By selling and immediately buying back some of its gold reserves, the central bank of Curaçao and Saint Martin managed to use its gold revaluation account to offset losses in 2021. Because many other monetary authorities are currently making losses too—and there is no limit to revaluing gold against fiat money—this trick could be used the world over to heal central banks’ balance sheets.

The central bank of Curaçao and Saint Martin, circa 2010.

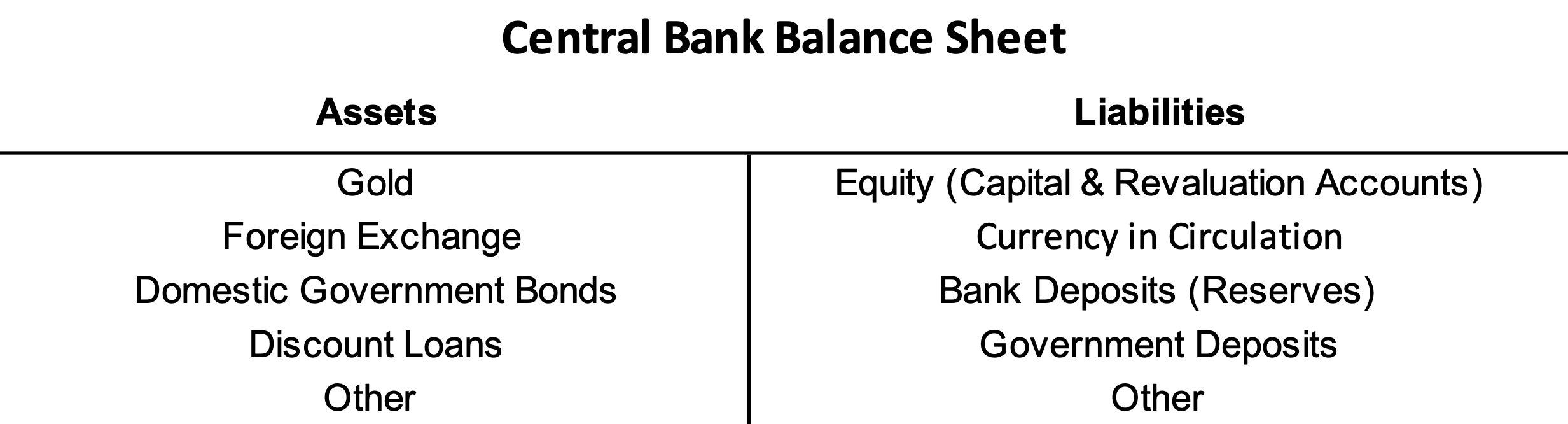

What is a Gold Revaluation Account?

A gold revaluation account (GRA) is an accounting item that records unrealized gains (or losses) of gold assets. When the price of gold rises, as it inevitably does in the long run, gold assets increase in value and concurrently the GRA swells. As a formula:

GRA = present gold market value – gold purchasing cost

The GRA is usually part of a central bank’s equity (net worth), while it’s not part of its capital (a narrower definition of equity)*. By their own rules, central banks can’t use their GRAs to cover general losses.

If the price of gold rises, gold assets and the GRA increase; if the price of gold falls, gold assets and the GRA decrease. Central banks that bought gold many decades ago have substantial GRAs.

Central bank losses eat into their capital, possibly pushing it into negative equity. For private entities negative equity means they are broke, as their liabilities outstrip their assets. Central banks, however, can continue their operations under negative equity, although it can interfere in monetary policy and deteriorate independence and credibility. A slippery slope: when a central bank’s credibility is lost, all is lost. Hence central banks prefer to have a healthy capital position.

Courtesy ofPictet Group

Late in 2022 the Dutch central bank (DNB) revealed it was suffering losses due to rising interest rates after consecutive years of Quantitative Easing (QE). During QE it bought domestic government bonds that yielded close to nothing with newly created reserves. When the European Central Bank instructed DNB to raise interest rates to combat inflation, its interest expenditures on reserve liabilities exceeded interest income from its assets, which equals a loss.

DNB Governor Klaas Knot was interviewed about losses and a weakening balance sheet in October 2022. Knot mentioned Dutch taxpayers possibly need to recapitalize their central bank as EU statutes prescribe. However, he also brought up DNB's GRA as a solvency backstop:

The balance sheet of the Dutch central banks is solid because we also have gold reserves and the gold revaluation account is more than 20 billion euros, which we may not count as capital, but it is there.

Based on Knot’s remarks, and an email exchange I had with the German central bank prior, I speculated DNB and other central banks could change the accounting rules for their GRAs to absorb losses. Why let taxpayers foot the bill if GRAs can be used? More recently, I discovered a loophole through which some central banks can use their GRAs for this purpose.

How the Central Bank of Curaçao and Saint Martin Used its Gold Revaluation Account

Curaçao and Saint Martin are two small islands in the Caribbean, both part of the Kingdom of the Netherlands. Because these countries are not included in the eurozone they have their own currency: the Netherlands Antillean guilder (local symbol NAf, international code ANG).

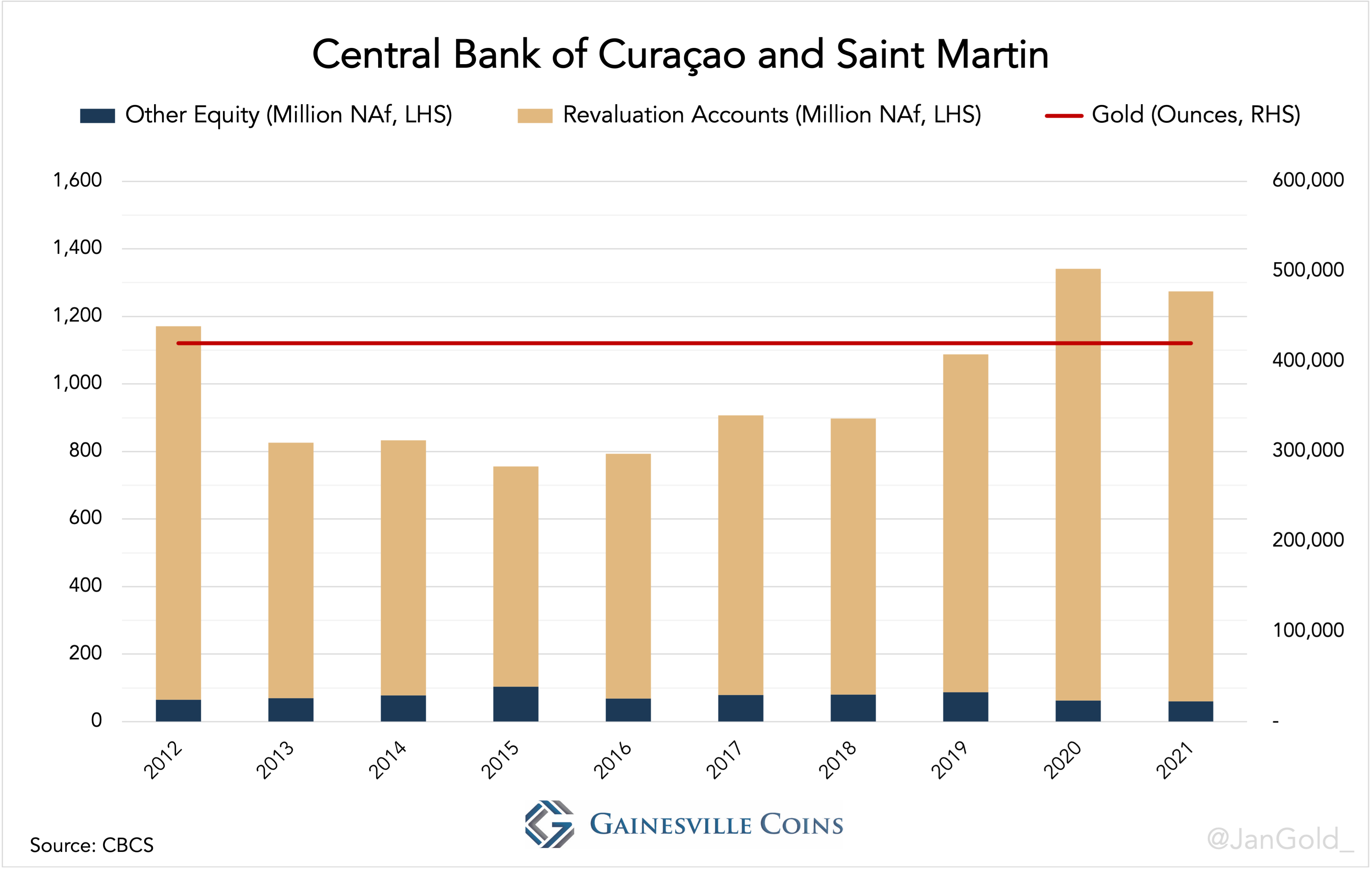

The central bank of Curaçao and Saint Martin (CBCS) started making losses in 2020 due to declining interest income, which accelerated in 2021. At the end of 2020, CBCS held 420,395 fine troy ounces of gold. Its equity position was NAf 1,341 million, of which its GRA accounted for NAf 1,275 million. Since the GRA makes up a large part of CBCS’s equity it was tempting to use some of it when confronted with losses.

CBCS’s total equity is correlated to the gold price due to its relatively large GRA.

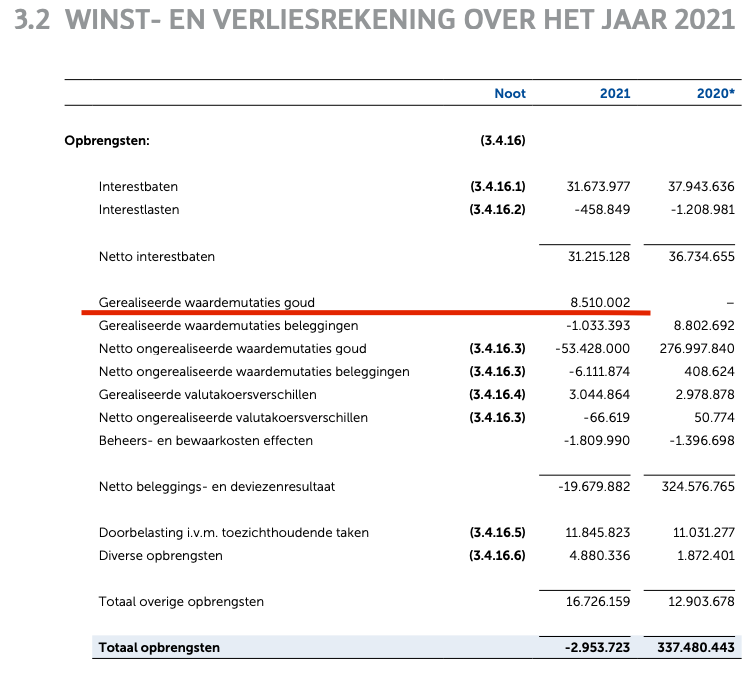

In 2021 CBCS decided to sell and immediately buy back 2,945 ounces of gold to turn an unrealized gain into a realized gain to offset losses. The value of the gold traded was NAf 9.55 million. On page 51 of their Annual Report 2021 it shows the metal was sold and repurchased at exactly the same price, implying the trades were handled off the market.

The realized gain is the value of the gold traded (NAf 9.55 million) minus the historic purchasing price of the gold traded (NAf 352.05) times the gold weight traded (2,945 ounces).

NAf 9.55 million – (NAf 352.05 per ounce * 2,945 ounces) = NAf 8.51 million

Page 41 from theAnnual Report 2021.In red it reads: “realized gold gains [NAf] 8,510,002.”

Note, CBCS’s total gold holdings did not change. The charge for the gold transactions is that the historic purchasing cost of CBCS’s total gold reserves went up by NAf 8.51 million, which is another way of saying its GRA declined by NAf 8.51 million**.

CBCS dampened losses by using a small portion of its GRA, whereby it kept a healthy capital position.

Conclusion

In my previous article I theorized the international monetary system can be deleveraged and stabilized by a substantial higher price of gold. More gold (a higher value) on the balance sheets of central banks increases the ratio of hard assets (gold) against international credit assets (foreign exchange), and hard assets against credit liabilities.

Bigger GRAs (more equity) can be used to cancel domestic government bonds on the balance sheets of central banks, and thus alleviate sovereign debt burdens. Other losses, such as previously discussed, can also be absorbed by GRAs.

For central banks to access their GRAs they either need to ditch the accounting rules they drafted themselves or find a counterparty to sell and buy gold (off the market) and materialize profits. Profits can be used to attenuate losses, helping central banks to maintain their credibility by not operating under negative equity.

What I describe above rhymes with a statement of the Governor of the German central bank (Bundesbank) from 2018:

Germany’s [gold] reserve assets ... are a major anchor underpinning confidence in the intrinsic value of the Bundesbank’s balance sheet. Gold has grown in importance over the course of history, first as medium of payment, later as the bedrock of stability for the international monetary system.

One reason GRAs are prohibited from being used to absorb losses is because once fully run down a declining gold price will cause GRAs to become negative, damaging central banks’ equity. The very thing they try to avoid. For central banks like DNB and BuBa—that bought their gold during Bretton Woods at $35 dollars an ounce—this risk is immaterial. The gold price will never again fall to $35 dollars. Central banks may also choose to support the gold price to use their GRAs and not see it turn negative.

The size of GRAs is infinite because gold is the only universally accepted financial asset that can’t be printed. Denominated in currencies issued by central banks, there is no limit on the price of gold, and consequently the size of GRAs.

Notes

*Central banks use their own accounting rules, and terms and definitions are not homogeneous. In comparison to my previous articles on this subject I have adjusted some terminology.

**The average purchasing price of CBCS’s gold reserves jumped from NAf 352.05 per ounce on December 31, 2020, to NAf 372.3 on December 31, 2021. The difference (NAf 20) times CBCS’s total gold holdings (420,395 ounces) is NAf 8.51 million, which is exactly the amount CBCS took from its GRA.

Further Reading

- Buiter, W. H. 2014. Can Central Banks Go Broke?

- Dalton, J. W. & Dziobek , C. H. 2005, IMF. Central Bank Losses and Experiences in Selected Countries

- Ducrozet, F., Costerg, T. & Gharbi, N. 2022. Do central banks’ losses matter?

- Malinen, T. 2019. Will central banks survive?

- Nieuwenhuijs, J. 2022. German Central Bank Doesn’t Rule Out Gold Revaluation

- Nieuwenhuijs, J. 2022. Governor Dutch Central Bank States Gold Revaluation Account Is Solvency Backstop

- Stella, P. 1997, IMF. Do Central Banks Need Capital?

- Sullivan, K. 2022, WGC. Central bank accounting practices for monetary gold - 2022 update

- Sweidan, O. D. 2011. Central bank losses: causes and consequences

Original article was published on Gainesville Coins: https://www.gainesvillecoins.com/blog/caribbean-central-bank-gold-revaluation-covers-losses

About the author