After more than a year of anticipation, the U.S. presidential election is finally upon us. News coverage is at a fever pitch, and rhetoric from both sides has turned increasingly intense. Many people are experiencing election fatigue, ready to get past the noise and move on with their lives. Naturally, precious metals investors are wondering how the election outcome will impact their holdings. Is there a simple answer, such as "Democrats boost gold and silver, while Republicans don’t" (or vice versa)? In this article, I’ll explore historical data to address that question and share additional insights that support a bullish outlook for precious metals in the years ahead.

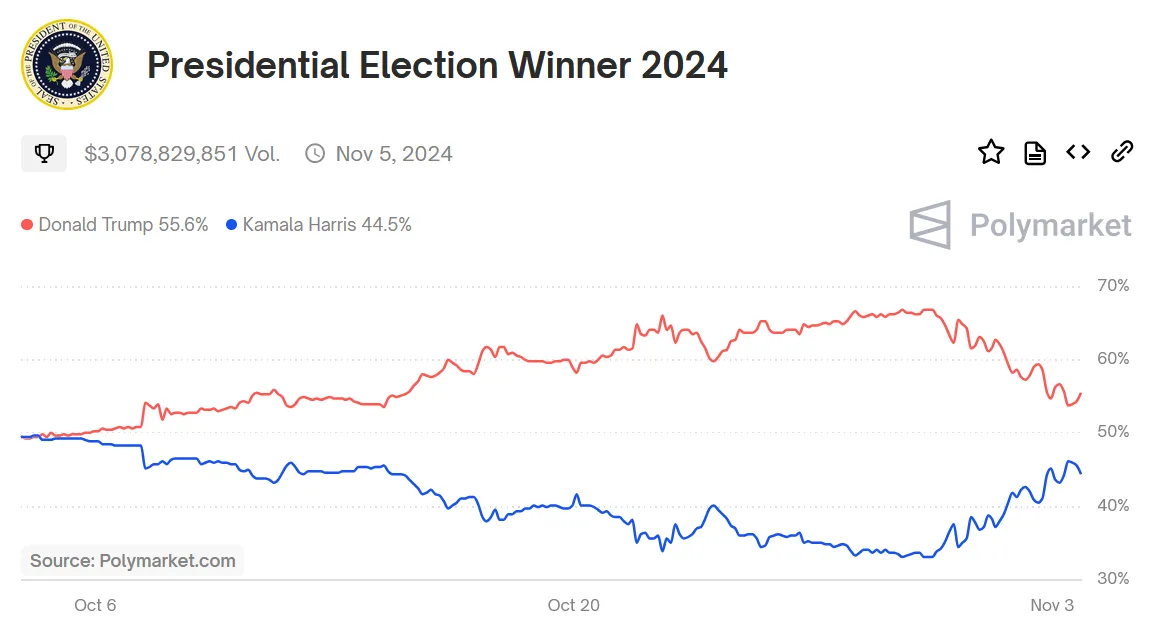

Since early October, presidential candidate Donald Trump’s election odds have risen significantly against candidate Kamala Harris. According to Polymarket, the world’s largest prediction market, Trump’s chances surged from 48.9% against Harris’s 50.0% to a peak of 66.9% against her 33.1% by October 30th. During this period, gold gained a solid 5.8%, and silver rose 8.5%. The U.S. Dollar Index, equities, and Bitcoin also saw increases, in what became known as the “Trump trade.”

By October 30th, however, Donald Trump’s election odds had peaked and subsequently declined to 55.4% at the time of writing. As Trump’s odds fell, precious metals, the U.S. Dollar Index, equities, and Bitcoin also experienced pullbacks. While other factors may be influencing these trends, the initial impression suggests that the prospect of a Trump presidency is bullish for gold and silver.

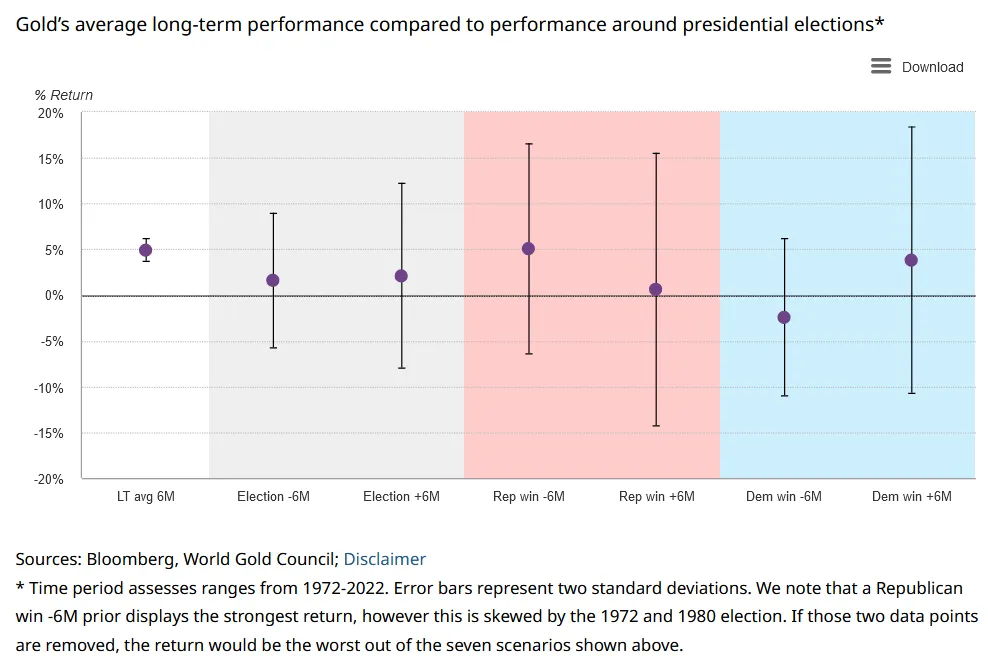

Many are curious whether one political party tends to be more bullish for gold and silver than the other. To address this, the World Gold Council recently analyzed gold's performance before and after U.S. presidential elections from 1972 to 2022. Their findings indicate that none of the results are statistically significant, however, leading them to conclude, “Overall, our analysis of gold and U.S. presidential elections suggests that gold does not react directly to party affiliation or changes in leadership.”

Many are curious whether one political party tends to be more bullish for gold and silver than the other. To address this, the World Gold Council recently analyzed gold's performance before and after U.S. presidential elections from 1972 to 2022. Their findings indicate that none of the results are statistically significant, however, leading them to conclude, “Overall, our analysis of gold and U.S. presidential elections suggests that gold does not react directly to party affiliation or changes in leadership.”

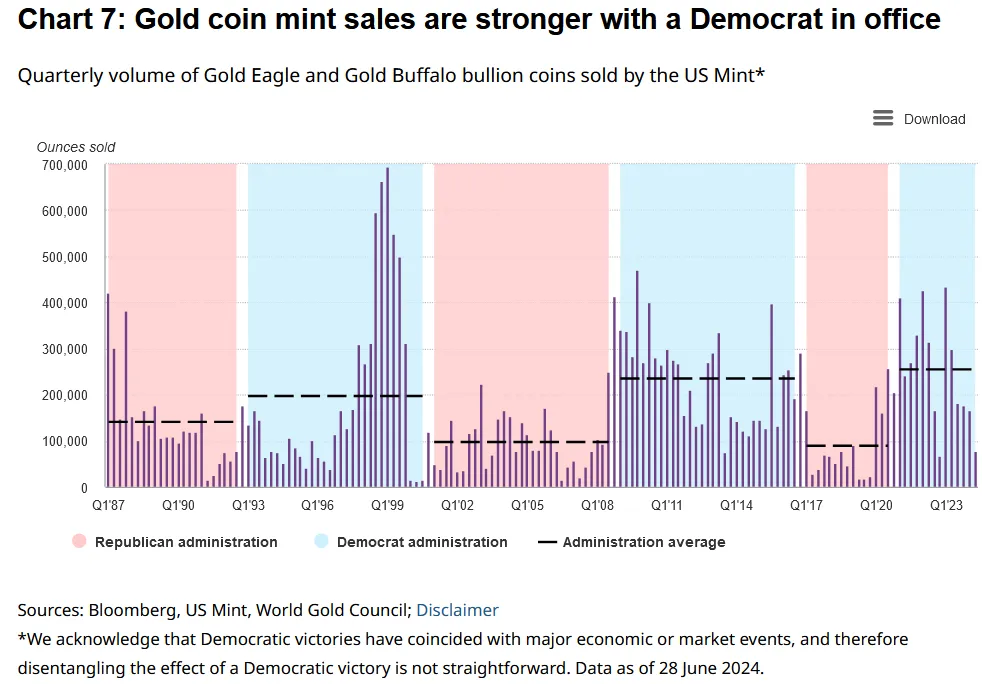

The same World Gold Council study found that gold bullion coin sales were higher when a Democrat was in office. They theorized this trend is likely because gold buyers tend to lean Republican and feel more apprehensive when a Democrat is in office, making them more inclined to purchase gold, traditionally viewed as a safe-haven asset (a theory I agree with). I’d also like to point out that the major gold-buying episodes of the past few decades have coincided with Democratic presidencies, though were not due to the actions or policies of any particular party—for example, the Y2K scare in the late 1990s, the Global Financial Crisis from 2007 to 2011, and the COVID pandemic in the early-2020s.

The same World Gold Council study found that gold bullion coin sales were higher when a Democrat was in office. They theorized this trend is likely because gold buyers tend to lean Republican and feel more apprehensive when a Democrat is in office, making them more inclined to purchase gold, traditionally viewed as a safe-haven asset (a theory I agree with). I’d also like to point out that the major gold-buying episodes of the past few decades have coincided with Democratic presidencies, though were not due to the actions or policies of any particular party—for example, the Y2K scare in the late 1990s, the Global Financial Crisis from 2007 to 2011, and the COVID pandemic in the early-2020s.

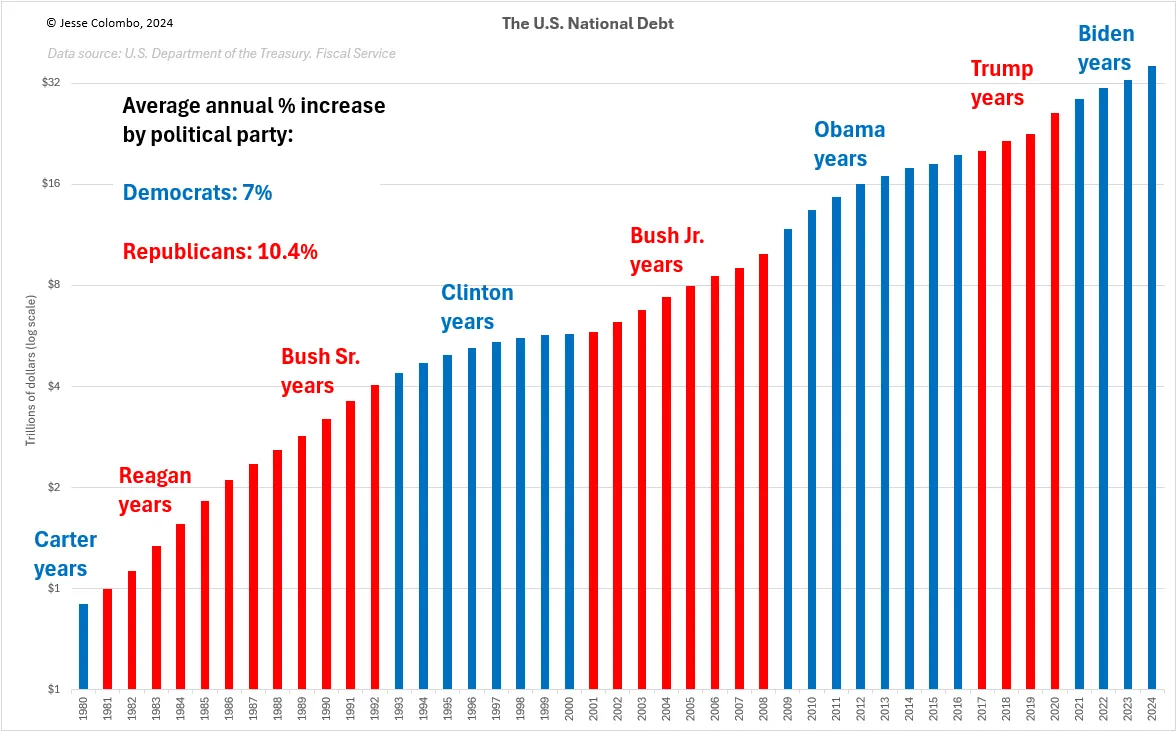

As we’ve seen, there’s no clear link between the party in the White House and the performance of precious metals—at least historically. I believe that regardless of which party wins, the long-term outlook for gold and silver remains bright. Both parties have shown a strong tendency to increase the national debt—a factor that supports a bullish case for precious metals, as illustrated in the graph below.

As we’ve seen, there’s no clear link between the party in the White House and the performance of precious metals—at least historically. I believe that regardless of which party wins, the long-term outlook for gold and silver remains bright. Both parties have shown a strong tendency to increase the national debt—a factor that supports a bullish case for precious metals, as illustrated in the graph below.

Though Republicans are often viewed as the more fiscally conservative party, the national debt—now nearing $36 trillion—has grown at an average annual rate of 10.4% under Republican presidencies since 1980, compared to 7% under Democratic administrations. It’s worth noting that the higher debt growth during Republican terms is largely due to Ronald Reagan’s significant defense spending during the Cold War. There’s a real risk that ambitious Democratic-backed initiatives, such as a potential Green New Deal, universal basic income (UBI), and funding those through the principles of Modern Monetary Theory (MMT), would drive national debt far higher—an outcome that would be very bullish for gold and silver.

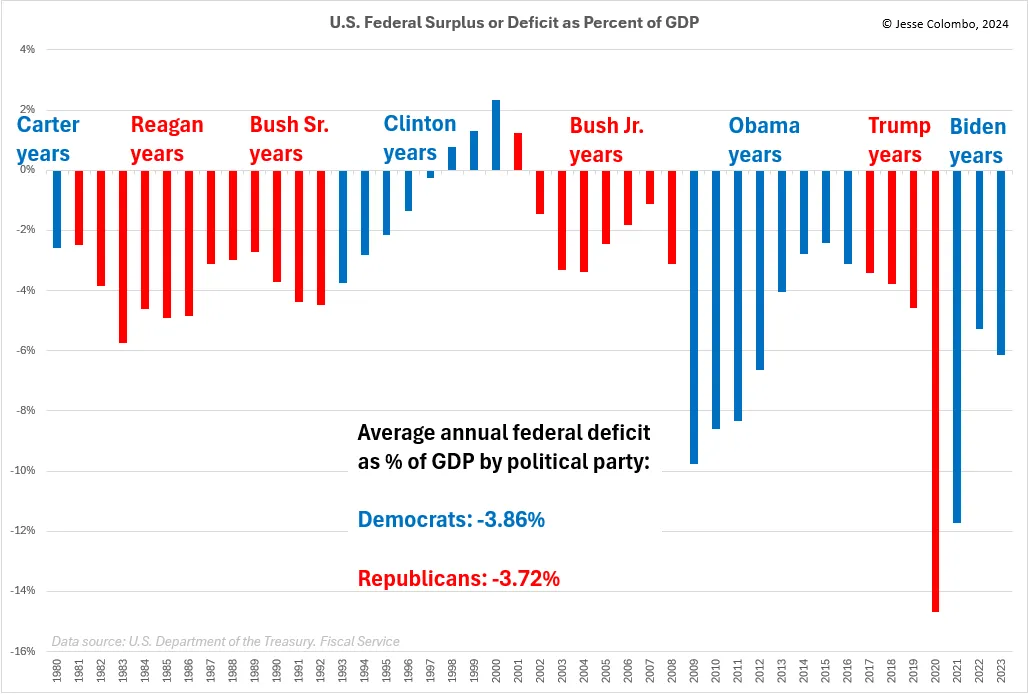

Examining U.S. federal budget surpluses and deficits as a percentage of GDP can also shed light on whether either party has a tendency to run larger deficits. My findings show that since 1980, there’s little difference between Democrats (an average annual deficit of -3.86%) and Republicans (-3.72%). This reinforces my view that the outlook for gold and silver remains strong, regardless of the party in power, as both are likely to continue running budget deficits well into the future.

Examining U.S. federal budget surpluses and deficits as a percentage of GDP can also shed light on whether either party has a tendency to run larger deficits. My findings show that since 1980, there’s little difference between Democrats (an average annual deficit of -3.86%) and Republicans (-3.72%). This reinforces my view that the outlook for gold and silver remains strong, regardless of the party in power, as both are likely to continue running budget deficits well into the future.

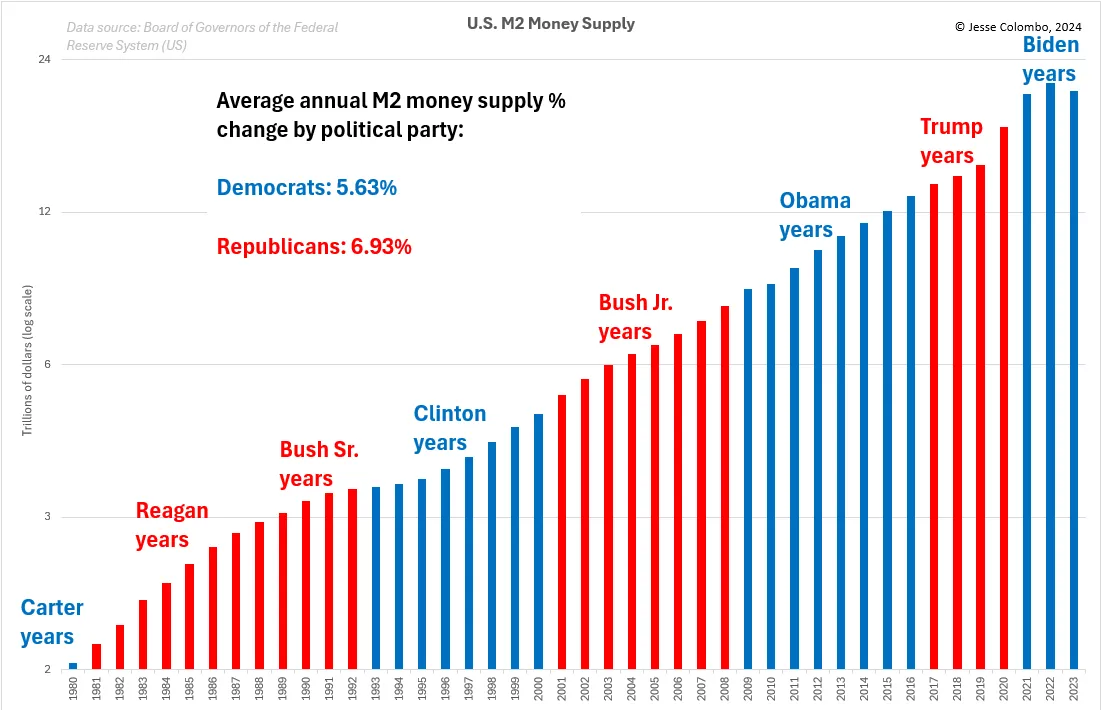

Money supply growth is the reason for inflation, and gold and silver benefit from inflation over the long run. Nobel laureate economist Milton Friedman famously stated, “Inflation is always and everywhere a monetary phenomenon.” The graph of the M2 money supply below illustrates its steady increase, regardless of the political party in power—a trend I expect to continue.

Money supply growth is the reason for inflation, and gold and silver benefit from inflation over the long run. Nobel laureate economist Milton Friedman famously stated, “Inflation is always and everywhere a monetary phenomenon.” The graph of the M2 money supply below illustrates its steady increase, regardless of the political party in power—a trend I expect to continue.

The M2 money supply encompasses all currency in circulation, checking accounts, travelers’ checks, savings deposits, time deposits under $100,000, and shares in retail money market mutual funds. Since 1980, M2 has grown at an average annual rate of 5.63% under Democratic presidents and 6.93% under Republican presidents, with the latter figure notably skewed by the high growth rates during the Reagan era.

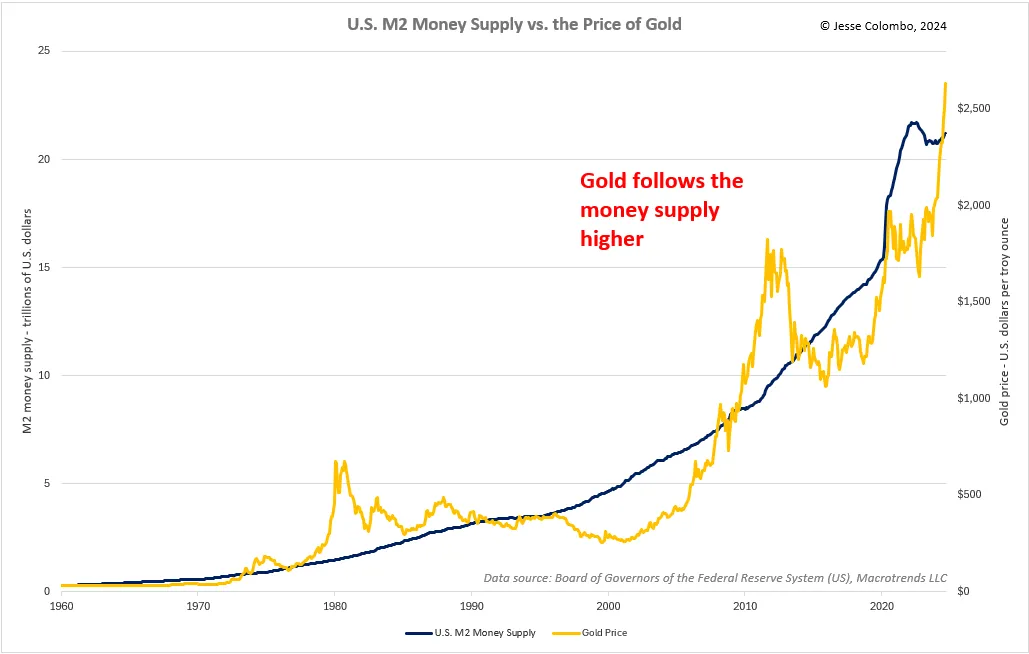

The graph below shows how gold follows the M2 money supply higher over time:

The graph below shows how gold follows the M2 money supply higher over time:

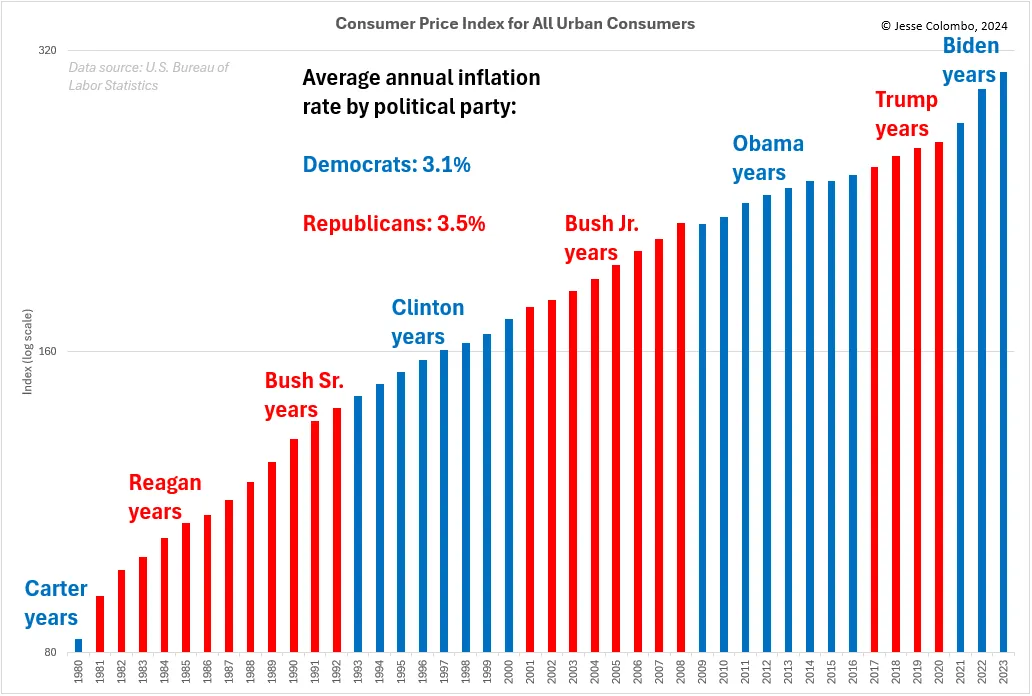

Examining inflation itself, the U.S. Consumer Price Index (CPI)—a measure of the cost of consumer goods and services over time—has steadily risen regardless of the political party in the White House. Since 1980, the average annual inflation rate during Democratic presidencies has been 3.1%, compared to 3.5% under Republican presidencies, with the latter figure skewed by the Reagan years. I expect inflation to keep climbing regardless of who holds office, which should bolster the case for gold and silver.

Examining inflation itself, the U.S. Consumer Price Index (CPI)—a measure of the cost of consumer goods and services over time—has steadily risen regardless of the political party in the White House. Since 1980, the average annual inflation rate during Democratic presidencies has been 3.1%, compared to 3.5% under Republican presidencies, with the latter figure skewed by the Reagan years. I expect inflation to keep climbing regardless of who holds office, which should bolster the case for gold and silver.

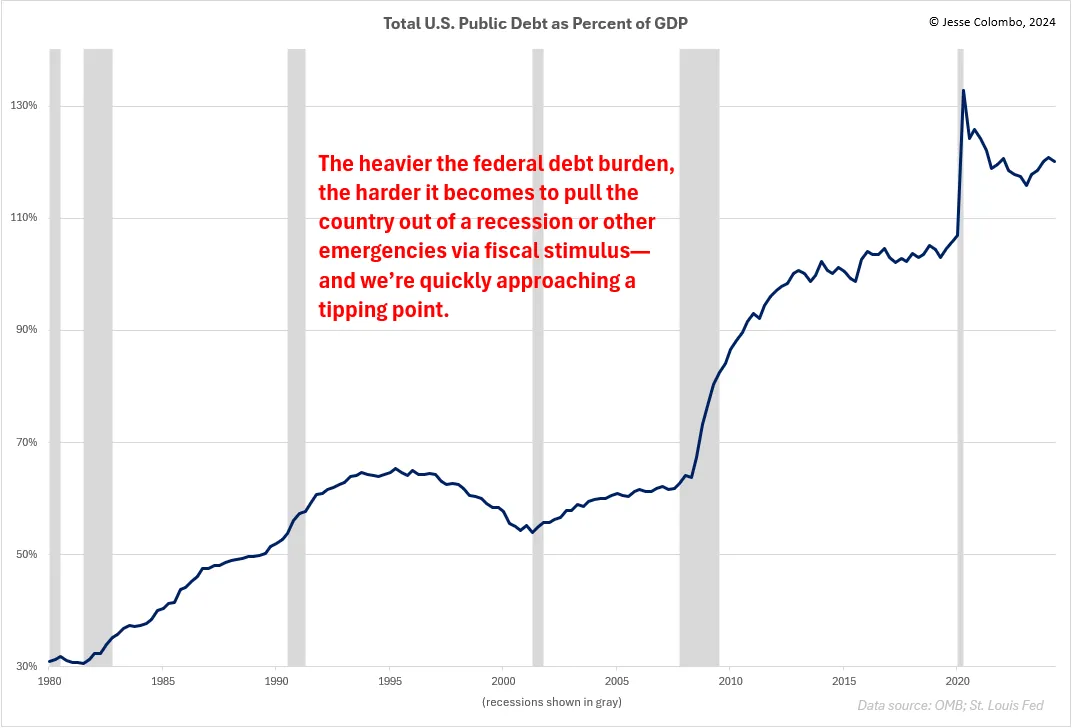

One key reason I expect inflation to accelerate in the years ahead is the increasingly precarious fiscal position of the United States. As the graph below shows, the national debt has been growing at a much faster pace than the economy, worsening our debt burden significantly. With the government nearing its fiscal limits, it will have far less flexibility to support the economy during recessions or national emergencies through traditional stimulus measures. This raises the likelihood that the government will eventually resort to outright debt monetization or "money printing" to cover expenses, which would lead to rapid inflation and push gold and silver to remarkable highs.

One key reason I expect inflation to accelerate in the years ahead is the increasingly precarious fiscal position of the United States. As the graph below shows, the national debt has been growing at a much faster pace than the economy, worsening our debt burden significantly. With the government nearing its fiscal limits, it will have far less flexibility to support the economy during recessions or national emergencies through traditional stimulus measures. This raises the likelihood that the government will eventually resort to outright debt monetization or "money printing" to cover expenses, which would lead to rapid inflation and push gold and silver to remarkable highs.

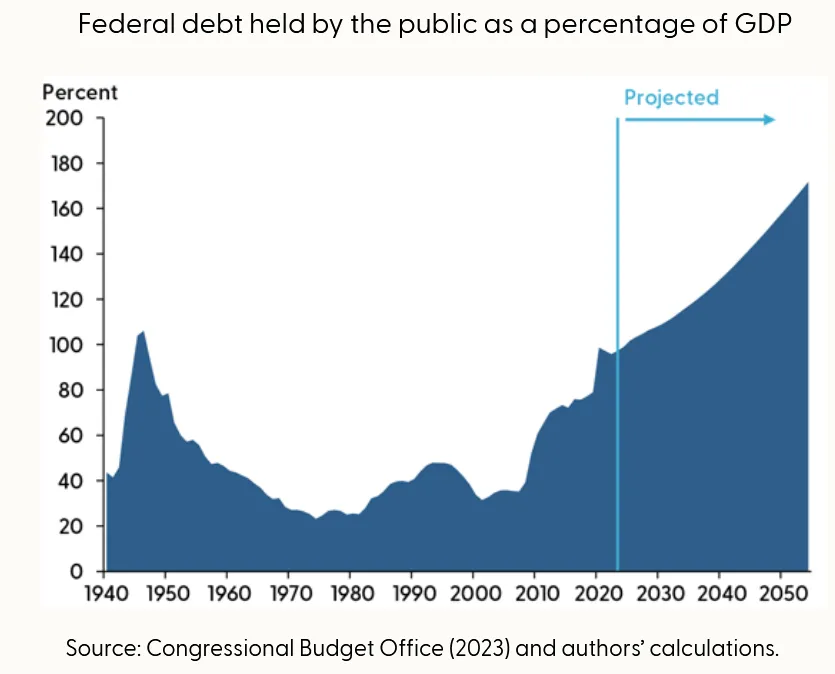

Even more concerning is the U.S. Congressional Budget Office's projection that federal debt held by the public, as a percentage of GDP, will soar from just below 100% today to around 170% over the next few decades:

Even more concerning is the U.S. Congressional Budget Office's projection that federal debt held by the public, as a percentage of GDP, will soar from just below 100% today to around 170% over the next few decades:

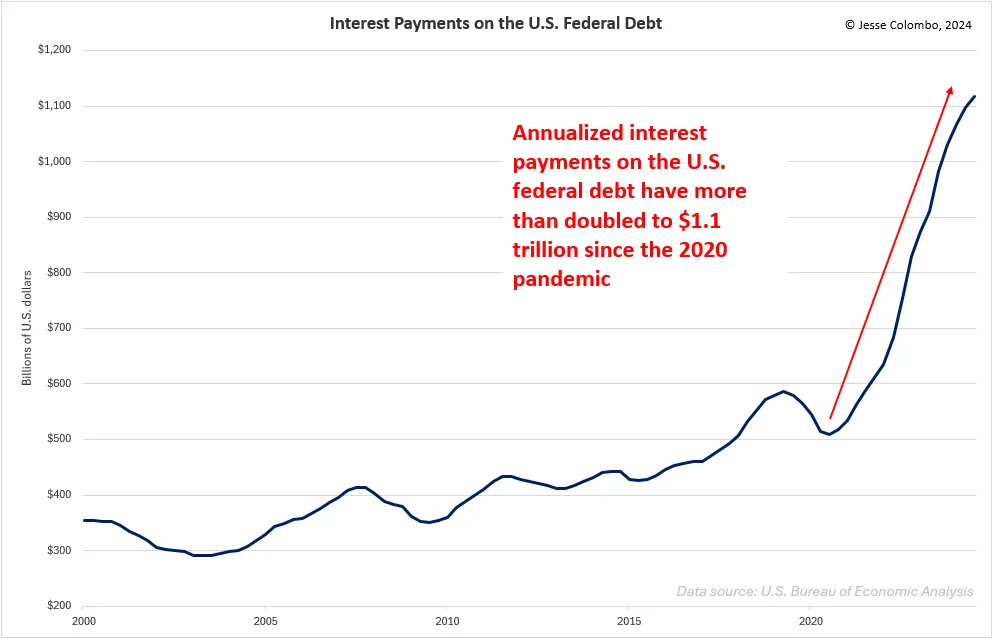

Since the 2020 pandemic, the combination of America’s surging national debt and rising interest rates has more than doubled annual interest payments to over $1.1 trillion:

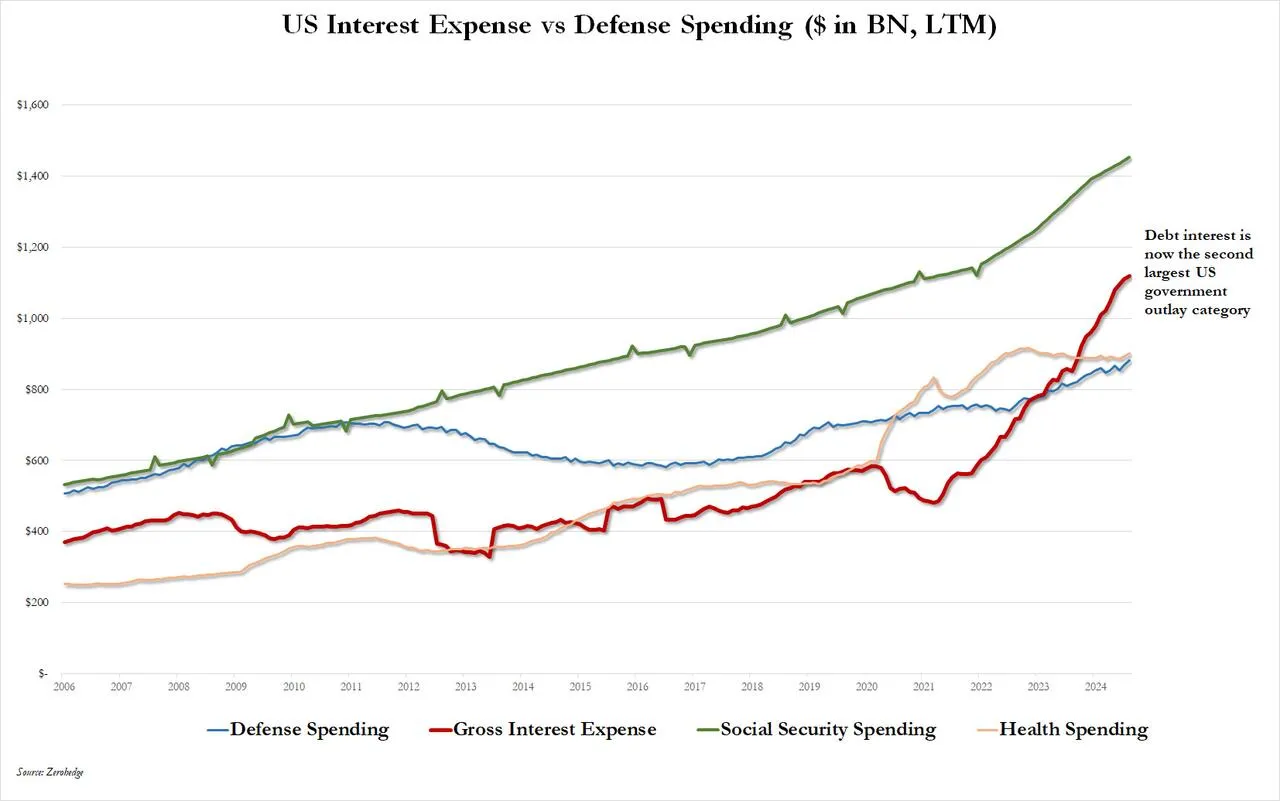

As of this year, gross interest on U.S. debt has exceeded spending on defense, income security, health, veteran's benefits, and even Medicare, making it the second-largest expense for the U.S. government—trailing only Social Security, which stands at approximately $1.5 trillion annually:

As of this year, gross interest on U.S. debt has exceeded spending on defense, income security, health, veteran's benefits, and even Medicare, making it the second-largest expense for the U.S. government—trailing only Social Security, which stands at approximately $1.5 trillion annually:

About the author