This is part one of a series on COMEX gold futures contracts, for those interested to reach a proper understanding on this section of the gold market. In this first part we will discuss the history of futures trading and the basics of COMEX gold futures.

COMEX is the commodity exchange administered by CME Group.

The History of Futures Trading

According to various sources the first traces of futures trading have been found in ancient Greece, medieval Europe, and seventeenth-century Japan. Though futures markets as we know them today emerged from North American commodity trade in the nineteenth century.

In 1848 workers completed the 96 miles long Illinois and Michigan Canal that connected the Chicago and Illinois Rivers, thus linking the Great Lakes to the Mississippi River. Through this canal Chicago was established as a trading hub just before railroads arrived. The agricultural harvest of the Illinois River valley that previously flowed downstream to St. Louis and New Orleans was now transported to Chicago and onwards to New York through the Erie Canal.

Because of to the local weather in Chicago, temperatures swung from hot humid summers to bitter cold winters. At times, merchants couldn’t transport crops produced in the river valley to Chicago, as the river and canal were frozen. Corn was stored in cribs until the ice melted. As soon as the waterways opened the markets in Chicago were overwhelmed by supply and prices tumbled.

Amidst these dynamics a merchant offered a producer in Chicago to deliver 3,000 bushels of corn three months later for 1 cent cheaper than the prevailing spot price. The producer agreed, and so on March 13, 1851, the first such timed contract was signed—or so the story goes. Some years later, in 1865, farmers, producers, merchants, and speculators began trading standardized futures contracts on the Chicago Board of Trade (CBOT). The first futures exchange that is similar to exchanges as they are currently organized with a clearing house appeared in 1891 in the United States.

Since Nixon closed the gold window in 1971, ending the era of fixed exchange rates, the underlying assets of futures expanded from commodities to currencies, stock indices, bonds, Eurodollars, crypto, and more. Gold futures were launched in 1974.

An Introduction to Gold Futures

A futures contract represents an agreement to make or take delivery of a specific quantity and quality of an asset at a specified future delivery month, with price as the only variable. Notwithstanding certain futures contracts are cash settled. Futures are standardized so they are fungible and can be centrally cleared.

By and far, the most traded gold futures contract globally is listed on the COMEX (the Exchange hereafter), a subsidiary of CME Group. Below is a summary of the specifications of this contract:

Contract size: 100 troy ounces

Price quotation: US dollars per troy ounce

Product code: GC

Listed contracts: Monthly contracts are listed for the nearest 3 consecutive months, any February, April, August, October in the nearest 23 months, and any June and December in the nearest 72 months.

Settlement method: Physical delivery at COMEX approved depositories in New York or Delaware.

Delivery period: Delivery may take place on any business day of the delivery month.

Contracts are not listed for every month six years into the future, as to concentrate trading in fewer months which improves liquidity. Delivery can be made in one 100-ounce bar or three 1-kilogram bars, having a fineness of no less than 995 parts per thousand. Of course, the buyer only pays for fine ounces delivered. The most actively traded months are February, April, June, August, and December.

Nowadays all trading is done electronically through CME’s Globex platform. Every contract month is traded through an order book where buy and sell orders are connected. Market makers—among other traders—quote limit order bids to signal the market at what price and in which quantity they want to buy, and limit order asks to signal at what price and in which quantity they want to sell. All together these limit order bids and asks comprise the order book. Market takers submit “market with protection orders” (simulating plain market orders), notifying the Exchange in what quantity they want to buy or sell at the best price. Once the Exchange has matched market to limit orders, they are being filled and the price moves.

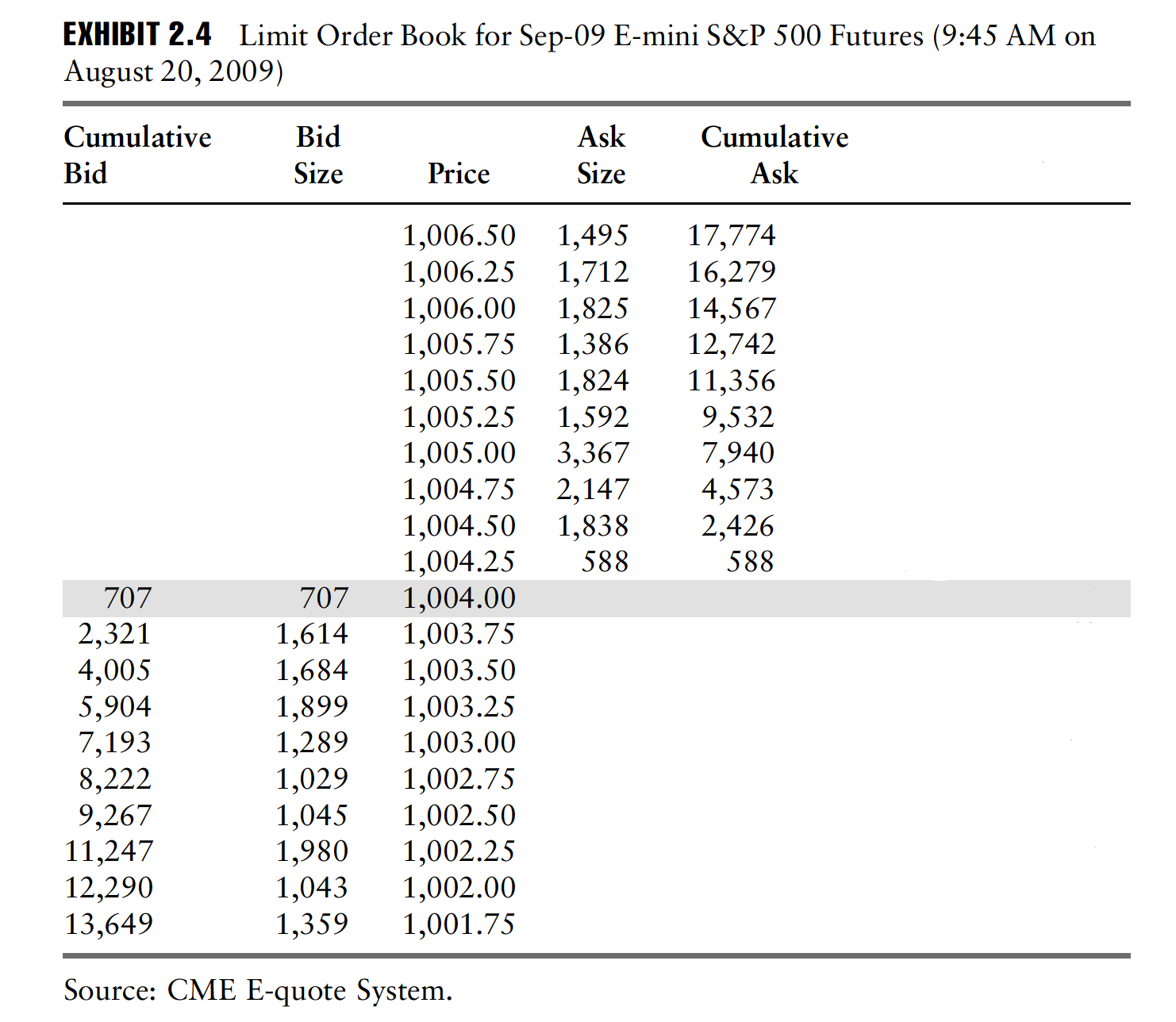

Example order book of S&P 500 index futures.

Above is an example order book of S&P500 index futures (the September 2009 contract), courtesy of The CME Group Risk Management Handbook. The highest bid in this example is $1,004.00 dollars, and the lowest ask is $1,004.25. The bid-ask spread and the cumulative order quantities disclosed indicate market liquidity (the ease with which an asset or security can be bought or sold without significantly affecting its price).

Every futures trade involves a buyer and a seller signing one or multiple contracts to take and make delivery in the future. Opening a position is referred to as “buy long” or “sell short.” A contract’s trading volume is set by how many contracts are signed during a particular timeframe. The open interest (OI) reflects how many contracts are outstanding at any given point in time. The number of outstanding longs and shorts for any contract is equal, because for every buyer there is a seller. On the COMEX both volume and OI are counted single sided. In example, an OI of 16 means there are 16 longs and 16 shorts.

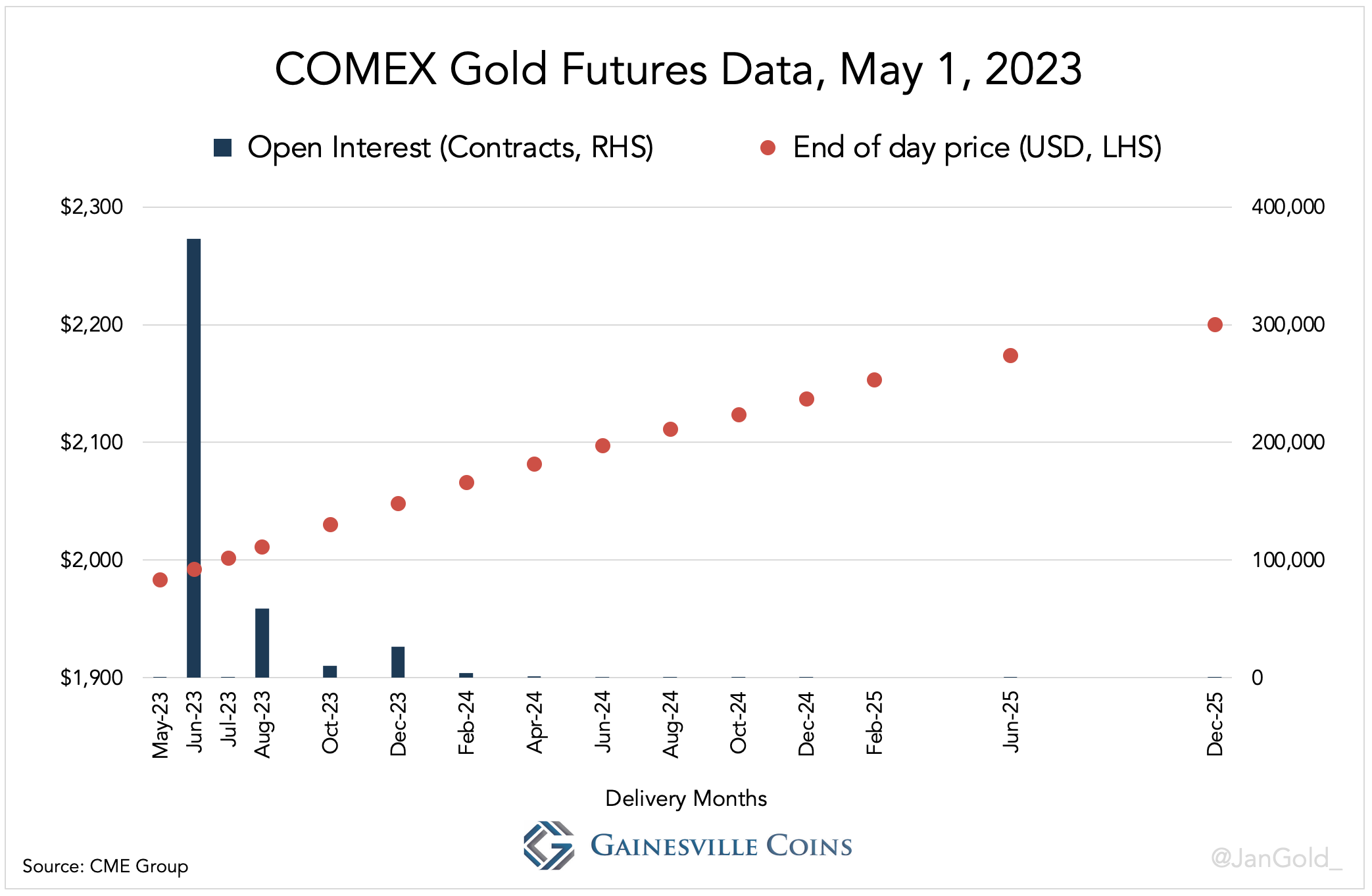

Charting the prices of listed contract months reveals the futures curve.

COMEX gold futures prices three years out on May 1, 2023, and the open interest for every contract month. As time progresses new contracts are listed at the end of the futures curve, while nearby contracts at the front of the curve expire and are delisted.

The futures curve shows if contract months trade at a premium or discount to the spot price. If the curve slopes upward (successive months are priced higher) the futures market is said to be in “contango.” In contrast, if the curve slopes downward the market is said to be in “backwardation.” Which variables shape the curve differs per asset. The shape of the gold futures curve can depend on storage costs, the US dollar interest rate, the gold lease rate, expectations about the gold price in the future, and scarcity in the spot versus futures market.

Important to understand is that futures prices do not determine the spot price of any asset in the future. For some assets, such as eggs, futures prices do reflect the market’s forecast of the spot price in the future, which may or may not turn out to be accurate, but for other assets the market composes the curve based on alternative models.

During business days the spot gold price in the wholesale market fluctuates based on supply and demand in the spot market, and the price of every contract month fluctuates based on supply and demand of that contract. Consequently, the form and price level of the curve continuously change. Gold futures are usually in contango though.

The gold spot price and futures prices are interlinked through arbitrage. Suppose demand for a nearby gold futures contract is strong and it trades rich relative to spot metal. An arbitrager will borrow dollars to buy spot gold and simultaneously sell short futures, whereby he increases the spot price and decreases the futures price until the gap is closed. To materialize his return, the arbitrager stores the gold, waits until the futures contract expires, and makes delivery with the gold bought in the spot market. His profit is the difference between the spot price paid and futures selling price, minus the costs of financing and storage.

This example illustrates how arbitragers cause futures prices to converge to the spot price when they mature. The price of an expiring futures contract can’t be far off from the spot price or arbitragers jump in and close the gap. In practice, even the threat of delivery causes the spot and futures market to converge. Arbitragers don’t always make or take physical delivery because it can be more convenient to strike a profit by closing their positions before futures expire.

The two main categories of futures traders are hedgers and speculators. Hedgers use futures to manage price risk; speculators accept that risk in an attempt to profit from price swings. For gold industrials, like gold miners and jewellery fabricators, an incentive to sign a futures contract can be to lock-in a price to buy or sell gold in the future. A miner may want to square his books by hedging the risk that the value of his output will collapse in the future. He will sell short to assure production can be sold at a fixed price in the future. Speculators try to make money by guessing the direction of prices, including futures prices. If a speculator makes the assessment that futures are cheap, he will buy long futures anticipating the price of the contract to rise.

The Role of the Clearing House

Futures markets serve their users best when there is sufficient liquidity, demanding traders to open and close positions smoothly. Closing a futures position is done by taking an opposite position of the same size and contract that offsets the former. Before the clearing house arrived in the late nineteenth century it was cumbersome for traders to close positions. Back then, if Tom sold short 5 corn futures to Bob and bought long 5 of the same contracts from Alice, Tom’s net position was zero, but he still had two open positions. For Tom to close he needed to find Bob and persuade him Alice was his counterparty. Bob might have agreed, or not if Alice previously defaulted on him when he stood for delivery.

To default was tempting, for example, if Alice was holding a short contract that expired while the prevailing spot price was higher than the price written on her contract. Selling her merchandise in the cash market produced more revenue than making delivery. For longs it was attractive to default if their futures matured and the spot price was below their contractual agreement.

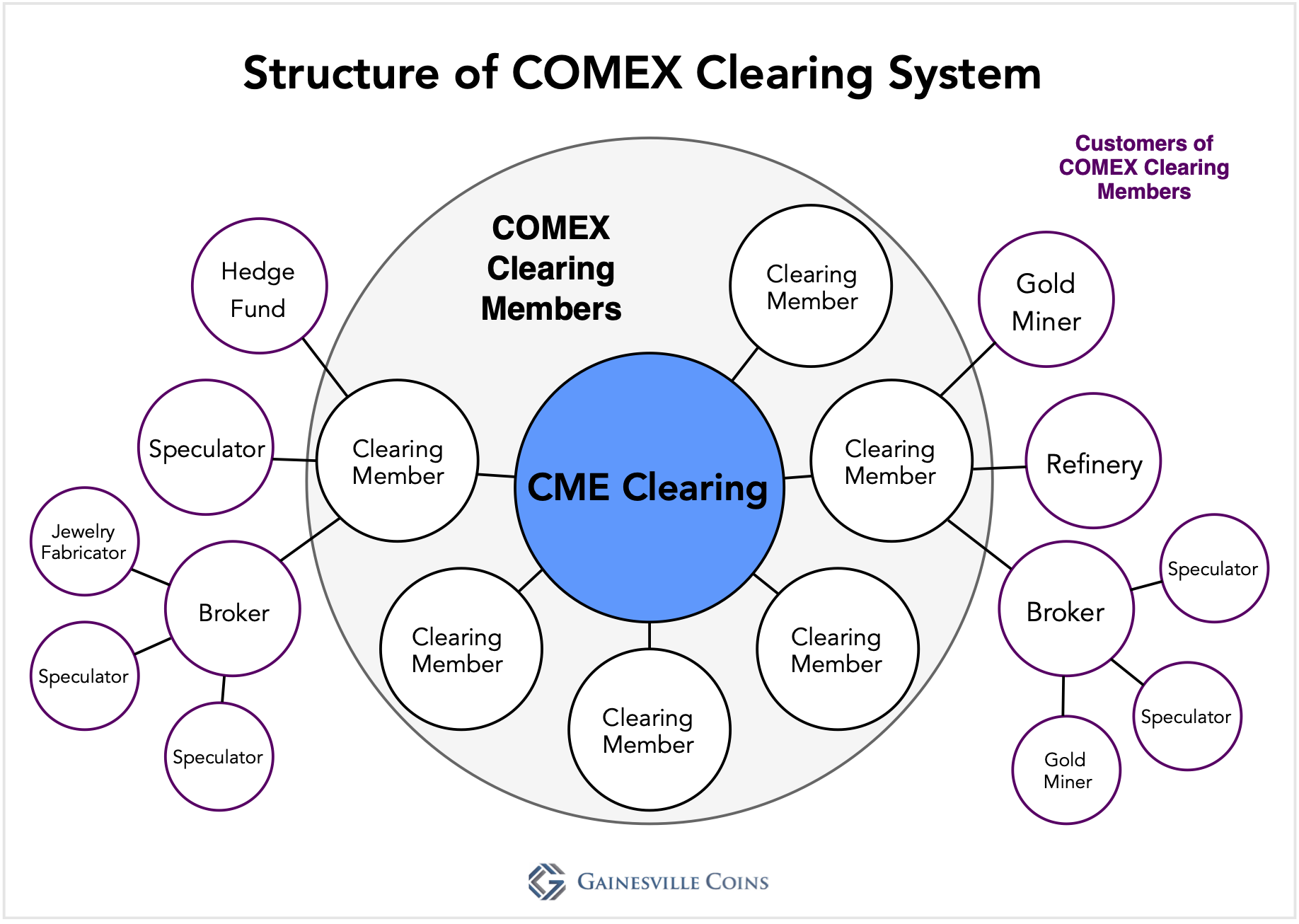

Without a clearing house futures trading is intricate and carries a higher risk for participants that the other side defaults on its commitment to make or take delivery. Trading is alleviated by the clearing house as it steps in as the buyer to every seller and seller to every buyer after orders have been filled, to streamline to process of offsetting contracts. Additionally, risk is ringfenced by recurrently settling margin deposits between traders based on price movement, limiting exposure on positions before anyone can default. That’s the easy way of describing it—believe it or not. In reality it’s more complicated as the clearing house only deals with clearing members that broker between their customers and the clearing house.

To reach a basic understanding of the clearing house we will examine it by example of the COMEX. Exchanges under the umbrella of CME Group (COMEX, NYMEX, CBOT, and CME) utilize the services of CME Clearing instead of running separate clearing houses. It follows, in terms of flow of funds and assets, that CME Clearing is the clearing house connecting all COMEX clearing members, which are brokerage firms or entities such as banks that offer brokerage services as an ancillary business. All participants trading COMEX gold futures are connected to a clearing member. For the sake of simplicity, we will ignore that clearing members can trade for their own account in this article.

CME Clearing connects all COMEX clearing members. Customers of clearing members can be individual speculators, investment funds, industrials, brokerage firms, etc.

Central clearing induces a chain of responsibilities. CME Clearing exclusively deals with clearing members, holds them accountable for all their positions, and routinely performs due diligence on them. In turn, clearing members review their customers’ creditworthiness before accepting a trade relationship.

After buy and sell orders have been matched on Globex, the clearing house becomes the seller to every buyer and the buyer to every seller. CME Clearing will close positions of traders that are short and buy in the same size and contract or those that are long and sell in the same size and contract.

For positions opened through clearing members, long or short, the clearing house requires traders to make an initial margin deposit to cover any losses they may incur. Traders deposit margin at clearing members, which clearing members deposit at CME Clearing. At the time of writing (May 2023), the initial margin requirement for a clearing member is $8,300 dollars per gold contract, though they may ask their customers for a higher margin deposit. In addition, each clearing member, according to its proportionate share in the system, has to make a contribution to CME Clearing’s guaranty fund designed to cover potential losses beyond margin deposits.

Margin accounts at the clearing house are marked to market twice a day—at the “settlement cycle”—to prevent the accumulation of debt obligations. When the price of a futures contract has risen margin funds flow from clearing members that are net short to clearing members that are net long. When the price has fallen funds flow in the opposite direction.

To make sure margin funds keep flowing throughout the system, traders get a margin call if their accounts fall below the maintenance level: either they deposit more cash to hold on to their positions or get liquidated (force closed) by their clearing member. In case traders choose to cough up more margin these funds become available to those on the other side of their positions via the clearing house, confining risk between market participants.

Clearing members that can’t meet their obligations to the clearing house may be declared to be in default, triggering a series of unified measures to restore stability. MF Global’s default in 2011 was the most recent.

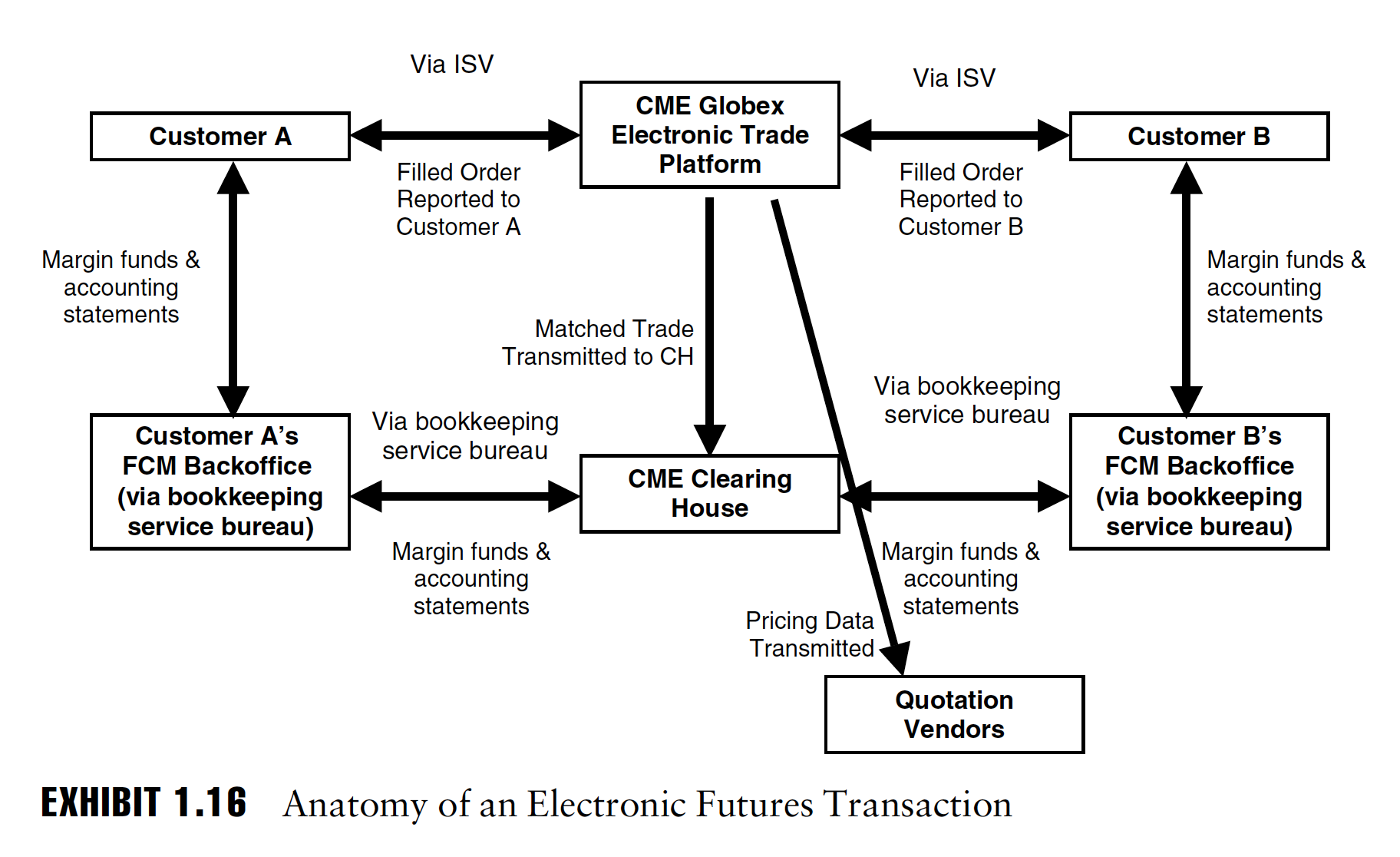

The anatomy of an electronic futures transaction, courtesy of The CME Group Risk Management Handbook. Clearing members must be registered as Futures Commission Merchants (FCM). ISV stands for independent software vendor.

All in all, margin deposits disincentivize default and marking positions to market further attenuates risk. Through margin calls, a gold miner that is short futures and confronted with a rising price as delivery approaches will have to wire more cash to his clearing member or will be liquidated. In both scenarios risk is diminished.

Let’s have a look at a few hypothetical trades that help us understand how everything works in practice.

Suppose a Refinery has 100 ounces of physical gold inventory that it wants to hedge and sells short 1 contract deliverable in June 2023 at a price of $2,000 dollars per ounce. On the other side a Speculator buys longs, though the clearing house promptly steps in between. Both the Refinery and Speculator are required by their respective clearing members to make a margin deposit of $10,000. Initial margin requirements are deposited at CME Clearing, while the remaining $1,700 in excess margin is held at the clearing members.

$10,000 (margin deposit) – $8,300 (initial margin requirement) = $1,700

The following day the price of the contract rallies and the settlement price hits $2,010. At the settlement cycle $1,000 is transferred by the clearing house from the Refinery’s clearing member account to the Speculator’s clearing member account.

1 (contract) * 100 (ounces) * $10 dollars ($2,010 – $2,000) = $1,000

Subsequently, the Refinery’s clearing member will deposit $1,000 from its excess margin to its account at the clearing house to keep up its initial margin requirement. The Speculator’s clearing member will be able to withdraw $1,000 from its account at CME Clearing to back its liability to the Speculator.

Suppose the Speculator wants to close as the price went up. He takes an opposite position of the same size and contract: he sells 1 June 2023 contract. The clearing house records it is both long and short 1 June 2023 contract against the Speculator and offsets his positions. Now that the Speculator has closed he can withdraw $11,000 from his clearing member.

$10,000 (margin deposit) + $1,000 (profit) = $11,000

Simplified, that’s how the funds flow.

We can also use our example to illustrate how the Refinery’s textbook hedge works. The Refinery holds 100 ounces of physical gold inventory, which is a long position, but didn’t want to be exposed to the gold price. She sold short 100 ounces of the nearest active contract (the “near month”), as that contract’s price was the closest to the spot price. Then the gold price went up by $10 per ounce, increasing the value of the Refinery’s inventory by $1,000 ($10 times 100 ounces) and decreasing the value of her short position by $1,000. On a net basis the Refinery was able to eliminate price risk.

Rolling, Delivery, and Leverage

The Refinery doesn’t want to make delivery as her motivation for shorting the June 2023 contract is hedging inventory. What she will do is rollover her position by closing her June 2023 short position before it expires, and open a new short position in the next active contract (August 2023).

Disregarding the bid-ask spread, shorts rolling in contango earn the roll yield because they buy the expiring contract (to close) and sell short the next active month at a higher price. The difference in prices between the contracts—regardless of what the prices are—eventually narrows as contracts converge to spot: this is where the yield comes from. Longs earn a negative yield when rolling in contango, while they earn a positive yield in backwardation (shorts lose in backwardation).

During the rolling process the price of the expiring contract is influenced by the ratio between how many positions are closed versus how many stand for delivery. To demonstrate, when more shorts want to make delivery than longs take delivery, selling pressure mounts by the longs that want to exit. The longs closing have to sell at a price which new longs entering feel comfortable to take delivery at.

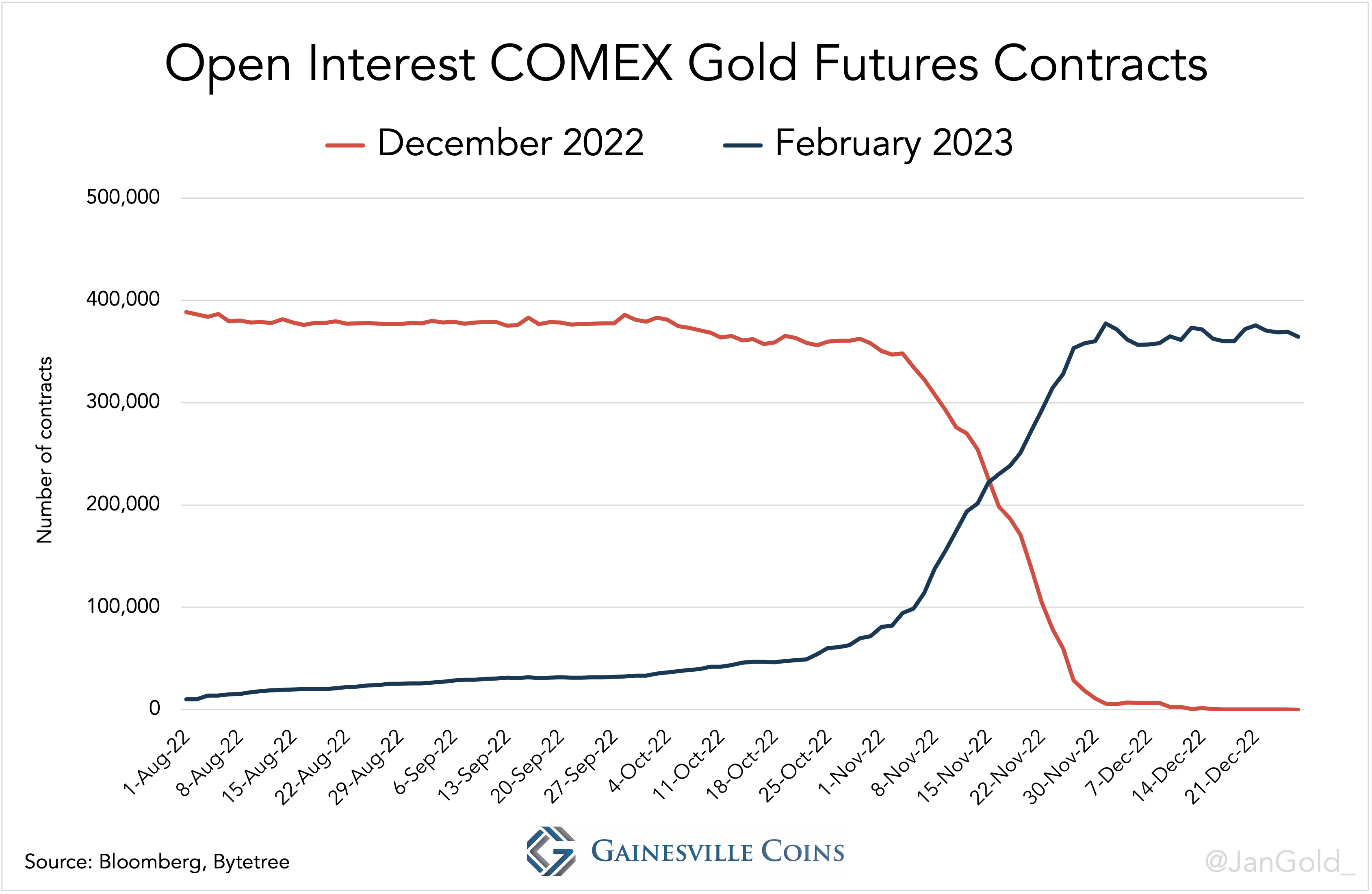

Much trading on the COMEX is similar to the example with the Refinery and Speculator, explaining why the bulk of OI is in the near month (see the first chart) and only a small percentage of traders prefer delivery. On average, two weeks before a near month contract expires most of the OI has been rolled into the next active month, which then becomes the near month.

As an example, on November 16, 2022, most of the outstanding positions were rolled from the December 2022 contract into the next active month, February 2023.

Leaving positions open at expiry will lead traders into the delivery month. The shorts initiate the delivery process, after which the clearing house assigns shorts to longs to transfer a “warrant”, a warehouse receipt. In possession of the warrant, metal can be withdrawn from the vault or resold in the futures market.

Another aspect of futures is that the margin deposit is much lower than the notional value of the contract, effecting leverage. In our example of the Refinery and Speculator the leverage is approximately 20. The notional value of a contract is 100 (ounces) times $2,000 (price), which compares to a sum of $200,000, divided by $10,000 (margin), is 20.

Futures trading comes with a warning due to the amplification of profits and losses. The Speculator made $1,000 in a day from a 0.5% gain in the gold price by opening a long position in futures with $10,000. But he would have made a big loss, and possibly got liquidated, if the price slipped by just a few percentage points.

To lower their leverage some traders deposit margin on top of what is asked by their clearing member, to avoid getting liquidated overnight or having to wire funds again and again when the market moves against them.

Conclusion

The essence of futures trading is that contracts come into existence if buyers and sellers open positions, and contracts are cancelled if traders take offsetting positions, or are terminated by physical delivery. Likewise, the price moves by buyers and sellers opening positions, and by traders closing positions or getting liquidated.

To get more feeling for trading futures you can open a practice account on CME Group’s website.

In forthcoming articles details about the futures curve, delivery process, position limits, Commitments of Traders (COT) report, default protocols, Exchange for Physical (EFP), and the impact of futures trading on the spot price will be fleshed out. If you have any questions or requests, please drop them in the comment section below.

In addition to the sources disclosed below I have consulted William Purpura, CEO at Great Lakes Trading Group LLC and Chairman of the COMEX Governors Committee, and CME Group’s Market Risk and Clearing House Financial departments for writing this article.

Sources

- Beale, R (1985). Trading in Gold Futures

- CME (2006). An Introduction to Futures and Options

- CME Group (2013). A Trader’s Guide to Futures (link)

- CME Group (2018). The CME Clearing Risk Management and Financial Safeguards (link)

- CME Group (2021). COMEX Gold Warrants (link)

- CME Group (2022). Precious Metals Physical Delivery Process (link)

- CME Group (2023). COMEX Rulebook (link)

- CME Group (2023). Demo Trading (link)

- Geman, H. (2005). Commodities and Commodity Derivatives

- Greyserman, A., Kaminski, K. (2014). Trend Following with Managed Futures

- Labuszewski, J. W., Nyhoff, J. E., Co, R., Peterson, P. E. (2010). The CME Group Risk Management Handbook

- Lambert, E. (2010). The Futures

- Santos, J. (2008). A History of Futures Trading in the United States (link)

About the author