Opening note: in setting this morning to write our 850th consecutive Saturday missive, we’ve just learned of the commencement of USA/ISR attacks on IRN. Whilst Gold “pre-attack” settled yesterday (Friday) at a record weekly closing high of 5296, (from which basis this piece shall be composed), weekend Gold trading (hat-tip IG International) has pushed price well-up into the 5400s; should such bid continue, the All-Time High of 5586 may come swiftly into play. That considered: we’ve in the past detailed geo-political price spikes tend to return from whence they came. Recall the RUS/UKR incursion (24 February 2022), Gold having spiked intra-day, only to then settle the following day lower than ’twas prior to the attacks.

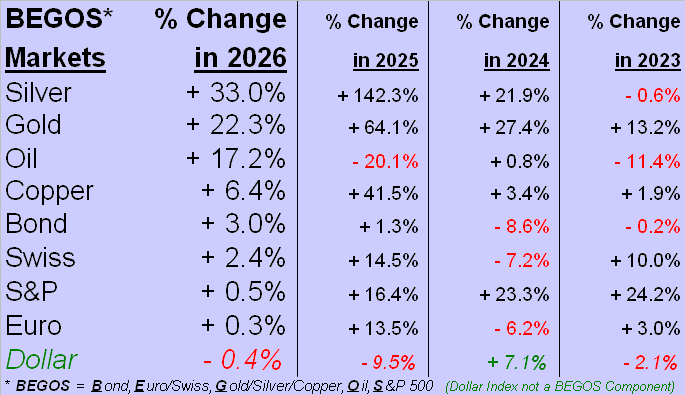

Either way, 2026 has begun so swiftly! Thus with February already in the books, let us start straightway with our BEGOS Markets Standings, wherein we find Sweet Sister Silver topping this year-to-date table for the seventh month in-a-row, joined on the podium as well by Gold and Oil, the non-BEGOS Dollar alone in the dumper:

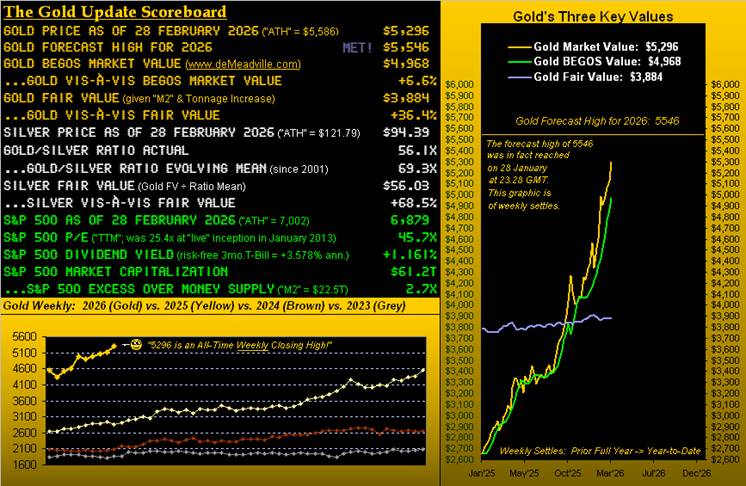

Regardless, Silver (94.39) is now (by the opening Scoreboard) +68.5% above its Fair Value (56.03) and Gold (5296) +36.4% above same (3884). To be sure, in periods of market mania — now further exacerbated by geo-political stress — the reality of Fair Value becomes relegated to the dust bin until such time reversion to that mean kicks in. And overvalued or otherwise, ’tis always a pleasure to find the precious metals atop the above BEGOS table.

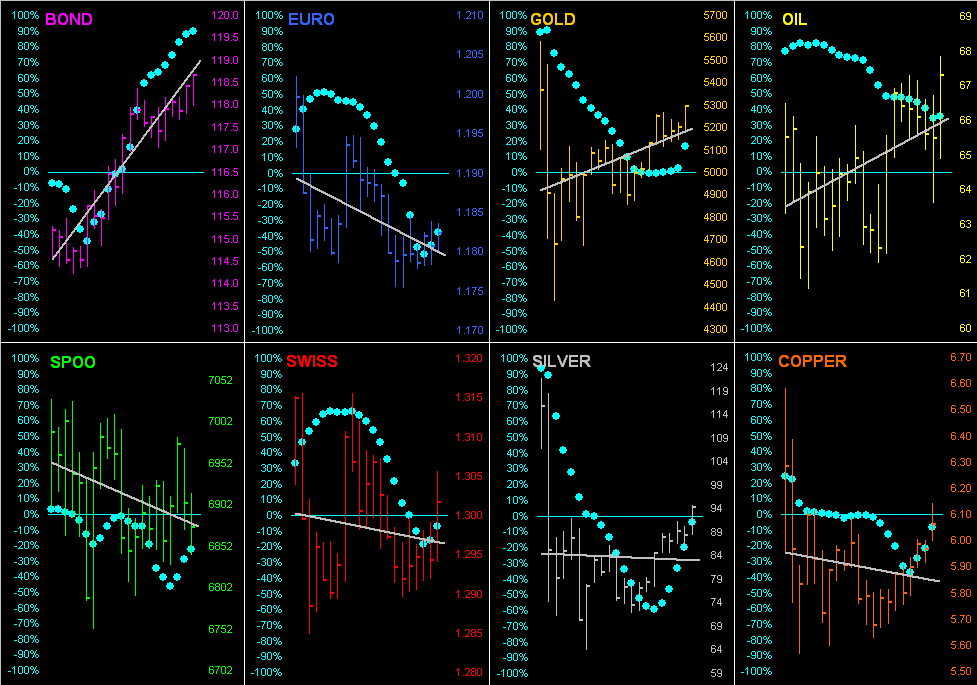

In staying with the theme of the BEGOS Markets, recall a week ago our citing Gold’s 21-day linear regression trend as having rotated (“barely”) to negative, but that a robust up day would right said trend back to positive, which is exactly what happened this past Monday, price recording a net gain for that day alone of +118 points ( +2.3%). And as we thus go ’round the the horn for all eight BEGOS components for these past 21 trading days (one-month), we therein see Gold’s grey diagonal trendline back to a positive tilt, whereas that for Silver remains mildly negative. Of greater import, the “Baby Blues” of trend consistency are firmly rising for both precious metals:

Now in parsing the first phrase of this week’s title “Gold Garners Praise…”, eight of Gold’s past ten trading days (13 through 27 February) have closed net up from the prior session. Praiseworthy indeed! In this young year thus far of just 39 trading days, eight up days in ten has occurred for only one other stint (14 – 28 January) following which Gold plunged nearly -1000 points in just three trading days (from 28 January’s close at 5411 to 02 February’s intra-day low of 4423). It happens, although given the Middle East conflict now underway, one senses we’ll see still higher Gold on Monday.

As for “…Silver Ablaze…”, the white-hot metal per the Standings already is +33.0% through the year’s first 39 trading days. That is the largest opening 39 trading-day-gain so far in this 21st century; (the second largest was +32.5% for the first 39 days of 2012 … just in case you’re scoring at home).

Too, our title queries “…but Must the Fed Raise?” The FinMedia and investment community regularly put forth guesstimates as to how many Federal Reserve Funds interest rate cuts will be made this year. Afterall, there are still plenty of opportunities given seven Open Market Committee Policy Statements are in 2026’s balance.

But rather than join the parrots, as you regular readers know, we keep a keen eye on StateSide inflation data: and ’tis going the wrong way to warrant a rate cut, perhaps so much so that a rate hike instead would be right.

But “Oh no!”, they say, because AI (Assembled Inaccuracy) is going to take all the jobs away eliciting massive unemployment and dismay. Ok. As long as folks still get their pay, (unless these newfangled Chinese robots get in the way). Remember H.G. Wells’ “The War of the Worlds” –[ novel 1898, film 1953/Paramount]? Perhaps E.R. Musk shall retaliate with a sequel “The War of the Bots”. But we digress.

The point is: with respect to the Fed’s targeted inflation rate of +2.0%, January retail core inflation (Consumer Price Index) came in at +0.3% (i.e. +3.6% annualized) whilst at the core wholesale level (Producer Price Index) ’twas +0.8% (i.e. +9.6% annualized). ‘Course, core readings assume that neither do you eat nor drive. Thus the January annualized all-inclusive headline paces were +2.4% and +6.0% respectively. (Waiting in the wings is January’s “Fed-favoured” Personal Consumption Expenditures data, due 13 March. The PCE December readings both ran at an annualized +4.8% pace. By our math, ’tis nowhere near +2.0%). Either way, have a great day.

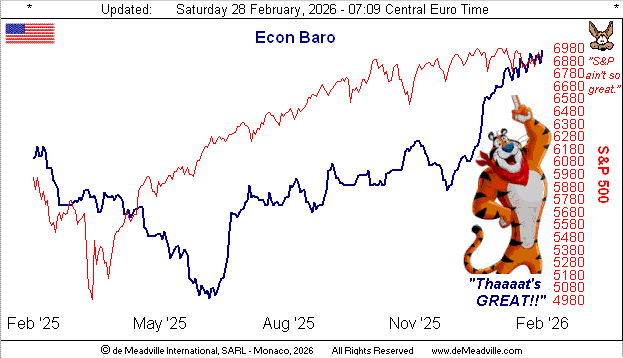

In fact, let’s next post the Economic Barometer, as ’tis be doing great! The Baro’s climb across the past 48 trading days (since mid-December) hasn’t previously been equaled since that culminating in mid-August 2020 during the first recovery wave (short-lived as it was) out of COVID. And specific to just this past week’s flow of nine incoming metrics, only three failed to improve period-over-period, one of which was Construction Spending, reported well in government “shutdown” arrears for back in November, (the December data notably improving). And February posted gains for both the Chicago Purchasing Managers Index and the Conference Board’s level of Consumer Confidence. Are you confident? Here’s the Baro:

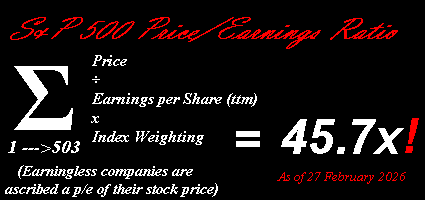

With respect to that “confident” query, the S&P 500 keeps us forever leery. The mighty Index’s honestly calculated price/earnings ratio remains ridiculously (dare we say dangerously) high (vs. Jerome Cohen’s average bull market P/E range of 15x to 18x). “Got stocks?” Sorry to hear it:

As an aside to you WestPalmBeachers down there, we just plugged that precise formula into AI (Assembled Inaccuracy) and “it” came up with 29x. Wrong. Mind your broker’s math and your equities.

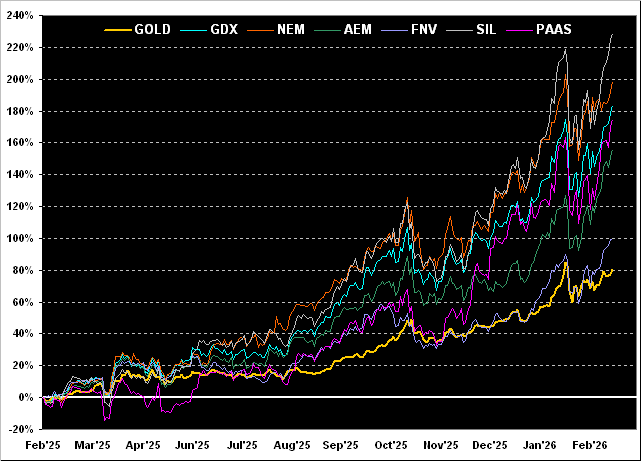

And speaking of equities, it being month-end, ’tis time once again for our year-over-year graphic of Gold’s percentage track compared with those of its high-level publicly-traded companies, all of which have been nicely recovering following their January El Plungo (technical term). Therein from the top down we’ve the Global X Silver Miners exchange-traded fund (SIL) up a stunning +229%, followed by Newmont (NEM) +198%, the VanEck Vectors Gold Miners exchange-traded fund (GDX) +184%, Pan American Silver (PAAS) +175%, Agnico Eagle Mines (AEM) +156%, Franco-Nevada (FNV) +99%, and Gold itself +81%. Equities-lovers’ leverage elation!

And with further respect to Gold itself, here next is the yellow metal by the week, also from one year ago-to-date along with price’s parabolic trend dots, the rightmost blue ones now 12 weeks in LongSide duration. Gold’s expected weekly trading range is 304 points, which with the Middle East offensive could be covered early on in the ensuing week; (the daily is 159 points). As for the “flip-to-Short” level, at 4794 ’tis -502 points (-9.5%) below Friday’s settle of 5296:

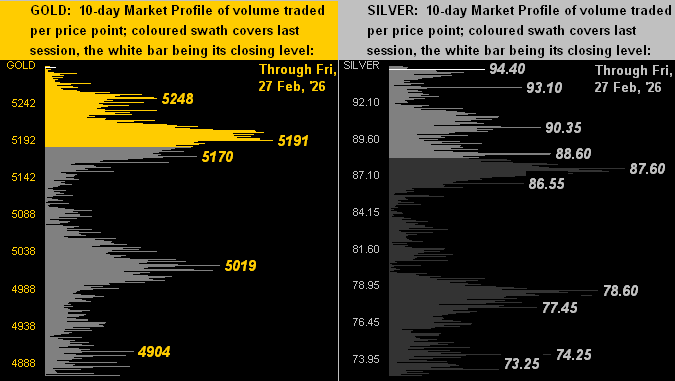

Drilling deeper into “The Now”, here are the 10-day Market Profiles for Gold on the left and for Silver on the right. As respectively labeled, the yellow metal’s most volume-dominant supporter is 5191, whilst for the white metal ’tis 87.60:

Towards the wrap, ‘twouldn’t be month’s end without our chart of the Gold Structure by the month from 2020-to-date. Note that the rightmost candle — indeed Gold’s eighth consecutive up month — for February could not eclipse that for January’s having reached the All-Time High of 5586; but again given the now amped-up geo-political stress, let’s see what the new week holds in store. For as sang Sly in ’69: “I want to take you higher”

Oh look –> our long-time valued assistant Miss Gibbs (she’s a winner) just dropped on our desk this photo as transmitted today from a waving Squire during his avalanche duties up in Les Grands Montets. He sends his congrats for our making it 85% of the way to missive No. 1,000. Thanks mate, albeit one week at a time is our gait. (We wonder as well if that avalanche is a prélude to an S&P “correction”):

Closing note: following this piece’s “Opening note”, in now approaching late Saturday afternoon here, the weekend Gold trade has not furthered itself higher from the 5400s we’d seen earlier this morning. Too, ’tis reported (reliably or otherwise) the Straits of Hormuz are now closed; (if so, best get to the petrol station before the lines get long). In any event, ’tis no time for panicky trading. Instead, patiently mind your Gold rather than fold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

deMeadville. Copyright Ⓒ 2010 - 2026. All Rights Reserved.

About the author