Investors in stocks, bonds and commodities should be aware of the rate of inflation and how it is affecting the value of their investments.

When a currency loses value as it does during bouts of inflation, cash, bonds and stocks are not where investors want to be.

A pile of cash today is worth 3% less a year from now if inflation is running at 3%. A bond promises to pay a certain amount of currency (the yield) in future (the term), so during inflation the purchasing power of that currency is being diluted.

Stocks don’t fare much better during high-inflation periods. When inputs are higher businesses make less profits, meaning less earnings per share. Also, an unstable currency makes planning harder.

Commodities, some more than others, are a much better place to park your money when inflation + low economic growth = stagflation. This article sets out to prove it.

Investing during stagflation

Up until recently, the US economy managed to avoid this unhappy stagflation scenario. Inflation had come down dramatically from the 9% peak in 2022 to 3.4% in December 2023.

Economic growth in the United States has been rising, in line with a resurgence in manufacturing.

In the fourth quarter of 2023, US GDP was growing at an annual 3.4%.

However, this appears to be changing.

A gross domestic product report on Thursday, April 25 showed the US economy grew at an annualized 1.6%, versus the 3.4% in Q4, ’23. That’s quite a slowdown.

Meanwhile, inflation is back on the rise.

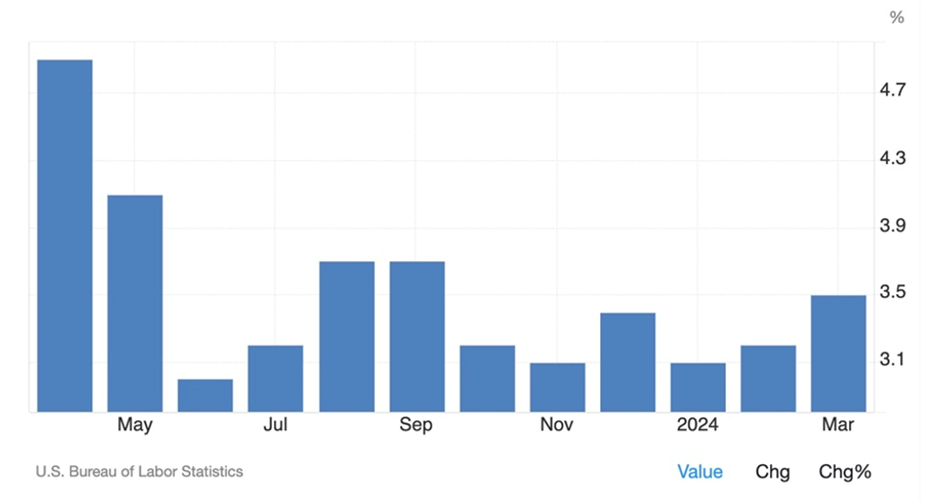

The March Consumer Price Index inflation print, made public on April 10, was 3.5%. In February it was 3.2% and in January it was 3.1%.

US inflation. Source: Trading Economics

US inflation. Source: Trading Economics

Evidence that inflation is walking away from, not walking towards, the Fed’s 2% target, continues to mount. According to the Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) price index, prices increased by 3.4% in the first quarter compared to 1.8% in the last quarter of 2023.

The monthly inflation numbers came in Friday. Again, they show prices rising higher than the 2% target, up 2.7% in March compared to a year earlier. The closely watched core PCE index, which leaves out food and energy prices, rose 2.8% in March.

Slowing economic growth plus rising inflation might mean stagflation for the US economy, according to many the outlook isn’t good. CNN reports:

[The] growing consensus among economists and investment strategists is that the days of the Goldilocks economy, where inflation was coming down without slowing GDP, are numbered.

Global manufacturing recovery underway, can it last?

GDP forecasts are now signaling lower growth starting in the second half of the year.

Investment strategist Lyn Alden writes that cash and bonds are a bad place to be because their yields are often below the level of inflation in an inflationary environment. (Of course, this argument doesn’t hold currently, with interest rates on savings accounts between 4 and 5% and government bond yields also in the same range.) Stocks as mentioned at the top don’t perform as well when inflation is high.

As for commodities, Alden says Industrial commodities (e.g. oil and copper) tend to be the big winners in inflationary environments. Almost by definition, if inflation is high, it means commodity prices are rising.

We know this to be true.

Commodity prices influence the prices of manufactured goods, whether the end users are consumers, car companies, construction firms, or food suppliers. The monetary policy response, of course, is higher interest rates.

Take oil, for example. Past increases in oil prices have been a strong indicator for inflation, given that oil is such a major input in the world economy. Try making plastics without petroleum, or fertilizer without natural gas.

According to Investopedia, commodity prices are a leading indicator of inflation through two basic channels: commodities respond quickly to economic shocks such as increases in demand — for example the level of increased demand for goods and services that followed the end of pandemic restrictions; and systemic shocks such as hurricanes or other natural disasters:

“By the time it reaches consumers, overall prices would have increased, and inflation would be realized.”

The link between commodities and inflation — Richard Mills

So ironically, commodities are both a cause of inflation, and the cure for it, in terms of being a safe haven during periods of rising prices.

Note that commodities have been rising all year, even as the US dollar is strong, along with high interest rates and high bond yields. The prices of base metals copper, zinc and aluminum have gone up substantially, along with the Bloomberg Commodity Index, which is on a tear.

Bloomberg Commodity Index. Source: CNBC

Bloomberg Commodity Index. Source: CNBC

Source: MarketWatch

Source: MarketWatch

Source: CNBC

Source: CNBC

Copper. Source: Google

Copper. Source: Google

Aluminum. Source: Trading Economics

Zinc. Source: Trading Economics

Zinc. Source: Trading Economics

Gold and silver are also doing extremely well so far in 2024.

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

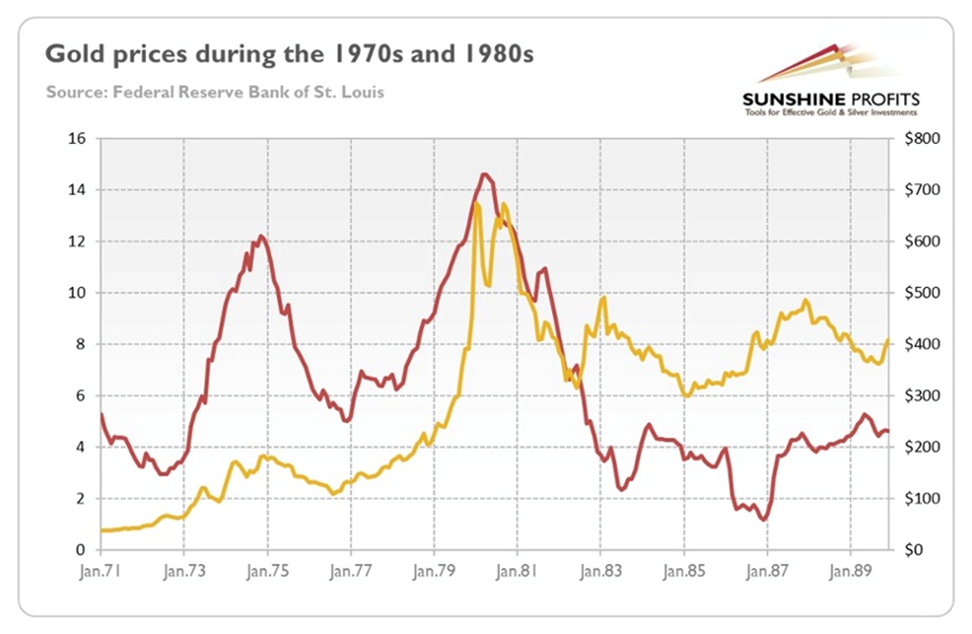

How has gold done during stagflation? As it turns out, quite well. The chart below by Sunshine Profits shows the gold price climbing during the stagflationary 1970s, surging from $100 per ounce in 1976 to around $650 in 1980, when CPI inflation topped out at 14%.

Gold prices in yellow compared to inflation in red.

Gold prices in yellow compared to inflation in red.

Source: Sunshine Profits

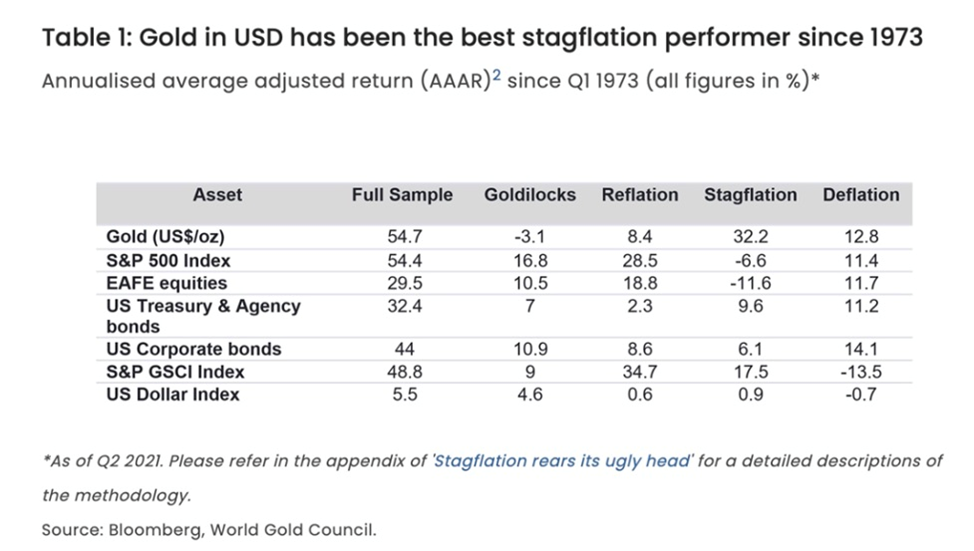

In fact, gold outperforms other asset classes during times of economic stagnation and higher prices. The table below shows that, of the four business cycle phases since 1973, stagflation is the most supportive of gold, and the worst for stocks, whose investors get squeezed by rising costs and falling revenues. Gold returned 32.2% during stagflation compared to 9.6% for US Treasury bonds and -11.6% for equities.

Simply put, gold does well in stagflationary environments because it benefits from the elevated risk environment, high inflation and falling real interest rates (interest rate minus inflation).

Alden writes, Gold in particular tends to do well during stagflationary environments, where economic growth is decelerating but inflation is still pretty high. It also tends to hold up well in outright recessionary/disinflationary environments, at least compared to equites.

If history is any guide, commodities do just fine when inflation rages and growth stalls, i.e., stagflation.

The economy was in a recession from December 1969 to November 1970 and again from November 1973 to March 1975.

The massive cost of the war in Vietnam and the expansion of social programs at home drove inflation higher.

Unemployment rose by 33% between 1968 and 1970 while the consumer price index went up by 11%.

In 1973 the country was hit by an oil crisis. The oil-rich nations of the Middle East were angered when the United States under Nixon devalued the dollar. When the US supported Israel in the Yom Kippur War, OPEC exacted their revenge by imposing an oil embargo on the United States and Israel’s European allies.

The price of crude oil shot up to $11.65 a barrel, an increase of 387%.

Nobody is suggesting the economic conditions of today are anything like the stagflationary 1970s. However there are certain lessons we can learn from history.

Last year, The Economist ran an article that referenced Credit Suisse’s ‘Global Investment Returns Yearbook’. The report shows that between 1900 and 2022, stocks and bonds beat inflation, posting annualized real returns of 5% and 1.7% respectively. However, during inflationary periods, both asset classes performed poorly. Real bond returns flipped from positive to negative when inflation rose above 4%, with stocks doing the same around 7.5%. During stagflation years, shares lost 4.7% and bonds lost 9%.

Thus, cash and bonds performed poorly as a hedge against inflation, whereas commodities offered an effective hedge. According to the Yearbook’s authors, commodity investors using dollars earned an annualized 6.5% in the long run, compared to American stocks’ 5.9%.

Better still, this return is achieved while being little correlated with shares, and moving inversely with bonds.

Commodity futures can be mixed with other assets for a portfolio with a much better trade-off between risk and return. At historical rates, a portfolio that is evenly split between stocks and commodity futures would have a better return than a stock-only portfolio, and three-quarters of the volatility. Best of all for an investor fearing high inflation and low growth, commodity futures had an average excess return of 10% in stagflationary years.

Ole Hansen, head of commodity strategy at Saxo Bank, explains why commodities shine during inflationary eras:

• Inflation Hedge: Traditional commodities like gold and silver are perceived as safeguards against inflation. As inflation erodes the value of paper currency, tangible assets, particularly precious metals, often keep their worth through rising demand and prices.

• Diversification: Amidst a stagflation backdrop where standard financial assets like stocks might underperform, investors often look to diversify their holdings. Commodities offer an asset class with minimal correlation, potentially enhancing portfolio performance during such times.

• Interest Rates: Central banks may be reluctant to hike interest rates in a stagflation setting for fear of hampering growth further. Moreover, a weaker dollar can make dollar-denominated commodities more affordable for non-dollar-based buyers, potentially amplifying demand and prices.

• Real Returns: In a climate where nominal returns on conventional financial assets are diminished by inflation, tangible assets like commodities can provide positive real returns. This is particularly pronounced when commodity prices surge due to supply limitations or strong demand.

The commodity sector consists of physical assets and the price settings of the individual commodity depends not only on demand but equally important on available supply.

The supply factor

Let’s return to bullet point four of the Ole Hansen piece above, i.e. that a commodity’s price depends not only demand but supply. While this seems obvious, it ties into the reason why commodities are such a good inflation hedge.

Lyn Alden, the investment strategist, writes that usually during inflationary periods, commodities are under-supplied and that it often takes years to bring on new supply.

Alden also observes that monetary inflation occurs when the money supply grows. If the amount of currency issued expands faster than “real-world resources”, (i.e., commodities, supply chain capacity, labor) then prices will rise because demand outpaces supply of real goods and services. We saw this when aggregate demand exceeded aggregate supply coming out of the covid-19 pandemic, which caused inflation to rise to levels not seen since the early 1980s. At the same time, we saw a huge increase in government expenditures paid for by printing money.

According to the US government’s Bureau of Economic Analysis, as of the third quarter of 2023, total government expenditures of $10,007.7 billion is 36.2% of total annual GDP of $27,610.1 billion.

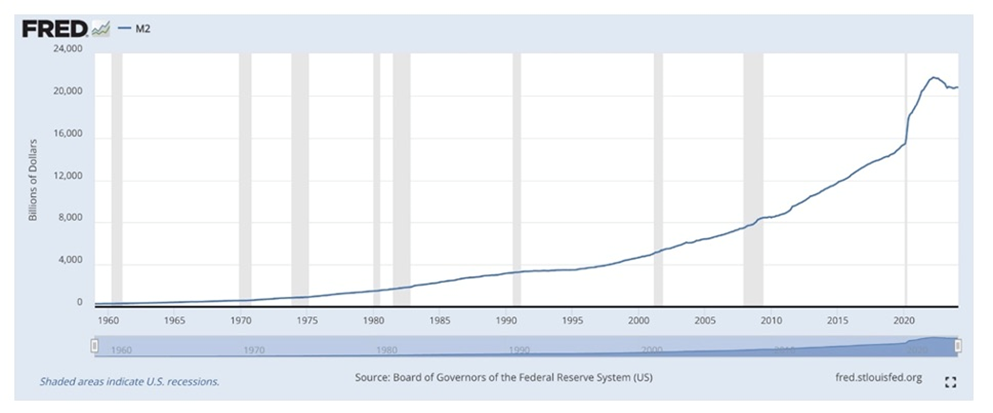

M2 money supply was about $16,000 billion in 2020 and it currently sits at $20,783 billion.

Source: FRED

Source: FRED

Alden says we can look at commodity capex (capital expenditure) cycles to see when commodities are structurally oversupplied or undersupplied — something we at AOTH are doing constantly.

For example, copper. To achieve net-zero emissions targets, annual copper demand is likely to double to 50 million tonnes (Mt) by 2035, according to a study by S&P Global. In 2023, mines only produced 22Mt globally.

(Net-zero is a target we will never achieve, doesn’t mean we are not going to try possibly reaching 30% of net-zero. Which means a still impossible copper increase of 9m/t annually.)

She notes the big inflationary periods usually have a mix of monetary inflation and supply-side bottlenecks, such as during World War Two.

Source: St. Louis Fed

Source: St. Louis Fed

Conclusion

What do we at Ahead of the Herd (AOTH) make of all this? Well, we’re not worried about all this stagflation talk. Why? Because we’re invested in commodities through junior resource companies – copper, gold, silver and graphite. Junior resource companies offer, imo, an excellent hedge against inflation.

Of course, the stagflation argument doesn’t hold currently – interest rates on savings accounts are between 4 and 5% while government bond yields are also in the same range, jobs are still strong and one month of slower GDP does not make a trend. But the Fed’s preferred inflation gauge is rising and interest rates will also have to rise. So while we’re currently re-thinking our positions in cash, stocks and bonds we are also considering committing even more to gold and silver and the electrification metals copper and graphite.

Our gold and silver stocks are safe if economic growth continues to slide and inflationary pressures worsen. Bad economic news leads to precious metals being are an attractive alternative to stocks. Gold/ silver perform even better if the dollar weakens. Investors also like gold and silver when inflation is high; unlike fiat currencies, precious metals don’t lose their value.

Industrial metals like copper also perform well during stagflation. Not only are they attractive for all the reasons presented by Ole Hansen (inflation hedge, diversification, interest rates, real returns), several, including copper, silver and graphite are supply-challenged. When the demand side of these metals is factored in, i.e., the fact that they are heavily required for electrification/ decarbonization purposes, they appear, to us, as stagflation-proof.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.