The transition from fossil fuels to electrified transportation and renewable energy is predicated on two assumptions: that there will be enough raw materials to make this change; and that eventually we won’t require fossil fuels anymore. Both of these claims are false.

The United States and its allies, such as Canada, the UK, the European Union, Australia, Japan and South Korea, face a dilemma when it comes to the global electrification of the transportation system and the switch from fossil fuels to cleaner forms of energy.

On the one hand, we want everything to be clean, green and non-polluting, with COP26-inspired goals of achieving net zero carbon emissions by 2050; and several countries aiming to close the chapter on fossil-fuel-powered vehicles, including the United States which is seeking to make half of the country’s auto fleet electric by 2030.

Yet in going “all-electric”, we are also hurting ourselves, because by lessening investment in fossil fuels, we are making the price of fuel (crude oil and its refined products, like gasoline) and petroleum by-products, of which there are literally thousands, more expensive. We’re heading down the road of spending more money on renewables than fossil fuels, but at what cost to the consumer?

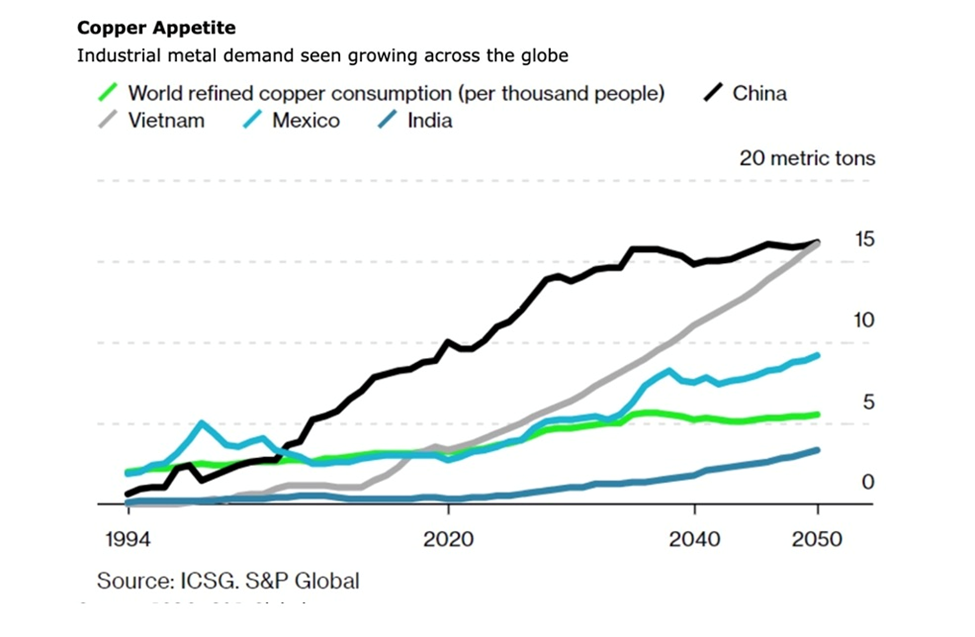

Electric cars continue to be out of most people’s price range. And as we place more emphasis on a green economy, we are putting extreme pressure on several of the metals required, including copper, zinc, lithium, nickel and graphite.

Copper and other industrial metals were already in high demand, before the world embarked on an electrification and de-carbonization drive. The planet is using more natural resources than nature can provide. Arguably, the shift to EVs and renewables will only exacerbate this problem of resource depletion.

In this article we are identifying “the elephant in the electrical room”, fossil fuels, and calling for an intelligent discussion of what is the right mix of oil and gas versus electrification metals, going forward.

Ubiquitous oil and gas

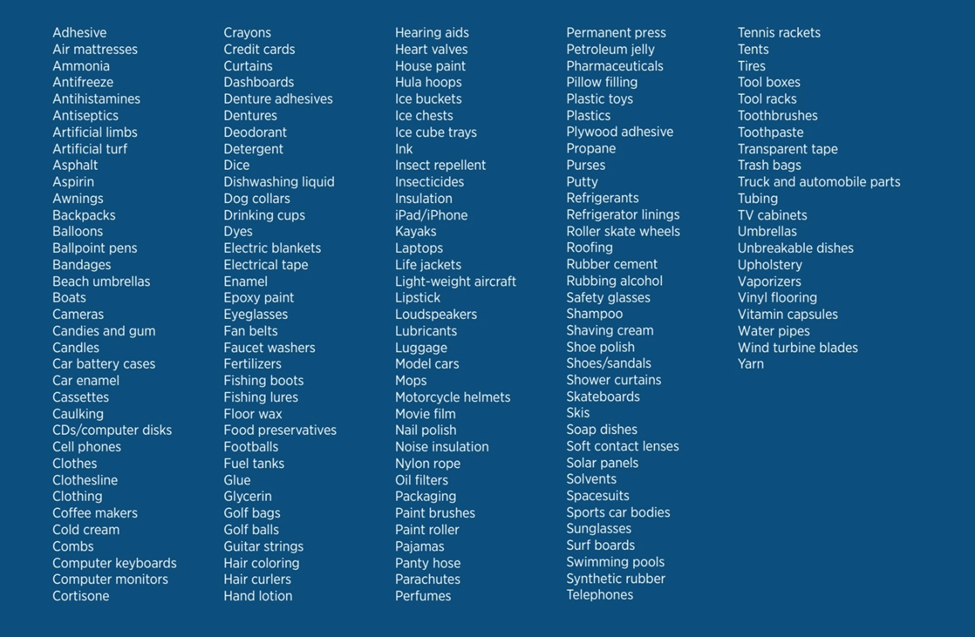

Transitioning from an oil-based economy will not be easy, because of our dependence on crude oil and its derivatives. The table below from the U.S. Department of Energy lists 161 products made from oil and natural gas. From cold cream to floor wax, dentures to pillow filling, many of our everyday items started off as primordial black goop.

A LinkedIn post from energy consultant Steve Pryor states that one 42-gallon barrel of oil creates 19.4 gallons of gasoline. The rest is used to make things. Below is a partial list of 6,000 petroleum-based items. Another interesting fact: Each American consumes 3.5 gallons of oil and more than 250 cubic feet of natural gas per day.

Products made from oil and natural gas. Source: U.S. Department of Energy. Click for larger image

Products made from oil and natural gas. Source: U.S. Department of Energy. Click for larger image

Most people are aware that cell phones contain rare metals. What they may not realize is that without oil & gas, hand-helds, laptops and other computers would not exist. Made of glass, metal, plastic, lithium and silicon, they all require fossil fuels to mine, process and manufacture.

Source: Canadian Association of Petroleum Producers (CAPP)

Source: Canadian Association of Petroleum Producers (CAPP)

According to Real Clear Energy, While some are chemical derivatives of fossil fuels, all depend one way or another on their combustion for electricity generation, process heat or transportation.

Unless non-petroleum-based alternatives to these products are invented, society will continue to rely on oil and gas extraction.

Clean-energy advocates say that tackling transportation, one of the largest sources of greenhouse gas emissions, is an effective means of fighting global warming. The electrification of the global transportation system is seen as the lowest-hanging fruit, and by doing away with tailpipe emissions, the air will get cleaner.

But many fail to appreciate that unless the electricity that goes into the batteries is clean, cars, trucks, planes, ships and trains will continue to need fossil fuels. Globally, most of the energy used to charge the batteries that go into EVs, will come from coal and natural gas. Facilities that produce wind, solar, nuclear and hydro power, are also reliant on fossil fuels, used to mine and manufacture their component parts.

As Real Clear Energy reminds us, the role of fossil fuels in manufacturing and farming (i.e. natural gas to make fertilizer, and diesel fuel to run equipment) is rarely highlighted. For example:

The manufacture of cement is one of the most energy intensive processes, requiring the mining of limestone and other minerals that are eventually heated in kilns at temperatures of 2,700 degrees Fahrenheit…

Paints, resins, fiberglass, coatings, varnishes, adhesives, and thousands of other materials are all made from fossil fuels. It is likely the clothing that you are wearing now was made using fossil fuels. In fact, most carpets, fabrics, coatings, cushions, upholstery, drapes, spandex and other textiles are made with the help of fossil fuels.

Fossil fuels are used as raw materials in the production of many chemicals and plastics. Lightweight, durable and versatile, plastics are used in a wide range of products, from packaging and consumer goods to automotive parts and medical devices…

Fertilizers – produced with the help of natural gas – replenish the soil with essential nutrients like nitrogen, phosphorus, and potassium, improving soil structure and fertility. Fertilizers have played a crucial role in meeting the global food demand by increasing crop yields by as much as 50 percent.

Source: Visual Capitalist, Canadian Association of Petroleum Producers (CAPP)

Source: Visual Capitalist, Canadian Association of Petroleum Producers (CAPP)

To my knowledge, there is no plan to wean the world off fossil fuels and their derivatives. In fact, most governments have set arbitrary “net zero” dates without filling in the blanks as to how this will be accomplished. Currently the trend is to accelerate spending on renewables and de-invest in fossil fuels.

Our recent article showed there were three records set in 2022.

Green energy investment matches fossil fuels for the first time

Last year the amount of money invested in decarbonizing the world’s energy system surpassed a trillion dollars for the first time. 2022 was also the first year that the $1.1 trillion which poured into the energy transition matched the $1.1T global investment in fossil fuels.

Another record: the year-on-year increase of >$250 billion (2022 vs 2021) was the largest ever jump, according to a recent Bloomberg story. While there has been $6.7 trillion invested in the energy transition since 2004, the article points out that it took eight years to reach the first trillion, less than four years to reach the next trillion, and under one more year to reach the latest trillion. In other words, the investment in green energy is accelerating dramatically.

Unsurprisingly, renewable power and electric vehicles received the lion’s share of the investment dollars, with more than 350 gigawatts of assets built and sales of >10 million EVs globally. Electrified transport is growing faster than renewable energy. Of the close to $500 billion in transport dollars invested, $380 billion went to passenger EVs. Other sectors received relatively less, with public charging infrastructure seeing $24 billion, $23B spent on two- and three-wheelers, $15B flowing to electric buses, and commercial vehicles getting $8 billion.

What has happened to fossil fuels investment, in the meantime?

Global energy investment saw its biggest fall on record in 2020 when the covid-19 pandemic hammered demand, while a push for energy transition to meet greener targets pulled more funds into renewable resources. (Reuters, Sept. 28, 2021)

The article said the International Energy Agency has called on investors to stop funding new fossil fuel projects to reach net zero emissions by 2050.

De-investment in the sector, combined with oil supply disruptions due to the war in Ukraine, and robust demand from post-pandemic economic recovery, pushed crude oil to a five-year high of $115 a barrel in April, 2022, before falling back to the current $79, at time of writing.

Source: Investing.com

Source: Investing.com

Last year, the head of Saudi Aramco told Reuters the world is facing a major oil supply crunch, with most companies afraid to invest in the sector as they face green energy/ ESG pressures.

Amin Nasser, head of the world’s largest oil producer, said the fear is that oil companies will have “stranded assets”, referring to the notion that significant oil and gas reserves will not be used because they are no longer needed.

However, Nasser also said that mis-steps during the global energy transition would only encourage greater use of coal by many Asian countries. “For policymakers in those countries the priority is to put food on the table for their people. If coal can do it for half the price they will do it with coal.”

(We also saw this in Germany, before Russia attacked Ukraine, precipitating the current energy crisis. The country tried to switch too soon to renewable energy, retiring its nuclear and coal power plants, only to find that the wind and sun didn’t produce enough electricity. Germany had to rely on Russian natural gas and the burning of lignite coal to keep the lights on and homes/ businesses heated throughout the winter.)

Last May, as the world was deriding coal as a relic of the 20th century, US coal investors were reaping triple-digit gains, due to tight supplies and increased demand, amid skyrocketing natural gas, a competing fuel.

Global coal use was set to rise by 1.2% in 2022, surpassing 8 billion tonnes in a single year for the first time and eclipsing the previous record set in 2013, according to Coal 2022, the IEA’s latest annual market report on the sector.

Back to oil versus renewables, though, the trend is clearly with the latter. According to research by BloombergNEF, to reach net zero emissions by 2050, investment in renewable sources needs to be quadruple the rate of finance flows to fossil fuels, over the next decade.

We’re talking an average of $4 invested in renewables for every $1 allocated to high-polluting energy supplies — compared to the current ratio of 90 cents to a dollar.

(For context, that is nearly five times US GDP of USD$23.3 trillion (2021), and over 50 times Canada’s $1.98T GDP.)

Without copper there is NO electricification

Commodities consultancy Wood Mackenzie estimated that nearly 10 million tonnes (9.7Mt) of new copper supply will be needed over the next decade, from projects that have yet to be put into development.

As we have pointed out, it’s the equivalent of putting a new Escondida copper mine, the biggest in the world, into production each year.

There are really only three ways for the mining industry to get this additional metal. First, they can increase production from existing mines; this often involves “going underground”, digging beneath the existing open pit to access more ore. An expansion to the existing concentrator or building a new one, is sometimes needed.

Second, they can expand their mines laterally, going after resources that weren’t part of the initial mine plan because they were less accessible, or un-economic. Third, they can explore for new mineral deposits, either internally, or working with junior mining companies, which have the exploration expertise to bring a deposit forward to the point when it can be sold to a major. Obviously option three, known as greenfield exploration, is more difficult, costly, and carries higher risk than options one and two, called brownfield exploration.

Over the past 10 years, greenfield additions to copper reserves have slowed dramatically. S&P Global estimates that new discoveries averaged nearly 50Mt annually between 1990 and 2010. Since then, new discoveries have fallen by 80%.

With so few new projects in the works, and as existing sources dry up, mine supply growth will peak around 2024, resulting in a historic deficit of 10 million tons (11,023,100 tonnes) in 2035.

BloombergNEF predicts that by 2040, the mined-output gap (mines currently produce about 21Mt annually) will reach 14Mt, a shortfall that, without new supply, will have to be filled by recycling metal.

Goldman Sachs says that mining companies will need to spend about $150 billion in the next decade, to address an 8-million-ton deficit.

Chilean state-owned Codelco is also predicting an 8Mt gap, but the world’s biggest copper miner thinks it will come a year earlier, in 2032, as soaring demand continues to exceed new mine supply.

The International Study Group puts the coming deficit into perspective, noting that in 2021, the global copper shortfall was 441,000 tons, equivalent to less than 2% of demand for the refined metal, but enough to drive copper prices 25% higher. Using S&P Global’s forecast, 2035’s shortfall will be 10 times higher, at about 20% of consumption.

New deposits are getting trickier and pricier to find and develop. In Canada and the United States, there is a lot of anti-mining sentiment and politicians are beholden to these pressure groups. Here, it can take up to 20 years to build a mine, after all the stakeholders (including indigenous peoples and greens) have been consulted and the many permitting requirements, at the federal level in both countries, and the states and provinces have been satisfied. Overall it is getting harder, and taking longer, for new projects to be green-lit.

The United States has enough reserves of lithium, copper and other metals to build millions of its own vehicles, but opposition to new mines may force the country to rely on imports that could delay efforts to electrify its roughly 275 million cars and trucks.

Anti-mining decisions could slam the brakes on US electrification plans

One of two recent examples concerns Antofagasta’s Twin Metals copper and nickel mining project in Minnesota. On Thursday, Jan. 26, the U.S. Department of the Interior blocked mining in northeastern Minnesota for 20 years, driving a dagger into the heart of the project.

The proposed underground copper-nickel mine, had progressed to the point of a 2019 feasibility study. A coalition of groups opposing the mine then went to court to challenge a Trump-era decision that opened the door to the mine, located near a wilderness area.

In August of last year, an Antofagasta subsidiary sued the US government in a bid to revive the project, which Biden administration officials had blocked due to concerns it could pollute a waterway.

There is no doubt that the mine, if built, would have been a major domestic source of copper and nickel. According to Twin Metals, the minerals within the Maturi deposit, part of the Duluth Complex geologic formation, is one of the largest undeveloped deposits of its kind in the world, with more than 4.4 billion tons of ore containing copper, nickel and other strategic minerals.

The fact that these minerals are condemned to stay in the ground for the next 20 years, while the Biden administration makes all sorts of promises to meet green energy targets, is a policy failure at the highest levels. Biden has backed off his 2020 presidential campaign endorsement of the mining industry. Instead, the president has signaled he prefers to rely on allies for EV metals, such as Canada, Australia and Brazil.

‘Friend-shoring’ threatens Western metals supplies

In another hit to US mining, the Environmental Protection Agency this week banned the dumping of mine waste near Bristol Bay, Alaska, due to potential harm to the region’s sockeye salmon industry.

The decision effectively halts the large copper-gold mine being developed by the Pebble Limited Partnership, a subsidiary of Northern Dynasty Minerals. Northern Dynasty has been seeking to mine in the area for roughly two decades.

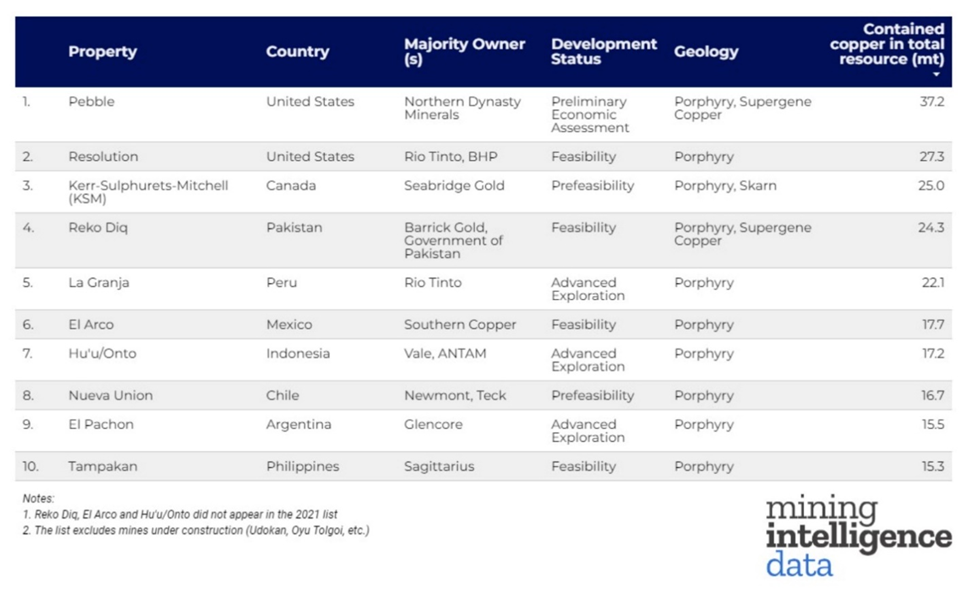

I couldn’t help noticing, on the same day this decision was announced, Mining.com published a list of the world’s biggest copper projects in 2023. The top of the list? Northern Dynasty’s Pebble project.

Source: Mining.com

Source: Mining.com

Number two is another controversial US mine that will likely never see the light of day. Mining giant Rio Tinto has been trying for over 25 years to launch Arizona’s Resolution copper project, one of the world’s largest underground copper reserves that reportedly has enough metal for 275 million electric vehicles.

However, despite spending $2 billion, Rio Tinto and minority partner BHP have little to show for it. In 2021, the project was put on hold due to opposition from native American groups and environmentalists. For an all-sides view of Resolution, read this New York Times article.

Numbers three, four and five on the Mining.com list are also highly doubtful, in my view. The KSM project in northwestern British Columbia, being developed by Seabridge Gold, has a 2019 price tag of USD$6 billion. With the recent spike in diesel fuel prices (the mine is too remote to connect to the electricity grid) and other mine cost inflation, I can’t imagine what it is now.

Reko Diq is in Pakistan, a country with a reputation not only for instability and devastating floods, but poor public infrastructure. Pakistan just suffered its second grid breakdown in three months, resulting in a loss of power to millions for over 12 hours, in the dead of winter.

According to Reuters, the outages add to the blackouts that Pakistan’s nearly 220 million people experience on an almost-daily basis. The government says it can’t afford to fix its aging electricity network. Not a good look for a country trying to attract mining investment from the likes of Barrick Gold.

The La Granga project is in Peru and only at the advanced exploration stage, meaning it has not even reached prefeasibility. Peru, as we have been reporting lately, has been rocked by a series of mining conflicts, as communities empowered by leftist ex-President Pedro Castillo, press their demands. Castillo was impeached in December and replaced by Vice President Dina Boluarte.

A wave of protests hit Peru’s major operations in early 2022, including Glencore’s Antapaccay Mine, Southern Copper’s Cuajone and MMG’s Las Bambas, the country’s fourth-largest copper mine and the world’s ninth biggest. The demonstrations threaten to block access to almost $4 billion worth of copper.

In January, Las Bambas stopped shipping copper concentrate due to security concerns. Glencore’s Antapaccay is also facing restrictions, Bloomberg said, adding the two mines together account for nearly 2% of the world’s copper output. They also share highway access to ports.

The Swiss firm said a group of citizens arrived at the site, demanded that the operation be stopped, and that Glencore issue a communique asking for the resignation of President Boluarte. The people then forced their way into mine facilities, stole workers’ belongings and set fire to the housing area. A week earlier, activists broke into the water plant and started a fire. A source said the plant provides drinking water for over 6,000 people in nearby communities.

Antapaccay had only been operating with 38% of its workforce due to protests. Following the attack, Glencore decided to halt operations.

Infrastructure needs

These obstacles to building new mines, alongside problems getting more ore out of existing mines, such as lower ore grades and the increased costs associated with mining, must be weighed against the much higher demand for metals and other raw materials that go along with electrification and decarbonization.

Building more mines? The devil is in the details

It’s hard to imagine the US being able to fulfill the Biden administration’s clean energy agenda without either a significant increase in critical metal imports that frankly may not be possible in current market conditions, i.e., the hostility between the United States and Russia and China; or executing a home-grown strategy to explore for and mine them in North America.

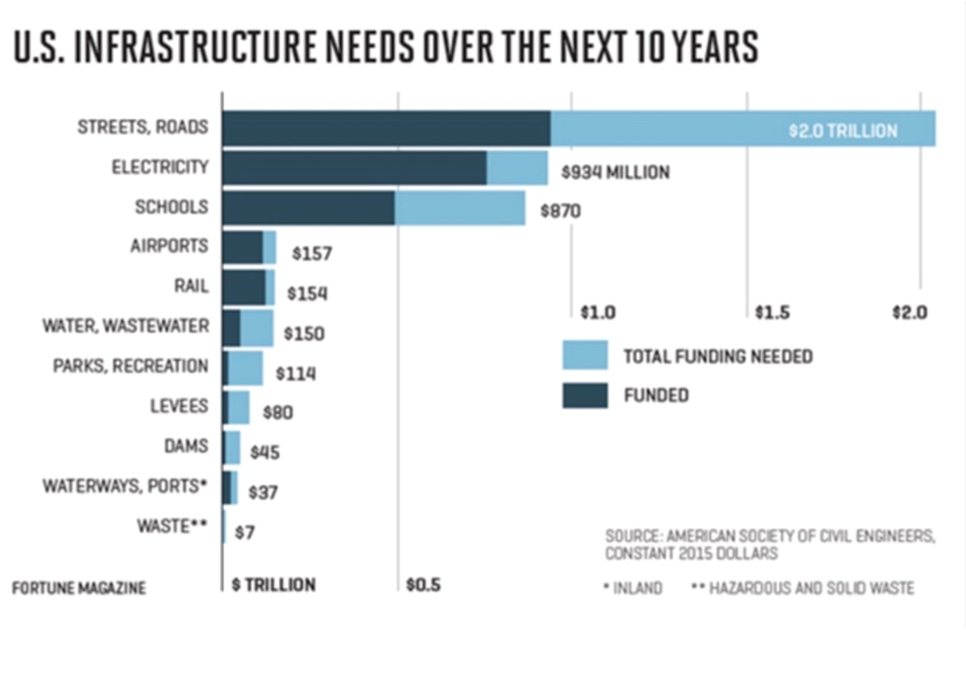

Many countries need to reduce their so-called “infrastructure deficits”. Basic infrastructure such as roads, bridges, water & sewer systems, has been poorly maintained, and requires hefty investments, measured in trillions of dollars, to repair or replace.

China, the world’s biggest commodities consumer, committed to spending US$2.3 trillion in 2022, on thousands of major projects, according to Bloomberg.

“Made in China 2025” was initiated in 2015 to reduce China’s dependence on foreign technology, promote Chinese manufacturers, and to change its perception as a low-end manufacturer.

China’s $900 billion “Belt and Road Initiative” is designed to open channels between China and its neighbors, mostly through infrastructure investments.

The United States is also pursuing its own $1.2 trillion infrastructure package, to be spent on roads, bridges, power & water systems, transit, rail, electric vehicles, and upgrades to broadband, airports, ports and waterways, among many other items.

The Infrastructure Investment and Jobs Act is the largest expenditure on US infrastructure since the Federal Highways Act of 1956. Rolled out over 10 years, it includes $550B in new spending. According to S&P Global, Among the metals-intensive funding in the legislation is $110 billion for roads, bridges, and major projects, $66 billion for passenger and freight rail, $39 billion for public transit, and $7.5 billion for electric vehicles.

An extension of the infrastructure buildout is the global transition towards a “green economy”, which can only be accomplished with renewable power, electric vehicles and energy storage technologies.

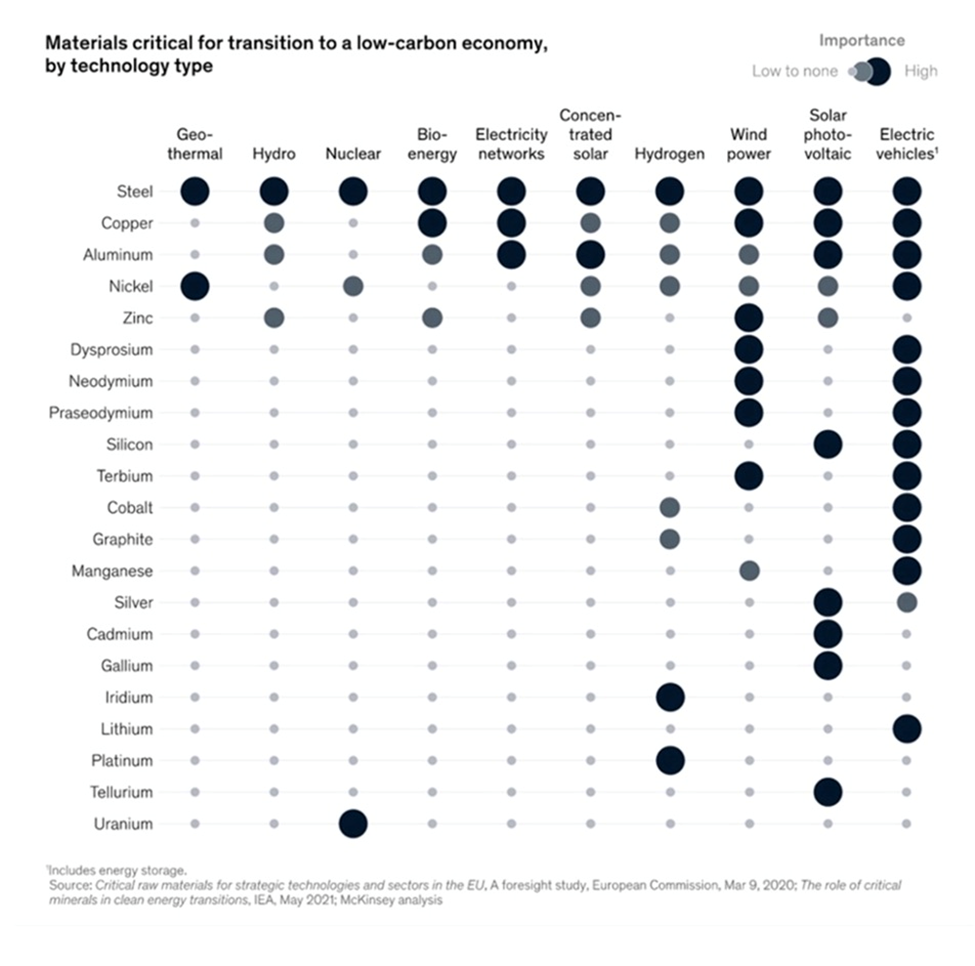

All of these require lots of minerals. The amount of raw materials we’ll need to extract from the Earth to feed this transition is staggering.

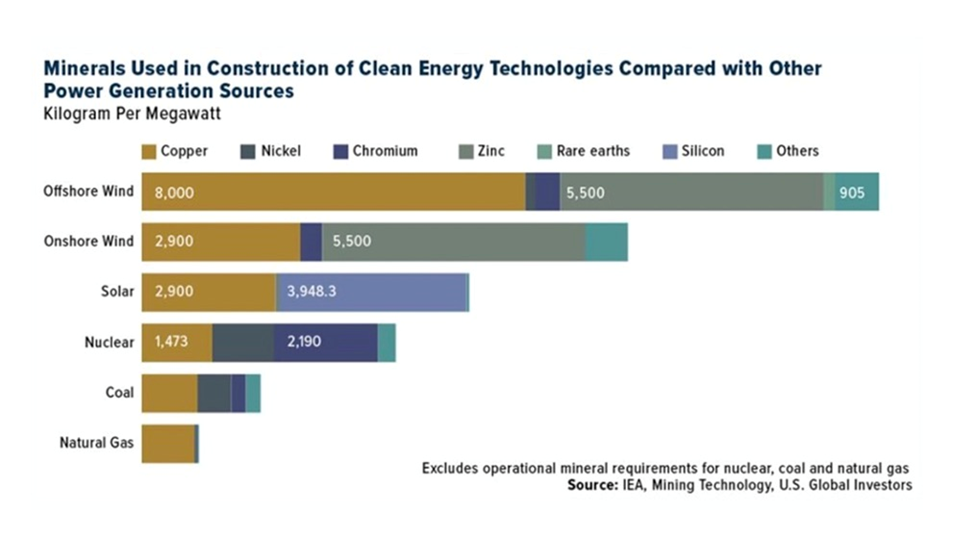

EVs require, on average, six times the amount of minerals such as nickel, copper, cobalt and lithium, as traditional gas-powered cars.

According to the International Energy Agency (IEA), an offshore wind farm uses nine times as many resources as a natural gas plant, with 8,000 kg of copper needed to produce just one megawatt of power (1GW = 1,000MW)

All in all, Bloomberg New Energy Finance estimates that the global transition will require about $173 trillion in investments over the next three decades; every commodity under the sun will be gobbled up.

Source: McKinsey & Company

Source: McKinsey & Company

Reality check

There are currently about 12 million electric vehicles on global roads compared to 1.4 billion vehicles run on internal combustion engines.

The world’s brightest minds not only have to come up with a plan to transition from ICEs to EVs, but how to fill all those new batteries with energy that is green, i.e., non fossil-fueled. Otherwise, the shift to electrification will have no net reduction of greenhouse gases.

Many countries will continue to require huge amounts of coal, oil and natural gas.

Unfortunately, the events of the past year have shown that it only takes a regional war in Europe to completely de-rail plans for decarbonization, as EU countries scramble to replace natural gas imports from Russia, and the prices of oil, natural gas and coal soar.

In 2021, Russia was supplying EU countries with 40% of their natural gas, with Germany the largest importer, followed by Italy and the Netherlands. That had dropped to around 17% by August 2022, according to EU figures. (BBC News, Jan, 26, 2023)

Japan, which has no natural resources of its own, in 2020 imported the majority of its oil from Saudi Arabia. And Australia, despite being a mining powerhouse (coal, iron ore), will by 2030 be 100% reliant on imported petroleum, due to the ongoing closure of its refineries.

Our addiction to oil means that hybrid vehicles, obviously requiring gasoline, are expected to continue outpacing electrics for years. The focus of government policies on electrification and renewables, at the expense of investment in traditional oil and gas, will keep the latter’s prices elevated, and the balance sheets of oil and gas companies fat.

Coal, the red-headed stepchild of the fossil fuel family, is making a comeback. Last summer Bloomberg reported that despite the world being in the grips of a climate crisis as temperatures soar and rivers run dry, it’s never been a better time to make money by digging up coal.

Coal use in the United States has dropped considerably over the years but it still burned 546 million tons in 2021, representing a tenth of total energy consumption, according to the US Energy Information Administration (EIA).

In Canada, despite a plan by the federal government to quit burning and exporting thermal coal by 2030, requests have been made by two provinces to keep their coal plants operational for another decade. Global News reported that Nova Scotia is negotiating an agreement in principle with Ottawa to keep its coal-fired electricity plants open until 2040. New Brunswick made a similar request of the feds. Coal is also burned for power in Alberta and Saskatchewan, although Alberta is on track to phase it out this year, Global News said.

Coal use, of course, is being driven by a huge increase in natural gas prices, with power plants sourcing coal as a cheaper alternative.

Trouble is, we’ve been so focused on expanding renewable energy, before it can actually replace fossil fuels, that we have virtually guaranteed oil, gas and coal prices will stay high for the foreseeable future.

As for the long-term, we, at AOTH, obviously don’t know to what extent renewables will replace fossil fuels and nuclear power (nobody else does either), but we have a hard time believing it will exceed 40% and we know it will ever reach 100%.

In a previous article we crunched the numbers, an edited version of which appears below.

To get rid of all fossil fuels — oil, NG and coal — in 20 years, we need to generate an additional 134,838,220 GWh of renewable energy.

1 gigawatt hour (GWh) = 1,000.00 megawatt hours (MWh).

A large solar farm would be 500 megawatts (MW), keeping in mind that the biggest solar farm in the US, the Topaz/ Desert Sunlight, is 550MW, the biggest in the world is 1,547MW; most solar farms in the US are much smaller, less than 5MW).

Let’s say it is able to operate half the time, or 182 days. 500MW x 24 = 12,000 MWh x 182 = 2,184,000 MWh. 134,838,220,000 MWh divided by 2,184,000 = 61,739 500MW solar farms.

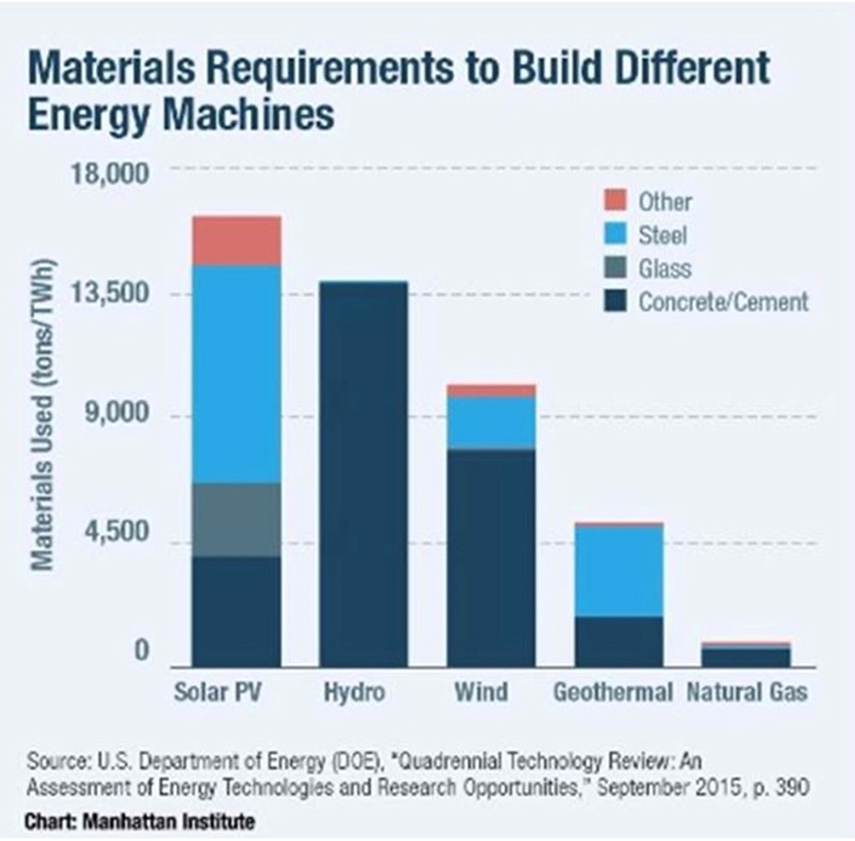

What does this mean for materials? We know that a 500MW solar conversion plant would cover 65 to 130 square kilometers with 17,500 tons of aluminum, a million tons of concrete, 3,750 tons of copper, 300,000 tons of steel, 37,500 tons of glass, and 750 tons of other metals such as chromium and titanium — 500 times the material needed to construct a nuclear plant of the same capacity.

The amount of aluminum and copper needed to build that many solar farms is off the charts. We calculated 1,080,432,500 tonnes of aluminum is required, or 16x global production. The amount of copper required is 11.5X global production.

But it’s not only the amount of materials, but the land, that would have to accommodate the more than 61,000 new solar farms. A study by Denholm and Margolis calculated the per capita solar footprint per person, based on the assumption that electricity needs in each state are met by solar power alone. Using an average of 200 square meters per capita, extrapolated to the population of the whole country, of 328.2 million, gives a figure of 65,640 square kilometers of land required for solar energy — a size roughly equal to the size of Nevada. Not taken into consideration is the amount of land needed to fit renewable energy storage batteries.

Is wind power any more feasible? The 10 largest wind farms in the world range from 630 megawatts to 20 gigawatts. Taking a 500MW wind farm, to facilitate a comparison between solar and wind, the Manhattan Institute estimates that replacing the output from a single 100MW natural gas-fired turbine, would require at least 20 wind turbines, each about the size of the Washington Monument, occupying 25 square kilometers of land. Upsizing that to 500MW would thus require 100 wind turbines, on 125 square km. That’s just for one wind farm equivalent in size to a natural gas or solar plant.

How many wind farms would be required to produce 134,838,220 GWh of electricity, the amount needed to replace fossil fuels? A 2MW wind turbine with a 25% capacity factor (the actual output over a period of time as a proportion of a wind turbine’s capacity), due to intermittency, can produce 4,380 MWh in a year. Upsizing this to 500MW = 1,095,000 MWh. 134,838,220,000 MWh divided by 1,095,000 MWh = 123,139 wind farms @ 500MW each.

To replace about 20% of Canada’s power generation that is still from combustible fuel sources, the country would need four times as many wind farms as today. Finding space for that many, a total of 46,800MW of nameplate capacity, would require 26,676 square kilometers. This is the size of five Prince Edward Islands, or around half of Nova Scotia. Remember this is just to replace 20% of Canada’s electricity still generated from fossil fuels.

Consider that in the United States, around 63% of its power still comes from coal, oil or natural gas. According to the EIA, replacing the 966 TWh generated from coal in 2019, would require 344.6 GW of wind farm capacity, spread over 200,000 square kilometers! (about the size of Nebraska)

How about materials? According to a report from the National Renewable Energy Laboratory, wind turbines are predominantly made of steel, fiberglass, resin or plastic (11-16%), iron or cast iron (5- 17%), copper (1%), and aluminum (0-2%). This isn’t counting the electrical system, which uses copper and rare earths such as dysprosium and neodymium.

A single 2MW wind turbine weighing 1,688 tons, comprises 1,300 tons of concrete, 295 tons of steel, 48 tons iron ore, 24 tons fiberglass, 4 tons each of copper and neodymium, and .065 tons of dysprosium. (Guezuraga 2012; USGS 2011).

The Manhattan Institute estimates that building a 100MW wind farm would require 30,000 tons of iron ore and 50,000 tons of concrete, along with 900 tons of non-recyclable plastics for the large blades. The organization says that for solar hardware, the tonnage in cement, steel and glass is 150% greater than for wind, to get the same energy output.

According to The Institute for Sustainable Futures at the University of Technology Sydney, Australia analyzed 14 metals essential to building clean tech machines, concluding that the supply of elements such as nickel, dysprosium, and tellurium will need to increase 200–600%.

Materials required to build solar PV, hydro, wind, geothermal and natural gas machinery. Source: Manhattan Institute

Materials required to build solar PV, hydro, wind, geothermal and natural gas machinery. Source: Manhattan Institute

If BP is correct in its outlook that in two decades, renewables are going to supply the equivalent amount of electricity currently generated by coal and gas combined, we have a problem, Houston. First of all, just replacing the current amount of energy demanded by coal and natural gas, let alone the inevitably higher figure in 2040, with solar and wind would be nothing short of miraculous. Our research shows that it would mean over 60,000 solar farms and more than 120,000 wind farms. In all it’s about a 450% increase in renewables.

Of course, solar and wind farms can’t be located just anywhere. They need to be in the right locations, where the winds are strong and frequent, areas that get a lot of sunshine, and close enough to existing power lines (most of which would need serious maintenance or upgrading) to be economical.

We already know that we don’t have enough copper for more than a 30% market penetration by electrical vehicles. Building renewable energy capacity is over and above supplying the ever-growing marketplace for EVs. How are we going to get enough solar and wind to produce a minimum of 134,838,220 GWh (that’s for 2019, it could be double by 2040), if we are to 100% replace fossil fuels in 20 years?

And even if we could, how are we going to find the raw materials? For solar power we are talking about finding 16 times the current annual production of aluminum, and 11 times the current global output of copper. Up to six times the current production levels of nickel, dysprosium and tellurium are expected to be required for building clean-tech machinery. Good luck!

Even if the mining industry could identify and produce this amount of metals to meet the world’s goal of 100% decarbonization, the supply shortages guaranteed to hit the markets for each would make them prohibitively expensive. It’s just supply and demand.

By all means, let’s electrify, but let’s produce the extra energy with nuclear and let’s dump the mega-raw-materials-consuming solar and wind.

Not only are solar and wind inappropriate for base-load power, because their energy is intermittent, and must be stored in massive quantities, using battery technology that is still in development, they don’t have anywhere near the energy intensity provided by fossil fuels, or nuclear. (read more)

Earth Overshoot

These are just the issues finding enough raw materials for the green-energy transition in the developed world. We also have to consider, that developing countries want the same kinds of products that we want, driving the demand for metals and fossil fuels even higher.

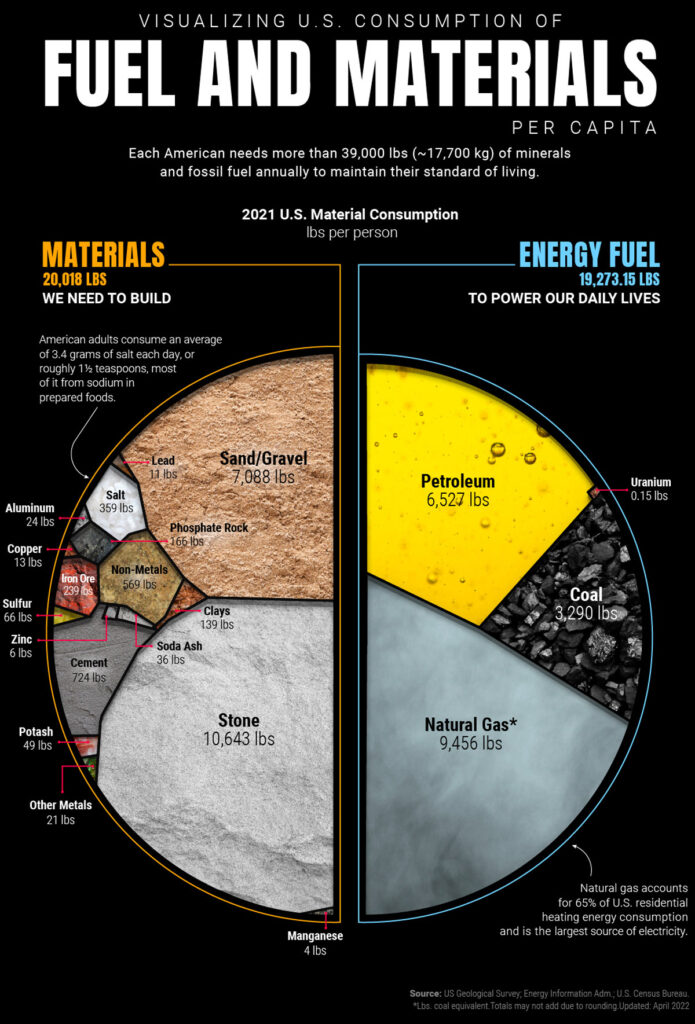

A recent infographic from Visual Capitalist, using data from the National Mining Association, found that the average American needs more than 39,000 pounds (17,700 kg) of minerals and fossil fuels annually to maintain their standard of living.

Source: Visual Capitalist Click for larger image

Source: Visual Capitalist Click for larger image

Remember, this is before any concerted effort to find, and mine, the materials required for electrification; 39,000 pounds per person is only what is needed for current everyday life.

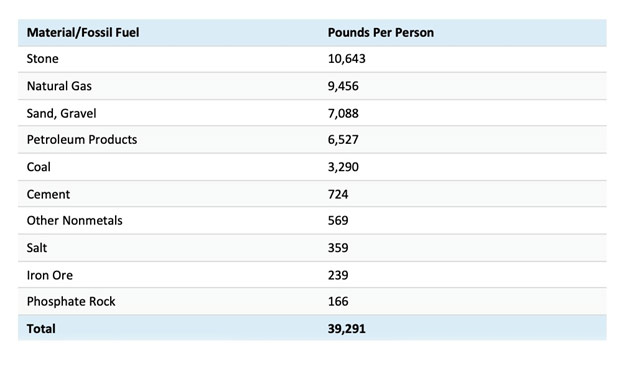

Sand, gravel and stone are the most used materials, @ just over 17,000 pounds combined per person. Natural gas is by far the most used energy fuel, @ 9,456 pounds, followed by petroleum (6,527 pounds) and coal (3,290 pounds). Uranium used in nuclear power plants weighs in at a fraction of a pound (0.15) per person.

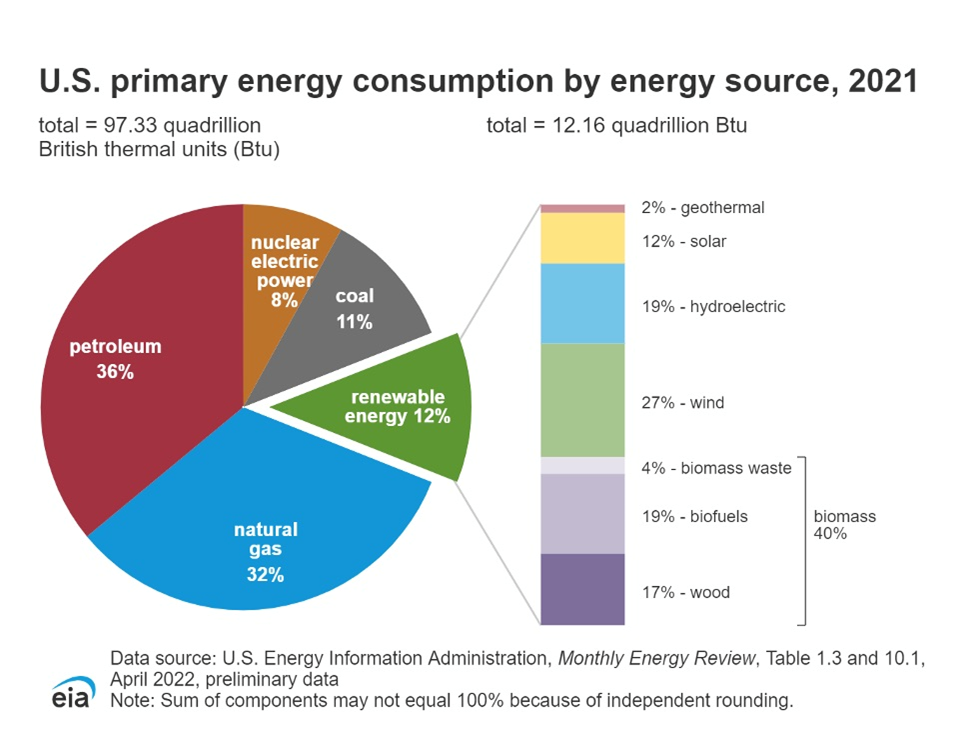

The writeup accompanying the infographic notes that, despite ongoing efforts to reduce carbon emissions, each person in the United States uses over 19,000 pounds of fossil fuels per year. The pie chart below makes our dependency on oil even more pronounced; only 20% of US annual energy consumption is sourced from renewables (12%) and nuclear (8%). Gasoline, of course, is the most consumed petroleum product, in 2021 averaging 364 million gallons per day.

The challenge the US, and rest of the world faces, is how to increase that 12% renewable energy slice and the 8% nuclear portion, while decreasing the combined 79% fossil fuels chunk.

We don’t have the answer, but we can provide context that, unfortunately, makes the goal even more daunting.

Recently I came across a statistic that said India’s copper consumption per capita is expected to double, from half a kilogram per person to 1 kilogram by 2025. The main drivers of Indian copper demand are infrastructure, including increased urbanization, new industrial corridors, rail projects and defense. American numbers are 13lbs of copper, do you think Indians can reach copper use parity with Americans? Or even come close?

Now consider that India is just one of many countries in the developing world, with plans to lower their carbon footprint and become more electrified, through higher usage of copper and other metals.

Another 2 billion people will be added to the world between now and 2050. Most will not be Americans but they are going to want a lot of things that we in the Western developed world take for granted – electricity, plumbing, appliances, AC etc. What if all these new consumers were to start consuming, over the next 10 years, just like an American? What’s going to happen to the world’s mineral resources if a billion more “Americans” are added to the consuming class?

Conclusion

The question we need to ask ourselves, is how much are we willing to pay, for electrification and decarbonization? The cost of making this transition is becoming more expensive and consumers are the ones being hit in the pocketbook. Recently it was reported that the cost to fuel electric vehicles in the United States is higher than gas-powered cars for the first time in 18 months.

“In Q4 2022, typical mid-priced ICE (Internal Combustion Engine) car drivers paid about $11.29 to fuel their vehicles for 100 miles of driving. That cost was around $0.31 cheaper than the amount paid by mid-priced EV drivers charging mostly at home, and over $3 less than the cost borne by comparable EV drivers charging commercially,” Anderson Economic Group (AEG) said in an analysis, via Epoch Times.

The argument for owning an EV has always been that it’s lifecycle cost is lower than a traditional gas vehicle. But with US pump prices falling from $5.10 a gallon in July, 2022, to the current $3.59, it may no longer be true.

In Canada, sticker shock and availability are the two factors working against more electric-vehicle sales. A CBC News article notes that, while the federal government wants every passenger vehicle sold in Canada to be electric by 2035, unless the prices become more reasonable for the average consumer, it might not be a realistic expectation.

A car dealer in Windsor, Ontario said in most cases, a fully-electric vehicle will run the buyer a cool CAD$55,000, minimum. According to the Canadian Automobile Association, EV prices range from $39,498 to $189,000. On average, an EV is 40-45% more expensive than an internal combustion engine powertrain vehicle.

And that’s if you can find one in stock. The Windsor car dealer says he probably won’t get fully electric vehicles at his dealership until 2024, citing supply chain issues.

Cars in general are getting beyond the price range of many Canadians. The CBC quotes an October, 2022 report from AutoTrader.ca, saying the average price of a new vehicle in Canada was $57,519 — the highest ever recorded and up 18.5% year on year.

A telling indication of where Canadian consumers’ car tastes are at, was an article in last weekend’s Globe and Mail, saying that 80% of new vehicles sold in Canada in 2020 and 2021 were SUVs. No breakdown was given between gas, hybrids and all-electrics, but I’m going to guess that the majority of the models sold came with a gas tank.

The federal and provincial governments are aiming to make EVs more affordable through rebates (your tax money at work). However, while the federal rebate of $5,000 for fully electric vehicles and $2,500 for hybrids was expanded last year, Ontario’s rebate program was canceled in 2018. Individual EV buyers in BC can apply for a rebate up to $4,000, and companies can get rebates of $3,000 off battery electric and long-range plug-in hybrid vehicles, or $1,500 off plug-in hybrids with a range less than 85 km.

Inflation, of course, is affecting every sector of the Canadian and US economies, so the cost increase for new EVs comes as no surprise. What might surprise some readers, is the notion that much of the inflation we are experiencing, is supply-, not demand-driven. Higher prices for fossil fuels and their thousands of derivative products will not be cured by interest-rate hikes aimed at squelching demand. The only way to bring these prices down is to increase the supply, of crude oil and natural gas.

While oil & gas prices have fallen from 2022 highs, the sheer demand for these products — per capita, Americans annually consume 9,456 pounds of NG and 6,527 pounds of petroleum — along with projected tighter supplies due to lower investments in fossil-fuel exploration compared to green energy, all but guarantee higher prices.

An article this week in Oilprice.com states that BP expects global oil demand to peak between the late 2020s and early 2030s, as the Russian invasion of Ukraine accelerates investment in clean energy and governments look to bolster energy security with higher shares of renewables in the energy mix.

The upshot is another seven to 10 years of higher oil prices, coupled with incremental price increases for commodities useful for the energy transition, including copper, nickel, graphite and lithium.

The other conclusion to be drawn, is there is no point making life harder for ourselves by trying to achieve 100% electrification, given that we do not have the metals supply to achieve this goal. In fact for some of the minerals in question, the opposite is happening, where severe supply shortages are imminent.

A huge hypocrisy is apparent in United States’ mining policy.

The country is going all-in to electrify, but the first thing the Biden administration does is close its mines! What on Earth are they thinking?

Rather than rushing pell-mell into electrification, we need an honest evaluation of how much of a shift can occur, within what time frame, at minimal added cost to consumers. As for fossil fuels I expect them to remain a significant part of the energy mix, and used in manufacturing, for the foreseeable future.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.