Strengths

- The best performing precious metal for the week was platinum, up 1.73%, as hedge funds boosted their bullish sentiment to a seven-month high. Perseus Mining’s production of 137,000 ounces was 10% ahead of consensus with Sissingué and Edikan both much better than consensus, while Yaouré also recorded a solid beat. Edikan’s production was up 82% quarter-over-quarter as throughput, grades, and recoveries all improved. Sissingué saw a healthy 11% quarter-over-quarter uptick in mill throughput while total movements also improved despite wet weather.

- SSR Mining announced the acquisition of an additional 30% interest in the Kartaltepe Mining JV at Copler for total consideration of $150 million in cash. This will increase SSR’s ownership interest from 50% to 80% of the entire Copler district from partner Lidya Mining. SSR sees this improving life-of-mine cash flows for the Cakmaktepe Extension and providing exploration upside.

- Aya Gold & Silver has secured $100 million in debt financing from the EBRD and CTF for the Zgounder Silver Mine Expansion. This is a major development for the company, since having EBRD's investment is considered to be a seal of approval and further validates the project. The company is in a strong financial position, considering much of the expansion is already funded by its current cash position of $65 million.

Weaknesses

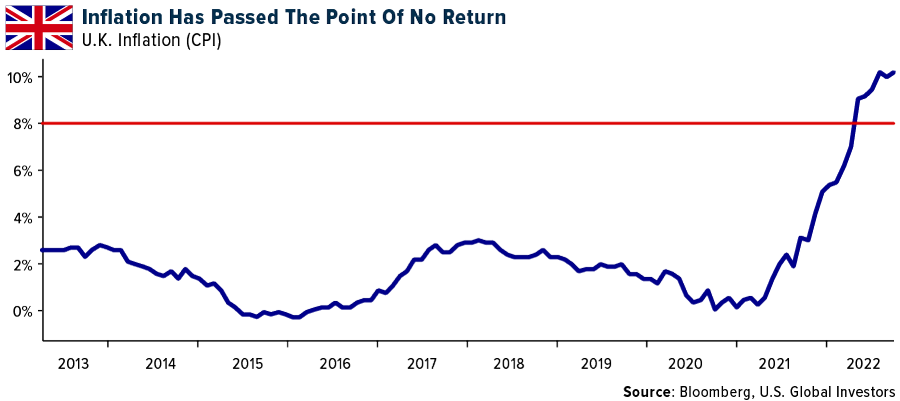

- The worst performing precious metal for the week was palladium, down 5.24%, as hedge funds boosted their bearish sentiment to a 12-week high. Once inflation hits 8%, history suggests that it sticks around, reads one Bloomberg article. This is according to a new report from the Deutsche Bank analysts, led by Jim Reid. The team looked at 318 separate occasions since 1920, Bloomberg explains, across both developed and emerging markets, where inflation had risen above 8%. On average, inflation then took “around two years to even fall beneath 6%, before settling around that level out to five years after the initial 8% shock.”

- Evolution Mining’s gold production came in at 161,000 ounces versus consensus of 176,000 ounces. The 8% miss was driven by 13% lower production at Cowal due to a bi-annual shutdown and a 27% miss at Mt Rawdon, attributed to above-average rainfall restricting access to the pit. Newcrest Mining announced that a team member from its mining and development contractor, Procon, was involved in a critical incident at the Brucejack mine. All mining and processing operations at Brucejack have been suspended until further notice.

- Royal Bafokeng Platinum reported a weaker-than-expected third quarter 2022 update with the metals in concentrate production missing consensus by 7%. The key production miss came from Styldrift, which management attributed to an extended Section 54 safety stoppage and operational challenges at the North mining sections. Higher on-reef dilution and reduced stopping tonnage contributions drove a 47% increase year-over-year in Styldrift's third quarter unit costs.

Opportunities

- Goldman Sachs expects the focus for miners will center around a handful of things going into the new year, including: 1) the ability to mitigate operating inflation and capital inflationary pressures, 2) capital allocation strategies, and 3) production expectations into the fourth quarter of this year and into 2023, particularly given weaker first half of the year volumes.

- Bloomberg Intelligence highlighted Centamin PLC’s potential to grow into a multi-asset producer with its Sukari mine projected to produce over 500,000 ounces of gold per year. If Centamin has success in delivering the Doropo project in the Ivory Coast, annual output could climb to almost 700,000 ounces a year by 2025. Exploration spending in West Africa will run about $25 million in 2022 with $15 million allocated to Doropo. Initial capex for Doropo is estimated at $275 million.

- According to Stifel, while K92 Mining has already grown its mineral resources to host 16 million ounces of gold, the group thinks drilling is only starting to scratch the surface. The high resolution and deeper MT geophysical surveys completed earlier this year have helped identify numerous prospects that will be tested in the coming years. The stock has recently come under selling pressure with some recent insider selling filings.

Threats

- Broader market and macro themes continue to weigh on junior gold valuations (at levels last seen with gold between $1,200-$1,300 per ounce). Many projects are continuing to advance toward construction decisions; however, investors will need to be patient and increasingly selective with a more challenging financing environment and ongoing cost risk. The junior gold/silver developer universe has seen a 30% average decline over the last 12 months, underperforming the metal by 25%.

- Pure Gold, after it announced insufficient liquidity, is immediately suspending operations and placing the mine under care and maintenance. Despite a downtrend in mine operating costs, the mine has been unable to consistently generate positive cash flow resulting in insufficient liquidity, and considering the current debt obligations, this puts the company at a high risk of default, should it be unable to secure additional financing.

- The United States imposed sanctions on a Nicaraguan state gold mining operation Monday, saying it finances the regime of President Daniel Ortega and his wife Vice President Rosario Murillo. The sanctions focus on the Nicaraguan General Directorate of Mines, as well as Lenin Cerna, a close advisor

and former security chief for Ortega. The U.S. Treasury said the directorate manages most mining across the country, and that proceeds from gold mining benefit Ortega’s regime directly. Calibre Mining, though not sanctioned directly, sold off more than 30% on the week on this news, with 12% of its float trading hands.

About the author