With a Shiller P/E of 34, US stocks are now priced at the top 1% level in history. Globally, stocks are also paying out record profits to shareholders, even as companies claim they need to raise prices to cover rising costs. It looks like a good part of those price increases are to create even higher profits for shareholders. Inflation is not all due to rising labor costs and materials costs, transportation costs, etc. It’s also largely driven by a huge effort to push fatter profits into bigger pockets.

Global dividend payouts to shareholders hit a record $1.66 trillion in 2023, according to a new report by British asset manager Janus Henderson. Around 86% of listed companies around the world either increased dividends or maintained them at current levels in 2023….

And the rate-of rise for those profits being paid out is increasing:

The Global Dividend Index report, published Wednesday, said payouts rose by 5% year-on-year on an underlying basis, with the fourth quarter showing a 7.2% rise from the previous three months….

The banking sector contributed almost half of the world’s total dividend growth, delivering record payouts as high interest rates boosted lenders’ margins, the report found.

So, everybody’s getting fatter as prices rise … except the consumer.

With earnings at record highs and price-to-earnings at record highs, you couldn’t have a more extremely positioned market. Says Jeremy Grantham,

As for the U.S. market in general, there has never been a sustained rally starting from a 34 Shiller P/E. The only bull markets that continued up from levels like this were the last 18 months in Japan until 1989, and the U.S. tech bubble of 1998 and 1999, and we know how those ended. Separately, there has also never been a sustained rally starting from full employment….

If you double the price of an asset, you halve its future return. The long-run prospects for the broad U.S. stock market here look as poor as almost any other time in history. (Again, a very rare exception was 1998-2000, which was followed by a lost decade and a half for stocks.

And, yet, corporate CFOs, even though they express darker views today on inflation that most investors, are still bullish on where the market will go from here. In displaying the paradox Grantham writes about, these CFOs also believe the Fed is doing a splendid job and will stick its soft landing, even though they believe inflation will run hotter for longer than most investors seem to:

Chief financial officers at large companies see a U.S. economy and equities market that can continue to grow, even as fears about sticky inflation and a potentially overextended, and concentrated, bull run in stocks weigh on investors….

The percentage of CFOs who think the Fed will be able to achieve a soft landing has reached a five-quarter high, at 48%. It’s a marked change from where CFOs were a year ago in Q1 2023, with expectations of a soft landing tripling since the first quarter of last year.

For the first time in five quarters, not a single CFO rated the Fed’s efforts to bring inflation down as “poor,” while those who described the central bank’s policy as “good” edged higher….

CFOs have been consistent across our surveying in their view that inflation will not return to 2% any time soon … with nearly 80% of CFOs saying inflation won’t hit the Fed’s 2% target before 2025 at the earliest.

So, CFOs believe the Fed will not move on lowering interest nearly as soon as investors are pegging the Fed’s turn. They place the date for the first cut sometime around September.

I think there is still a lot of blue sky and optimism in that number.

CFOs don’t see rate anxiety as being a major short-term hurdle for stocks. Over 80% of CFOs believe the Dow Jones Industrial Average

is more likely to continue its run up to the 40,000-point mark, with technology continuing to lead the way among sectors, than slip into a bear market.

Even though they are likely too optimistic about the Fed’s turn, they will be right if the the economy crashes and takes stocks down with it before the Fed gets to its turn; but they’ll be right on the Fed’s timing for the wrong reasons.

Restrictive monetary policy ultimately leads to a large drop in consumer credit quality and demand that damages the economy and, even if in the short-term the labor market remains solid, ultimately layoffs spiral across sectors before the Fed can reverse course and avoid a recession.

Fed tightening never ends well, and the Fed has a long way to go on inflation. Even the CFO’s acknowledge a longer framework than their investors foresee, but others who are not trying to pump stock prices see an even longer road, as do I.

The long road ahead

As Grantham lays out,

Every technological revolution like this – going back from the internet to telephones, railroads, or canals – has been accompanied by early massive hype and a stock market bubble as investors focus on the ultimate possibilities of the technology, pricing most of the very long-term potential immediately into current market prices. And many such revolutions are in the end often as transformative as those early investors could see and sometimes even more so – but only after a substantial period of disappointment during which the initial bubble bursts. Thus, as the most remarkable example of the tech bubble, Amazon led the speculative market, rising 21 times from the beginning of 1998 to its 1999 peak, only to decline by an almost inconceivable 92% from 2000 to 2002, before inheriting half the retail world!

These times, flush with enthusiasm and priced in stocks to record highs that are almost inconceivable with CFOs betting stocks will go a lot further, don’t end well. (Eventually, as Grantham says, some of the revolutionary companies go on to enormous growth and transform the world, but not before the huge bubble that inflated around them bursts and takes their stock way down, too.

It also seems likely that the after-effects of interest rate rises and the ridiculous speculation of 2020-2021 and now (November 2023 through today) will eventually end in a recession.

Just like the views expressed by CFOs seem almost self-contradictory, so does the reality behind stocks appear to contradict what the market is showing:

If things are so good, why on earth is the rest of the world so down at heel, with very average economic strength and average profitability and with both getting weaker? The UK and Japan are both in technical recessions; the EU, especially Germany, also looks weak; and China, which has done a lot of the heavy lifting in global growth for the last few decades, is pretty much a basket case for a while (although getting very cheap in its stock market). Global residential real estate looks particularly tricky also….

I’ve spent 90% of my time for the last 15 years studying what I call underrecognized long-term problems, and oh my has this been an interesting and busy time for such a specialty! Particularly right now as all these long-term issues, which seemed just a couple of years ago to be offering the hope of 5 or 10 years before they took a bite out of us, have decided to all arrive in a hurry.

And they are certainly arriving. There is more news today of massive store closures, and oil prices took a 2% jump again today. Oil was the biggest factor holding down inflation, so the likelihood I see is that inflation will rise more than even those CFOs are seeing. One headline today says “inflation is starting to feel like a forever war” which is the kind of war I’ve said it will feel like. Some economists say inflation is likely to remain longterm at or above 3% because this last part of inflation is going to be very, very stick. Rising petroleum prices, which seem quite likely, would certainly make inflation go back up, having been the big thing that took it down but also because ricing petroleum prices push up all other prices.

Lara Rhame, chief U.S. economist at FS Investments, thinks that we're living in a "3% world" until further notice.

As inflation keeps raising prices higher, and consumers keep paying higher interest because the Fed has to keep interest rates up longer to fight this enduring inflation, the consumer, as Grantham noted historically, will wear out.

Economist Wolf Richter, who doesn’t run with the usual economist pack, says, in reviewing the latest CPI Report, that the inflation saga is “far from over”:

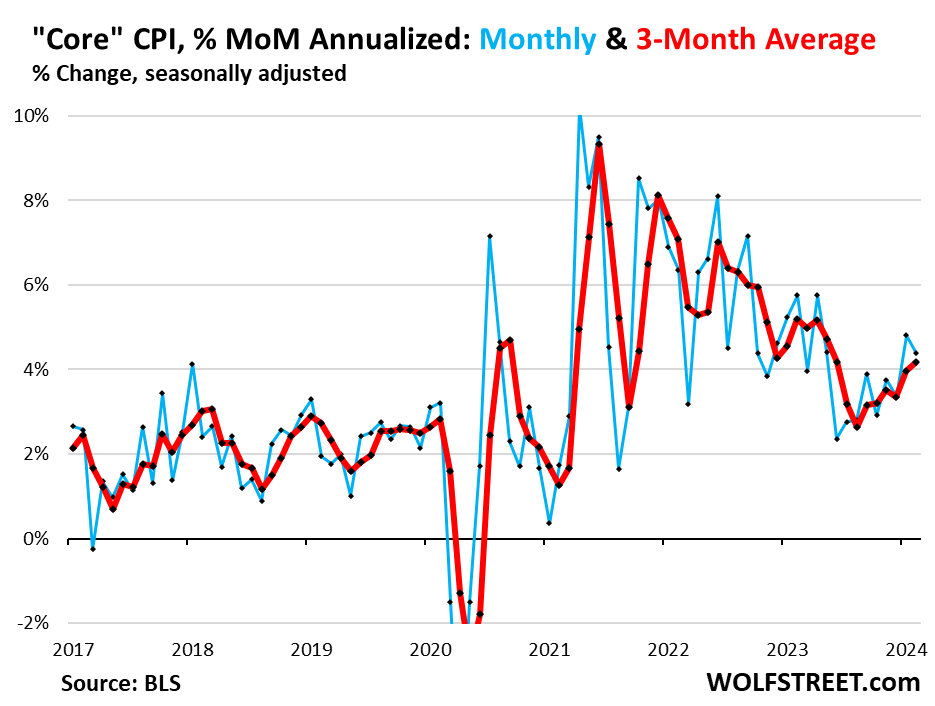

Core services CPI — 61% of total CPI and infamous for historic head fakes — is approaching 6% annualized six-month average….

The overall CPI has been pushed down by plunging energy prices and by dropping durable goods prices. But it has also been re-accelerating on a month-to-month basis for the past three months….

Here, again, is a picture of the rising trend in the core services part of CPI that the Fed watches most intently:

Not a hopeful picture for the road ahead.

The Fed has been in search of “confidence” that inflation continues to cool. But this is not a confidence-inspiring chart. Maybe they’ll have to search for confidence a little longer….

We’ve been disconcerted here for months how inflation in core services, after cooling a bunch, has been reheating. But that’s how inflation is – it produces head fakes and then serves up nasty surprises….

The six-month moving average accelerated to 5.8% annualized, the worst since May 2023.

As Grantham concludes in his article linked in the headlines below (and I’ll finish with his words):

The paradox that worries me here for the U.S. market is that we start from a Shiller P/E and corporate profit margins that are near record levels and therefore predicting near perfection; yet we face in reality not just a very risky disturbed geopolitical world, with growing concerns about democracy, equality, and capitalism, but also an unprecedented list of long-term negatives beginning to bite. The stark contrast between apparent embedded enthusiasm and these likely problems seems extreme, illogical, and dangerous.

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!