We have a few stories that demonstrate the usual fakery in financial media that supports the common greed in the marketplace. First off, CNBC wanted to milk a little optimism out of the just-released housing data and ran a story saying “Mortgage demand JUMPS 10%.” (Emphasis mine.) That happened in spite of the fact that mortgage interest eked up.

“The increase in purchase and refinance applications for both conventional and government loans is promising to start the year but was likely due to some catch-up in activity after the holiday season and year-end rate declines,” said Joel Kan, an MBA economist, in a release. “Mortgage rates and applications have been volatile in recent weeks and overall activity remains low.”

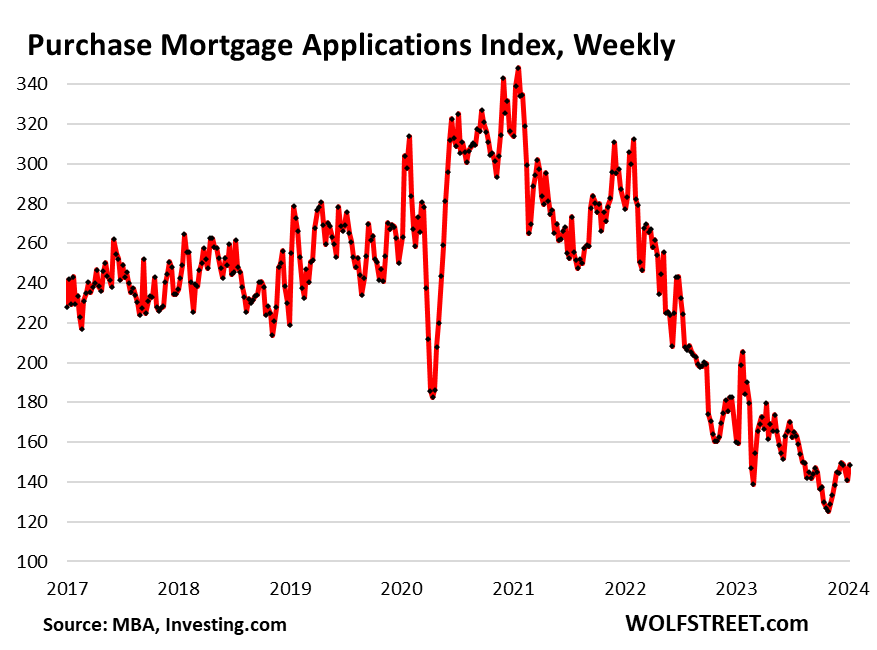

Well, yeah. The word “jump” is a little too high. Fortunately, we have analysis from Wolf Richter of this same story to put some perspective on it. As Wolf notes, that JUMP was just a little less than the SLUMP into which mortgage demand fell the week before. They merely jumped the slump and not even quite that:

Hype in the media about real estate going to the moon or whatever is a never-ending drama. For example, on CNBC this morning, we read this headline: “Mortgage demand jumps nearly 10% to start the year, even as interest rates tick up again.” Which was a joke?

This was in response to data by the Mortgage Bankers Association today that mortgage applications to purchase a home during the week ended January 5th had risen by 6% from the prior week, seasonally adjusted. But in that prior week, applications had plunged from the week before the holidays, and so today’s reading didn’t even go back to where it had been two readings ago, and was down from the same week in:

2023: -16%

2022: -48%

2021: -56%

2019: -42%

So, the “jump” looks like this:

Wolf Street

See that little wiggle at the tail end there? That was the “jump.” Thank God! The three-year collapse in sales must be ending in a pre-spring thaw!

Zero Hedge drinks and serves the hogwash again

Zero Hedge is doing the same thing again with the Fed pivot in an article titled “Why The Fed Capitulated,” as if that actually happened. How do you “capitulate” on policy when you didn’t change policy one iota? We already know the idea of interest rate cuts in March is a rapidly fleeing fantasy; and, if we see inflation stage a comeback, as I am continuing to predict for 2024, then that fantasy gets pushed back even further!

As another article recently warns,

Thursday’s inflation report could challenge the market outlook for big Fed rate cuts

Economists expect that inflation nudged higher in December, a trend that could call into question the market’s eager anticipation that the Federal Reserve will slash interest rates this year.

So, even the market-pumping CNBC gets it better than ZH. No pivot. No capitulation. And maybe a return of that inflation, as I’ve said we were seeing hints of—hints that will become clear reality in the months ahead, especially in YoY inflation once the “base effect” begins to fade from months back when inflation was very high, before the Fed had achieved much in the way of progress.

Oops. I spoke too soon. CNBC, after almost getting it right, partially stumbles back into the same camp as ZH:

At a time when the Fed is fighting inflation through tight monetary policy including elevated rates, news that prices are holding at high levels could be enough to disrupt already fragile markets.

So far so good, but …

“The Fed did its policy pivot, and the data’s got to support that pivot,” said Jack McIntyre, portfolio manager at Brandywine Global Investment Management. “The market seems to have gotten excited that the Fed’s going to have to do more than what the Fed thinks in terms of rate cuts now. ... The market got ahead of itself.”

The Fed did its policy pivot? When did that change in policy happen? Policy continues to hold high for longer. The Fed said nothing definitive about even lower interest rates later in the year. Yet, here we are with the market mongers talking as if the pivot has already happened! The truth would be that the inflation data coming out tomorrow has to support the FANTASY that the market has believed in if the fantasy is going to find any more run time. If it doesn’t, it will likely be another round lost for the idiot Pivotheads.

And, no, the market did not get excited that “the Fed’s going to have to do more than what the Fed thinks.” The Fed never thought what Mr. McIntyre or the rest of the market thought it thought. The market got excited thinking the Fed is going to do more in rate cuts than the Fed ever even suggested.

So, depending on how CPI comes in on Thursday, there may be a little rethinking among the market maniacs.

After months of insisting that easier monetary policy is still a ways off, central bank policymakers in December penciled in three quarter-percentage point rate cuts by the end of 2024, effectively a policy pivot for this inflation-fighting era.

No they did not. These deluded liars can’t think past the end of their forked tongues because they go on to note …

Minutes from that meeting released last week did not indicate any discussion about a timetable for the reductions.

They did not indicate any discussion about a timetable for reductions because they did not even say there would be reductions! They did not “pencil in” three quarter-percentage-point rate cuts either. They penciled in little dots that show their GUESSES of where rates might go, but those guesses barely got discussed and certainly not in a way that was a discussion on policy. They even stated in their minutes about what little discussion they did have that they were “very uncertain” about which way inflation and policy will go from here — far from capitulating on policy.

My prediction, of course, is that inflation will keep holding the Fed’s feet to the fire awhile longer. I’m not looking for a big rise in inflation, but enough to keep the Fed in the fight.

Markets hold a different view.

Yes, because they are not too bright and are riddled with greed, seeking a narrative that will fulfill their greed. It is the markets that will capitulate to Fed policy. Here is how full of lunatics the markets are:

Traders in the fed funds futures market are pointing to a strong chance of an initial rate cut in March, to be followed by five more reductions through the year that would take the benchmark overnight borrowing rate down to a range of 3.75%-4%, according to the CME Group’s FedWatch gauge.

These same people are all spouting “soft landing,” too. Do they not realize that the only way the Fed would ever, EVER think of making six rate cuts in a year would be if we were diving deep into a recession? Six rate cuts is a panicked Fed. Why would they do that if the landing is as soft as the lunatic stock and bond markets believe? They will do it if things break up badly enough. Or I should say “when they break up badly enough.”

So, this is “have your cake and eat it, too” fantasy: “We’re going to have no recession, and the Fed, having just fought a fierce battle against inflation that still isn’t over, is going to do six panic rate cuts this year for no necessary reason other than to be nice!”

Good luck with that wish.

You just have to wonder where people’s brains are.

In fact, the market has likely assured itself of more rate hikes or certainly of delayed cuts just because of its euphoric rise:

Fed Governor Michelle Bowman said this week that while she expects rate hikes could be done, she doesn’t see the case yet for cuts. Likewise, Dallas Fed President Lorie Logan, in more pointed remarks directed at inflation, said Saturday that the easing in financial conditions, such as 2023′s powerful stock market rally and a late-year slide in Treasury yields, raise the specter that inflation could see a resurgence.

So, the Fed is talking back to markets now that Powell’s relaxed tones, which came right when the markets needed to be brought up short, have undone a lot of the work that Powell said the market was doing for the Fed (which was what gave him cause to sound a little softer in the first place). He undid himself:

“If we don’t maintain sufficiently tight financial conditions, there is a risk that inflation will pick back up and reverse the progress we’ve made,” Logan said. “In light of the easing in financial conditions in recent months, we shouldn’t take the possibility of another rate increase off the table just yet.”

The false profits of the profiteers

Finally, Charles Hugh Smith gives a nice recap of the argument I raised in a previous editorial about how a lot of inflation is just profit gouging for the sake of supporting those high and mighty stock buybacks that enrich the already rich.

The profits are real, but the way they are made is rigged through fake inflation. They are profits made on false pretenses. They are profits that aren’t made honestly from hard work or good products, but profits made by misleading people into believing you must lower quality or reduce quantity in order to compensate for higher costs just so you can make more money off your inferior products. And, while the inflation is real for the customer, the need for so much price inflation—the claims that it is all necessary due to higher corporate costs—is a lot of fakery. You’re not really running a more profitable company; you’re running a more profitable con game.

The other source of sharply higher corporate profits is shrinkflation, the relentless reduction in the quantity of product in the packaging. One wonders how thin the can of tuna will eventually be--the thickness of a pancake? Or how thin can they make the box of cereal before the container can no longer stand upright?

The reduction of the quality of goods and services, a.k.a. crapification, is a key source of soaring corporate profits. As the unhappy buyer of three replacement appliances this year alone, all replacements for failed name-brand appliances that lasted 7 years or less--I can attest that crapification / planned obsolescence is a core source of higher profits.

Design the product to fail, or default to the lowest cost components, i.e. failure by default, and consumers are forced to replace appliances every few years that once routinely lasted decades. This conveyor belt of products to the Landfill is highly profitable….

No wonder Corporate America added $1.2 trillion in profits to be distributed to the elites of America: everything is diminished, stripped of quality and rendered miserable. Too bad there's no real competition left in the US economy.

It’s all greed that gets tucked away in inflation. And these bloated profits of the profiteers get handed down to themselves by using the company cash pile to buy back stocks — sometimes even their own stocks in non-public sales when they want to cash out just before the bad times come.

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!