With gold starting to run again, the mid-tier and junior gold miners’ stocks in their sector’s sweet spot for upside potential are increasingly surging. Those mounting gains on accelerating upside momentum are attracting back traders. How far these smaller gold stocks can likely rally in coming months partially depends on how they are faring fundamentally. Their latest earnings season recently wrapping up illuminates that.

Gold-stock tiers are defined by their production rates. Small juniors mine less than 300k ounces of gold annually, medium mid-tiers have outputs running from 300k to 1,000k, large majors yield over 1,000k, and huge super-majors operate at vast scales exceeding 2,000k. The mid-tiers offer a unique mix of sizable diversified production, great output-growth potential, and smaller market capitalizations ideal for outsized gains.

Mid-tiers are much less risky than juniors, and amplify gold’s uplegs much more than majors. These mid-tiers are nicely tracked by the GDXJ VanEck Junior Gold Miners ETF. Birthed in November 2009, it now commands $3.7b of net assets making it the second-largest sector ETF after its big-brother GDX. While GDXJ is way superior on multiple fronts, despite its name it is overwhelmingly comprised of mid-tier gold miners.

Like their major brethren, the mid-tiers have had a tough year on the Fed’s most-extreme tightening ever catapulting the US dollar parabolic. Between mid-April to late September, GDXJ collapsed a dreadful 48.8%! That was driven by a parallel 17.9% gold plunge on an epic 14.2% skyrocketing in the US Dollar Index! But that crazy-anomalous Fed dollar/gold shock was ending, as I analyzed a month ago in another essay.

The miserable day I wrote that in early November, gold and GDXJ were still languishing near $1,631 and $28.23. The gold-stock sector had been abandoned and left for dead after a brutal summer. But the Fed’s ability to keep goosing the USDX igniting withering gold-futures selling was waning. Then I argued the Fed’s “federal-funds rate is nearing terminal-level projections, leaving little room for more hawkish surprises.”

And without those forcing the US dollar higher “it is overdue to roll over hard in massive mean-reversion selling. That weaker dollar will fuel huge normalization buying in gold futures, which have been driven to bearish extremes. ... A strengthening gold bull will attract back investors, amplifying its gains as inflation ravages stock markets. The battered gold stocks will soar with gold, winning fortunes for contrarian traders.”

That indeed started to happen between early November into the middle of this week. Gold blasted 8.5% higher in less than a month on the US Dollar Index plunging 6.3%! That launched GDXJ up 26.5% in that short span, with better mid-tiers far outperforming their benchmark. Exiting November, we had unrealized gains in our recent newsletter trades running as high as +66.5%! The gold stocks are off to the races again.

So the legions of ostriching traders who ignored this sector’s incredible buy-low opportunities in recent months need to start paying attention. While the mid-tiers’ and juniors’ stock-price gains are accelerating, they remain small if a major gold upleg is getting underway. GDXJ skyrocketed 188.9% higher in just 4.8 months out of March 2020’s pandemic-lockdown stock panic, and GDXJ was just bashed back to those levels!

With massive upside potential as gold mean reverts higher, the mid-tiers’ and juniors’ fundamentals are important. For 26 quarters in a row now, I’ve painstakingly analyzed the latest operational and financial results reported by GDXJ’s 25 largest miners. They accounted for 65.1% of this ETF’s total weighting as of mid-November when Q3 earnings season ended, the lion’s share of GDXJ’s sprawling 101 component stocks.

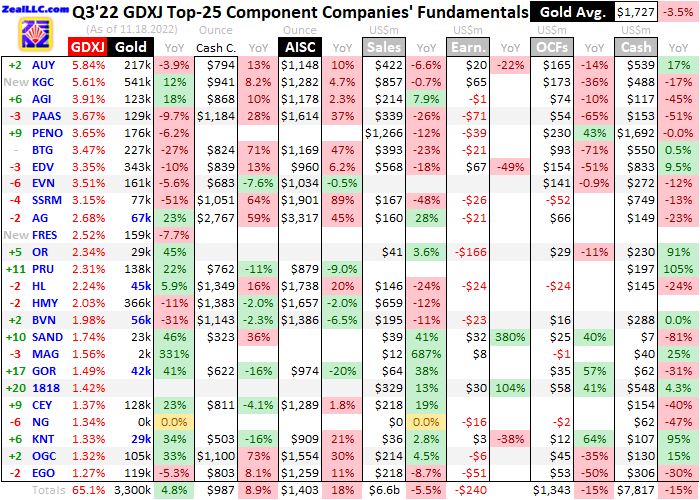

This table summarizes the operational and financial highlights from the GDXJ top 25 in Q3’22. These gold miners’ stock symbols aren’t all US listings, and are preceded by their rankings changes within GDXJ over this past year. The shuffling in their ETF weightings reflects shifting market caps, which reveal both outperformers and underperformers since Q3’21. Those symbols are followed by their current GDXJ weightings.

Next comes these gold miners’ Q3’22 production in ounces, along with their year-over-year changes from the comparable Q3’21. Output is the lifeblood of this industry, with investors generally prizing production growth above everything else. After are the costs of wresting that gold from the bowels of the earth in per-ounce terms, both cash costs and all-in sustaining costs. The latter help illuminate miners’ profitability.

That’s followed by a bunch of hard accounting data reported to securities regulators, quarterly revenues, earnings, operating cash flows, and resulting cash treasuries. Blank data fields mean companies hadn’t reported that particular data as of mid-November. The annual changes aren’t included if they would be misleading, like comparing negative numbers or data shifting from positive to negative or vice versa.

The elite mid-tier and junior gold miners filling GDXJ’s upper ranks reported another challenging quarter. Adjusted for a big GDXJ composition change, their gold production generally declined. And their mining costs collectively surged on output problems at individual mines and raging inflation. Nevertheless, these smaller gold miners remain well-positioned to continuing multiplying gold’s gains at it mean reverts way higher.

Marketed to investors as a “Junior Gold Miners ETF”, GDXJ certainly shouldn’t have any super-majors in its ranks! They belong in this same ETF manager’s larger GDX ETF. But inexplicably over this past year, GDXJ’s custodians readded super-major Kinross Gold. It had been a past top GDXJ component, but got rightfully booted in Q4’20. In 2022 KGC expects to produce near a colossal 2,000k gold-equivalent ounces!

For years I’ve railed against majors and super-majors tainting GDXJ’s mission and effectiveness. There’s no reason all miners producing over 250k ounces per quarter can’t be exclusively included in GDX. With 100+ component stocks, GDXJ has plenty of other holdings to boost weightings on that far better reflect smaller mid-tier and junior gold miners. Forcing Kinross back in contrary to GDXJ’s specialty is really distorting.

Last quarter the GDXJ-top-25 gold stocks mined 3,300k ounces of gold which climbed a solid 4.8% year-over-year. Yet excluding KGC’s enormous 541k Q3’22 output since it wasn’t a GDXJ component a year earlier in Q3’21 paints a way-different picture. That slashes last quarter’s collective production to 2,759k ounces, plunging 12.4% YoY! That was much worse than the GDX-top-25 majors’ 4.1% YoY decline in Q3.

Yet GDXJ’s sequential production growth from Q2’22 really outperformed, rocketing up 13.3% quarter-on-quarter! Kinross isn’t a factor here, since it was added back in before that prior quarter. The GDX top 25 which I analyzed a couple weeks ago saw their Q3 aggregate production plunge by 3.9% sequentially from Q2. That was damning because global gold-mining output usually surges dramatically from Q2s to Q3s.

The World Gold Council tracks all that global gold supply-and-demand data in its fantastic quarterly Gold Demand Trends reports. In Q3’22 total world mine production surged a strong 6.5% QoQ. That’s actually par for the course according to the WGC. During the entire decade ending 2021, on average Q1s, Q2s, Q3s, and Q4s saw sequential QoQ world gold production running -8.5%, +4.1%, +7.0%, and +0.7%!

So the mid-tiers and juniors of GDXJ clocking in with outstanding 13.3% QoQ gold production growth are far outperforming their larger major peers. That’s the primary attribute of smaller gold miners that makes them more attractive than larger ones. Operating at smaller scales, it is far easier for mid-tiers and juniors to consistently grow their gold output on balance compared to majors which usually fail to overcome depletion.

These sweet-spot-for-upside-potential mid-tiers and juniors usually only operate a few mines at most, so occasional expansions and relatively-affordable mid-sized mine-builds really boost their outputs. That helps them overcome depletion to generally grow their production over time. Meanwhile most of the majors have struggled with shrinking production for years, unable to find enough gold and buy enough mines.

The smaller gold miners’ second big advantage over larger ones is their lower market capitalizations. In mid-November right after Q3 earnings season, these top 25 GDXJ components averaged market caps of $2,890m. That was just 30% of the average market caps of the GDX-top-25 majors, and that is skewed high by the majors wrongly included in GDXJ. This smaller-miner ETF is mostly a subset of that larger one.

I’ve long argued GDX and GDXJ inclusion should be mutually exclusive, greatly increasing these ETFs’ utility to investors. Since the same company manages both, that should be easy to do. Yet 14 of these GDXJ-top-25 stocks are also GDX-top-25 ones, and fully 21 are also GDX components! The GDXJ top 25 were clustered between the 12th to 34th rankings in GDX, totaling 26.4% of it compared to 65.1% of GDXJ.

Yet despite that big overlap, the larger majors and super-majors GDXJ excludes are mostly dead-weight in GDX. Its top 11 majors accounted for a whopping 66.8% of its weighting exiting Q3’s earnings season, and averaged huge market caps of $17,647m! So despite the commingling of GDX and GDXJ holdings, the latter ETF is much better weighting fundamentally-superior mid-tier and junior gold miners much more highly.

Cost inflation was extensive in the GDX-top-25 majors’ Q3’22 results. Not surprisingly mid-tiers suffered these same pressures. In normal times, unit gold-mining costs are generally inversely-proportional to gold-production levels. That’s because gold mines’ total operating costs are largely fixed during pre-construction planning stages, when designed throughputs are determined for plants processing gold-bearing ores.

Their nameplate capacities don’t change quarter to quarter, requiring similar levels of infrastructure, equipment, and employees to keep running at full-speed. So the only real variable driving quarterly gold production is the ore grades fed into these plants. Those vary widely even within individual gold deposits. Richer ores yield more ounces to spread mining’s big fixed costs across, lowering unit costs and boosting profitability.

But while fixed costs are the lion’s share for gold mining, it also demands sizable variable costs. Energy is the biggest category, including electricity to power ore-processing plants like mills and diesel fuel to run excavators and dump trucks hauling raw ores to those facilities. Other smaller consumables range from explosives to blast out ores to chemical reagents necessary to process various ores to recover their gold.

The GDXJ top 25’s generally-lower outputs would’ve driven their costs higher last quarter regardless of consumables prices. Less ores processed through mills or lower-grade ores both reduce gold ounces produced, forcing each to bear more fixed costs. But these elite mid-tier gold miners were also paying more for variable-cost consumables. That proved a common theme through the majority of their quarterlies.

Pan American Silver’s Q3’22 Management Discussion and Analysis was a representative example of this challenge. PAAS’s management warned that “During Q3 2022, all operations were negatively impacted by inflationary pressures, mainly reflecting increased prices for diesel and certain consumables, including cyanide, explosives, and steel products (such as grinding media), as well as supply-chain shortages.”

That continued “We are also experiencing indirect cost increases in other supplies and services due to the inflationary impact of diesel and consumable prices on third-party suppliers.” And B2Gold advised “The Company’s operations continue to be impacted by global cost inflation with fuel costs reflecting the most significant increases.” Diesel prices skyrocketed in the middle of this year, more than doubling in the US!

Cash costs are the classic measure of gold-mining costs, including all cash expenses necessary to mine each ounce of gold. But they are misleading as a true cost measure, excluding the big capital needed to explore for gold deposits and build mines. So cash costs are best viewed as survivability acid-test levels for mid-tier gold miners. They illuminate the minimum gold prices necessary to keep the mines running.

In Q3’22 these GDXJ-top-25 mid-tiers reporting cash costs averaged a record $987 per ounce, surging 8.9% YoY! While that is far below prevailing gold prices, it is concerning. Thankfully a couple extreme outliers skewed this average way higher. Excluding the lofty cash costs reported by SSR Mining and First Majestic Silver, the rest of these miners averaged a way-better $878 which would’ve retreated 3.0% YoY.

SSRM suffered a horrendous Q3, seeing its total gold production crash 51.5% YoY which was far worse than any of its peers! That was because operations were temporarily suspended at its primary gold mine in Turkey. In late June, a small cyanide leak was discovered from a pipe running to its leach pad. That was quickly cleaned and fixed, but local regulators didn’t authorize mining to resume until late September.

That mine being offline for a quarter catapulted SSR Mining’s cash costs up 64.5% YoY to $1,051. They will collapse back to inflation-adjusted norms in coming quarters with that mine running. Even worse were First Majestic Silver’s insane $2,767 cash costs which soared 59.5% YoY! That company operates three primary silver mines that are thriving, and a fourth small gold one yielding under a quarter of AG’s gold in Q3.

That problematic mine has been plagued with sky-high costs ever since AG bought it, and they continue to worsen despite much guidance to the contrary. The three-fourths of First Majestic’s gold production coming from its silver mines is considered a byproduct, so reported cash costs are only for that little gold mine’s 16k ounces in Q3. That rounding error of a sliver of GDXJ-top-25 output shouldn’t unduly taint the whole.

Thanks to these same extreme outliers, the GDXJ top 25’s average all-in sustaining costs blasted 17.7% higher YoY to a record $1,403 per ounce in Q3’22! Interestingly that was right in line with the GDX-top-25 majors’ $1,391. GDX also includes SSRM and AG, so they heavily distorted its average costs as well. They reported extreme AISCs skyrocketing 89.0% YoY to $1,901 and 45.1% YoY to a dumbfounding $3,317!

Exclude them, and the rest of these elite mid-tier and junior gold miners averaged far better AISCs of just $1,252 per ounce last quarter. That would’ve merely been up 5.0% YoY, really impressive with inflation raging worldwide! That is also right in line with the GDX majors’ average of $1,239 excluding SSRM and AG. Both companies expect their AISCs to plunge, forecasting full-year 2022’s running $1,330 and $1,800.

But even GDXJ’s adjusted $1,252 is still really high, and high AISCs cut into profit margins. A great proxy for sector unit profits is calculated by subtracting mid-tiers’ quarterly-average AISCs of $1,403 from the quarterly-average gold prices. Those ran $1,727 in Q3’22, slumping a slight 3.5% YoY. That implies the GDXJ top 25 earned $324 per ounce of gold produced last quarter, which collapsed a massive 45.8% YoY!

These elite mid-tier and junior gold miners haven’t earned so little in any quarter since Q4’18. During the couple years leading into Q3’22, those quarterly implied unit profits averaged a hefty $681! But Q3’s unit earnings are also heavily distorted by those anomalous costs at SSR Mining and First Majestic Silver. If they are excluded the rest of the GDXJ top 25 earned a much-more-reasonable $475 per ounce last quarter.

And that ought to really improve going forward. The majority of these elite smaller gold miners still have 2022 AISC guidance lower than their Q3’22 actuals. While those again averaged $1,403, the average full-year forecasts were much lower averaging $1,232. And to drag down 2022’s four-quarter averages so much, this current Q4 needs to see way better AISCs. Many of the GDXJ top 25 predicted much-lower ones.

Gold is faring better too, again soaring $138 higher in less than a month since early November! With this exceedingly-hawkish Fed out of room to keep surprising markets after such uber-aggressive tightening, gold is mean reverting out of this year’s extreme anomaly. While gold is only averaging $1,697 quarter-to-date in Q4, that should improve considerably as gold continues powering higher on the weakening US dollar.

Assume gold averages around $1,725 this quarter and GDXJ-top-25 Q4 average AISCs plunge near $1,175 on better production, and mid-tiers’ implied unit profits could nearly double back up to $550 per ounce! While predicting a precise target is impossible, all signs are pointing to much-better profitability in Q4 than Q3. Last quarter had a lot of individual-mine challenges that these companies said are being resolved.

These elite gold miners’ hard accounting data reported to securities regulators under Generally Accepted Accounting Principles or other countries’ equivalents also reflected Q3’22’s trials. Even including Kinross, the GDXJ top 25’s total revenues still fell 5.5% YoY to $6,555m. That reflects generally lower gold output excluding KGC, which again fell 12.4% YoY. Those lower average gold prices certainly didn’t help either.

The mid-tiers’ and juniors’ actual accounting profits looked far worse, plummeting from $212m a year earlier to a $240m loss in Q3’22! But these weak earnings were skewed by unusual one-time losses that were flushed through income statements. An example is Osisko Gold Royalties’ big $108m non-cash loss in Q3’22, on no longer consolidating its former mine-development division in its corporate financial statements.

Cash flows generated from operations were also weak even with Kinross’s addition, falling 14.6% YoY to $1,343m. That’s still consistent with lower production and softer gold prices though. Finally the GDXJ top 25’s aggregate cash treasuries fell a similar 15.0% YoY to $7,817m. That’s above midway between the 26-quarter range running from $3,576m to $10,144m, leaving these smaller gold miners with plenty of cash.

They’ll probably continue using it to expand their existing gold mines and develop new ones, growing their production on balance. Some of these mid-tiers have new mine-builds that are going live in coming quarters. They are projected to operate at much lower all-in sustaining costs than existing mines, which will drag down companies’ overall costs. The fundamentally-superior mid-tiers and juniors have huge upside potential!

If you regularly enjoy my essays, please support our hard work! For decades we’ve published popular weekly and monthly newsletters focused on contrarian speculation and investment. These essays wouldn’t exist without that revenue. Our newsletters draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks.

That holistic integrated contrarian approach has proven very successful, yielding massive realized gains during gold uplegs like this overdue next major one. We extensively research gold and silver miners to find cheap fundamentally-superior mid-tiers and juniors with outsized upside potential as gold powers higher. Our trading books are full of them already starting to soar. Subscribe today and get smarter and richer!

The bottom line is the mid-tier and junior gold miners reported a challenging Q3. They generally suffered lower production on individual-mine problems, which combined with inflationary pressures to force mining costs to record highs. Yet these companies are reporting those issues are largely resolved, paving the way for better output and lower costs during this current Q4. That should really boost mid-tiers’ profitability.

And their earnings should be further supercharged by gold itself mean reverting way higher. Big gold-futures buying is fueling a growing gold upleg as the Fed-goosed US dollar rolls over hard. Gold’s strong upside momentum is attracting back traders and rekindling bullish sentiment. That will drive increasing interest in the fundamentally-superior smaller gold-mining stocks, which really amplify gold’s gains during uplegs.

Adam Hamilton, CPA

December 2, 2022

Copyright 2000 - 2022 Zeal LLC (www.ZealLLC.com)

About the author