The new Yield Curve steepener has not yet un-inverted, but it’s in progress and thus far mildly inflationary

Reference Inflationary Yield Curve Steepening? from January 11.

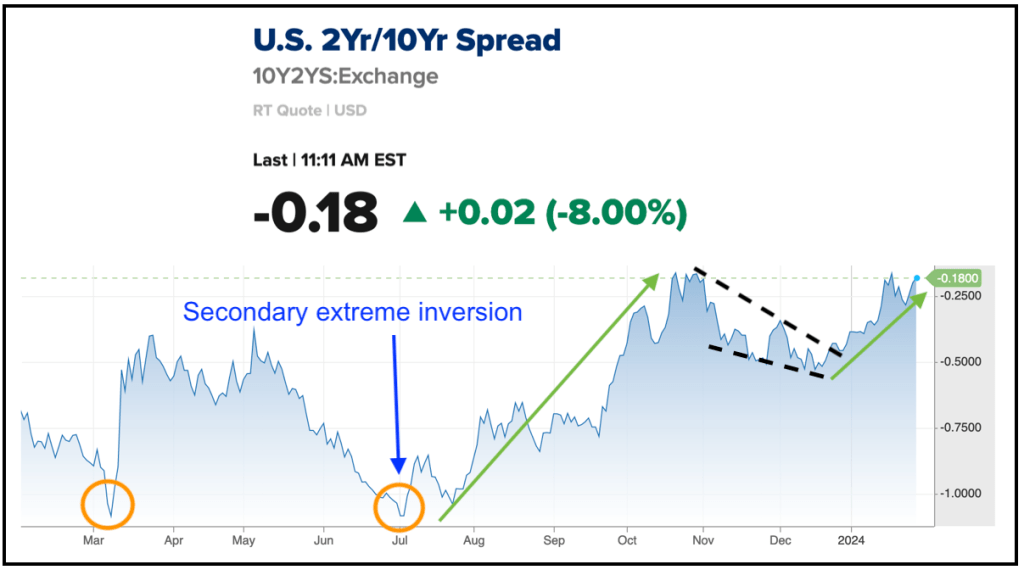

In my opinion, after the secondary extreme inversion of the 10-2 yield curve in July a new yield curve steepener was in the bag. That is exactly what the curve has been doing since the secondary inversion.

cnbc.com

cnbc.com

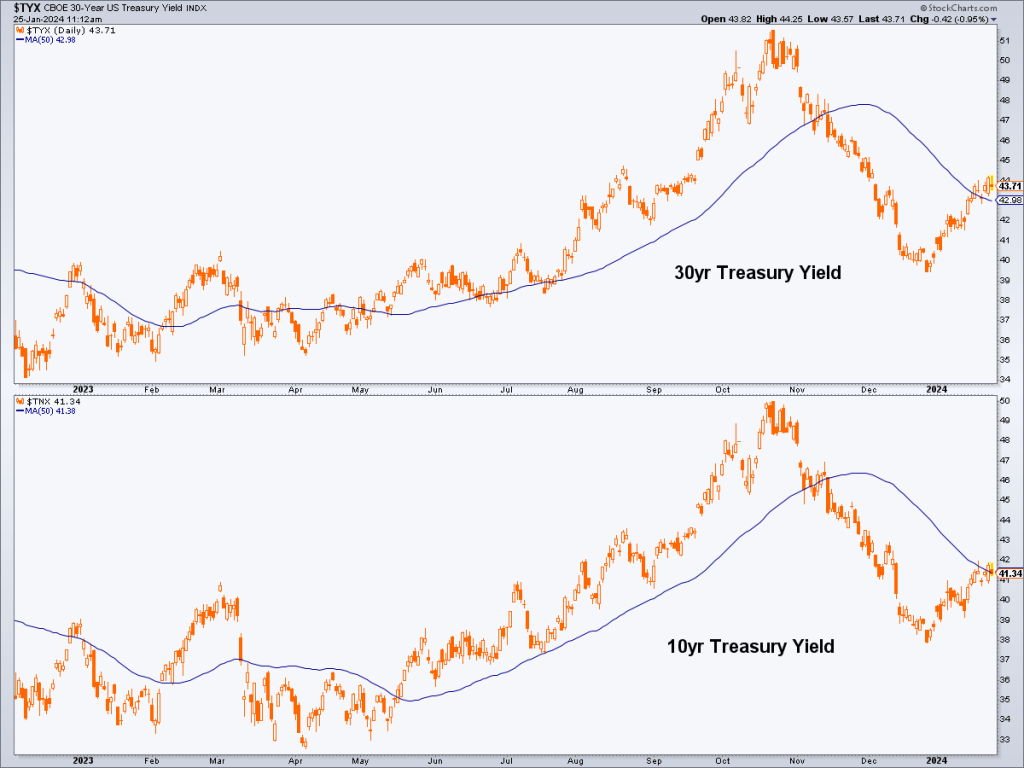

This phase of the yield curve steepener is thus far mildly inflationary in its signaling. We know this because the nominal 10yr yield has been rising since December along with the yield curve steepener. Indeed, the curve has been steepening under inflationary signaling since July, with a brief interruption of a Goldilocks style consolidation (black dashed ‘handle’/bull flag) as nominal yields dropped from October to December.

Keep in mind the word “signaling” used above. It’s important. The bond market was signaling inflation concerns even as the macro went disinflationary Goldilocks for the majority of 2023. That implied monetary tightness included what may turn out to have been a policy overshoot, again, in its signaling. In reality and in my opinion, there is no more paper and digital policy that can really rehabilitate this experiment gone way off the path of sound practices and into a Twilight Zone of the unknown.

But if the machines are programmed to interpret literally, then maybe so should we at least be aware of that which they are interpreting. The Yield Curve steepener is thus far inflationary. It calls into question the next step after the Goldilocks call a year ago. That was for disinflation to morph deflationary (and there are still signals in play indicating the potential for that outcome). But it could also reverse and brew a worsening inflation problem.

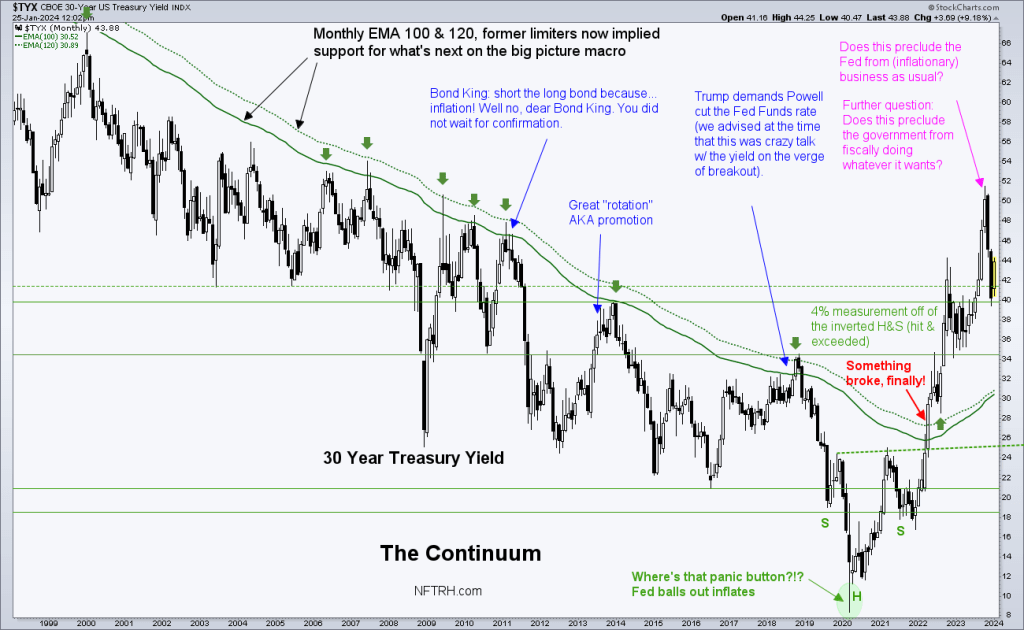

To make matters more complex, over the course of a yield curve steepener, both inflation and deflation can be the root instigator at different times. For an example, refer to 2007 when the yield curve steepener began as a long phase of inflationary pressure was just starting to ease (sound familiar?) and then it steepened impulsively in 2008 as deflationary pressure became undeniable. Then there was the 2020-2021 steepening that was purely under inflationary pressure. That one failed into Goldilocks and now here we are. Pick your poison.

In my opinion the administration in power is all but ready to pull the fiscal (inflation) lever sooner, not later, and to try to strong arm the Fed as well. We’re well under T-minus one year after all. Despite the political rancor tearing this country apart, confidence in the system (and its monetary and political, AKA fiscal, overseers) is still intact. The average American has no idea the risk they are being routinely subjected to by legions of financial advisers and finance managers operating to the old rules. Rules, I think, that are highly suspect in the new age of the Continuum’s secular trend break.

About the author