Treasuries to take a rocket ride up past 4.8% yields on the 10-YR bond. The 30-YR joined the move, also rising to its highest point in 16 years. All because those jobs means the Fed will going “higher for longer” just like it has been speaking into the disbelieving heads of bond investors and stock investors for a long time. In fact, Atlanta Fed president Raphael Bostic emphasized today that the Fed should hold rates higher for longer “for a long time.”

Rising yields combined with the jobs report caused the stock market to finally have a heart attack and plunge 500 points intraday on the Dow. It closed the day down 430 points, which wiped away all of the gains the Dow had seen this year!

MarketWatch reports that banks are now bracing for a recession. Two weeks ago, it seemed like everyone in the mainstream media, as I reported, believed there would be no recession and that a soft landing was practically certain. I stuck to my guns. Just like my endless refrain of “no pivot” to all the pivot heads last year, I’ve stayed with inflation is likely going to rise again, forcing the Fed to tighten harder into a deep recession, which means a lot more serious trouble for stocks.

Trying to make a soft landing when yield rates are this inverted for something like 16 months now looks like this:

Fed Pilot Cpt. Powell scores a soft inverted landing.

As a result of today’s thrill ride in Treasury yields, mortgage interest rates also shot up toward 8%. In keeping with this week’s housing theme, another video posted below explains how new-home housing, which escaped the same Fed-caused shortage problem that has swept up existing homes to new reaches for reasons described yesterday and in my last “Deeper Dive,” is now looking ready to collapse.

The producer of the video lays out how overstressed to the breaking point home builders are likely becoming in their efforts to hold down new-home prices. Prices have already fallen, unlike the soaring prices of existing homes that have hit a new all-time high, which is also an inversion of reality because new homes usually sell for more than existing homes, but the producer in the video says a huge avalanche in new home prices is likely to ensue quickly, making this inversion even more grossly distorted unless there rush downward catches existing homes in it wake. This was covered in yesterday’s Wealthion video.

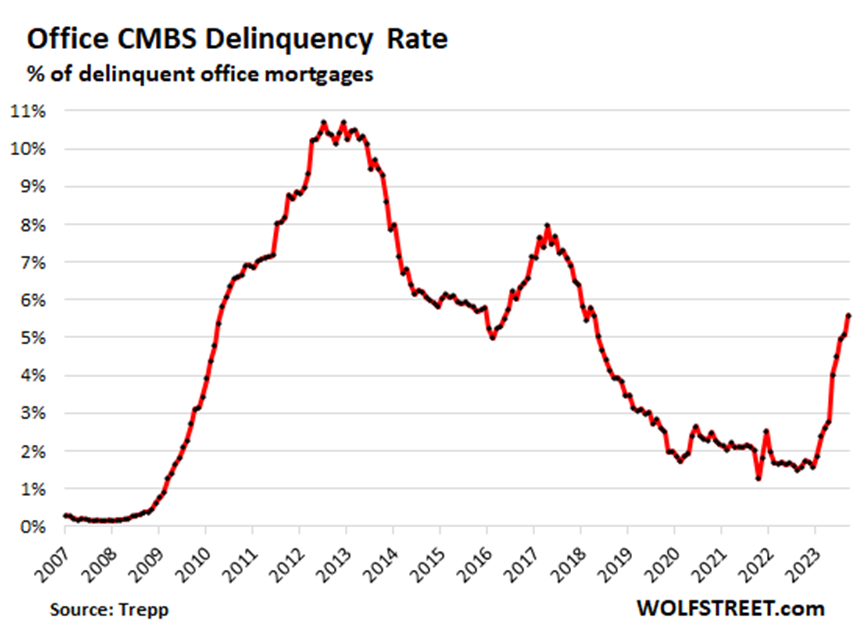

Commercial real estate is already in worse shape than housing, as has said JPMorgan chief Jamie Dimon (I always pronounce it “demon” in keeping with the company he keeps). Likewise, Wolf Richter now reports that delinquencies in commercial mortgage-backed securities (Remember those MBS?) have suddenly spiked to “nightmare levels,” and Richter is not one who speaks in hyperbole.

That rocket-ride looks like this:

While that doesn’t look as bad as CMBS delinquencies reached at their peak right after the Great Recession or as they were during the Fed’s last hiking cycle from 2016-2018, which ended in the Repocrisis, the ascent in CMBS delinquencies is steeper and as high as it was from 2009 to 2010 when the economy was collapsing into the Great Recession. So, we’re in the starting years. Whoohoo! Get ready for the ride that follows!

Says Richter, “This is a ferocious deterioration.”

It is; and, according to the Fed’s Bostic, the Fed still has a loooong way to go with this tightening cycle because THIS TIME it has inflation to fight, which it did not have to worry about at all last time when it was merely tightening to deflate the housing bubble. The Fed has a vastly tougher task today, as it is popping every bubble out there:

The stock bubble is now imploding again, after an 8-month reprieve in one of the market’s largest bear-market rallies (but what can you expect in the middle of what will likely be the market’s biggest bear market since the Great Depression?).

The bond bubble has been popping for a long time, reluctant to go where reality dictates it should. However, it seems to have “gotten the memo” at last, as Richter said in yesterday’s Daily Doom, because it certainly has picked up speed.

And now the housing bubble is joining the cascade — at least in new home prices. Existing home prices, however, have been swept up in something much worse — a fire tornado created by the Fed where the Fed’s tightening is causing shortages in supply that are actually driving prices upward, rather than taking them down. That dangerous dynamic may bust at some point, but it means the housing bust will be more chaotic than if that dynamic were not happening. It is hard to say for sure because we haven’t seen something like this before. If the tension doesn’t break between sellers and buyers, the most bizarre housing freeze in a long time — if not ever — will soon look like a nightmare in Wonderland.

Another article in the news today lays out why the present rout in government bonds is perilous while another video quotes JPM as warning of “shock wave” to hit soon in the implosion of the housing nova. All of which is why I’ve chosen this week to put the housing conundrum in the center of your radar screen in yesterday’s Daily Doom, today’s edition and in my last “Deeper Dive” for supporters of this work. The time is here for the third bubble implosion to develop alongside the bond implosion and for stocks to resume implosion with them.

Still another article shows via a graph how US money supply has now fallen by the largest percentage of total money in circulation since the Great Depression, and that is quite extraordinary when you consider how vastly greater the mountain of money is that the Fed has created since it was given new powers after the Great Depression, particularly in the Nixon era. So, this should go well.

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!