Next week brings the long-awaited September FOMC meeting. What is said and what is unsaid will have significant impacts on the short-term direction of COMEX gold and silver prices, so let's take some time today to speculate upon what may be coming.

And "speculate" is precisely what we will do today, as there is no one anywhere who can accurately predict what the Fed will do next. This has been the case since Greenspan and "the size of his briefcase" all the way through to Bernanke, Yellen, and now Powell. You may think you know what the Fed will do next, but they often end up moving too soon or too late. So, anyone who claims to know precisely what the Fed will do next is most likely selling something.

To that end, though, hard-earned experience and wisdom can offer some guidance. For example, the Fed often floats "trial balloons" through their sycophant media outlets. For a long time, Jon Hilsenrath of the Wall Street Journal served this role for Ben Bernanke. Steve Liesman of CNBC often seemed to be the "leaker of choice" for Janet Yellen. Though Chairman Powell doesn't seem to have a preferred media mouthpiece as yet, his Fed still operates under the same "trial balloon" method.

And what do we mean by a trial balloon? Let's let the nice folks at Merriam-Webster explain:

Hmmm. "A scheme tentatively announced to test public opinion". Keep that in mind as we next recall a few of these headlines from the past few months.

At the conclusion of the June FOMC, Chairman Powell conducted his usual press briefing. In his answer to the very first question, you'll find the statement below:

https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20200610.pdf

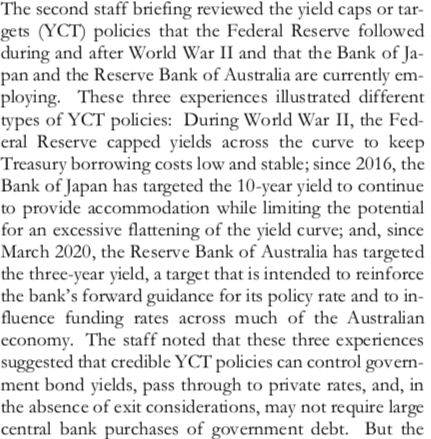

More details were provided when the minutes to the June FOMC were finally released three weeks later. You can read through them if you'd like by clicking this link:

https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20200610.pdf

Here's a key snippet:

The next balloon was sighted on July 17, when this article appeared at Bloomberg in the wee hours of the morning. You should be sure to read it now if you've not seen it before, as it contains the text shown below: https://www.bloomberg.com/opinion/articles/2020-07-17/the-fed-is-setting-the-stage-for-a-major-policy-change

On August 5, the next balloon floated by with this article from CNBC: https://www.cnbc.com/2020/08/04/the-fed-is-expected-to-make-a-major-commitment-to-ramping-up-inflation-soon.html

And finally, Powell himself began to lay it all out with his speech at the Fed's "Virtual Jackson Hole" conference on August 27. While not addressing the Yield Curve Control part of the equation, Powell made it abundantly clear that achieving price inflation was the Fed's #1 goal at present and that his Fed will be ready to employ all sorts of unconventional monetary tools to make it happen: https://www.federalreserve.gov/newsevents/speech/powell20200827a.htm

So let's cut to the chase. What are Powell and his Fed trying to tell you?

- They are desperate to spark inflation in order to manage the extreme level of U.S. debt and ongoing deficits.

- They've made it explicitly clear that they will NOT raise the fed funds rate before 2023, even if inflation actually begins to surge.

- "Conventional" monetary tools have failed to spark inflation in places like Japan. Therefore, the Fed will actively consider "non-conventional" tools.

- Among the many non-conventional tools under consideration is Yield Curve Control. In June, the FOMC was briefed on the historical experience of YCC in the United States.

Will a formal policy announcement of Yield Curve Control come out of next week's meeting? Maybe. Perhaps Yield Curve Control is already in place and the Fed just hasn't told anyone.

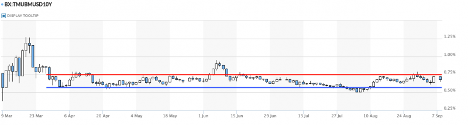

Note that since March 27, the yield on the U.S. 10-year note has closed between 55 and 75 basis points on 101 of the 114 trading days. Stated differently, the yield on the 10-year note has closed between 55 and 75 basis points 88.6% of the time since March 27. If the Fed has already instituted a covert, de facto Yield Curve Control program, they certainly appear to have done a good job so far!

So listen closely to what the FOMC says—and doesn't say—next Wednesday. The trial balloons floated since June all suggest that major policy changes will be forthcoming and these changes will all be designed to drive higher inflation. Higher inflation with Yield Curve Control will lead to sharply negative real interest rates. And sharply negative real interest rates will lead to higher gold and silver prices.

About the author

Our Ask The Expert interviewer Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.