According to Bidenomics, it’s new construction everywhere and robust consumers.

Yet, as the tech sector in US stocks saw shares slammed down around 4%, NVIDIA, which so many stock promoters said could not see a collapse like a dot-com bust, fell almost 10% in just this one day (down 9.5%). No biggie! The economy is great!

Last week, we got a revised GDP report from Uncle Joe’s Fantasy Land that said GDP rose 3% in the second quarter due to surging consumer expenditures, while two of the nation’s large retailers reported hugely declining sales or bankruptcy due to failing consumer expenditures. That adds up.

Surely, Dollar General didn’t collapse entirely in the first two months of the third quarter, so how did it begin the bankruptcy process, giving a reason for declining consumer expenditures if the consumer is so robust and exuberant as to be the big driver of GDP growth in the second quarter? Maybe they are just so rich they don’t need dollar stores anymore and are buying cars and refrigerators and new homes! Zero Hedge also pointed out in more than one article this peculiarity.

It’s like seeing many flocks of geese appearing to fly south on a scorching summer day. It doesn’t make sense. Something is wrong.

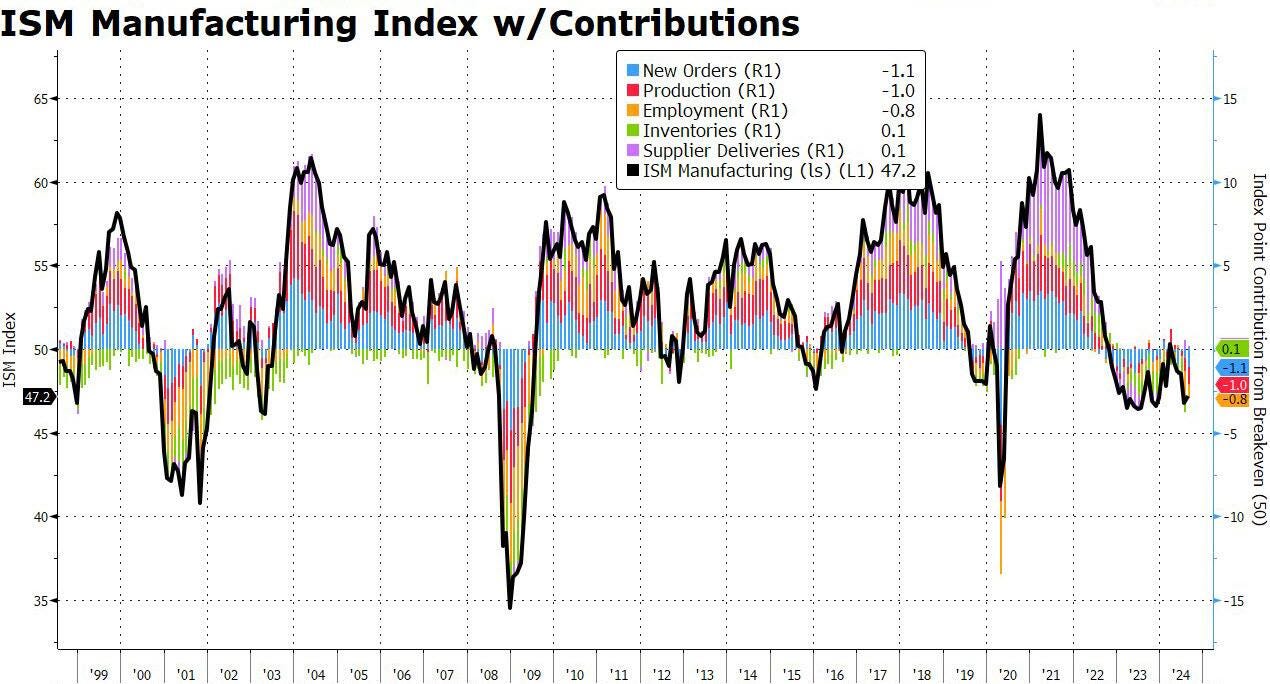

Just as people were believing in this big economic rebound reported in GDP and expecting to see it show up in upcoming reports, manufacturing and construction spending crushed those unrealistic hopes, missing expectations. Unlike GDP, which was revised upward, the Manufacturing ISM was revised downward. Apparently no one is interested in manufacturing in order to fill that large swell in consumer demand caught by GDP. The PMI (Purchase Managers’ Index) also came in, again, in solid recession territory. So odd for a time of GDP cruising along at a smooth altitude of 3% growth.

(Any reading below 50 is recessionary.)

(Any reading below 50 is recessionary.)

Visually, every component measured fell:

New orders particularly fell, which is especially odd, given that consumer expenditures are reportedly soaring (according to the Biden administration’s statisticians). If purchases were flying out the door like we were told, you’d think retailers would be ordering stock in a hurry.

New orders particularly fell, which is especially odd, given that consumer expenditures are reportedly soaring (according to the Biden administration’s statisticians). If purchases were flying out the door like we were told, you’d think retailers would be ordering stock in a hurry.

There was, however, one uplifting note—one area in manufacturing that saw a tidy gain—prices. Prices paid rose from 52.9 (above the recessionary level) to 54.0. So, at least something is rising under Bidenomics. You’ll notice that means—when one looks further up the pipeline from where consumers are standing—that manufacturing prices have resumed their gains in a clear and well-maintained trend channel, in spite of the couple of months of modest inflation reprieve that Powell & Co. said could be the basis for the Fed’s first rate cuts:

Other than the prior two reported months of declining prices before this one, what I see is a trend of very clearly rising highs and rising lows. So, the background price pressure for eventual consumer prices remains sturdy and consistent.

Other than the prior two reported months of declining prices before this one, what I see is a trend of very clearly rising highs and rising lows. So, the background price pressure for eventual consumer prices remains sturdy and consistent.

Assuming manufacturers make things to be consumed by consumers, why are things looking upside-down as follows if consumer expenditures are expanding robustly?

That looks to me like manufacturing inventories soared, which is usually because fewer stores are stocking up, which would be consistent with new orders going down, which is usually because people are not buying things as quickly.

That looks to me like manufacturing inventories soared, which is usually because fewer stores are stocking up, which would be consistent with new orders going down, which is usually because people are not buying things as quickly.

Says Zero Hedge,

The manufacturing pipeline is now hopelessly clogged, price liquidations are imminent and mass layoffs are about to begin!

That didn’t stop the government lies from abounding all the more to create cover:

While traditionally a 50 print in the ISM is the cutoff for contraction, the highly politicized ISM report was quick to claim that a "manufacturing PMI above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy": spoiler alert: it does not, but it is an election year, so anything goes. In any case, not even the ISM was able to put much more lipstick on this pig and explained that this "contractionary expansionary" print was hardly the stuff expansions are made off with ISM chair Tim Fiore saying that "the past relationship between the Manufacturing PMI® and the overall economy indicates that the August reading (47.2 percent) corresponds to a change of plus-1.3 percent in real gross domestic product (GDP) on an annualized basis.”

Translation: we are this close to stall speed.... and the survey respondents by large agreed:

“A noticeable slowdown in business activity. Staffing and production rationalization has been triggered. Previous optimism about future growth has been dashed.” [Chemical Products]

“Backlog has dropped in half as invoicing remains strong, but orders have slowed significantly….

“New order intake is sluggish at best….

“Our order levels are on a slow, steady decline; it looks like the trend will continue through the end of the year. We are downsizing through attrition and not hiring backfills…. [Fabricated Metal Products]

“Business is cooling down, and we don’t expect a rebound until after the election is over.… [Paper Products]

“We are preparing for a slowdown in U.S. auto sales….” [Primary Metals]

“High interest rates are curtailing consumer spending on large discretionary spending for furniture, cabinetry, flooring and decorative trim, which has affected our industry sales potential…. Interest rate cuts may not happen soon enough to have an impact this year.” [Wood Products]

All so very odd … like geese flying south in the heat of the summer.

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!