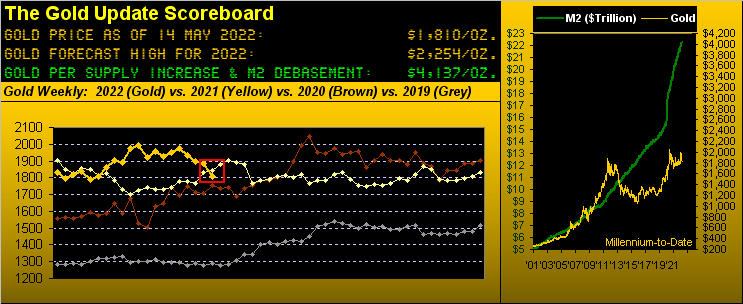

Since this week ending one year ago (on 14 May 2021), we've had:

■ a +9.2% debasive increase to the StateSide "M2" money supply from $20.42 trillion to $22.29 trillion, driven largely over COVID liquidity accommodations, the proceeds thereto ending up in the stock market, (oops...);

■ a dysfunction of supply chains, energy sourcing, and currencies elicited from an appallingly inhumane war;

■ a stagflationary shrinkage in deflator-adjusted Gross Domestic Product for three consecutive quarters in the U.S per REAL economic erosion;

■ a increase in interest rates which when starting from 0.00% we've demonstrated ad nauseam is beneficial for hard assets;

■ plus your etc, et alia, ad infinitum...

And yet, the price of Gold in settling out the week yesterday (Friday) at 1810 is -1.8% below where 'twas on this day a year ago. You can comparatively see the crossover within the red rectangle on the above Gold Scoreboard's annual price tracks.

Thus, we've just had both Gold's fourth consecutive weekly drop and fourth consecutive weekly "lower low", price this past week not having just re-tested the 1854-1779 critical support zone, but having bored well down therein as shown here in our updated year-to-date graphic:

Technical analysis aside, Gold's swoon is incredulously beyond any and all fundamentally analytical common sense, even as today mention is made of a "five-figure" price. We're content to stay with the Scoreboard's valuation of 4137, and moreover maintain our forecast high for this year of 2254, (the "M Word" crowd notwithstanding)

"Well, mmb, belief in Bitcoin is growing at the expense of Gold..."

Well, let's see: priced today at 1810, Gold is -13.4% below its All-Time High of 2089; bits**t's settle for the week at 29,785 is -57.1% below its all-time high of 69,355. "Bit" of a difference there.

But Squire is making an interesting point. We seem to read more lately of Gold becoming a "has-been" whilst bits**t is what to "be-in". And 'tis curiously in line with how Leonardo Bonacci (aka "Fibonacci") may well put it today: a "herd mentality" naturally induced through nature is in force. One pro-bits**t person will "dis" Gold, and then a second; then two more, then another three, then five, eight, 13, 21, 34 and suddenly 'tis "Holy Golden Ratio, Batman!" for one can now predict 55 more will be next to jump on the "dis" Gold bandwagon. And so on. Herd mentality driven by emotion and copying whatever everyone else is doing is extraordinarily fascinating until one ends up with nothing. (Pssst: Got Gold?) Something that endures millennia is not nothing.

Nothing however has been gained from Gold of late other than to be able to purchase it at less than half what 'tis worth. So rationalizing price's coming off as we here see by the weekly bars is in fact "a good thing", even as the red-dotted parabolic Short trend completes its seventh week in duration. For Gold's swoon is a bargoon:

All that said, 'tis best that Gold not penetrate the bottom of the 1854-1779 critical support zone, toward which it gave a scare via this past week's (indeed yesterday's) low of 1797. To be sure, further downside cases can be for 1753, 1721, 1678, and so on; but let's not go there. Rather, the "The Herd" need be made more aware. (Or as a long-time Gold colleague says: "There will come the day to sell your Gold: the day that everybody else wants it.")

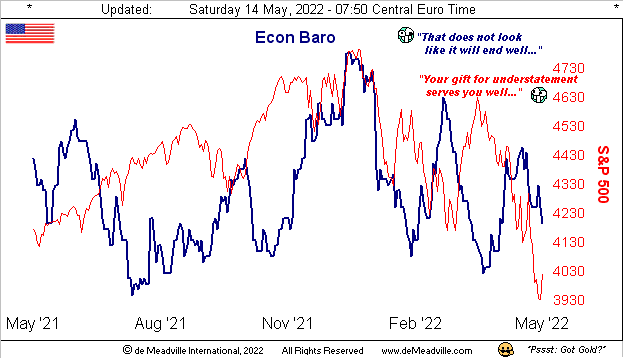

What nobody really wants is an economy suffering the ravages of stagflation which continue to mount, in turn furthering the Economic Barometer's dismount. Again assuming that neither do you take nourishment nor consume energy, your April cost of living rose +0.6% as measured by the Core Consumer Price Index: just in case you're scoring at home -- or perhaps sweating at home given your perfected day-trading methodology has stopped working -- that is double the inflation increase for March. But wait, there's more: the venerable University of Michigan "Go Blue!" Sentiment Survey preliminary reading for May just came in at its lowest level of those finalized since August back in 2011. As we've on occasion quipped about the Conference Board's reading on Consumer Confidence: "Are you confident?" The Baro sure ain't:

As for the last place you'd wanna be working these days, FedHead Jerome "Jumpin' Jay" Powell has secured another four-year stint overseeing it all, within which New York FedPrez John "It's All Good" Williams is confident the Federal Reserve has the "right tools" to lower inflation, whereas FedGov Christopher "Up The" Waller says: "We have to cool off demand and try to get inflation pressures down." Which for you WestPalmBeachers down there there means your variable rate funding sources are going to further squeeze you.

And speaking of squeezing, what is supposed to be a record-setting year for travel is instead finding costs too dear to manage and (in the words of Dow Jones Newswires) "spoiling summer plans." (One bright spot: here in wee MC, indoor masking requirements were just lifted yesterday, should you be headed this way; just add €uros).

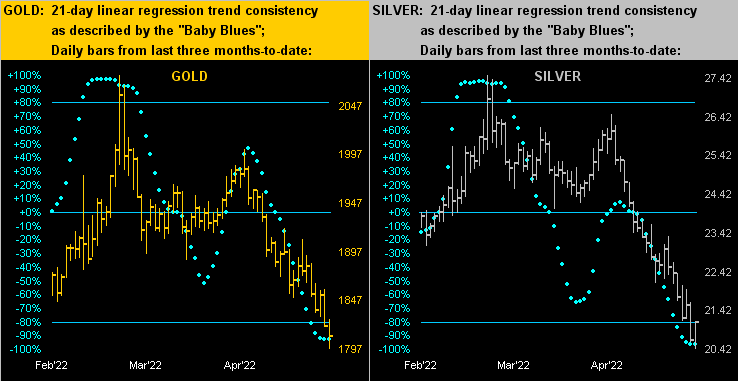

Either way, the precious metals' ways obviously remain down as we see across their respective three months of daily bars for Gold on the left and for Silver on the right. The "Baby Blues" of trend consistency in both cases need curl back above the -80% axes to become indicatively leading of higher price levels:

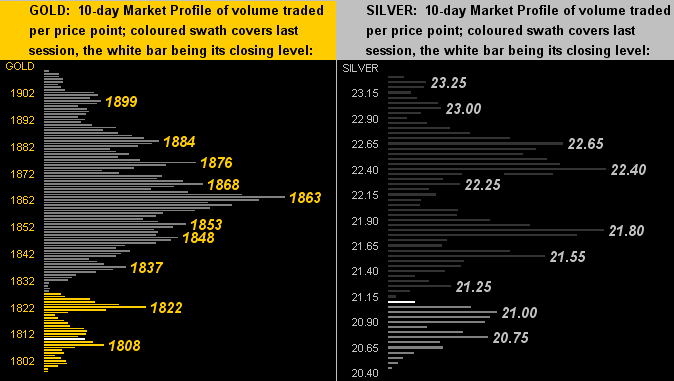

And upon prices inevitably turning higher, by the 10-day Market Profiles for Gold (below left) and Silver (below right) it clearly looks to be an arduous climb near-term, (barring the "buying light bulb" suddenly going on for "The Herd"):

As to where Gold sits in its broadest sense, here we've:

The Gold Stack

Gold's Value per Dollar Debasement, (from our opening "Scoreboard"): 4137

Gold’s All-Time Intra-Day High: 2089 (07 August 2020)

2022's High: 2079 (08 March)

Gold’s All-Time Closing High: 2075 (06 August 2020)

The Weekly Parabolic Price to flip Long: 2027

The Gateway to 2000: 1900+

10-Session “volume-weighted” average price magnet: 1859

The 300-Day Moving Average: 1824 and rising

Trading Resistance, (notable Profile apices): 1822 / 1837 / 1863

Gold Currently: 1810, (expected daily trading range ["EDTR"]: 32 points)

Trading Support: 1808

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

10-Session directional range: down to 1797 (from 1911) = -114 points or -6.0%

2022's Low: 1779 (28 January)

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr '18 preceded by 1362 in Sep '17

Neverland: The Whiny 1290s

The Box: 1280-1240

Peeking ahead to next week, 10 of the Econ Baro's 13 incoming metrics are "by consensus" expected to be worse than their prior readings. To that end, we'll part for this week with these few observations:

■ U.S. Secretary of the Treasury Janet "Old Yeller" Yellen sees the financial system carrying on in an orderly fashion (now stop laughing out there) in spite of "volatility". Orderly or otherwise, with respect to "volatility" we see it continuing to clobber the stock market; (have a glance at the website's S&P Moneyflow page: scary!). Given the S&P's high (4819 vs. 4024 today) being in for the year (see our 23 April missive), 'tis quite a way to go for the low, our 3587-3198 band still at hand.

■ Speaking of the Treasury, everyone's favourite segment therein -- the delightful Internal Revenue Service -- has apparently (due to COVID 'tis said) fallen significantly behind such that delayed refunds now pay an interest rate of 4%. That's better than the bank, and moreover, 'tis perfectly OK to overpay. So don't delay, file today!

■ Finally, per the NYFed, those responding to a survey on inflation expectations put prices up by +3.9% three years from now! (Yes, you're laughing again). Query: shouldn't that decimal point be moved a bit to the right?

Regardless, don't you miss out on what's right: whilst 'tis in a swoon, grab the Gold bargoon!

Cheers!

...m...

About the author