For now, we are in the calm before the storm. We feel little sense of its coming. For the past month, stocks have been in somewhat of a lull. While they trended up for the two months prior to May, they trended generally flat to down in May. The S&P eeked out a meager toe-hold for the month, closing up just 0.3% for all of May, but the Dow dropped 3.6%. The Nasdaq rose strongly up about 5.8%, but that was entirely on the backs of only a few major AI companies, such as Nvidia. Overall, pretty mild stuff, and certainly not evidence of a market set to soar.

Growth may remain strong in these companies with AI becoming the new equivalent of FAANG stocks because AI is seen as a revolution in business and culture that begins a new era as much as the internet did two decades ago and as the personal computer did two decades before that. Now that people have seen what AI can do, investors are charged up about it.

There is one caveat to that glimmering prospect, however, that I noted in my editorial to The Daily Doom today:

As the Maverick of Wall Street points out in his typically humorous style today, the so-called smart money is making the dumb push, BUT they are the smart money because they always know how to push the frenzy high enough to get retail investors all cashing in, and that is when these Wall-Street Big Bucks cash out, reaping the rewards by shifting suddenly from pump to dump, letting it all land in the quick-to-be emptied hands of dumb retail investors who were foolish enough to fall for the mania. The Maverick says he sees signs of that starting to happen yesterday.

Because of the big AI push by major investors, the AI-connected stocks stormed the tech-heavy NASDAQ higher and gave just enough of a lightning jolt through the much broader S&P to keep it alive. However, nearly the entire rest of the stock market spent May falling, which doesn’t bode well for the foundations of the recent rally. And take note that even the big, shiny, new internet companies took a hard fall in the dot-com bust as the new internet industry took root and the unproductive stocks got trimmed out. Even the companies that ultimately lasted had to weather that rough passage for all.

The House’s passage of the debt ceiling agreement this evening is likely to give many stocks another jolt for a relief rally tomorrow morning, but how many days can the new mojo drive the stock market up before the relief from the political battle that held stocks back in May gives way to the enormous downdraft that is likely to be coming from the hundreds of billions of dollars in new Treasury issuances the government will have to begin making?

The Treasury Storm of the Century

As soon as the dust settles in the Senate over the final vote on the debt ceiling, a Treasury storm commences, the likes of which we will have never seen! Not only does the Treasury have about half of a year of being locked out by the debt ceiling to make up for, but it has to do this during a time of much higher ongoing new debt spending than at other times and following a time when there was a much higher rate of debt pileup while the ceiling was in place than ever before and right at a time when the Fed cannot jump in as the government’s buyer-of-first-resort funding to assure low interest rates and ample demand.

Unless Janet Yellen has a brick for a brain, she will spread the issuance of new debt out as much as possible to reduce the shock on … government interest rates, bond values and bank reserve values in general, all interest rates tied to Treasury rates (including mortgages and, from there, the troubled real-estate market), and on stocks due to the rising risk premium that is certain to grow between normally risk-free Treasuries and higher-risk stocks? While she will likely spread that out all she can, the long delay in raising the debt ceiling means a fair amount of the government’s new debt issuance will likely have to be front loaded.

As a result, a lot of churning is likely to build in the atmosphere around us during the month of June and likely the remainder of summer as these bond issuances play through. Not only do they affect everything just mentioned, taking bank reserves that have already failed three banks even lower by dropping the value of existing bonds more as new bonds offer rising yields above the yields originally priced into the existing bonds forcing those existing bonds to drop in price in order to compete if they must be sold, but reserve-pummeling purchases of Treasuries by businesses and individuals when the Fed backs away as a buyer, are exactly the mechanism by which the Fed’s quantitative tightening reduces money throughout the financial system.

Here is how that works, as the Fed explained directly to me last time they attempted tightening: As businesses and individuals buy Treasuries, money from their bank accounts go to the government’s bank account. That happens by money in their banks’ reserve accounts moving over to the government’s general account at the Federal Reserve. That lowers overall bank reserves on the Fed’s balance sheet, which leaves banks tighter. That results in all of those banks making fewer and fewer loans because they have less in reserves to loan against. All of that clamps down on the economy as intended during the Fed’s tightening, raising interest rates, and reducing the creation of new money because banks are the ones that create money in our fractional reserve banking system via making loans. They are required by the Fed to maintain a certain ratio between loans they hold and reserves, so they slow down as they have less in reserves to loan against.

Of course, the Fed can change that ratio, but the whole point of this entire exercise is to tighten the economy in order to battle inflation by sucking money out. As money is sucked out of the system via this tightening process, that naturally starts to bring inflation down. What this also means, though, is that, because the US Treasury stopped issuing supply of new Treasuries above the amount of old debt it continued to roll over during the debt-ceiling freeze, there was not nearly as much tightening from the Fed’s QT as there would have been. The Treasury wasn’t sucking additional money out of bank reserves throughout that time.

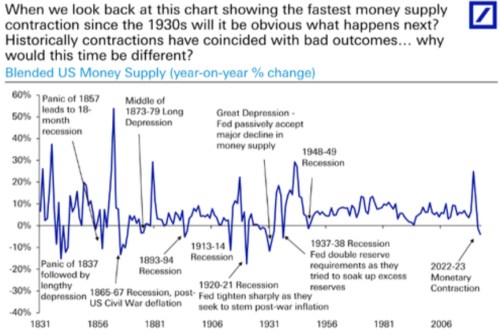

There was some drop in money, and it certainly can be seen in how the rate of rise in the supply of dollars rapidly declined and finally turned negative, meaning money supply finally started to actually come down, rather than just go up less quickly:

So far, the amount of reduction in actual money supply is incremental compared to other times when the Fed has tightened against inflation. Moreover, the massive amount of reserves that have to be drawn down is far greater than at any time before, even though money supply did not rise much more than other times as a result of all that extra in reserves, as banks bought stocks and did other things than make loans. That makes the drawdown all the more insignificant, which is, in part, because the Treasury did not suck any money out of bank reserves during the past half year in which its hands were tied by the debt ceiling. We have, all the same, seen the first downtick in global dollar supply on a year-on-year basis in over seven decades!

As you can also see, the kind of serious tightening necessary to drop money supply enough to reduce inflation tends to be associated with harsh economic times. The hope for roaring times to return as we now finally move into the phase where QT starts seriously rolling back money supply is certainly imperiled by the move in bank reserves that is likely as soon as the Treasury starts making up for lost time. So, how will stocks and everything else fair when this downdraft, from which we were spared by the debt ceiling, suddenly sweeps in?

The Fed must fight, though the banks go bust

First, let us consider the following graph to see the unique situation in which this summer event will transpire:

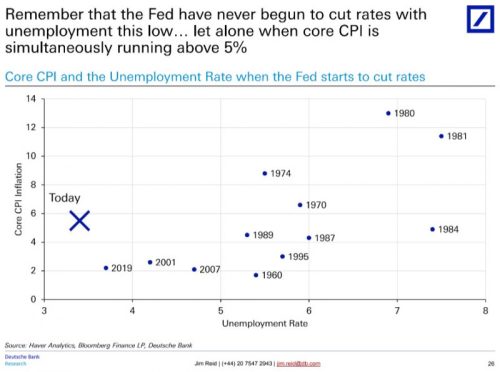

Most other periods of rate cuts in more recent decades did not happen when inflation was this high. To the extent that they did, they all happened when the unemployment rate was much higher, meaning the Fed had less work to do to bring inflation down by suppressing wage growth if that is its plan. I don’t really buy the idea that wage growth is the big thing the Fed needs to focus on, but many financial writers believe it is. The Fed has said it is not specifically targeting wages, and it would probably accomplish far more by causing executive wages, stock options and benefit growth to fall since those have all soared outlandishly higher than wages. For the longest part of this inflationary burn, stocks also soared more in value as did dividends, so much of the heat comes from that wealth effect that predominantly benefited those at the top. Even during high inflation, buybacks and dividends continued to inflate the pockets of the wealthy as they profiteered off inflation to actually push profits up, too. Wages are barely keeping up with any of that.

NEVERTHELESS, most people see the fight against wage growth as essential to the Fed’s inflation plan. If it is, this graph screams the Fed started the battle far behind compared to any other start because it has much further to go on job cuts than it ever has while it is still facing inflation that is fairly high historically compared to other inflationary periods. Which is all to say, the Fed is still not likely jumping in to the rescue with new QE if things go badly until they become terribly bad, as the Fed has a long war ahead of it still.

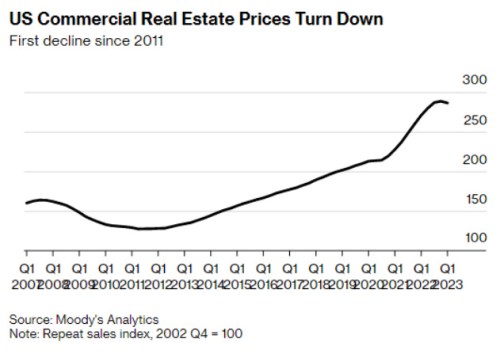

The perils from continued heavy QT as the Treasury finally lets us feel the blows will be happening just as we enter the next likely cause of banking collapse from an industry that is already being tossed around by the winds that blow — declining commercial real estate (CRE) market. Here is where we are right now:

The actual downturn in prices, versus just decline in number of sales, has set in, but barely. Rising Treasury yields are certain to mean more rising mortgage costs and real-estate bonds, and, therefore, rising problems in mortgage-backed securities and in real-estate investment trusts. I recently quoted Jamie Dimon, head of JPMorgan Chase, stating that the second wave of bank crashes is going to begin with the downturn in commercial real-estate that has just started. I am certain he is right when you consider that banks, which already distressed about the state of their reserves, are going to lose more of their banked reserves due to Treasury purchases by their customers. Then factor in how the value of whatever reserves are left is going to be devalued further than it already has been by the rising yields of Treasury bonds (which always equals falling bond prices/values).

In other words, the problem we saw just a couple of months ago with three bank crashes — two of which hit the top-three medals bracket for all of US banking history — gets compounded this coming summer and fall as the Treasury goes mad issuing new debt and the Fed remains forced out of the game (based on the chart above).

You take that continued inflationary heat, which keeps the Fed embattled, and add bonds interest rising, US debt, therefore becoming much more expensive, requiring even more debt financing, and everything else just mentioned, then add in crashing commercial real restate and the stresses those CRE loan defaults will place on regional banks that have a lot of CRE loans, and it all looks like this:

But that’s just the beginning. Consider also the current state of the US economy.

Dark skies for the economy

The US is clearly taking a second dip into the “technical recession” it fell into during the first half of 2022, which was called by many a “technical recession” because the governing body that declares recessions (the National Bureau of Economic Research) did not tag it as a recession, most likely because our economic geniuses believed the tightness in the labor market was proof of economic strength, rather than extreme weakness in the labor pool, just because that is what they are used to it meaning, and they cannot see past the boxes they are used to living in.

At any rate, we are going back into recession, as I said we would this year.

After the unexpected resurgence in April, Chicago PMI plunged in May from 48.6 to 40.4 (against expectations of 47.3). That is the ninth straight month below 50 (in contraction)…

Nine straight months of business contraction in one of the nation’s leading manufacturing surveys is certainly a strong recessionary indicator, which looks like this in historical perspective:

As you can see, this level and length of contraction almost always means a recession is present, not just coming. We plunged into it during the undeclared recession of 2022, and now we’re taking a second dip down (and that is before the likely coming storm described above).

Prices rose, albeit at a slower pace. New orders fell. Employment fell (as the Fed presumably, according to many is hoping to see). Inventories fell at a faster pace. Production fell. Backorders fell.

The manufacturing economy is slowing hard.

This was also seen in the Dallas Fed’s Manufacturing Survey, which has remained in contraction territory even longer (13 straight months), and which actually plunged even harder:

New orders fell. The growth rate in orders fell. The factory/shop capacity-usage rate fell even further. General business activity dropped. And business outlooks fell to the lowest they have been since the deeply catastrophic Covidcrash that slaughtered the labor market and set a benchmark low for all things economic in the present century. In fact, many of the problems in this report were tagged to the inability to find labor and supplies that came about from the Covid lockdowns.

Financial market turmoil

Consider also this perilous weight, likely to spell trouble when bond values start plunging again as the Treasury goes back to work blowing up debt:

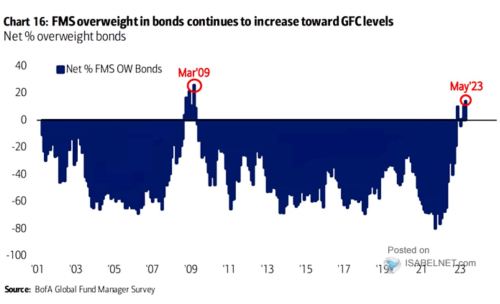

Fund Managers Most Overweight in Bonds Since GRC:

At first blush, it’s easy to understand the overweight on bonds. Yields are modestly attractive for the first time in a decade and high quality bonds and treasuries may provide a safe haven in the widely anticipated event of a recession.

Of course, the picture gets more complicated when one realizes that … the debt ceiling impasse, which has shielded the market from virtually all of the Fed’s QT, is likely soon coming to an end and will lead to a tsunami of supply.

What happens when the next wave of bond devaluations begins, which got a reprieve from the Treasury but now gets amplified above what we saw at the start of Fed tightening as the Treasury now piles that half year period of reprieve in on top of the normal needs of the coming period?

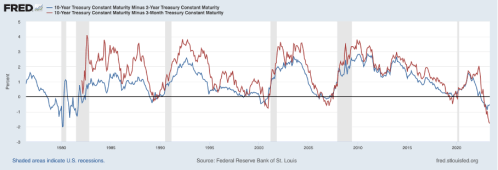

Consider also the inverted yield curve, the most reliable of all forward-looking recession indicators:

When has it ever looked this bad?

Well, one answer is rarely ever without a recession by this point and never more deep than this for the Fed’s favorite measure. The measure the Fed considers its most reliable of all recession advance indicators is the 10-year Treasury versus the three-month Treasury (red line).

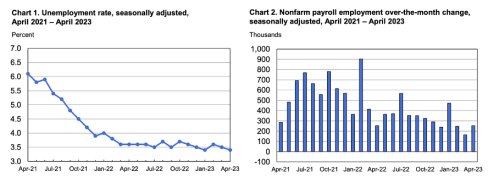

Labor market still stubbornly not responding to Fed tightening:

Totally unresponsive. However, that, as I keep saying, is because the labor market is badly broken, not strong. There simply isn’t enough laborers in the pool to even meet diminished needs. That has been the basis for my longstanding prediction that the labor market will be very slow this time to respond to the Fed, so by the time it does respond, the Fed will have overtightened badly, and the damage set in for the economy will be considerable.

We can now clearly see how long that has remained true — throughout the entire past year-plus of Fed tightening. We are probably getting to that point where unemployment will turn upward, but there will be a lot of damage set in place by the Fed to play out in the months thereafter.

So, stock euphoria may find some reason to rise when the debt ceiling gets lifted, unless major investors are seeing all that I am seeing here, but they are clearly missing the big picture if they do; and their summer surprise is likely to be severe. We’ll avoid the one true risk of a credit downgrade once the preset bill makes it through the Senate, but then the whole next set of piled up troubles starts blowing in that built up while the debt ceiling kept the Treasury at bay. However, it was always catch-22 because a failure to raise the debt ceiling, while it would not cause default, would cause a serious multi-agency US credit downgrade, throwing a whole bunch of other yield-escalating chaos into the bond world.

You can thank the Fed and your long-term spendy government for creating this mess. It is what happens when you don’t pay for what you do as you go and fund it all with practically free Fed funds until you can’t anymore because inflation starts burning up your backside. If the Fed jumps back in to buying US Treasuries, thus expanding reserves, and thereby creating more monetary supply, it will be dumping gasoline from its firefighting plane into the fire tornado, and all hell will break loose.

If you value this writing, please take a second to support David Haggith on Patreon!

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!