- No One Wants to Say “A Recession Is Fine”

- Why Is Unemployment So Low?

- Staring Us in the Face

- Ponzi-Like Dynamic

- Dallas, Energy, and Jared Dillian

The Federal Open Market Committee’s 12 voting members differ on where they think interest rates should go this year. But we know they’re unanimously against cutting rates until at least 2024—or at least they were as of December, according to that meeting’s minutes.

That means one of the three possible directions (up, down, sideways) is currently off the table. Rates will thus move either sideways or up—unless the FOMC members change their minds, which is quite possible. They all profess to be “data dependent.” However, the bond market doesn't believe that. Traders continue to price in rate cuts later this year.

My own forecast, as noted in last week’s Year of the Pause, is they will hike to 5% and possibly 5.5% then wait to see how the economy responds. They want to control inflation without causing too much pain. But of the two, controlling inflation takes priority. I think we have to take Powell at his word.

These policy arguments have a lot of nuances, meaning “subtle distinction or variation,” as Merriam-Webster defines it. We live in a time when subtlety is often lost in the yelling and insults. Fortunately, I have a wide group of well-informed, thoughtful friends with whom I can debate economic questions vigorously but amicably.

Today I’ll share some of their comments and forecasts with you. They don’t necessarily match my own outlook but that’s why they’re valuable.

The beginning of wisdom is to constantly question yourself. That can be harder than it looks. As humans, we tend to seek out those who agree with us. Confirmation bias is a strong human trait. Mea culpa.

|

[Unbiased Analysis on Today’s Economic Issues] The only way to respond to the challenges in the market today is with the best information at your fingertips. That’s why over thousands of readers rely on John Mauldin’s research to receive top-level insights and out-of-consensus perspectives, sent to their inbox 3–4 times per week. |

No One Wants to Say “A Recession Is Fine”

As I’ve mentioned, a recent email technology fiasco scrambled my usual reading habits. It had some benefits, though, highlighting what I really missed. It also reminded me that the way I consume news isn’t what most people would call “normal.”

Like you, I have a bunch of favorite sources. Mine tend to be people I know personally or have read a long time. When I see someone make a perceptive point, I can often pick up the phone or drop an email asking them for more. Frequently (and sometimes remarkably), they answer me. To me this seems so natural, I have to remind myself not everyone can do it. I wish they could because it leads to some amazing conversations—especially when I pull several sources together. (The panels you see at SIC are an effort to replicate this.)

Here's a recent example. Last week I saw bond market wizard Jeff Gundlach placing this year’s recession odds at 75%. That seemed low to me, but Jeff is someone I have learned not to ignore. Here was a chance to question myself and maybe learn something.

Frankly, Jeff's forecasting approach makes more sense. Very little is absolute about the future, other than the sun coming up. While the large consensus (and I am in it which makes me uncomfortable) says we will see recession this year, some very good analysts like my friend Dr. Ed Yardeni think we will see a soft landing. Jeff Gundlach believes that the Fed is close to finishing its rate hike cycle, whereas my friend and trading guru Michael Boyd tells me he thinks Powell will keep hiking rates until something looks like it will break. He thinks 6%+ is on the table. (You likely don’t recognize his name, but you wish you did. I have a lot of friends like that. I am blessed on that front.)

Anyway, I was reading Gundlach’s piece before bedtime which, thanks to the (perfectly legal and awesome) gummies I take to help me sleep, is not easily postponed. But I jotted off a quick email to a few friends asking what they thought of this outlook. Within a half hour I had several fascinating replies.

One came from CORBU’s Samuel Rines, who has a habit of saying incredibly thought-provoking things in just a couple of sentences. Quoting (with his permission):

“Why does deceleration in headline / core [inflation] matter? The FOMC reaction (higher rates) isn’t breaking markets. So, why stop? Markets are rallying on every sign of a pause in the future.

“No one wants to say, ‘a recession is fine.’ But the FOMC is highly implying it.”

That really cuts to the core issue. The Fed got a late start but when you include the balance sheet reductions, it’s been tightening at an almost unprecedented pace for almost a year now. We see some signs of weakness, though it’s not clear Fed policy caused them. Job growth is still positive. Stock prices are down yet corporate earnings remain relatively strong. Home prices are retreating from very high levels but not crashing, except in certain localities.

Could worse conditions still be coming? Sure. Fed policy changes have lagging effects. But from the FOMC’s perspective, the current strategy seems to be producing the desired benefit (lower inflation) without undesirable consequences (unacceptably high unemployment or credit markets crashing). This gives them room to continue.

If they do that, the real question isn’t so much whether we get more rate hikes, but when previous hikes will show their full impact. It’s a slow erosion as higher financing costs change consumer and business decisions. As time passes, more people see their debt servicing costs rise as rates reset to higher levels. That leaves less money for other spending—which is exactly what the Fed wants: lower aggregate demand.

I have written many times on the deficiencies of our unemployment data. That being said, it’s consistently wrong in the same way so it is a good tool for relative comparisons.

With the Fed raising aggressively, when there are clearly signs of the economy slowing down in certain sectors, we have to ask why unemployment is so historically low. Some of it is demographic trends but there are other reasons.

- COVID accelerated retirement. Literally millions of experienced and productive workers left the workforce. Maybe for retirement, maybe doing something to stay busy, but they are not showing up in the unemployment numbers.

- Numerous lower-wage service sectors simply saw their employees drop out in 2020‒2021. Higher wages plus disappearing benefits are slowly bringing them back, and even though we read of layoffs and slowdowns, the fact of the matter is there are more jobs than potential workers. You can bet the Fed is closely watching the ratio of available jobs to available workers. That ratio, along with the potential for a credit crunch, is far more important in Powell's calculation than many other things pundits bring up.

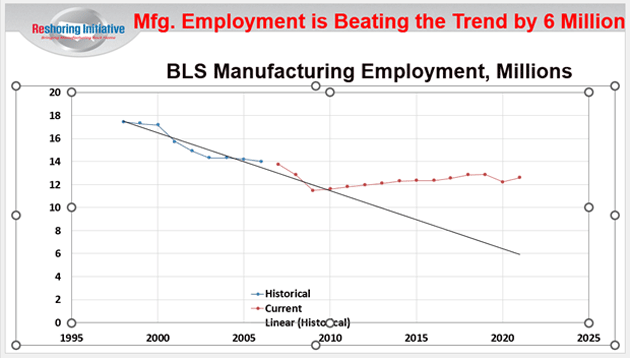

- Harry C. Moser of the Reshoring Initiative, sent me this note responding to a chart we recently sent Over My Shoulder members. Harry has been assiduously working for over a decade to help US businesses “re-shore” their manufacturing and create jobs here. That process is clearly accelerating. He writes:

“The flattening in manufacturing corresponds exactly with:

- The growth of annual reshoring and foreign direct investment job announcements which accelerated from 6,000/year in 2010 to 350,000/year in 2022.

- A dramatic reduction in the rate of job losses due to offshoring.

“Our regression analysis of BLS manufacturing labor data shows the same impact and timing. Conclusion: Manufacturing employment is now 5 or 6 million higher than one would have predicted before the Great Recession.”

Source: Reshoring Initiative

In theory, the Fed could balance all these moving parts and get inflation down to its 2% target without sparking recession. It is difficult, though, and I have no confidence they can do it. (Reminds me of the Yogi Berra quote: “In theory, it works; in practice, it doesn’t.”) Nor does my friend Dave Rosenberg, who sees a 100% chance of recession this year.

Dave kindly gave me permission to quote from his annual forecast. (Rosie is sometimes labeled a perma-bear, but he went very bullish at my 2009 conference when many others were still bearish. You might say he is data-driven.) Here is his introductory section:

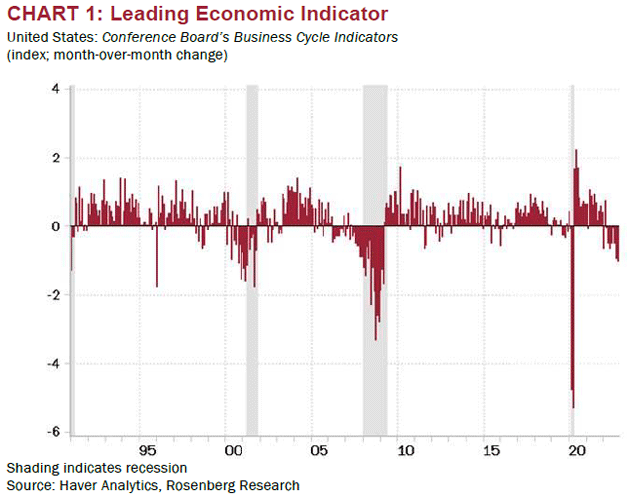

“The seeds for the 2023 recession were sown a while ago by the relentless decline in the Conference Board’s leading economic indicator, which has now fallen for nine consecutive months. The data go back to 1959 and I can tell you that at no time in the past have we seen a string of weakness like this, with a 5.6% annualized contraction over such a timeframe, that failed to presage a recession within a quarter or two. Call it nine for nine back to fifty-nine. The recession is staring us in the face (and if it is so ‘priced-in,’ why is the consensus calling for positive EPS growth for next year?).

Source: Rosenberg Research

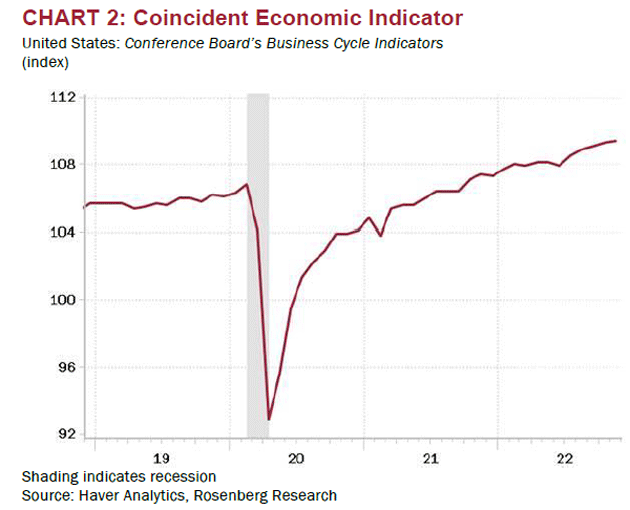

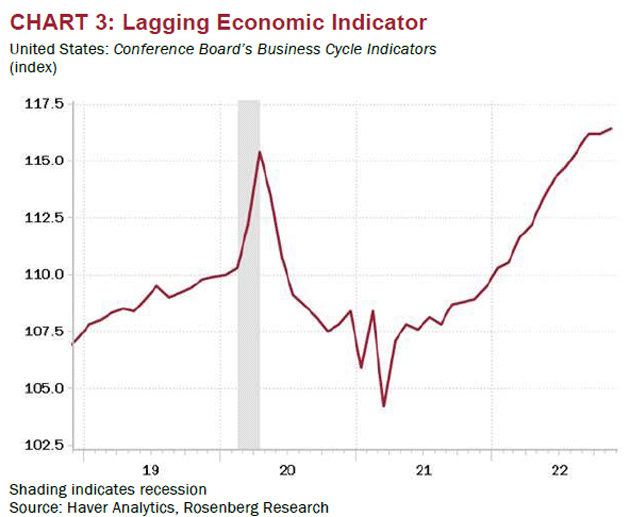

“What the Fed is focusing on is the coincident index, which is still on a mild uptrend—but that only tells you where we are today. And the index of lagging economic indicators, which also are hitting new highs at the current time, tells you where we were yesterday. The leading indicator is chock full of leading factors like capital goods orders, building permits, the workweek, and consumer buying plans. The coincident index has nonfarm payrolls, and the lagging index consists of the unemployment rate, wage costs, and consumer services inflation. The Fed is driving the bus all right but is not looking through the front window. Which means what? It means we are going into an outright recession. A national haircut to GDP, rising unemployment, asset deflation, and looming debt defaults. This is the theme for 2023 and is typical for the year that follows the Fed tightening cycle—think 1970, 1975, 1982, 1990, 2001, and 2008.”

Source: Rosenberg Research

He’s somewhat less depressing on employment, but more bearish than many.

“Another shoe to drop is employment, and if the Fed is right on its jobless rate forecast, up to 4.6% from the 3.5% low, we are talking just under 2 million jobs being lost from that development. The Fed has given us this on a silver platter because it is not the level of the unemployment rate but rather the change that dictates recessions—and we have never failed to have a downturn with the jobless rate going up this much. Not the end of the world, but definitely in keeping with the Powell pain doctrine. In fact, companies have already been rationalizing on labor by cutting the workweek and replacing full-time jobs with part-time jobs.”

Back in 2021 Dave was firmly on inflation being “transitory.” He’s never wavered on that point and thinks the rest of us will see it soon.

“What changed [vs. the pre-COVID period —JM] was the series of supply shocks the economy endured over these past two-plus years, and in 2022 this included the Russian invasion of Ukraine, the frequent Chinese lockdowns in key port cities, and earlier on, the impact that the omicron variant exerted on the female labor force participation rate.

“In other words, it is clear that the inflation burst was transitory after all, and reflected the shift in the aggregate supply curve, which is now in the process of thawing out in both the labor and product markets. With demand growth now slowing down to a trend below that of aggregate supply, one can expect excess capacity to be the next chapter of the story. For all the talk of commodities, the reality is that oil prices were higher in 2014 than they are today; copper was higher in 2010 than it is today; wheat is below 2011 levels; and shipping rates, like the Baltic Dry Index, are lower today than they were in 2018. High prices are not inflationary. Prices stayed high throughout the Paul Volcker years. Inflation is all about price momentum, and that is clearly subsiding.”

A lot to chew on there. I’m struck by his description of the “wealth effect” from falling home prices. In macro terms, he says a big housing downturn would do more damage than a stock market crash because more people own homes than stocks, and they are more highly leveraged. Fortunately, we are a long way from such a drop, but it could yet happen.

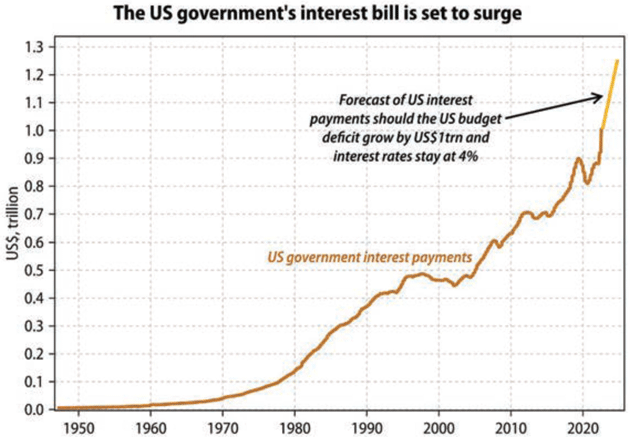

The late-night email discussion I mentioned above also included mi bueno amigo David Bahnsen, who provocatively said maybe Jeff Gundlach was asking the wrong question. David’s own annual outlook rather boldly suggests the Fed’s policy rate will be lower by year end—meaning the FOMC will cut rates at some point this year. He expects this mainly because the higher rates are especially problematic for the US Treasury. Here’s David:

“Many have used the impact of higher rates on the P&L of the federal government to argue for more damage coming to our bond market and to our nation’s economic health. It is a fair and partially correct argument. But it also begs the question—couldn’t the damage higher rates create to national spending be an argument for why such higher rates will not be allowed to persist?

Source: David Bahnsen

“That is, in fact, exactly my argument. Quoting the ghost of Herb Stein seems fair here—‘If something can’t happen, it won’t.’ I would first argue that the longer end of the yield curve sees excessive government indebtedness as a sign of weaker economic growth and therefore puts downward pressure on the long end of the curve (for more support of this position see: all countries everywhere on earth, for 35 years). But we are talking about the short end of the curve here, and I simply do not believe that the Fed is apathetic (in the myriad of factors they have to consider) to the impact of short-term borrowing costs on the biggest short-term borrower on the planet.”

David ends his forecast report with some wise advice about investment risk:

“Investing requires certain principles, disciplines, beliefs, and behaviors, that are timeless, universal, and true. I was struck by this line in a recent Strategas Research report: ‘With this in mind, and with our conviction that monetary conditions will continue to get more restrictive, we believe the biggest unforced error an investor can make today is to make long-term investments in companies that have come to rely on the kindness of strangers for capital.’

“The kindness of strangers. Put differently, investments that work only so long as people keep believing, hoping, and envying. They don’t work because they are productive, or profitable, or proven—they work only as long as someone else keeps putting money into it. The period of time that the ‘ponzi’-like dynamic being described here can work is extended in times of easy money and excessive monetary accommodation. When that punch bowl gets taken away, the inevitable fate of such malinvestment is accelerated.

“My concluding thought in the analysis of 2022 and looking forward to 2023 is to never be tethered to the punch bowl of FOMO, monetary excess, or ill-advised speculation again. History is filled with manias and speculations, and in just the last 25 years we seem to have gone through an unprecedented amount of truly dramatic ones. 2023 and the years beyond it will present enough challenges in terms of economic health, geopolitical stability, and monetary policy that investors need not invite excessive risks to the party. Winning a race is hard enough without tying ankle weights to yourself.”

A few bullet point highlights of his annual forecast (with my comments), which is a must-read for me:

- Like Rosie, David thinks inflation will drop a lot more than people think. I think energy and commodity prices, along with wages, will keep inflation higher than some do, but still coming down. This is important because I don't think the Fed will “pause” until we have a “3 handle” on the inflation number, and then will keep rates there until inflation is well and truly gutted, or unemployment breaks really bad.

- David and I part company on his next call: He thinks the Fed funds rate will be lower at the end of the year. I actually hope he's right.

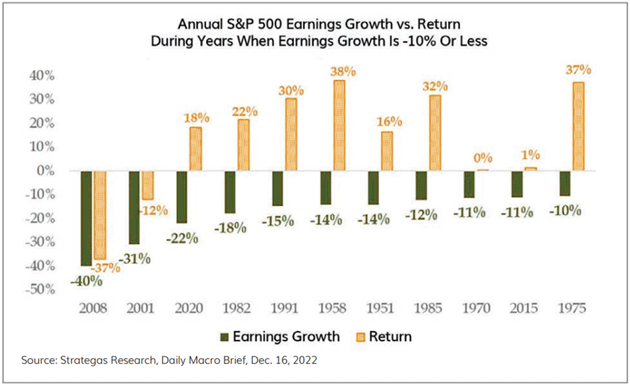

- His call on earnings growth is nuanced: “The S&P 500 delivered a positive return in 9 of the last 11 times we saw negative earnings growth year over year… Even in those nine positive years where earnings growth was negative, there was a drawdown (on average) of -14% along the way. In other words, whether markets end positive or not, we expect downside volatility along the way in periods where earnings growth is stunted.

Source: David Bahnsen

- Value beats growth (again). I agree. And I am bullish on the true value of high-quality, dividend-paying companies.

- More on this next week, but he writes to not underestimate the impact of China reopening. Totally agree.

- Emerging markets finally find some time in the sun.

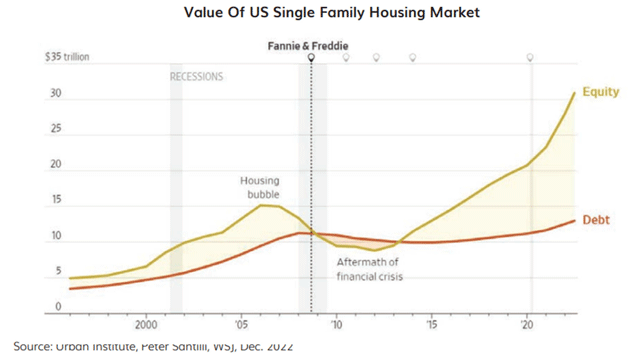

- Housing is going lower, and “I feel fine.” The quality of credit is much higher than 2005‒7, and there is more equity in those homes (in general).

Source: David Bahnsen

- China, Russia, and geopolitics will leave [the US] with weaker global stability at the end of 2023 than we have now.

- David believes skepticism on private markets is misplaced. A very nuanced section.

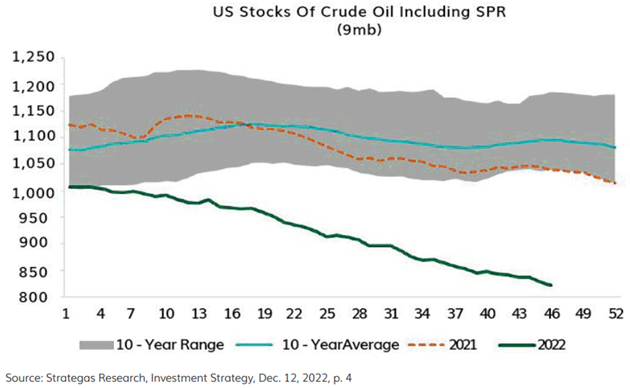

- The energy story is not dead. We will be going into this in detail in the future, as I am very bullish on energy in general, especially in the medium and long term.

Source: David Bahnsen

Those are important thoughts from Rosie and David. Risk is inevitable. Risk is also what makes profit possible. But we can take risk wisely or foolishly. Years of artificially cheap money made risk easier to take. The punch bowl was always at hand and always full. Now it’s not. Worse, if you believe Jerome Powell, the punchbowl is gone.

Dave Rosenberg says the time to buy stocks is not when the Fed stops tightening, but when it stops cutting because the recession is over. Right now, we’re not even sure the recession has started. Yes, there are opportunities in select areas like energy. That may be a prudent risk. Throwing good money into an index fund is a different matter. We will continue this discussion on the forecasts of other analysts next week.

Dallas, Energy, and Jared Dillian

I will be in Dallas the last week of January filming videos on a series of energy-related issues. I am doing a lot of research and writing on energy and the more I read the more bullish I get. Note that bullish for me is oil above $60. Whenever the recession is over and China demand kicks in? I think it goes a lot higher.

Shane and I will host Jared Dillian and his wife tonight here in Dorado Beach. That should be a lot of fun. I mentioned gummies above, and I would have bet a great deal 10 years ago that you would never see me using any form of marijuana. But old dogs can learn new tricks. It took some experimenting, but the gummies help put me to sleep instead of using alcohol in addition to sleeping pills. Much healthier.

My computer issues are about 90% resolved after 30 days, but it has been an absolute #$%$% (insert your favorite expletive). And with that I will hit the send button. You have a great week! And don’t forget to follow me on Twitter! I have friends urging me to post on TikTok. Now that would be a really new trick for an old dog.

Your having more fun than I thought legally possible analyst,

|

|

John Mauldin |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.

About the author