The Fed is going to tighten an already tight labor market by making sure more of those workers who are already too-few in number are laid off in order to reduce production that was already lower this year than last year in order to lower prices that are too high because of production shortages.

If that makes sense to you, the Fed is your friend.

Where we’re going or where we are?

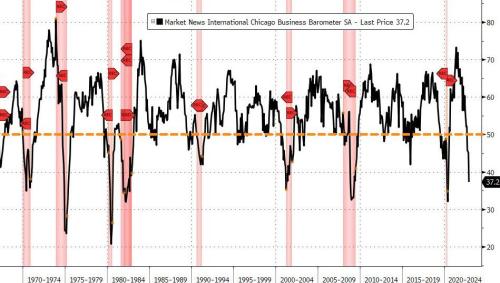

And, if you are a friend of the Fed, you will be among the many who believe we are not yet in a recession, even though the Chicago Purchasing Managers’ Index (PMI) has never been this low without ALREADY BEING IN a recession — often months into a recession:

OK, in the dot-com bust at the end of 2000 we were about a month shy of being in the declared recession when the PMI hit this level. But all other recessions were solidly in the red before this barometer hit this low level. However, I’ve been barking up this tree all year, and all I have to show for it so far is a mouthful of bark. So, go ahead and believe we’re not already in a recession, in spite of those two quarters of negative GDP earlier this year if you want.

And then you’ll be a friend of the Fed.

Before you do though, even Zero Hedge says this PMI level “screams recession“:

In 55 years, this level of Chicago PMI has never not failed to coincide with a recession.

I’m not sure what “never not failed” means, but I think what they really meant was “a reading this low has never failed to coincide with a recession.” Indeed, the graph shows the two always arrive hand-in-hand, but with recession leading the way, with the exception of that one time at the end of 2000 when recession slipped one shoulder in the door ahead of PMI. Not surprisingly, this recent reading was considerably lower than all twenty-five economists who were surveyed thought it would be. Economists rarely see a recession coming until it’s already half over.

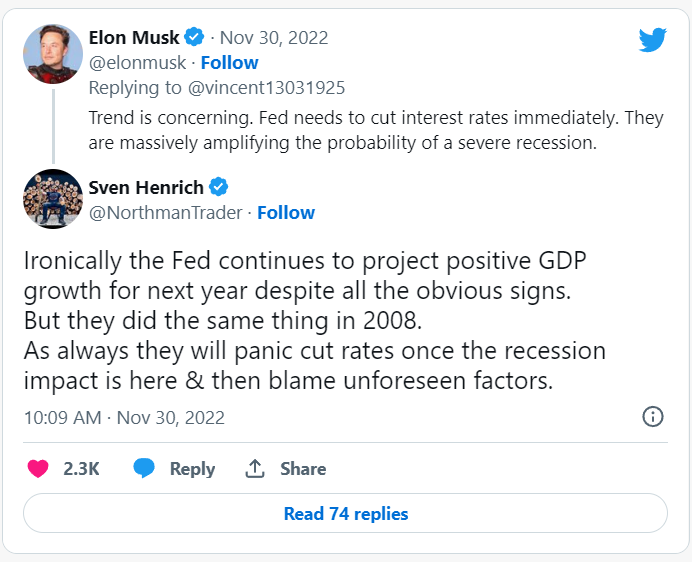

Elon Musk says the Fed must cut rates ‘immediately’ to stop a massively amplified severe recession:

Recessions do tend to become amplified when you are rapidly raising interest rates after you are already in the recession. And I see Sven Henrich, whose work I always respect and oft’ quote, feels the same way I do about the track record of the Fed’s economists when it comes to seeing a recession (negative GDP growth) before it gets here. He even lays out the reason I’ve given for making my predictions — because I know the Fed will say, “No one could have seen this coming” (“unforeseen factors”), so I like to show in advance that the factors have been seen.

Even if you are friend to the Fed, the Fed is not your friend

The Fed took the governor off the economic engine and ran with the accelerator hammered to the floor through months of this “transitory inflation” as inflation’s momentum was building, and now YOU’RE paying the price for that reckless abandon of sense every day. Now they’re going to do the same thing with the brakes, hitting them hard and slamming the transmission into reverse right after running into the wall. When it comes to driving skills, these guys should never be allowed anywhere near a tricycle, let alone behind the steering wheel of a eighteen-wheeler.

Don’t worry, though, because the recession they already created will be as transitory as your life. And, while you might lose your livelihood, they will certainly keep theirs. They always do. No reason the perps should pay, nor the financial pervs who seem to thrive on your pain. It would be funny to watch the Fed try to stamp out the flames of inflation with their feet on fire, as they clearly are doing, if not for the fact that they’re wearing your best shoes. They stole the soles right off your feet because you pay for there mistake every day, and they openly plan to steal a lot more while you’re looking. These brazen bankster robbers even announce they’re coming. The don’t break in. They expect your government to leave the door open for them as it lets them run the economy that your existence depends on.

Next time you walk through the red-meat section of your grocery store, just close your eyes, turn three times, tap your ruby-red slippers and say, “It’s transitory; it’s transitory; it’s all transitory.” Those are the words that got us here; maybe they’ll get you out. Better are the odds, though, that, by the time you stop spinning and open your eyes, the prices will be higher still.

Dr. Jerome Powell, nevertheless, assures you you’ll only feel a pinch as he applies the cure and takes us into what he still says can be a soft landing. By which he means only some of you will have to sacrifice your livelihoods in the job crash that he says will not hurt as much as the pinch of rising inflation is sure to if he doesn’t apply the brakes hard enough to skid into the cliff-edged curve.

Powell’s soft landing promise is premised on the strong labor market that assures him the economy is strong and resilient, meaning it assures him those negative GDP numbers earlier this year were but the mirage of a distant desert you’ll never know and not the barren landscape of latter-day lockdowns, Covid and/or vaccine deaths and illness, supply chains first broken by trade wars then shattered into shrapnel by real war and then stomped into sand by sanctions.

Meanwhile, more news just came out supporting my terribly important thesis for understanding the economic peril befalling us, which I first stated almost three months ago. That is that the labor market is only tight because labor died or got chronically ill, leaving producers unable to produce due to lack of productive laborers. That explanation of the severe labor shortage (currently 0.6 available workers for every existing job) made sense to me, and it appears it does finally to some others:

Long Covid may be ‘the next public health disaster’ — with a $3.7 trillion economic impact rivaling the Great Recession

[There are] millions of Americans with long Covid, also known as long-haul Covid, post-Covid or post-acute Covid syndrome. While definitions vary, long Covid is, at its core, a chronic illness with symptoms that persist for months or years after a Covid infection.

Up to 30% of Americans who get Covid-19 have developed long-haul symptoms, affecting as many as 23 million Americans, according to the U.S. Department of Health and Human Services….

Researchers think most Americans have had Covid-19 at this point.

Studies suggest subsequent infections raise the chances of an “adverse” outcome, including hospitalization and death. The virus has killed more than 1 million Americans to date, and some 2,000 more die each week, according to the Centers for Disease Control and Prevention.

Whether you want to attribute all of those deaths and long-term illnesses to Covid or to the vaccine or to the effects of masks trapping people’s own viral exhalations inside their bodies or isolation is irrelevant for the purpose of this particular discussion. The point here is, regardless of how it happened, we have a million deaths in excess of the norm and millions of additional people who are ailing chronically. How can anyone not think that millions of excess dead and sick in one nation alone might be contributing to the labor shortage? Might?

Meanwhile, the millions extracted from the participating labor force who are too sick to work who are still consumers, leaving us short of products to consume but with plenty of people who still want to consume them, assuring continued high inflation as people compete for shorter supply. So, how is Powell’s plan to drive more people out of work going to solve inflation if it means even lower production in an already low-production world with just as many people consuming or nearly so? One would think the math would be self-evident; but I can’t get most people to believe it.

Long Covid demonstrates that the virus is taking a lingering, pervasive and perhaps even more insidious toll. Medical experts have called it “the next public health disaster in the making.”

“There are just large numbers of people affected by this,” said Dr. Peter Hotez, co-director of the Center for Vaccine Development at Texas Children’s Hospital and a dean at Baylor College of Medicine….

But the tentacles of long Covid reach far beyond its medical impact: from the labor gap to disability benefits, life insurance, household debt, forfeit retirement savings and financial ruin….

All told, long Covid is a $3.7 trillion drag on the U.S. economy — about 17% of our nation’s pre-pandemic economic output, said David Cutler, an economist at Harvard University. The aggregate cost rivals that of the Great Recession, Cutler wrote in a July report….

Lost earnings and reduced quality of life are other sinister trickle-down effects, which respectively cost Americans $997 billion and $2.2 trillion.

That sounds like enough damage created to already be in a recession to me. So, the longterm economic crippling of the labor market is starting to be realized in the numbers. Don’t worry, though: There is completely zero chance I’ll get credit for ringing that alarm months ago, yet the Fed will still tell you in a few more months that this was an “unseen factor” that caused them to err’ in tightening an already tight labor market by laying off more workers when there are already too few to produce all that we need. This is not a situation where more unemployment helps, but they haven’t figured that out yet because …

No one could have possibly seen this coming!

(And if you want to make sure you see all of it coming so you are not blindsided by anything, sign up for The Daily Doom for free.)

Liked it? Take a second to support David Haggith on Patreon!

![]()

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!