The major gold stocks dominating their sector’s flagship GDX ETF have suffered chronic undervaluation over this past year. Traders simply haven’t been interested, starving gold stocks of the capital inflows necessary to normalize their prices with prevailing gold levels. But a momentous psychological catalyst is nearing that will force a violent mean reversion and overshoot in gold stocks, new nominal record highs in gold.

Financial markets are forever cyclical, perpetually oscillating between opposing extremes. Conditions constantly shift between bulls and bears, uplegs and corrections, overboughtness and oversoldness, herd greed and fear, and overvaluation and undervaluation. The longer any cyclical pendulum lingers at one end of its arc, the greater the odds a mean-reversion swing back is imminent. That’s the case in gold stocks.

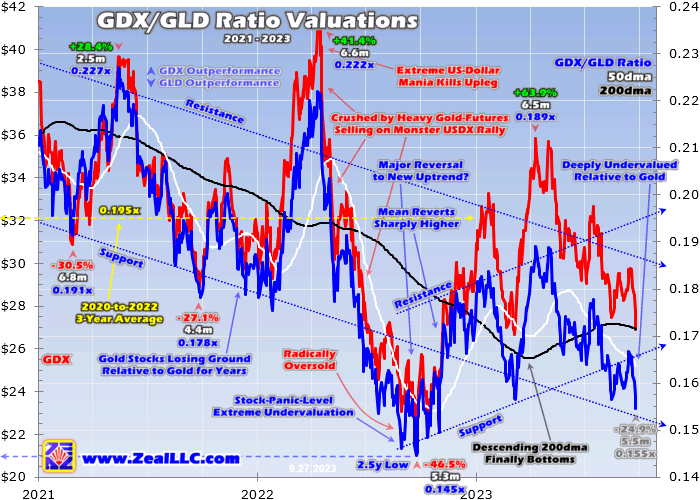

Because gold-mining earnings amplify gold price trends, gold stocks are effectively leveraged plays on gold. So their price levels relative to gold’s are a great valuation proxy, revealing cycles when charted over time. The most-popular gold-stock benchmark today remains the GDX VanEck Gold Miners ETF. Dividing its price by that of the mighty GLD SPDR Gold Shares gold ETF illuminates gold-stock valuations.

Mid-week GDX and GLD were slammed to $26.91 and $174.10, yielding a GDX/GLD Ratio of 0.155x. That’s on the lower side of recent years’ range, which hit an extreme 0.133x at its nadir during March 2020’s brutal pandemic-lockdown stock panic. Then the violent mean reversion and overshoot out of that was quick to catapult the GGR to a high of 0.241x in late July 2020. That gives some context for today’s valuations.

The major gold stocks are running about one-fifth up into their latest secular trading range relative to gold. While certainly not stock-panic-grade, these undervaluations have been chronic festering for this past year. The midpoint of that GGR range is 0.187x. From July 2022 to September 2023, GDX only traded above that level compared to GLD on 5 trading days out of 312! Gold stocks have been really out of favor.

From 2020 to 2022, this GDX/GLD Ratio averaged 0.195x through some major cyclical waves going both ways. Yet year-to-date in 2023, GDX’s closing prices have merely reached 0.171x GLD’s on average. So there’s no doubt gold-stock prices have lagged well behind gold’s recently. But this cyclical ebb can’t and won’t last, as the endless market waves soon force gold-stock prices to catch up with then surpass gold’s.

This chart superimposes the GGR and its key technicals over the raw GDX during the last several years or so. Gold-stock prices have really underperformed relative to gold in this span, carving the downtrend rendered here. But the cyclical pendulum has already started swinging back the other way, enjoying a mounting uptrend since the GGR plunged to deep secular lows in late September 2022. This ought to continue.

GDX’s major gold stocks have been losing ground relative to the metal they mine for years, as seen in this GGR downtrend. Gold-stock valuations have drifted lower deeper into undervalued territory as this sector’s popularity waned. It wasn’t just declining resistance and support lines defining this downtrend, but GGR’s 200-day moving average. These key technical lines distill out daily volatility to reveal trends.

This gold-stock valuation proxy’s 200dma peaked in early 2021, then relentlessly ground lower on balance into early 2023. But the cyclical tides subtly started shifting in March, when that 200dma slump bottomed. Then the GGR’s 200dma reversed decisively higher for the first time in years! That is a major technical reversal heralding a cyclical trend change. Gold-stock prices have finally started outperforming gold’s again.

And this mounting wave lifting gold-stock valuations relative to gold is likely to continue. After regaining ground for an entire year now, this GGR uptrend is well-established. Once that happens, these valuation mean reversions tend to run to completion. And that’s not merely a return to average, but usually a proportional overshoot challenging opposing extremes. And the one birthing this reversal was extraordinary.

The major gold stocks were slaughtered in mid-2022, with GDX plummeting 46.5% in 5.3 months on radically-unprecedented events! With inflation raging out of control, the Federal Reserve executed its most-extreme rate-hike cycle ever. Starting from zero, in just 6.2 months the Fed catapulted its federal-funds rate an incredible 300 basis points higher! Resulting soaring yields launched the US dollar stratospheric.

In just 6.0 months, the benchmark US Dollar Index rocketed parabolic with an epic 16.7% gain to extreme 20.4-year secular highs! That exceedingly-anomalous dollar strength unleashed withering gold-futures selling, bludgeoning the yellow metal 20.9% lower in 6.6 months. A couple weeks ago I wrote an essay analyzing these critical FFR-dollar-gold dynamics since the Fed started hiking, gold is overcoming the dollar.

With gold indirectly crushed by that scorching Fed-rate-hike cycle, the gold stocks amplified its downside like usual. GDX’s overall 2.2x downside leverage to gold in that crazy time was normal, actually on the low side. The major gold stocks of GDX tend to amplify material gold moves by 2x to 3x. But that huge selloff still left gold stocks radically oversold, with both GDX and the GGR languishing at stock-panic levels.

Both gold and GDX bottomed at deep lows in late September 2022 as the US dollar’s moonshot peaked. GDX’s $21.87 close just over a year ago was its worst since the dark heart of March 2020’s stock panic. Even during that scary time when no one knew the full extent of lockdowns’ impacts, GDX only closed lower on four trading days. It takes extreme fear to pound major gold stocks under $22 in GDX terms!

Gold stocks were so undervalued relative to gold after mid-2022’s USDX parabola that the GGR crashed to just 0.145x. That was an extreme 2.5-year low not seen since mid-March 2020, and even then the GGR only closed lower on two trading days! So that last gold-stock valuation-wave trough sure ended at crazy extremes. The farther cyclical pendulums swing, the bigger and more certain the resulting mean reversions.

The post-stock-panic one is a great example of how violent mean reversions and overshoots can get out of such extremes. The GGR had been pummeled to a deep 4.1-year low of 0.133x in mid-March 2020. Over the next 4.8 months, GDX skyrocketed 134.1% catapulting the GGR to a 4.0-year high of 0.241x! Although this past year’s mean reversion has been slower, it could easily extend to a similar magnitude.

Again that post-stock-panic rebound defined the GGR’s range in recent years totaling 0.108x. When the US dollar finally stopped soaring on monster Fed rate hikes in late September 2022, the GGR was 1/9th up into that range. A proportional mean-reversion overshoot would ultimately take it back to 8/9ths up in. That would yield an upside target of 0.229x, which is right in line with the GGR highs seen in recent years.

Gold-stock uplegs leveraging gold’s advances drove the GGR to 0.227x in May 2021 and 0.222x in April 2022. So regaining 0.229x in coming months isn’t a stretch at all. At mid-week prevailing gold prices of $1,876, GLD shares are running $174.10. Multiply that by the GGR mean reverting to 0.229x, and that makes for a $39.87 GDX. That’s another 48% higher from mid-week levels, a solid gold-stock run worth riding.

The primary reason gold stocks’ chronic undervaluation will soon end is gold itself powering much higher. Markets’ valuation waves are inexorably linked with their sentiment ones. Sectors only grow overvalued when traders greedily chase them, piling in to ride their upside momentum. So there’s nothing more bullish for gold-stock psychology than gold powering higher, especially when new record highs are in sight.

GDX’s mean-reversion upleg out of last September’s extreme lows has soared 63.9% higher at best in 6.5 months into mid-April 2023. That was driven by gold’s own parallel 26.3% mean-reversion upleg, for average 2.4x gold-stock leverage. That left gold at $2,050 before the US dollar bounced again on more Fed-hawkish economic data, challenging gold’s nominal all-time-record high of $2,062 from August 2020.

Since gold’s latest upleg was born at such crazy extremes a year ago, I’ve long argued it should exceed 40% before giving up its ghost. This gold upleg is already the biggest by far since a pair of monsters that peaked in 2020 at 42.7% and 40.0% gains! Another 40% this time around would leave gold way up near $2,275, and up just 27% it would forge into new record-high territory. That would work wonders for sentiment.

While the mission of trading is buying low then selling high, only hardened contrarian traders attempt that. The vast majority of speculators and investors hate buying low, refusing to even pay attention to sectors when they are out of favor and cheap. Instead they buy high in hopes of selling even higher later, piling into popular sectors to chase their upside momentum. This dynamic will explode as gold hits new record highs.

Traders are fascinated by and attracted to record-breaking surges, which the financial media loves extensively covering greatly amplifying herd greed and interest. We saw this in summer 2020 with gold, spring 2021 with bitcoin, and autumn 2021 with mega-cap technology stocks. You couldn’t turn on CNBC or Bloomberg or read major market websites without wall-to-wall bullish coverage of the record-breaking sector!

While professional traders are aware and should be positioned well before rallies hit record territory, retail traders often aren’t. They usually don’t start paying attention until the financial media ramps up reporting on new record highs. Then they rush to chase that hot sector, and their capital inflows supercharge those strong gains into escalating virtuous circles of buying. Gold-stock fortunes rely heavily on retail traders’ interest.

They pretty much abandoned gold and its miners’ stocks in mid-2022 as the Fed’s extreme rate hikes just crushed them. After that capitulation they largely forgot about this sector and haven’t paid much attention since. So when gold powers decisively over August 2020’s $2,062 nominal peak and the financial media starts breathlessly talking about it, retail traders will get excited. They will really start chasing GLD and GDX.

While gold sentiment has sure felt bearish in recent months, new record territory isn’t that far from here. From its mid-week close, gold would only have to rally another 9.9% to start besting $2,062. That’s not much. After getting forced into a pullback by another dollar rally this year, gold blasted up 13.2% from late February to early May! And in just over a couple weeks from late June to mid-July, gold surged another 3.6%.

Another sharp gold rally soon is virtually guaranteed by speculators’ excessively-bearish positioning in gold futures. Because the US dollar rocketed higher again from mid-July to late September, these hyper-leveraged traders dumped lots of long contracts while radically ramping their short selling. The resulting gold-futures shorting spike is really bullish for gold, as these shorts have to be covered with proportional buying.

That short covering quickly feeds on itself as other traders scramble to buy and close their bearish bets, accelerating gold’s upside. Soon that drives gold high enough for long enough to attract in other long-side speculators commanding much more capital. They pile in to chase gold’s gains too, growing them much larger. Eventually that upside momentum attracts back investors, who vanished during this past year.

Gold could probably surge near nominal-record territory on gold-futures short covering alone, and well above it on gold-futures long buying. The resulting excited and greedy financial-media coverage would bring back traders in droves, forcing gold stocks far higher. Like usual during major gold surges they will really outperform their metal, ending the chronic undervaluation plaguing this sector over this past year.

Again another 40% gold upleg out of September 2022’s extreme secular lows would boost it way up near $2,275. That equates to about $211 per share for GLD. Applying that conservative GDX/GLD Ratio mean reversion of 0.229x to that yields a GDX target near $48.25. That’s another 79% higher from mid-week levels, and would extend this leading major-gold-stock ETF’s total upleg since those deep lows to 121%.

That would make for normal 3.0x upside leverage to gold, and is even smaller than GDX’s 134% gains in mid-2020 during gold’s last 40% upleg. So the left-for-dead gold-stock sector has great upside potential here before retail traders swarm back in. And if the major gold stocks dominating GDX thrive, the smaller fundamentally-superior mid-tiers and juniors we’ve long specialized in at Zeal should trounce GDX’s gains.

The majors fail to overcome depletion at the vast scales they mine, leading to shrinking gold output. Their large market capitalizations have large inertia requiring big capital inflows to move. But the mid-tiers and juniors are often able to consistently grow their production as they bring new expansions and mines online, which investors prize above all else. Their smaller market caps make them much easier to bid higher.

Successful trading demands always staying informed on markets, to understand opportunities as they arise. We can help! For decades we’ve published popular weekly and monthly newsletters focused on contrarian speculation and investment. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks.

Our holistic integrated contrarian approach has proven very successful, and you can reap the benefits for only $8 an issue (now 33% off!). We research gold and silver miners to find cheap fundamentally-superior mid-tiers and juniors with outsized upside potential. Sign up for free e-mail notifications when we publish new content. Even better, subscribe today to our acclaimed newsletters and start growing smarter and richer!

The bottom line is gold stocks’ chronic undervaluations should soon come to an end. Like everything else in the markets, gold-stock price levels relative to gold’s are cyclical. And they have already reversed and resumed trending higher on balance over the past year. This gold-stock outperformance relative to gold should continue, accelerating as gold’s powerful upleg resumes fueled by gold-futures mean-reversion buying.

Big short covering triggering even-bigger long buying ought to be plenty to propel gold up to challenge nominal record highs. New records will rekindle bullish financial-media coverage and traders’ interest, driving big momentum-chasing buying. That will include retail traders necessary to catapult gold stocks into major uplegs, fully mean reverting and overshooting back to overvalued levels relative to gold again.

Adam Hamilton, CPA

September 29, 2023

Copyright 2000 - 2023 Zeal LLC (www.ZealLLC.com)

About the author