The next recession has all the ingredients to become the worst since the Great Depression because it will happened due to the collapse of the Everything Bubble—the biggest collection of major market bubbles in history. To size up the potential scale of this economic collapse, consider all the bubbles the Federal Reserve has inflated, each of which has expanded to a hot-air balloon size unseen heretofore:

- Another housing bubble like the solitary bubble that imploded into the Great Recession, but with prices now much, much loftier than anytime in history.

- A commercial real-estate balloon-size bubble rapidly losing altitude now due to the seismic demographic shift away from brick-and-mortar retail trade and away from office space in favor of more remote working.

- A maniacal stock-market bubble of froth built over more than a decade to reach valuations that have extended far above where they were at their peak when the dot-com crash hit or when the Great Financial Crisis plunged us into the Great Recession.

- The most gigantic bond bubble in the history of the world due to central banks—especially the Fed—sucking up more government and commercial bonds at very low interest than at any time in the history of the world. The collapse of this bond bubble will include the defaults of many zombie corporations, which means companies that were only able to survive due to very cheap interest on their corporate bonds being used to keep the lights on and the doors open, which all goes away.

Bubble trouble

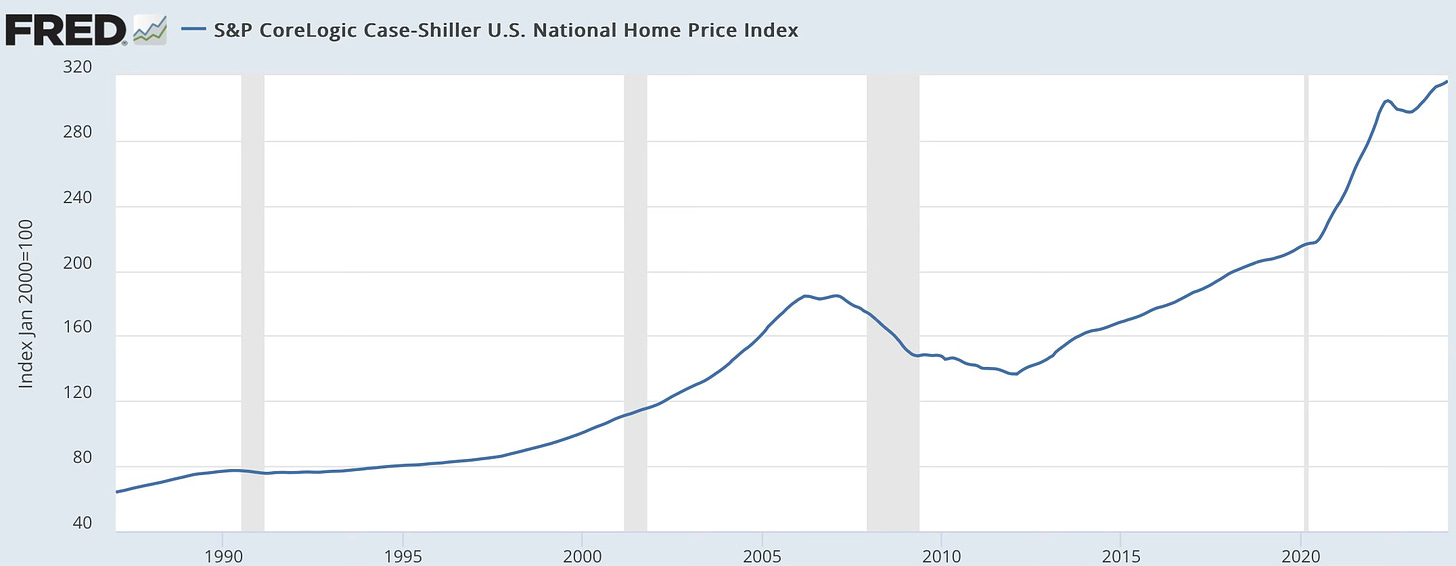

To get a sense of the problem, consider just the scale of the housing bubble the Fed has inflated since the previous housing bubble that crashed in 2007-2010:

Federal Reserve Bank of St. Louis

Double in size! It makes the last housing bubble look like the foothills compared to the Himalayas. Obviously, the Fed learned absolutely nothing about the danger of inflating housing bubbles after the devastation it set up in housing that gave us the Great Recession. It chose to solve the problem of that collapsing bubble by deliberately inflating it to the highest level it could hit before pulling out the plug and collapsing it.

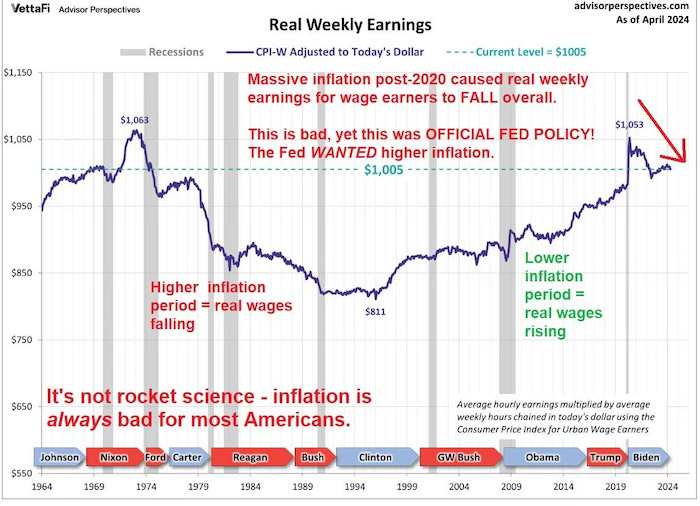

While prices have doubled, REAL incomes, on the other hand, haven’t gone up nearly enough to cover such outrageous inflation in home prices:

Inflation-adjusted wages have topped out right where they were over half a century ago! What went up, instead of wages, to make these home purchases possible was debt, made possible solely by extremely low mortgage rates, established by exceptionally low Federal-Reserve interest rates along with Fed QE over a period of time far more protracted than the period that set up the previous housing bubble (therefore made all the more dependent on those low mortgage rates):

Inflation-adjusted wages have topped out right where they were over half a century ago! What went up, instead of wages, to make these home purchases possible was debt, made possible solely by extremely low mortgage rates, established by exceptionally low Federal-Reserve interest rates along with Fed QE over a period of time far more protracted than the period that set up the previous housing bubble (therefore made all the more dependent on those low mortgage rates):

Federal Reserve Bank of St. Louis

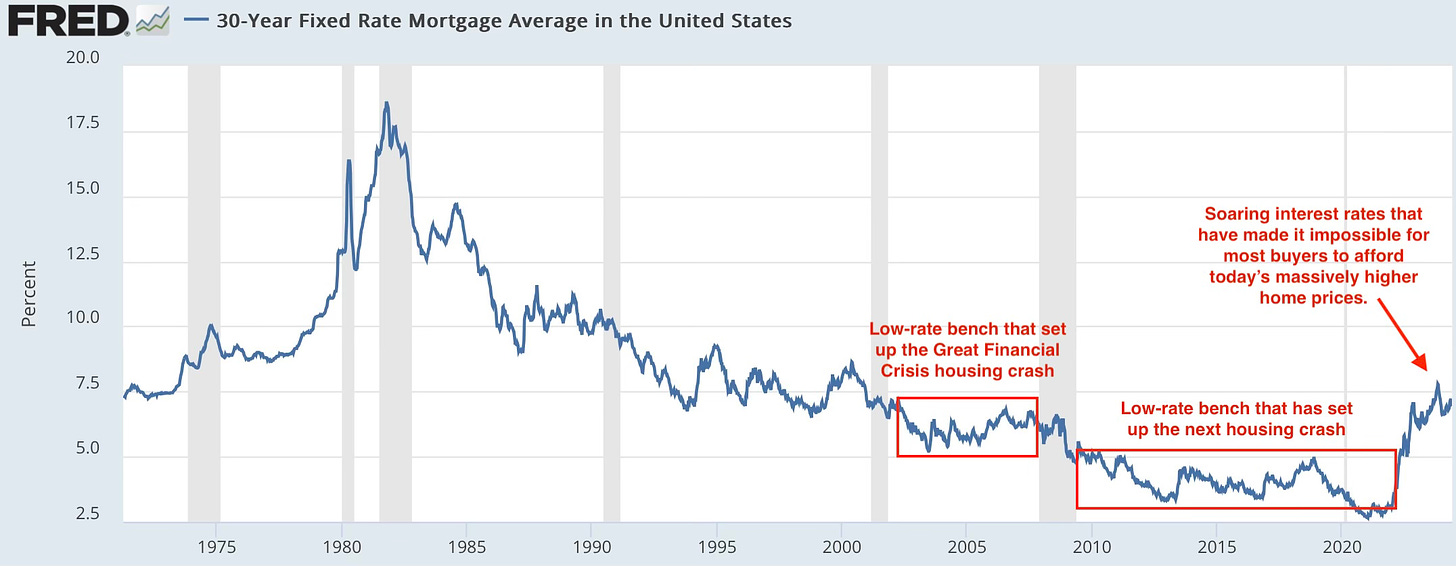

One thing distinguishes the peril of this bubble: There was no significant rise in mortgage rates before the last housing bubble’s crash. Look hard, and you’ll see that the final two years of that first lowered bench where rates sat for about six years barely rose higher than the early part of that period. The last bench of bubblicious mortgage rates, however, dropped by 50% compared to the previous level and were extended over a period more than double in length. Then they took an even deeper plunge at the end of that period because of the Covidcrisis, raising prices astronomically.

Mortgage rates now, however, are elevated far above that last period. We’ve not seen a period where mortgage rates went up as quickly as the Fed has just raised them since the double-dip recessions of the eighties. While mortgage rates are nowhere near as high as they rose to in the eighties, consider the fact that all current mortgages comprise far greater heaps of debt due to the massive rise in home prices. (Look at where the Case-Shiller index of housing prices (top graph) sat way back in the eighties before any bubbles had been inflated—only 14% as high as where recent prices have topped out.)

With real wages frozen at the same level they were back in the eighties, but housing prices many times higher and mortgage rates now soaring, is it any wonder that most buyers are frozen out of the market and most potential sellers are petrified from selling because they know what that means as soon as they become buyers at the new higher rates?

The one strength this bubble has against popping that the previous bubble did not have is that most of these loans are fixed-interest loans. Last time, a great many of the loans were adjustable-rate-mortgage time bombs (ARMs). So, IF people can weather the bad times of the next recession, the Fed’s rises in interest will not impact these loans.

On the other hand, there is a an absolutely massive amount of room to go underwater compared to any other time when housing prices do fall from their present Case-Shiller peak in values due to raised mortgage rates now making such lofty valuations impossible for most buyers. That’s why the housing market is frozen at the top. Essentially no one dares move down in price in order to sell their home because they could never afford to replace what they have at these raised interest rates.

For example: Suppose they bought their last home for $250,000 with next-to-nothing down on a mortgage with 2.8% interest (with no points), and they have paid the mortgage down to a balance of $150,000. Now, they sell the same home for $500,000, pocketing $300,000 after the pay-off of the mortgage and all closing costs, including broker fees. The next home they buy also costs, $500,000 plus closing costs to maybe come to $520,000. After deploying all the cash left from their sale, they have to finance $220,000, almost as much as they financed the first time. However, this time it comes at 7.5% interest (with no points). Their original payments (without property taxes, insurance, etc.) were $1,030 per month. Their new payments will be $1,530 per month, almost 50% more, and they are buying a house at the top of the market that they know will NOT appreciate like their last home did, likely leaving them underwater for a long time to come as the homes value falls. Moreover, the current market has very low inventory, greatly reducing their chances of finding anything they like.

So, the market is on ice.

The housing market is just an example of the bubble trouble we are now in; yet, it may be the most solid of all the bubbles because, so long as buyers and sellers remain in their frozen positions, people will not be impacted by the change in interest. For those who have to sell for personal reasons, such as a change in job location, however, there is a lot of peril.

All of these bubbles are now having the easy money that inflated them sucked away with the Fed’s quantitative tightening or are deprived of the cheap financing that enabled the sale of their bonds as the Fed raises rates. So, as those commercial bonds have to roll over, their collapse begins to unfold as we saw this week in the commercial mortgage-backed security default of 1740 Broadway where all tranches were completely wiped out, except the supposedly pristine AAA-rated tranche, and even that top tier got back only 74 cents on the dollar. (See: “Revealed: Major Economic Cracks and Crackpots.”)

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!