It all goes down in the same heap of rubble — zombie corporations and the junk bonds that are their sole life support and, piled on top, some of the banksters that funded them. Like a zombie apocalypse, it spreads around the world, taking out the weakest first but then the stronger players as the zombie horde grows.

Banking Busts

The fringe breakdowns are not just happening in the currencies of emerging markets and the defaulting of sovereign debts of those nations (as I discussed in Part 2 of this series). Neither are they limited to the newest frontier on the periphery of finance — crypto currencies and their banks where we have already seen major wreckage (as I discussed in Part 3, available only to my Patrons). They are also starting to show up in junk bonds where financing has suddenly run dry (something I said was coming and explained in detail in a much earlier Patron Post, but will now lay out here for all).

Unsurprisingly, the first banks to bust were some of the new crypto banks or crypto loan companies that got flushed. Next to go will be the weakest zombie corporations (as I also warned of in an even earlier Patron Post but am now mentioning for all as we near the actual event). In fact, just posted an article in “The Daily Doom” this morning about how zombie financing is now drying up quickly.

That article notes that banks are now rapidly tightening lending standards due to the deteriorating economic outlook and high inflation that were the overarching themes of all of those Patron Posts that I’ll now share from — inflation being in the driver’s seat of this particular crackup because it is driving the Fed to tighten right into a recession. Says, the article,

It would be shocking if this wasn’t happening…. This is part of a process by which lower quality borrowers and zombie corporations are getting cut off from their sources of funding. We recently noted that junk bond issuance was grinding to a halt and IPOs have also all but stopped…. Given how much of the economy has been zombified by a decade of excessively accommodative monetary policy, don’t under-estimate the effects that this will have down the road.

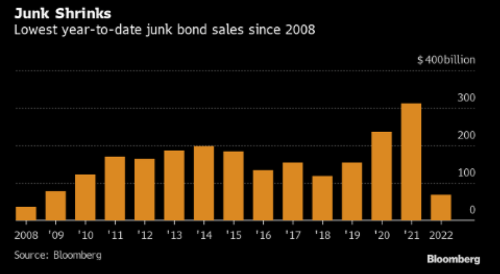

With new junk issuance drying up to less than a third of last year’s level as of this time of the year, just as those earlier Patron Posts warned would be coming, refinancing will fail those corporations, and they’ll sink quickly. As you can see, the last time that looked this bad was in 2008 as we plunged headlong into our nation’s worst banking crisis.

No one wants to bet on highly speculative enterprises once psychology shifts from making huge gains to financial preservation. That requires a rise in yields in order to attract buyers into this ugly junk market. The following is the explanation I gave in one of the Patron Posts as to how this rapidly turns into a total blowup:

The corporate bond market essentially has two buckets of bonds — investment grade and high-yield (junk) bonds. Many kinds of institutions and investment products are only allowed to buy investment grade. When bond yields rise, numerous companies whose bonds were in the investment-grade bucket because they could easily pay off or roll over their bonds at low interest get rerated into the junk bucket when interest rises above their means to cover.

When the credit rerating happens, all the institutions or investment products that are required to buy only investment-grade are forced to sell all those bonds. You can see that, if the entire bond market suddenly has a repricing that has nothing to do with the quality of companies and what the economy is doing to them (where repricing is individual), but with central-bank unified actions that reprice the full market, many companies that could easily pay off their bonds in the present ultra-low interest environment will get rerated into the high-yield bucket, forcing the institutional sale of those bonds. That huge supply being forced onto the market will lower the price of those bonds to attract buyers from a much smaller buyer pool now that they are in the junk bucket from which far fewer buyers are allowed to participate, forcing yields higher still. Sudden credit downgrades become their own cascade in the nuclear fusion of this supernova event.

“The Everything Bubble Bust Pt. 3: The Big Bond Blowup“

While average junk-bond yields recently settled a little to 7.29% as of August 10, that is still substantially higher than the 4.42% received at the start of the year. When the Fed doubles its pace of bond roll-offs next month, as it continues to pressure interest rates up higher from the bottom by raising its Fed Funds Rate, I expect yields to rise to an even higher level.

At the margin, rising interest rates may make it more difficult for some bond issuers to cover their debt, especially those with maturing bonds that need to refinance, said Matthew Gelfand, a CFP and executive director of Tricolor Capital Advisors in Bethesda, Maryland. “I think that investors and lenders will demand somewhat higher rates as a result,” he said, noting that rising interest rates may continue for a while.

In Europe, the bond cascade has already begun due to inflation exacerbated by sanctions driving up bond yields.

I also warned,

The collapse of the Everything Bubble will be an economic supernova. Think Lehman Bros. and Bear Stearns and all the rest of what happened to cause the great recession, then raise it an order of magnitude

“The Everything Bubble Bust Pt. 3: The Big Bond Blowup“

As you can see from the chart above, we have moved into a situation that looks very much like the junk-bond collapse that happened in 2008, but we are still waiting for our Lehman moment … as we were through the first half of ’08 when we had no idea such a moment was coming until it leaped out of the bushes and mugged us. I imagine that’s how it will happen this time. No one in the media will pay much attention to the small zombie companies that are falling away already; but then, on some ordinary day in the year ahead, a major company like a bank where the many little troubles have aggregated will reveal its own bad condition and jerk everyone to attention.

The Dimon on my shoulder

The concern of major banks could be heard earlier this year in the howling of a lone loan banker screaming from the top of his tower. That would be Jamie Dimon, who went from fair-weather Jamie at the start of the year to Hurricane Dimon in a hurry and who has been spinning like a tin weathervane in the wind ever since. Most of the rest of his colleagues remained silent, so they must have been deluded enough not to see the storm clouds coming that Dimon suddenly saw or too scared to mention it, lest they flush their own bank vaults by creating panic. Dimon, however, was ringing some pretty loud alarms about what was right on the horizon.

Dimon’s shift from sunny skies to hurricanes in the space of a few months shows how quickly things turned as inflation heated up and forced the inflation-ignorant Fed to cool off more quickly than most anticipated, including the Fed. At the time when I wrote the above articles, Dimon was still in Sunnyland — “strongest economy ever” and all that stuff. What turned him upside down was the quick pace at which the Fed suddenly decided it needed to offload mortgage-backed securities and treasuries from its balance sheet, pressuring this bursting bond bubble because the Fed is effectively dumping bond supply into the market by not refinancing it so that the debt slaves have to find funders willing to carry them without that Fed backing. The oversupply drives down bond prices, which pushes up yields, raising the costs particularly for zombie companies. Dimon was concerned the Fed’s faster-than-ever QT schedule would blow up the bond market.

Those who were with me in 2018 may recall how I said the Fed’s biggest impact on markets from its year of QT would not be felt until after September when it would bring its QT up to full speed. The same will be true this time when the Fed doubles down on its QT rate sometime in September. The Fed appears to as badly underestimate the impact of its QT now as it clearly did back then when it thought it would run on autopilot for a couple of years. It appears to have learned nothing … or it is just that pressed by inflation to tighten beyond any speed we have ever witnessed.

Dimon also recognized that, as soon as the Fed started sucking liquidity from bank reserves, which is what happens when it starts reducing its balance sheet, banks would start showing troubles just as they did in the Repocalypse. Once we get below a certain unclear level, Dimon & Co. will do exactly as they did last time and stop doing repo loans. Because JPM is the biggest source of such loans, interbank financing will seize up again, zombies will run dry of cash at a faster rate, and hedge funds will become imperiled all over again as they did in the Repocalypse.

Because it was Dimon’s JPM that hit the brakes on its willingness to keep playing in 2019 that sent us into the skid of the Repocalypse, I’m paying attention to the warnings he gives, even though he flip flops. If JPM, one of the world’s largest bond-market primary dealers, gets to the point where Dimon isn’t willing to keep playing the Fed’s bond game, big trouble can suddenly emerge somewhere in the financial markets.

The big bond bust

Of course, a disorderly bong market is the very kind of thing that could actually force Powell to pivot; but, as I noted in that Patron Post, it’s not so easy this time — not nearly as easy to go back into easing as it was to start quantitative easing the first time after the MBS bond blowup in ’08:

If you think the Fed will, as it has done throughout the lives of many investors, simply rush right in to buy corporate bonds to suck up all the slop or buy government bonds to stop the rise in rates that reprice other rates, remember why the Fed is taking all this risk in the first place: the Fed has a constitutional mandate in its charter to fight unstable inflation, so racing back in may require an act of congress to override its mandate (or the majority in congress to tacitly turn a blind eye to the outright illegality). CBs also have their own innate fears about inflation devaluing their sole proprietary product, which is their currency. So, think again

While a disorderly bond market will force Powell ultimately to reverse course, inflation is the sand in his gears that will slow his shifting down, and that means he’ll grind a few gears trying, and his shift into reverse will happen too late for the simple legal reason noted above. Imagine if he needs to make that shift at a time when congress, which will have to approve it, is dysfunctional! Oh, wait, it already is.

As another article I quoted within that Patron Post warned,

If rates rise rapidly, inflation pressures intensify, and fears trigger a selloff in the bond market, investors will experience significant market-value losses. Just a moderate interest rate increase could result in [bond] market losses dwarfing credit losses [defaults]—even if defaults reach highs consistent with a historic stress scenario, which would be much more severe than the credit issues experienced in the pandemic.

Just a little slowness in the Fed’s shift away from QT could have devastating consequences. Of course, the Fed created this problem for itself when it decided to go down the path of letting inflation rise because it was, after all, just “transitory.” Well, we’re well in transit now, and the Fed is not going to make its shift in any more timely a manner than it did in recognizing it needed to tighten against inflation. My view of the Fed’s plan has always been that it has no end game, so the Fed will trap itself to where it is damned if it does and damned if it don’t … and so are we along with the Fed since we all use its money and ride in the economy it is attempting to drive … in a manner that looks more than a little inebriated to me.

That kind of bond selloff in the Everything Bubble cascade happens like this:

An interest-rate shock [Hello? Developing now.] would cause mark-to market … losses in corporate-bond mutual funds, and those losses would pose contagion risks to other asset prices. Investors would react to falling prices—and to forward-looking projections of further declines—by redeeming their holdings. And because [bond] funds tend to hold relatively low levels of cash and near-cash instruments, they would be forced to sell into declining markets to meet these redemption requests…. Material selling could trigger further negative price migration, thus fueling further redemption requests and even lower liquidity among the remaining assets.

Dawn of the zombie apocalypse

As we see the new issuance of junk-bond debt falling to a 2008 low, we know that those companies that are staying alive (zombie corporations) only by managing to cover their bond interest until they can refinance the principle will be unable to refinance when the time comes. I went into great detail about the ins and outs the Bond Bubble Bust and the circuit breakers that would likely try to prevent this cascade and how they would fail in that Patron Post quoted above, but in the other Patron Post I focused on this problem of the zombie corporations because “I found that one part of the bond bubble is sooo big it may be a bubble within a bubble.”

The bursting bond bubble may include a zombie apocalypse…

The number of zombie firms in a nation rises as a “share” (or percentage) of total corporations whenever credit grows cheap. Zombies, of course, tend to fall into the “junk bond” category of credit. When interest rises, some of these firms die off because they cannot afford to refinance their debt when their bonds mature, while they have made little to no progress at paying it down because all their income can cover is the interest on their debt….

“The Everything Bubble Bust Pt. 2: Zombie Apocalypse“

Dr. Agustin Carstens, head of the BIS

Dr. Agustin Carstens, head of the BIS

Speaking of big bankers, The Bank for International Settlements (BIS), I noted, appropriately run by the world’s most bloated bankster, had expressed concern about the threat posed by these zombie corporations, even as the Fed tried to downplay it.

It may be the Fed, in downplaying the whole thing, is playing the same game it did when convincing itself and the nation that inflation was not a prominent feature of the new U.S. recovery it had created, so not something it had to deal with. Perhaps it would like to dodge responsibility for setting up a zombie apocalypse like it tried to dodge the inflation inferno it helped set up.

I did not feel inclined to let the Fed off easily with its diminishment of the prospects for a zombie apocalypse. In fact, I believed the Fed’s blindness to inflation was the very blindness that would cause it not to see the zombie apocalypse coming either:

While the Fed brought up the concern that their cheap finance may cause a rise in zombie firms, the number of zombie firms has also been found to rise during periods of high inflation because businesses with tight margins struggle more to survive.…

During high inflation, most businesses try to absorb some of the producer costs of inflation and not pass them on in order to maintain market share. Zombie companies, because they have razor-thin profit margins (if any at all), are the least able to do this and so are more likely to lose market share by having to raise their prices above their competitors. Similarly, zombie corporations are more likely to go bankrupt during times of declining GDP.

The Fed wrote its argument diminishing the buildup of zombie corporations well before it saw inflation coming as a problem. So, the build-up the Fed didn’t see happening in its study of zombie corporations in America prior to our soaring inflation could easily have built up during the inflation period it also didn’t see happening. That would be the Fed’s blindspot. Having already determined there was no zombie problem for it to be concerned about, it certainly wouldn’t be looking for that problem to emerge during a period of inflation it didn’t even acknowledge was happening as anything more than an inconsequential transitory problem. These blind spots of the nation’s central planners may slay us all.

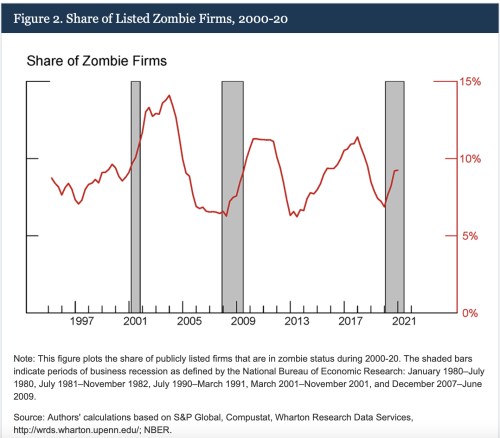

At the time of the Fed’s counting of US zombie corporations, the Fed’s count looked like this:

But the Fed’s assessment and its conclusion that we were safe was completed at the start of the Covidcrisis when the Fed was worrying a bit about what all its super-funding might do. What do you want to bet the number of such corporations became even bigger? The total number of zombies was already higher than it was in 2008 and about equal to where it was at the start of the dot-com bust. More cheap Fed funds mean inevitably more companies stayed alive using the nearly free funding … and even then could barely pay the pitifully low interest.

The Fed concluded all was safe because …

The share of listed firms that we identify as zombies displays a cyclical pattern, rising in recessions and falling during expansions, likely reflecting a mix of aggregate and industry-specific shocks.

In other words, it had nothing to do with their easy funding, so nothing to see here folks.

The BIS differed. So did I, noting…

The other thing cyclical about [the Fed’s] graphs is that the zombies rise and fall inversely with the Fed interest rates that rise and fall during times of expansion and recessions, and that the Fed is largely responsible for creating these “business cycles” anyway by raising rates until it creates a recession, then lowering them throughout the recession until it helps foster a recovery to the recession it created (by its own admission from those at the top). Other institutions present a much sicker zombie picture than the Fed.

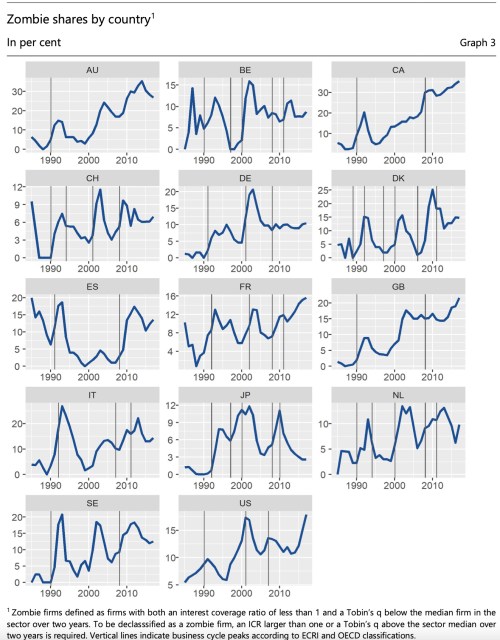

And that is where the BIS weighed in. They showed a graph for the US (bottom right in the image below) that presented a MUCH different picture for the number of zombies (something not apparently that easy to count, given there are conflicting methodologies involved based on definitions of a zombie:

According to that graph, the number of US zombies has never been higher!

My take on that presentation, and the BIS’ take as well was:

This is a global problem caused by the US Federal Reserve, the Bank of England, the Bank of Japan, the People’s Bank of China, and the European Central Bank (for the European nations shown). There is an upward trend almost across the entire board with each new cycle of zombies getting worse as each new QE/bailout cycle by central banks has gotten bigger!

We’ve let a lot of dead wood pile up in this forest, and that tinder in times of business drought can imperil the entire forest.

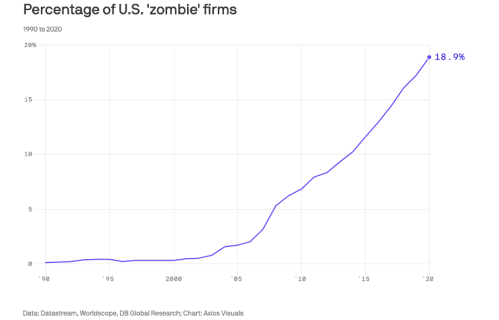

Another firm, I noted, presented an image of US zombie corporations that looked even worse:

It turns out you can cherry-pick your zombies. In defining a “zombie,” you might include, for example, how much of an interest rise would it take to club them over the head and kill them off. It also depends on what sources of information the study uses and what kinds of data the studiers choose to include.

Even the Federal Reserve in its study said,

There is no formal definition of a zombie firm, but it is generally agreed that these firms are economically unviable and manage to survive by tapping banks and capital markets.

And the BIS says,

Given the novelty of our zombie definition, we assess the robustness of our results with respect to variations in the specification of our zombie definition and with respect to alternative zombie definitions used in the literature.

Based on their definition, they conclude …

that the number of zombie firms has on average risen significantly since the 1980s across the 14 advanced economies covered by our analysis.

… and that, yes, it is a problem, and potentially a big one. It is a problem that has grown worse with each of the major busts in 2000 and 2008.

My summation:

2022 will be a much different kind of fire season for this tinder-filled forest with higher and drier winds financially. Moreover, we may have actually piled in new zombie corporations during 2021 that were carried along by all those CB relief programs and dirt-cheap credit. But there are no data for that, so it’s a guess for all of us as to what is out there.

“The Everything Bubble Bust Pt. 2: Zombie Apocalypse“

Most zombies typically get their heads blown off within three years of hitting zombie status (depending, of course, on how tightly you define that). If you go by the broadest graph above, that could mean 20% of the corporations in America vaporize if credit costs rise. Now, worst-case scenarios may not be the most likely ones, and the Fed will likely pivot somewhere in that phase, if it reaches systemic crisis, with more rescue packages; but that will be because the economy is in free-fall by that point because the Fed will have to wait until it can forge some sort of credible argument that says “we have inflation under control.” Of course, the cost of a pivot back to major QE will be a return to soaring inflation that, at that point, could finally become hyperinflation. The Fed will be forced to decide whether to bail out all the failing zombies and pile on inflation or let them all die and let the corporate forest go up in flames because of all the tinder their bailout policies have built up over the years.

The latter would be the better route, of course, because with the deadwood cleared out, there would, at least, be room for new growth down the road. With the old wood left and scorched, the forest that is left will be weaker and diseased for years to come. However, when has the Fed allowed the inevitably grim reaping forces of capitalism to destroy bad investments if the problems become systemic?

Either way, we have major economic problems left over, so the discussion as to whether the Fed will pivot is an academic interest because either path is rife with destruction at this point. Letting things run their natural course means economic ruin we have to rebuild from. Bailing things out again with more free Fed funds, just piles the tinder higher and increases the spread of disease harbored in dead wood while scorching us all with even hotter inflation for years to come. (Remember, there never was an end game for the Fed’s Great Recovery schemes.)

The BIS notes that the relapse rate for zombies that recovered because they were bailed out or via bankruptcy has been climbing, too. So, saving the dead wood has not made a healthy forest. The zombie disease seems to cause long-term damage also on those that recover from it. The weakness and risks in advanced economy corporate sectors may therefore not be fully captured by headline figures…. With respect to the causes, our analysis suggests that zombies often emerge in the wake of business cycle downturns and financial crises.

This time around, central banks cannot so readily run to rescue the zombies as they have in the past due to inflation; so, the situation is far more likely to become disorderly because of all the times we “kicked the can down the road,” as John Boehner liked to say about all of congress’s approved rescue plans … some of which he voted for because no one wanted to face the pain. We chose to deal with greater pain in the future, and the future is now.

Says, the BIS,

With respect to the wider consequences of zombie firms, our findings point to a growing army of enfeebled recovered zombies who underperform compared to healthy firms as a so far unrecognised consequence of the rise of zombie firms over the past three decades.

The company that posted the highest zombie chart above says,

In the US zombie companies are estimated to control 2.2 million jobs and have built up $2 trillion of debt over the pandemic, nearly $500 billion higher than the peak of the Great Recession. These are not just small firms either, with an analysis by Deutsche Bank Securities identifying nearly one in every five publicly traded U.S. companies as a zombie, double the number in 2013. They include iconic brands such as Macy’s, Boeing, Carnival, Delta Air Lines, Exxon Mobil and Marriott International.

With the huge reduction in zombie (junk bond) financing showing in the first graph above, meaning a likely huge reduction in the refinancing of zombies, the time has come to face the music. I believe, as one of my predictions for the remainder of 2022, we will now start to see the number of these zombie fails rise significantly in the latter half of the year, though I don’t think it will become a major problem, taking down some of the bigger-name corporations, until next year.

Letting the zombies burn is the price that has to be paid if we are ever going to return to a vibrant economy. Said one corporate restructuring specialist,

The combination of the long-term build up of these zombies and the turning off of support measures, which is going to have to happen, will finally mean that we start seeing a number of these businesses begin to fail, and in quite significant numbers…. If better businesses are able to come into the spaces they [zombie businesses] occupied and do things more imaginatively and flexibly, they will not only survive but adapt and prosper going forward…. Although it means a bit of pain in the short term, it’s the price to be paid for a more efficient economy and a sharper recovery curve going forward.

“The Everything Bubble Bust Pt. 2: Zombie Apocalypse“

Of course, corporations going bust means more downside ahead for the major stock averages that contain those corporations that will eventually get hosed for pennies on the dollar.

As Bill Blain, a big investment banker highly involved in hedge funds and private debt and corporate bonds, observed,

Corporate debt is likely to crack on rising rates, price distortion, forgotten risk metrics, and rising defaults. It will signal the perilous financial health of some sectors – bursting the current bubble violently.…

The reason we are in for trouble is that large parts of the markets now implicitly believe companies don’t go bust – because for the last 12 years of monetary experimentation, distortion and insanely low interest rates have kept all those companies that should have failed and tumbled into default… sort of solvent….As companies haven’t been going bust at normal rates since 2008….

When a bond crash comes the market will set like concrete.…Corporate defaults are going to rise. That’s simple logic

And back to the big banking bust

Where things set like concrete in the world of finance is in banks.

The section above just describes the zombie part of the bursting bond bubble — the bubble within the bubble. The bigger question is what the knock-on effects of those fails will be to the full world of finance.

This is more than just about the zombies that go out of business with the impact they have on the stock market, the jobs market and other aspects of the economy. It’s about more than the loss of wealth for the average investor or some crashed bond funds. It is also about what so many defaults do to banks.

“The Everything Bubble Bust Pt. 3: The Big Bond Blowup“

How heavily invested are banks in some of those corporations? What will the loss of those jobs do to the overall economy, causing it to take another leg down, resulting in the additional loss of jobs in companies that are not zombies but must restructure to the lowered business climate that happens when more people go jobless who did work for zombies?

One of the other really big global banks, the International Monetary Fund, estimated there is about $19 trillion in outstanding zombie debt globally. In nations where companies make their money in a national currency that is falling against the dollar but are financed in US-issued bonds, that means big trouble. However, we’re also seeing trouble emerge now right here at home:

The average price of U.S. high-yield bonds fell as much as 16% between January and early July, according to the ICE BofA U.S. High Yield Index. With interest rates rising and the world heading for recession, it’s unlikely that banks will claw back all of the losses.

Leveraged-finance bankers are nursing a headache after one hell of a party. Bank of America (BAC), JPMorgan (JPM), Goldman Sachs (GS), Morgan Stanley (MS), Credit Suisse (CS) and Deutsche Bank (DB) collectively took about $1.5 billion of writedowns in the second quarter on loans they made to highly indebted companies.

It’s just a headache so far; but, as you can see, big banksters are in for their share of the hits because they do have exposure. The zombie horde has grown, and so, likely, has the exposure of banks all over the world. At the same time, the huge 50% decline in mortgage applications this year due to Fed hikes is already causing some of the weaker lending institutions to go broke for reasons having nothing to do with the zombies, and you can be sure it is stressing many stronger banks. What will happen if the Fed piles stress on stress by tightening to the point of causing another Repocalypse, as it did in 2019 when JPMorgan stopped working with hedge funds, causing internal banking credit streams dry up again?

One banking venture, First Guaranty where PIMCO, a huge financial institution, is the majority owner, just declared bankruptcy due to the mortgage situation. Other major firms like PIMCO almost certainly have similar exposures. The question will be which big firms are just weak enough and have exposure to enough failing mortgage ventures plus failing zombies that the big firm will wind up in serious trouble? Can’t happen like Lehman couldn’t happen, right?

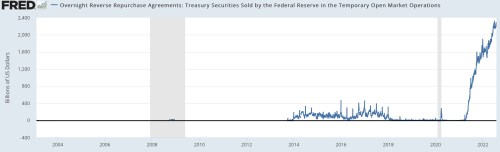

The Fed appears to have pumped a lot of slack into the system, but no one has ever seen how this kind of slack plays out either. The Fed stacked in a tremendous amount of the exact opposite of repo loans — reverse repo loans, whereby it took excess cash out of bank reserves and replaced it with bonds as collateral. I noted last year that the Fed was taking money out the back door almost as quickly as its continuous QE was creating it. It had to do this because there was too much cash sloshing around from all the Fed’s excess liquidity, leaving me to wonder why they were even creating so much liquidity that they had to remove it in this clandestine fashion. I suggested maybe they were banking it as slack for when they started to tighten, should the need it. That money taken out of bank reserves on loan that can go immediately back has piled up like this:

St. Louis Federal Reserve Bank

St. Louis Federal Reserve Bank

Theoretically, banks could stop rolling those over and get cash back from the Fed as a buffer for the Fed’s tightening, just as this appeared to be a way for the Fed to sop up the slop from its excess creation of reserves during the recent QE period. I’ll note that, as the Fed tapered its QE and barely started to roll that off its books, these reverse repos also appear to have started tapering off, perhaps creating some slack for the tightening.

Whatever line of future defense this historical massive pile of reverse repos may be intended to provide, Jamie Dimon still sounded plenty worried with his original overnight flip from sunny skies as far as the eye can see to hurricane warnings (from which he recently halfway re-flipped). Should there be any banks that did not have the foresight to lay in a lot of reverse repos as loans to the Fed in exchange for bonds as collateral when they had too much cash, I would think those might be the first banks to falter during this new QT phase. As you can see from the graph, we’re in uncharted territory. Here’s a view over a wider expanse of time to make clear what this reverse-repo anomaly looks like by historic comparison:

I have no idea whether that stack of cards tumbles during the Great Unwind, or if it provides some sort of buffer against another Repocalypse (being the opposite kind of transaction), but let’s keep an eye on it. I suspect it mostly helps avert another repo crisis … if it is utilized as I think must be intended. The risk I see here is that, to the extent banks reverse the reverse repos to rebuild their reserves, QT will be slow to tighten down on inflation. The pile means there are still Fed money sources squirreled away that can rapidly backflow into reserves.

Even if CBs rapidly retreat [from QT] to avoid the global supernova above, you’ll know how bad it would have been by 1) the scale of the recovery effort they make to stop it from getting worse and 2) by how bad it ends up even after their massive recovery efforts.

Complexity adds to risk. It doesn’t diminish it. It means there are more unforeseen flight paths along which a single black swan like Lehman can swoop down. So, I’m sure no one can predict how all this complexity on such a grand scale falls apart in any specific ways; but one can certainly see that untried complexity is piled higher than ever before. I doubt even the Fed knows if it will work as a buffer, but I’m willing to say such a massive house of reverse-repo cards is not likely to come down without creating some unanticipated troubles of its own. So, I’ll try to keep my eye on it, as it as a new kind of problem likely to emerge in the backchannels of banking.

The biggest risk in banking is a crisis of confidence in central banks. As society sees how badly they failed us, we can go from bank runs to currency runs. Smaller nations will start to enter that phase soon and maybe even larger ones like China, which has already seen some of that kind of trouble. While this is too messy and complex to have any idea how it will play out, the combination of more zombies than ever likely defaulting and financial institutions with such odd positions banked along with the huge decline in mortgage business plus stock-investment losses adds up to a lot of potential for banking chaos that could exceed the crisis-management abilities of central banks.

It’s a situation like we saw early on with inflation where I said back in 2020, keep your eye on it. “Thar be dragons.” I’ll track it, and try to figure it out for my Patrons as things develop, but will provide some warning as I just did here, even for those who don’t or can’t support my writing, as that is what the patronage is really all about — making it possible for me to focus on this for the good of as many as possible. There may not be much you can do to protect yourself from something this systemic — not even the old standby of precious metals (rigged by the likes of Dimon & Co) or cash (utterly controlled by the likes of Dimon & Co.) — but I’d rather see it coming than not. I can try to create good navigational charts, but I can’t plot the best routes for you as everything depends on the vessel you’re operating, your own skill in managing currents and rough seas and what channels your vessel can take based on its draft and where you need to shelter from the storm and where you want to go from there when the storm finally settles. I’m just a weatherman and chart maker, laying out the troubles ahead.

Liked it? Take a second to support David Haggith on Patreon!

https://thegreatrecession.info/blog/economic-predictions-h2-2022-bond-busts/

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!